Malaysia Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

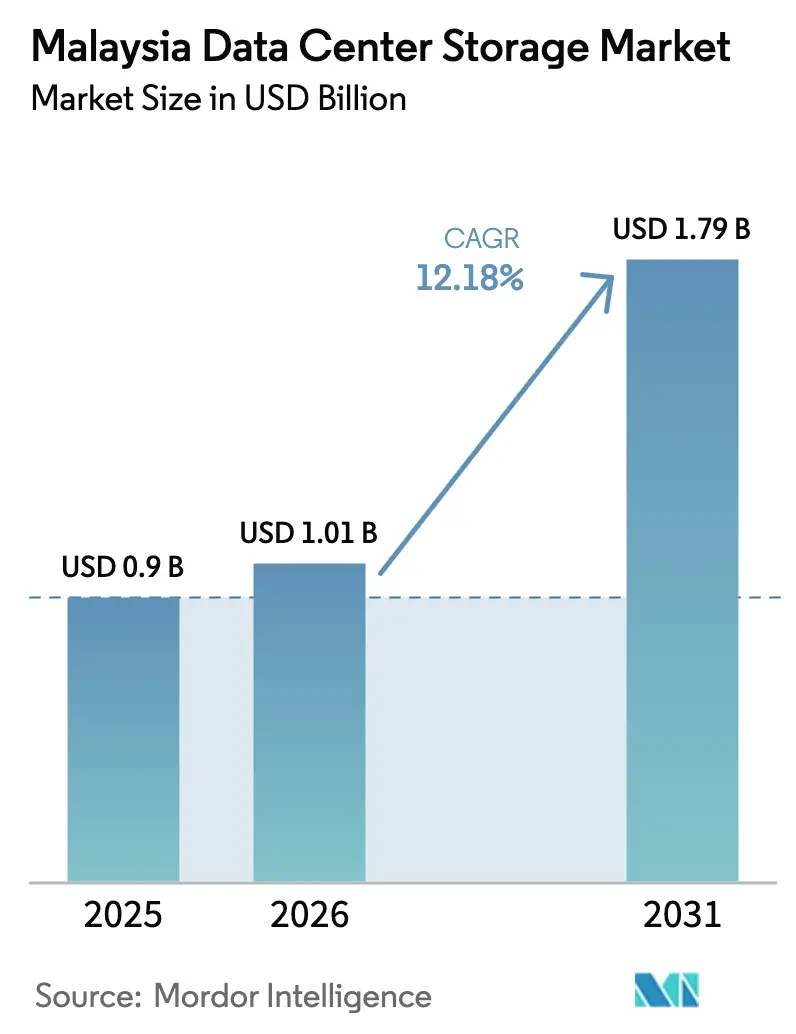

| Base Year Market Size (2025) | USD 0.90 Billion |

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Data Center Storage Market Analysis by Mordor Intelligence

The Malaysia data center storage market size is expected to grow from USD 0.90 billion in 2025 to USD 1.01 billion in 2026 and is forecast to reach USD 1.79 billion by 2031 at 12.18% CAGR over 2026-2031. Surging hyperscale capital expenditure, a nationwide fiber backbone, and the country’s first full-stack sovereign AI platform place the Malaysia data center storage market on a steeper growth trajectory than any other ASEAN peer. AI-centric workloads, 5G standalone core roll-outs, and strict data-residency amendments accelerate the transition from HDD arrays to flash-centric and software-defined architectures. Hyperscale build-outs in Johor Bahru alone exceed 1.6 GW of capacity, fueling multi-petabyte demand for enterprise-grade storage while amplifying competition among vendors to supply NVMe-enabled systems. Talent deficits in storage architecture and volatile NAND pricing remain the primary constraints, yet government skills funds and fiscal incentives for high-performance computing soften the impact.

Key Report Takeaways

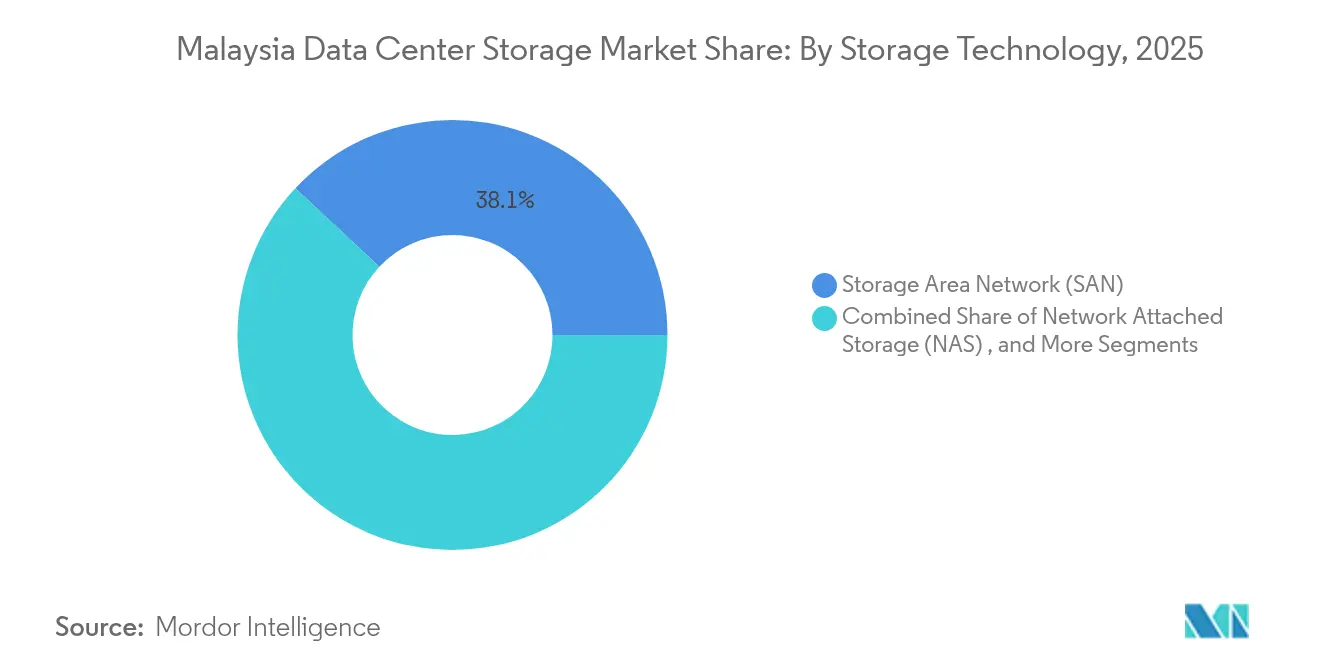

- By storage technology, Storage Area Networks led with 38.05% revenue share in 2025, whereas Network Attached Storage is forecast to expand at a 15.72% CAGR through 2031.

- By storage type, traditional HDD arrays accounted for 46.55% of the Malaysia data center storage market size in 2025, while all-flash arrays are advancing at a 16.92% CAGR to 2031.

- By data center type, colocation facilities held 53.55% Malaysia data center storage market share in 2025; hyperscalers and CSPs post the fastest-growing CAGR at 17.86% through 2031.

- By end user, IT and Telecommunications commanded 30.95% share in 2025, yet BFSI is set to grow at a 19.05% CAGR up to 2031.

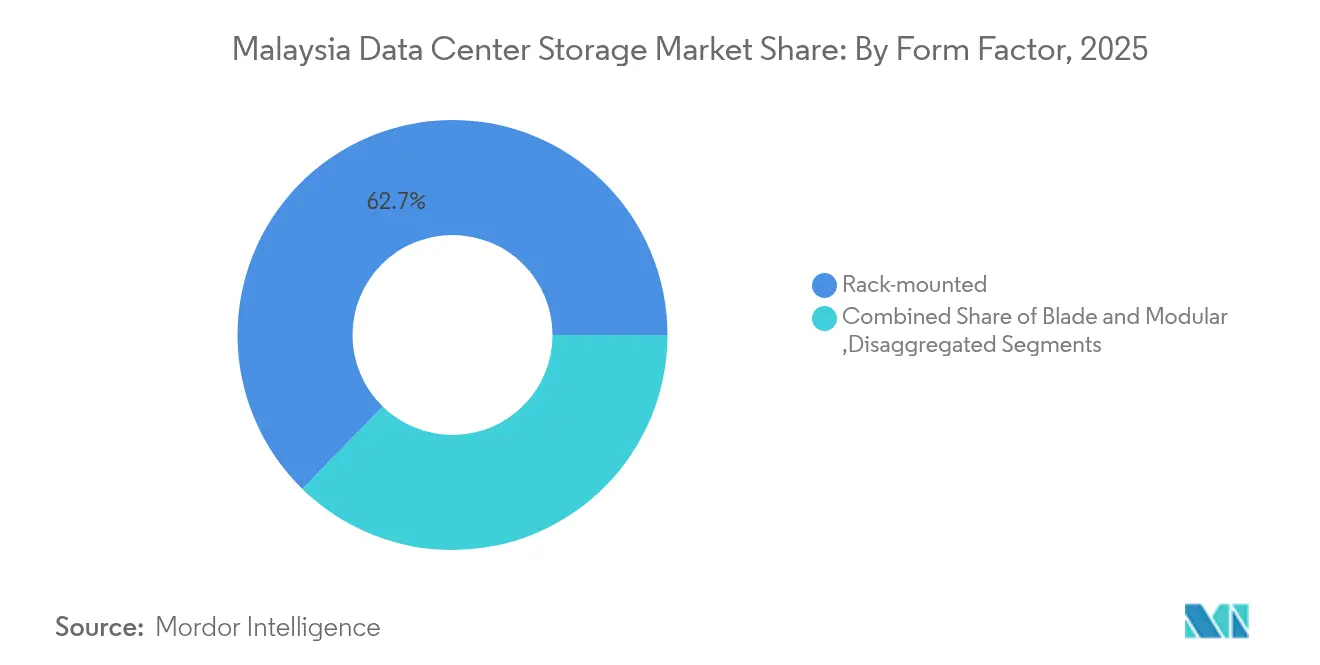

- By form factor, rack-mounted systems dominated with 62.70% revenue share in 2025, whereas disaggregated and composable platforms will post a 14.78% CAGR through 2031.

- By interface, SAS/SATA retained 53.85% share in 2025; NVMe is projected to rise at a 16.12% CAGR across the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hyperscale and colocation build-outs | +3.2% | Johor and Selangor | Medium term (2-4 years) |

| JENDELA Phase 2 fiber backbone expansion | +1.8% | Nationwide | Short term (≤ 2 years) |

| 5G SA core rollout and private 5G campuses | +2.1% | Urban and industrial zones | Medium term (2-4 years) |

| Government cloud-first initiatives | +1.5% | Nationwide | Long term (≥ 4 years) |

| Edge-ready plantations and smart factories | +0.9% | Peninsula, Sabah, Sarawak | Long term (≥ 4 years) |

| Strict PDPA data-residency compliance | +1.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Hyperscale and Colocation Build-outs

Johor Bahru doubled operational capacity in 2024 and now exceeds 1.6 GW, attracting Google, Microsoft, Oracle, and NTT to commit more than USD 10 billion to new campuses. Oracle’s USD 6.5 billion plan, Princeton Digital Group’s 150 MW AI-ready facility, and the Johor-Singapore Special Economic Zone signal an escalating need for petabyte-scale all-flash arrays that can sustain AI training throughput. This influx drives the Malaysia data center storage market toward NVMe architectures that synthesize low latency with high bandwidth, giving vendors with AI-optimized offerings a competitive edge

JENDELA Phase 2 Fiber Backbone Expansion

By early 2024, 81.5% population coverage and nearly 40,000 upgraded transmitters under the RM 21 billion JENDELA program produced gigabit links to 7.5 million premises. The extended backbone empowers SMEs in Penang’s semiconductor cluster to adopt distributed storage nodes for latency-sensitive process control. Rural edge nodes in palm-oil plantations leverage JENDELA’s reach to stage IoT sensor data locally before replicating to colocation hubs, stretching the Malaysia data center storage market into previously underserved districts.[1]Ministry of Communications and Digital, “JENDELA Quarterly Report Q1 2025,” mcmc.gov.my

5G Stand-Alone Core and Private 5G Campuses

Digital Nasional Berhad’s multi-operator 5G core delivers 99.8% uptime and ultra-low latency, enabling factories to run machine-vision analytics that depend on local cache arrays for split-second inference. Private 5G licenses spur automotive test tracks and industrial parks to embed micro-data centers near base stations, inflating demand for ruggedized flash clusters certified for harsh environments and pushing the Malaysia data center storage market beyond metro zones.[2]Digital Nasional Berhad, “Malaysia 5G Network Update 2025,” digitalnasional.com.my

Government Cloud-First and Digital Nasional Initiatives

A USD 356 million national electronic health-records platform and the sovereign AI infrastructure outfitted with 3,000 GPUs mandate on-premises, compliance-grade storage tiers that interoperate with public cloud. Agencies migrating legacy databases to SaaS still need local vaults for citizen data protected by the amended PDPA, broadening hybrid and object storage uptake across the Malaysia data center storage market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for Tier III/IV infrastructure | -2.1% | Nationwide, SME centric | Medium term (2-4 years) |

| Skilled storage-architect talent shortage | -1.8% | Kuala Lumpur and Johor | Short term (≤ 2 years) |

| Global NAND/HDD supply-chain volatility | -1.4% | Import-dependent Malaysia | Short term (≤ 2 years) |

| Ringgit-dollar exchange risk | -0.9% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex for Tier III/IV Infrastructure

Meeting Tier III redundancy elevates initial storage costs by 40-60%, a hurdle for Malaysia’s 3,000 Penang-based SMEs that rarely budget RM 500,000 per project. Although the Industry4WRD fund subsidizes upgrades, many firms delay transitions, limiting near-term penetration of advanced all-flash arrays within the Malaysia data center storage market

Global NAND/HDD Supply-Chain Volatility

AI-triggered demand spikes have prompted multinationals to signal 5–10% list-price increases on flash and HDD media. Malaysian buyers, already cost-sensitive, now renegotiate procurement calendars or down-scope capacity, postponing refreshes across the Malaysia data center storage market.[3]WD Technologies, “2025 NAND Market Price Notification,” wd.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Amid NAS Acceleration

Storage Area Networks captured 38.05% of Malaysia data center storage market share in 2025, confirming entrenched demand for block-level performance in financial services and smart-factory ERP clusters. High-availability SAN fabrics synchronized across Cyberjaya and Johor underpin regulatory DR mandates. Network Attached Storage, growing at a 15.72% CAGR, appeals to SMEs that prioritize simplified file shares and scalable capacity without FC licensing. The Malaysia data center storage market size for NAS solutions is projected to double by 2030, aligning with expanding creative-content workloads and collaboration suites.

Adoption of software-defined storage overlays amplifies both SAN and NAS flexibility. Dell’s PowerScale, already deployed by more than 16,000 GPU users globally, gains traction among AI start-ups seeking petabyte consolidation without forklift migrations. NetApp’s distributed cloud fabric with Google Cloud grants CIOs a single namespace across on-prem, Johor hyperscale nodes, and sovereign AI clusters, reinforcing hybrid leadership in the Malaysia data center storage market.

By Storage Type: Traditional HDD Resilience Versus Flash Uptake

Conventional HDD arrays held 46.55% share of the Malaysia data center storage market in 2025, leveraged for video surveillance archives and low-frequency medical images that tolerate higher latency. Yet all-flash arrays are sprinting at 16.92% CAGR as AI training, real-time payments, and high-frequency analytics dictate sub-millisecond latency. The Malaysia data center storage market size for flash is forecast to surpass USD 782.6 million by 2031, despite macro headwinds.

Hybrid platforms mitigate cost and performance tension: automatic tiering drives hot data onto NVMe SSD pools while cold blocks remain on nearline HDD. Seagate’s 40 TB HAMR drives and NVMe HDD prototypes could further compress TCO, delaying full flash substitution but expanding total terabytes shipped within the Malaysia data center storage market.

By Data Center Type: Colocation Primacy with Hyperscale Surge

Colocation suites represented 53.55% of revenue in 2025 as enterprises outsource resilience and compliance to specialized operators. Hyperscalers, however, clock an 17.86% CAGR through 2031, propelled by Google’s USD 2 billion Elmina facility and Microsoft’s tri-zone launch. Hyperscale investors integrate liquid cooling and composable fabrics that redefine density norms, steering the Malaysia data center storage market toward rack-level flash enclosures exceeding 700 kW per hall.

Meanwhile, edge micro-data centers install 42U cabinets in factories and plantations to localize AI inference. These deployments, though individually modest, aggregate to double-digit contribution by 2030, underscoring the Malaysia data center storage market’s diversification beyond traditional metros.

By End User: IT and Telecoms Lead, BFSI Accelerates

Operators such as Telekom Malaysia and Maxis, combined with cloud platforms, secured 30.95% 2025 revenue through fiber backhaul expansions and private 5G offerings. Banking and Financial Services, under Bank Negara’s refreshed RMiT framework, records a 19.05% CAGR as digital-bank licensees and incumbent institutions encrypt core databases on Tier IV SAN clusters. The Malaysia data center storage market size for BFSI is expected to approach USD 332.4 million by 2031, driven by open-API ecosystems and real-time fraud analytics.

Government ministries modernize census and taxation workloads onto sovereign clouds while retaining sensitive rows in on-prem flash vaults. Manufacturing SMEs adopting OEE dashboards and AI-assisted quality inspection equally stimulate incremental array shipments in the Malaysia data center storage market.

By Form Factor: Rack-Mounted Dominance with Composable Innovation

Rack-mounted arrays controlled 62.70% of 2025 spend due to universal cabinet dimensions and re-use of existing PDUs. Composable disaggregated infrastructure, posting 14.78% CAGR, grants hyperscalers dynamic assignment of GPU, CPU, and NVMe pools, slashing over-provisioning by some 45%. Malaysia data center storage market entrants that certify against liquid cooling and Open Compute Project specs are poised to outpace legacy chassis vendors.

Blade and modular enclosures survive in telecom huts and disaster-recovery bunkers where space and serviceability override other factors. Their persistent share safeguards multi-vendor competition inside the Malaysia data center storage market.

By Interface: SAS/SATA Stability with NVMe Transformation

Legacy SAS/SATA counted for 53.85% 2025 port shipments. NVMe’s 16.12% CAGR is anchored by GPU clusters that saturate PCIe 5.0 lanes and require microsecond access. Prototype NVMe HDDs may bridge protocol gaps, allowing operators to converge management stacks across flash and magnetic media—a development likely to reconfigure cost models inside the Malaysia data center storage market.

Fibre Channel remains a mainstay in regulated BFSI zones. iSCSI persists in branch environments where 10 GbE switches capex is sunk. Even so, NVMe-over-Fabrics pilots in two Kuala Lumpur trading floors demonstrate the next performance step for the Malaysia data center storage market.

Geography Analysis

Johor Bahru anchors the Malaysia data center storage market with more than 1.6 GW of operational capacity in 2025, reflecting over USD 10 billion of disclosed hyperscale investments. The Johor-Singapore Special Economic Zone further institutionalizes cross-border cloud traffic under aligned compliance frameworks, encouraging metro-cluster SAN replications across the causeway. Selangor’s Cyberjaya corridor remains the nation’s enterprise nucleus, hosting Google’s inaugural Malaysian data center and a 256 MW campus by Vantage; its colocation halls report 82% utilization in Q1 2025, ensuring steady refresh cycles for flash arrays.

Kuala Lumpur drives transactional workloads and hybrid migrations from ministries embarking on cloud-first policies. The forthcoming Microsoft cloud region will swing substantial AI-training demand into nearby edge cache tiers, swelling flash and NVMe interface uptake across the Malaysia data center storage market. Penang’s 3,000 electronics SMEs accelerate Industry 4.0 pilots, each embedding modest yet proliferating NAS appliances that cumulatively add high-double-digit petabytes by 2030.

Sarawak and Sabah trail in current capacity yet show strongest percentage growth. State-funded fiber backbones and green-hydro PPAs lure operators seeking renewable power footprints, positioning East Malaysia as the next expansion wave. Distributed edge nodes in palm-oil estates and smart ports funnel streaming data into regional micro-data centers, enlarging geographic breadth for the Malaysia data center storage market.

Competitive Landscape

The Malaysia data center storage market sits at a moderate concentration level, with Dell Technologies, Hewlett Packard Enterprise, and NetApp holding a collective leadership yet facing vigorous pursuits from Pure Storage and Huawei. Dell’s Partner-First Storage initiative, aligned with Johor hyperscale builds, aims to quadruple managed accounts by 2027. NetApp’s workload-aware fabric tightly integrates with Google Cloud’s dual-region strategy, carving a niche in regulated hybrid environments. Pure Storage invests in LandingAI and deploys FlashBlade//E in sovereign AI clusters, sharpening differentiation on low-carbon flash.

Huawei, riding sovereign AI contracts, offers ARM-based servers bundled with OceanStor arrays that rival established vendors on price-performance, injecting downward pricing pressure within the Malaysia data center storage market. Seagate’s HAMR roadmap secures future high-capacity HDD continuity, vital for cold archives in compliance-bound enterprises. White-label ODMs, meanwhile, cater to hyperscalers adopting open rack standards, fragmenting share beneath the Tier 1s and ensuring robust vendor competition.

Strategic moves include Equinix pursuing renewable PPAs to hedge tariff creep, and Vantage Data Centers’ RM 6 billion Cyberjaya project that embeds liquid-cool composable fabrics from inception, signaling an industry pivot toward density-optimized flash rows and GPU-linked NVMe fabrics across the Malaysia data center storage market.

Malaysia Data Center Storage Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

NetApp Inc.

Huawei Technologies Co. Ltd.

Kingston Technology Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Malaysia launched the region’s first sovereign full-stack AI infrastructure with 3,000 GPUs and established the Malaysia-China Trusted Data Zone

- May 2025: Google awarded a RM 1 billion construction contract to Gamuda Bhd and bought 389 acres in Negeri Sembilan for additional data center capacity

- April 2025: Microsoft confirmed three Malaysian data centers will go live in Q2 2025, expected to generate USD 10.9 billion in new revenue by 2028

- March 2025: Digital Nasional Berhad and Ericsson rolled out an Enterprise Virtual Cellular Network at DNB headquarters, creating the world’s first 5G-first office

- February 2025: Vantage Data Centers broke ground on a 256 MW campus in Cyberjaya, embedding liquid-cool storage aisles at scale

- October 2024: Oracle announced USD 6.5 billion in Malaysian cloud infrastructure, marking one of the largest tech investments to date

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Malaysia data center storage market as all revenue generated within Malaysian borders from the sale, lease, or as-a-service provision of enterprise-class storage arrays and software that reside inside purpose-built data centers, covering SAN, NAS, DAS, all-flash, hybrid, and software-defined storage platforms that support server racks of colocation, hyperscale, edge, and private facilities. According to Mordor Intelligence, the baseline excludes client devices, on-prem closet servers, and cloud storage capacity hosted outside Malaysia.

Scope exclusion: Backup media shipped offshore for disaster-recovery vaulting is outside our numerical scope.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Desk Research

We began with governmental and tier-1 open sources such as the Malaysian Communications and Multimedia Commission's JENDELA fiber progress bulletins, DOSM's ICT satellite accounts, MIDA investment approvals, customs import data for HS-code 8471.70 hardware, and MyDIGITAL policy notes. Trade association updates from the Asia Pacific Data Centre Association, Uptime Institute outage reports, and peer-reviewed IEEE papers on NVMe deployment patterns informed utilization assumptions. Paid intelligence from D&B Hoovers and Dow Jones Factiva helped us verify vendor financials and shipment announcements. These references illustrate, not exhaust, the document stack we mined for volumes, values, and regulatory cues.

A second sweep pulled annual reports, investor decks, tender logs, and press releases from storage OEMs and facility operators to benchmark average selling prices (ASP) and rack counts; this is where Mordor analysts tie consumption trends to commercial outcomes before moving to primary work.

Primary Research

Our team interviewed facility technical directors, hyperscaler procurement leads, telco storage architects, and large BFSI IT managers across Kuala Lumpur, Cyberjaya, and Johor. Surveys captured live migration ratios from HDD to flash, planned NVMe adoption, and expected rack-density road maps, allowing us to validate desk findings and stress-test model sensitivities.

Market-Sizing & Forecasting

We start with a top-down reconstruction: installed megawatt capacity and average GB per watt yield a national storage pool, which we price using blended ASP curves. Select bottom-up checks, vendor shipment tallies, channel audits, and sampled contract values anchor the totals. Key variables include hyperscale CAPEX announcements, rack density (kW/rack), NAND price indices, 5G traffic growth, and PDPA-driven data residency mandates; each is forecast through multivariate regression and scenario analysis that captures upside from AI workloads. Gaps in bottom-up granularity are bridged by regional penetration proxies before final alignment.

Data Validation and Update Cycle

Outputs pass variance and plausibility screens, then two-stage peer review. Whenever new capacity over 50 MW is commissioned or a material price swing exceeds 10%, analysts reopen the model. Full refreshes occur annually and clients receive the freshest view right before publication.

Why Mordor's Malaysia Data Center Storage Baseline Commands Reliability

Published estimates often diverge; scope cut-offs, pricing ladders, and update cadences rarely match. We flag these drivers upfront so decision-makers see why numbers move.

Key gap drivers include: some studies bundle server and network hardware with storage, several apply global ASPs without Malaysia-specific subsidies, while a few freeze exchange rates at proposal date rather than transaction date. Mordor's model limits scope to in-country storage revenue, rolls ASPs quarterly, and refreshes capacity inputs every six months, yielding a tempered, transparent figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.90 B (2025) | Mordor Intelligence | - |

| USD 4.04 B (2024) | Regional Consultancy A | Includes servers and network gear; assumes constant 16% CAGR without price erosion checks |

| USD 0.65 B (2024) | Industry Association B | Omits hyperscale self-build spend; relies on three-year-old import data |

In short, our disciplined scope selection, variable tracking, and quicker refresh cadence give stakeholders a balanced baseline they can retrace and defend with confidence.

Key Questions Answered in the Report

What is the current size of the Malaysia data center storage market?

The Malaysia data center storage market stands at USD 1.01 billion in 2026 and is projected to grow to USD 1.79 billion by 2031.

Which storage technology leads in Malaysia?

Storage Area Networks are the leading technology, holding 38.05% revenue share in 2025, with Network Attached Storage growing fastest at a 15.72% CAGR.

How will hyperscale investments impact storage demand?

Hyperscale projects exceeding USD 10 billion, especially in Johor Bahru, are driving multi-petabyte demand for flash and NVMe-based systems across the Malaysia data center storage market.

Why are all-flash arrays gaining traction?

AI training, real-time analytics, and sub-millisecond application needs are pushing enterprises toward all-flash arrays, which are forecast to grow at a 16.92% CAGR to 2031.

What regional areas show the strongest growth?

Johor Bahru leads in absolute capacity, Selangor’s Cyberjaya remains the enterprise hub, and East Malaysia (Sarawak and Sabah) posts the highest percentage growth due to new green-energy data centers.

What are the main challenges facing the market?

High capital expenditure for Tier III/IV facilities, talent shortages in storage architecture, and volatile global NAND/HDD pricing are the key headwinds limiting rapid deployment.

Page last updated on: