Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

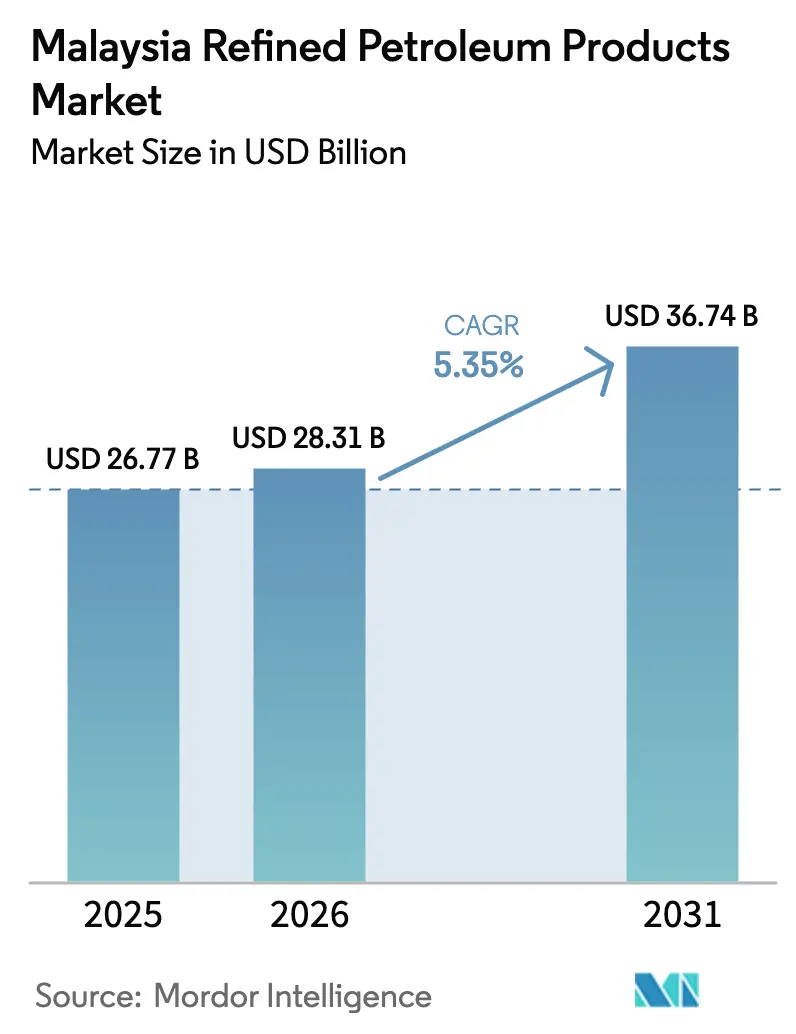

| Base Year Market Size (2025) | USD 26.77 Billion |

| Market Size (2026) | USD 28.31 Billion |

| Market Size (2031) | USD 36.74 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Refined Petroleum Products Market Analysis by Mordor Intelligence

The Malaysia Refined Petroleum Products Market size is expected to grow from USD 26.77 billion in 2025 to USD 28.31 billion in 2026 and is forecast to reach USD 36.74 billion by 2031 at 5.35% CAGR over 2026-2031.

This market size underscores Malaysia’s status as Southeast Asia’s key refining and bunker-supply node, yet policy pressure that favors Euro 5 fuels and bio-blends is reshaping product slates. Petrol retained volume leadership in 2025, but aviation fuel is rising fastest as airlines restore capacity and a 650,000-tonne-per-year sustainable aviation fuel (SAF) plant comes onstream at Pengerang. Low-sulfur grades already account for more than half of the pool, reflecting the April 2021 Euro 5 diesel mandate and the September 2025 Euro 5 petrol rollout. Domestic refineries deliver two-thirds of the overall supply, even while periodic imports from Singapore and North Asia balance outages. Retail fuel stations still dominate distribution, but online and automated delivery applications such as Setel are expanding briskly. Transportation stands as the largest consuming sector, whereas marine bunkering is registering the sharpest growth as Port Klang and Pengerang challenge Singapore’s scale.

Key Report Takeaways

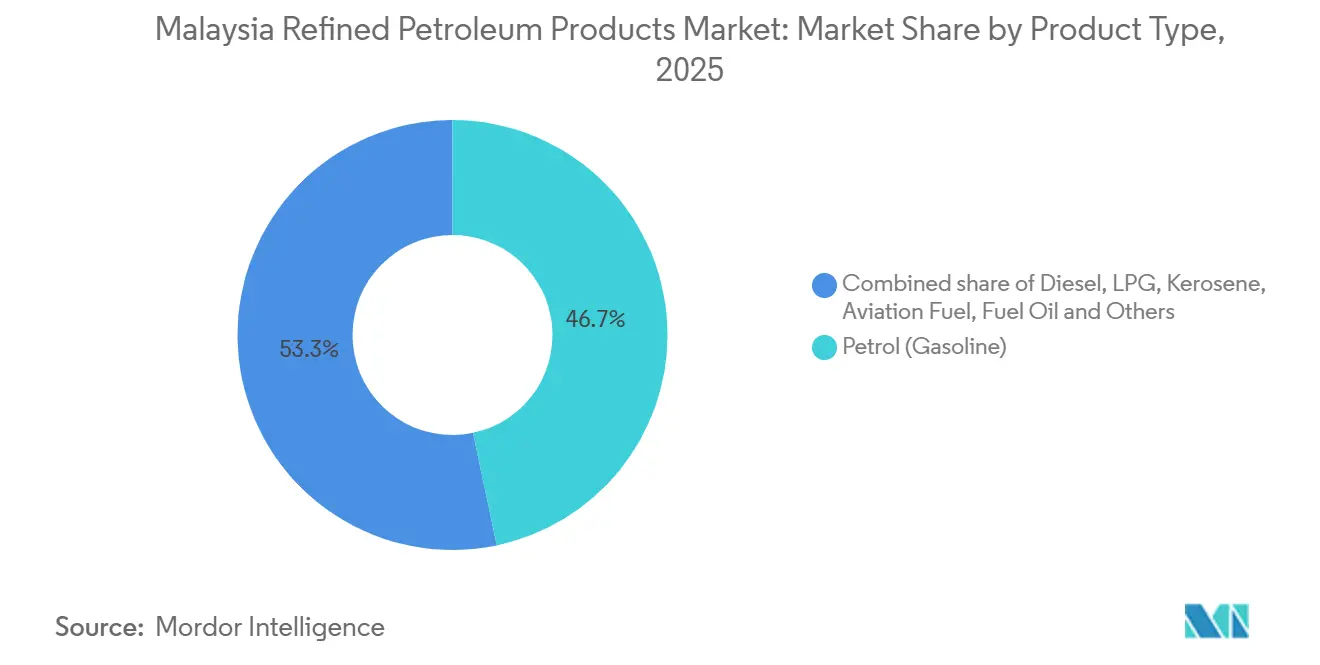

- By product type, petrol held 46.7% of Malaysia's refined petroleum products market share in 2025, and aviation fuel is forecast to expand at a 7.5% CAGR to 2031.

- By sulfur content, low-sulfur fuels captured a 55.1% share of the Malaysia refined petroleum products market size in 2025 and are advancing at a 5.9% CAGR through 2031.

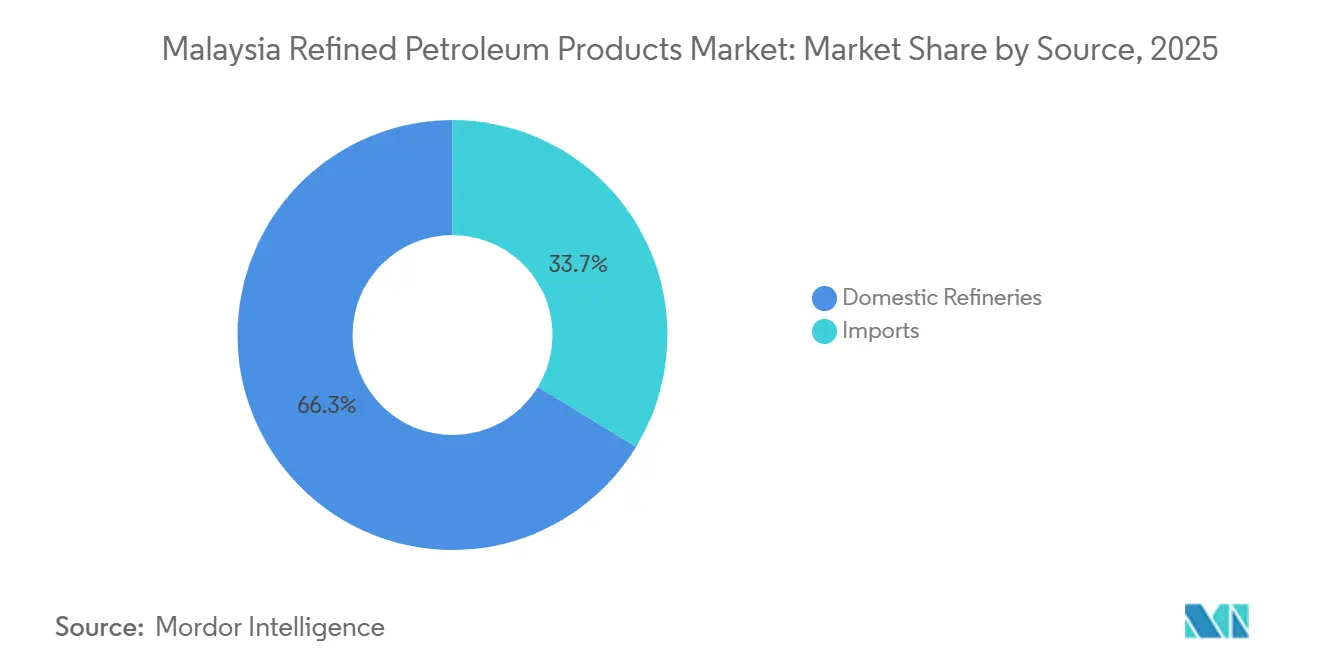

- By source, domestic refineries supplied 66.3% of demand in 2025, while imports posted a 4.6% CAGR to 2031 as seasonal balancing cargoes persisted.

- By distribution channel, retail fuel stations commanded 60.5% volume in 2025; online and automated delivery is growing at 9.7% CAGR to 2031.

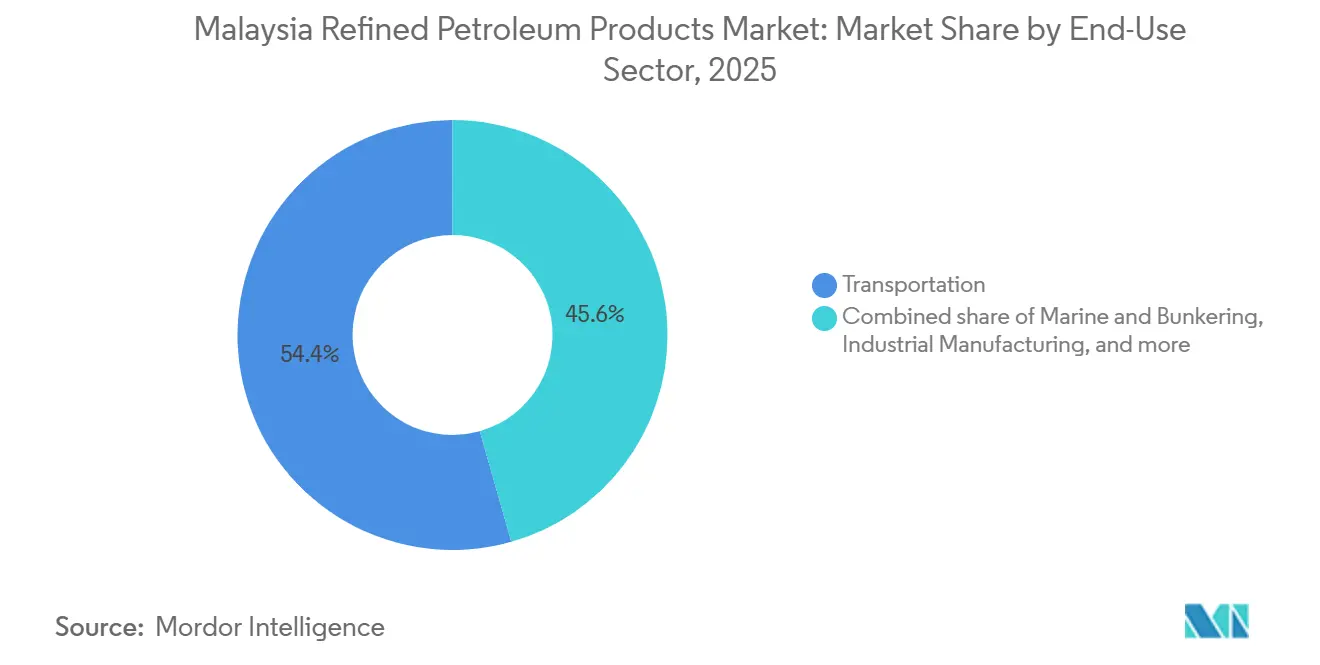

- By end-use sector, transportation absorbed 54.4% of demand in 2025; marine and bunkering are expanding at a 10.1% CAGR through 2031.

- Peninsular Malaysia represented more than 60% of the Malaysia refined petroleum products market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Refined Petroleum Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in domestic transportation fuel demand | 1.2% | Peninsular Malaysia (Selangor, Kuala Lumpur, Johor), spillover to Sabah and Sarawak | Medium term (2-4 years) |

| Expansion of petrochemical downstream integration | 0.8% | Johor (Pengerang), Melaka, potential expansion in Sarawak (Bintulu) | Long term (≥ 4 years) |

| Government incentives for bunker fuel hub development | 1.0% | Johor (Pengerang, Port of Tanjung Pelepas), Selangor (Port Klang) | Medium term (2-4 years) |

| Bio-refinery investments for Sustainable Aviation Fuel | 0.6% | Johor (Pengerang), national aviation sector impact | Long term (≥ 4 years) |

| Strategic stockpiling policies enhancing refinery utilization | 0.5% | National, with primary storage expansion in Johor (Pengerang, Tanjung Langsat) | Medium term (2-4 years) |

| Regional supply-chain shifts due to shipping lane realignments | 0.4% | Malacca Strait corridor, Johor (Pengerang), Selangor (Port Klang) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Domestic Transportation Fuel Demand

Malaysia added 799,731 vehicles in 2023, with passenger cars dominating registrations and cementing a robust gasoline and diesel requirement despite fewer than 20,000 cumulative electric vehicles by 2024.[1]Road Transport Department Malaysia, “Vehicle Registration Statistics 2023,” JPJ, jpj.gov.my Subsidized RON95 pricing at MYR 1.99 per liter shields household budgets, yet mid-2025 subsidy retargeting moves higher-income drivers toward RON97, sustaining overall throughput. Fuel retailers are cushioning thin margins through Setel’s DuitNow QR and Touch ’n Go e-wallet integration, which streamlines forecourt payments for nine million users. Long-haul trucking between Peninsular hubs and East Malaysian states depends on diesel, insulating demand from localized EV adoption concentrated in Klang Valley urban centers.[2]Ministry of Finance Malaysia, “Budget 2025 and Carbon Tax Announcement,” MOF, mof.gov.my

Expansion of Petrochemical Downstream Integration

The Pengerang Integrated Complex couples 300,000 bpd of refining with 3.3 million tpy of petrochemical capacity, allowing PETRONAS to swing output between fuels and higher-margin olefins.[3]PETRONAS, “Annual Report 2024,” PETRONAS, petronas.com Hengyuan is studying a similar naphtha-to-olefins retrofit at Port Dickson but must lock in feedstock and financing before proceeding. Integrated assets position Malaysia to ship polymer precursors to Vietnam and Indonesia, which imported more than 1.5 million t of Malaysian chemicals in 2024. Dialog Group’s storage farms at Pengerang provide blending and staging flexibility that minimizes vessel waiting time.[4]Dialog Group, “Annual Report 2024,” Dialog Group, dialoggroup.com.my

Government Incentives for Bunker Fuel Hub Development

Putrajaya introduced tax holidays on bunker fuel and funded floating-storage upgrades to lure some of the 94,000 annual Malacca Strait transits that now refuel in Singapore. Dialog’s additional 150,000 m³ of tankage at Tanjung Langsat will be ready by FY 2027 and is earmarked largely for marine fuels. PETRONAS Marine already supplies very-low-sulfur, ultra-low-sulfur, high-sulfur, bio-blend, and LNG bunkers, letting operators hedge among compliance options.

Bio-Refinery Investments for Sustainable Aviation Fuel

PETRONAS, Enilive, and Euglena reached a final investment decision on a 650,000-tpy SAF and hydrotreated vegetable-oil unit that will start commercial operations in H2 2028. Feedstock is palm-oil-mill effluent and used cooking oil, converting a waste stream into jet fuel that sells at up to five times the conventional price. The Malaysian Aviation Commission will rebate landing fees for flights fueled with local SAF, creating a demand pull that de-risks the plant’s offtake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV adoption and fuel efficiency improvements | -0.3% | Selangor, Kuala Lumpur, early spillover to Penang and Johor Bahru | Medium term (2-4 years) |

| Carbon taxation and removal of fuel subsidies | -0.5% | National, with acute impact in Peninsular Malaysia (diesel, RON95 gasoline) | Short term (≤ 2 years) |

| Volatility in crude import differentials affecting refinery margins | -0.4% | National refining sector, particularly independent refiners (Hengyuan, Petron Malaysia) | Short term (≤ 2 years) |

| Tightening marine fuel sulfur regulations compressing HSFO demand | -0.3% | Johor (Pengerang bunkering hub), Selangor (Port Klang), national marine sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Adoption and Fuel Efficiency Improvements

Charging points increased from 1,500 in 2023 to 3,354 by October 2024, and the target is 10,000 by the end of 2025. Even so, range anxiety outside Selangor and Kuala Lumpur slows uptake. Deloitte finds that 58% of consumers still prefer internal combustion vehicles, given the MYR 42,000–60,000 entry price versus MYR 124,000-plus for EVs. Fuel-efficiency standards that push automakers toward hybrids will trim per-vehicle consumption by 20-30% over a decade.

Carbon Taxation and Removal of Fuel Subsidies

Malaysia will introduce a carbon tax in 2026, expected at USD 5–10 per tonne of CO₂, following the June 2024 diesel subsidy removal that lifted pump prices 40% in Peninsular Malaysia. RON95 subsidy retargeting in mid-2025 exempts the top income decile, saving MYR 50 billion in annual outlays but exposing refiners and retailers to margin squeeze. Exporters must also prepare for the EU Carbon Border Adjustment Mechanism, which will penalize high-carbon fuels landing in Europe from 2026 onward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aviation Fuel Outpaces Gasoline Volume Leadership

Petrol retained 46.7% of the Malaysia refined petroleum products market share in 2025, powered by 719,160 passenger-vehicle additions in the prior year. Aviation fuel is poised for a 7.5% CAGR as passenger traffic rebounds toward 112.9 million journeys and as local SAF supply ramps from 2028. Diesel remains essential for a commercial fleet that burned 7.9 billion liters on roads in 2025. LPG dominates household cooking, while kerosene shrinks with near-universal electrification. Fuel oil demand hinges on scrubber-equipped ships and industrial boilers; high-sulfur grades persist in the bunker segment. Naphtha supports PETRONAS RAPID's 3.3 million tpy cracker, generating a higher downstream margin than gasoline blending.

This segment will continue to pivot toward jet and marine grades as air travel and shipping expand, whereas gasoline growth moderates under efficiency norms. Aviation fuel will therefore raise its slice of Malaysia's refined petroleum products market by 2031, even as petrol maintains absolute volume dominance.

By Sulfur Content: Low-Sulfur Mandates Reshape Refinery Yields

Low-sulfur fuels captured 55.1% of Malaysia's refined petroleum products market share in 2025 after Euro 5 diesel took effect in 2021 and Euro 5 petrol followed in 2025. The category should post a 5.9% CAGR, aided by SAF blending that inherently meets ultra-low-sulfur thresholds. High-sulfur fuels hold the remaining 44.9% share, buoyed by power plants and scrubber-equipped vessels yet capped at 4.6% CAGR as compliance costs rise.

Domestic refiners have invested in hydrotreaters to meet the 10 ppm ceiling, with PETRONAS Melaka spending MYR 1.2 billion in 2020 and Hengyuan operating a hydrocracker that can hit Euro 5 specs when feedstock availability allows. The shift secures regional arbitrage opportunities, since Singaporean and Thai refiners already supply Euro 5 blends, but it also raises hydrogen demand and operating costs.

By Source: Domestic Refineries Anchor Supply Amid Import Arbitrage

Domestic refineries delivered 66.3% of output in 2025 and will grow at a 5.8% CAGR as turnarounds abate, and new hydrotreating units run at high utilization. Malaysia's refined petroleum products market size, attributed to imports, will remain material because Q2 2025 alone saw USD 4.7 billion in incoming cargoes, mostly from Singapore, South Korea, and China.

While Malaysia exported USD 4.9 billion in products the same quarter, the net trade balance can swing quickly when unplanned downtime hits. Dialog Group's additional 150,000 m³ of storage by FY 2027 will strengthen buffer capacity and support a strategic-reserve target of 90 days' cover by 2028.

By Distribution Channel: Automated Delivery Disrupts Retail Dominance

Retail forecourts handled 60.5% of sales in 2025 but face margin compression from subsidy roll-backs. Setel’s mobile ordering and QR payment features have raised forecourt throughput and user stickiness, helping participating stations recover 3–4 percentage points of lost margin. Online and automated refueling shows a 9.7% CAGR as fleet operators favor time savings over loyalty points.

Commercial bulk and direct contracts remain critical for airlines, shippers, and power utilities that negotiate formula-linked diesel, marine gas oil, and SAF supply. The Malaysia refined petroleum products market will increasingly blur channel lines as retail sites add EV chargers under a streamlined 87-day permitting process that cuts retrofit cost to MYR 56,700.

By End-Use Sector: Marine Bunkering Surges as Transport Plateaus

Transportation accounted for 54.4% of 2025 demand but will flatten toward 2031 as efficiency gains offset vehicle growth. Marine bunkering stands out with a 10.1% CAGR as Malaysia offers tax-exempt fuels and competitive pricing to divert traffic from Singapore.

Industrial, power, petrochemical, residential, and agricultural segments each have niche drivers. Pan-Borneo Highway construction sustains bitumen and diesel demand, while RAPID’s naphtha cracker secures feedstock from its adjacent refinery. Tenaga Nasional reduces fuel oil burn as natural gas capacity rises, trimming a traditionally price-sensitive slice of the Malaysia refined petroleum products market.

Geography Analysis

Peninsular Malaysia houses four refineries totaling more than 700,000 bpd, supplies over 60% of national consumption, and concentrates the majority of the 3,354 EV charging stations reported in October 2024. Diesel subsidy removal in June 2024 raised logistics costs but accelerated the adoption of aerodynamic kits and route-optimization software among haulers. Selangor and Kuala Lumpur lead early electrification, so that gasoline erosion will occur first in these corridors.

Johor’s Pengerang hub is evolving into a dual-energy node where conventional crude runs alongside renewable feedstock conversion. Dialog’s 5.1 million m³ storage, much of it connected to RAPID, supports both endeavors. The state benefits from port infrastructure and preferential tax schemes that aim to build a bunker-fuel ecosystem capable of challenging Singapore on price and product breadth.

East Malaysia lacks major refinery capacity and continues to receive fuel via coastal tankers or imports routed through Singapore. Diesel subsidies remain intact in Sabah and Sarawak at MYR 2.15 per liter, buffering plantation and mining operations. PETROS is evaluating a 150,000 bpd Bintulu refinery to cut import reliance, but no final decision has been reached. Ongoing Pan-Borneo Highway work keeps bitumen flows robust, and LNG shipments from Bintulu spur local demand for marine gas oil bunkering.

Competitive Landscape

Top Companies in Malaysia Refined Petroleum Products Market

PETRONAS integrates upstream production, three large refineries, petrochemical assets, and more than 1,000 stations, granting scale that competitors cannot match. Independent refiners Hengyuan and Petron Malaysia rely on merchant margins tied to Singapore crack spreads, which averaged USD 8.11 per barrel for gasoline and USD 15.53 for diesel in 2024, leaving thin buffers for maintenance shocks.

Strategic themes include petrochemical integration, renewable feedstock processing, and digital engagement. PETRONAS secured SAF leadership via the Pengerang biorefinery, while Dialog is locking in long-term take-or-pay storage contracts. Setel’s nine-million-strong platform adds value through loyalty bundling, EV charging, and roadside services, transforming traditional fuel retail into a mobility ecosystem.

Barriers to entry revolve around hydrotreating capital, carbon reporting capability, and logistics footprint. The upcoming 2026 carbon tax forces refiners to model capture options or absorb additional costs. Meanwhile, adherence to IMO lifecycle assessment rules favors suppliers with transparent feedstock chains, a niche where PETRONAS leverages its palm-oil-mill-effluent sourcing advantage. Overall, the competitive field is consolidating around players able to fund low-carbon upgrades and multichannel customer interfaces.

Malaysia Refined Petroleum Products Industry Leaders

Chevron Corporation

Petroliam Nasional Berhad

Shell PLC

FIVE Petroleum Malaysia Sdn Bhd

Petron Malaysia Refining & Marketing Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Malaysia’s Pengerang Refining & Petrochemical (Prefchem) resumed operations at key gasoline production units after a significant halt for repairs. Refining activity is gradually recovering, with output and run rates still below optimal levels. The restart highlights ongoing operational challenges at Malaysia’s largest refinery complex.

- September 2025: Malaysia’s refined product output fell by approximately 12.6% in July to 886,000 bpd, despite increases in gasoline and diesel production. The decline was driven by changes in refinery product mixes, with fuel oil production dropping significantly due to weaker margins and reduced shipping activity impacting refined product flows.

- May 2025: Indonesia’s plan to reduce refined fuel imports from Singapore may affect Malaysian export opportunities, altering regional refining trade dynamics. By increasing independent sourcing of crude and processed fuels, Indonesia aims to enhance energy security and reduce foreign exchange losses, potentially impacting Malaysia’s refined product market share.

- May 2025: Malaysia’s Pengerang Integrated Refinery & Petrochemical complex restarted previously offline units, addressing reduced gasoline output. The restart follows a significant production slowdown that affected crude throughput and domestic refined fuel availability, emphasizing the refinery’s critical role in Malaysia’s downstream petroleum sector.

Malaysia Refined Petroleum Products Market Report Scope

Refined petroleum products are produced in a refinery. They are derived from crude oil through processes such as catalytic cracking and fractional distillation.

The Malaysia refined petroleum products market report is segmented by product type, sulfur content, source, distribution channel, end-use sector, and geography. By product type, the market is segmented into petrol, diesel, LPG, aviation fuel, fuel oil, and others. By Sulfur content, the market is divided into low-sulfur, high-sulfur. By source, the market is divided into domestic refineries, imports. By distribution channel, the market is segregated into retail, commercial, direct, and online/automated. The end-use sector, the market is divided into transportation, marine, industrial, petrochemicals, and others. For each segment, the market sizing and forecasts are done based on revenue (USD).

By Product Type

| Petrol (Gasoline) |

| Diesel |

| LPG |

| Kerosene |

| Aviation Fuel |

| Fuel Oil (HSFO, VLSFO) |

| Others (Bitumen, Naphtha) |

By Sulfur Content

| Low-Sulfur (Up to 10 ppm) |

| High-Sulfur (Above 10 ppm) |

By Source

| Domestic Refineries |

| Imports |

By Distribution Channel

| Retail Fuel Stations |

| Commercial Bulk Sales |

| Direct Supply Contracts |

| Online/Automated Fuel Delivery |

By End-Use Sector

| Transportation |

| Power Generation |

| Industrial Manufacturing |

| Petrochemicals |

| Residential and Commercial |

| Marine and Bunkering |

| Agriculture and Mining |

| By Product Type | Petrol (Gasoline) |

| Diesel | |

| LPG | |

| Kerosene | |

| Aviation Fuel | |

| Fuel Oil (HSFO, VLSFO) | |

| Others (Bitumen, Naphtha) | |

| By Sulfur Content | Low-Sulfur (Up to 10 ppm) |

| High-Sulfur (Above 10 ppm) | |

| By Source | Domestic Refineries |

| Imports | |

| By Distribution Channel | Retail Fuel Stations |

| Commercial Bulk Sales | |

| Direct Supply Contracts | |

| Online/Automated Fuel Delivery | |

| By End-Use Sector | Transportation |

| Power Generation | |

| Industrial Manufacturing | |

| Petrochemicals | |

| Residential and Commercial | |

| Marine and Bunkering | |

| Agriculture and Mining |

Key Questions Answered in the Report

How big is the Malaysia refined petroleum products market in 2026?

The market is valued at USD 28.31 billion for 2026, continuing its 5.35% CAGR toward USD 36.74 billion in 2031.

Which product category is expanding fastest?

Aviation fuel is projected to post a 7.5% CAGR through 2031, outpacing all other refined products.

What share of supply comes from domestic refineries?

Domestic plants provided 66.3% of national demand in 2025 and are expected to edge higher as utilization improves.

How will the 2026 carbon tax affect refiners?

A levy of USD 5-10 per tonne of CO2 will squeeze margins unless refiners invest in capture technology or low-carbon fuels.

Which distribution channel is growing quickest?

Online and automated fuel delivery, led by Setel, is registering a 9.7% CAGR to 2031.

Where is the SAF biorefinery located?

The 650,000-tonne-per-year SAF and HVO facility is under construction at the Pengerang Integrated Complex in Johor.

Page last updated on: