Magnesium Stearate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

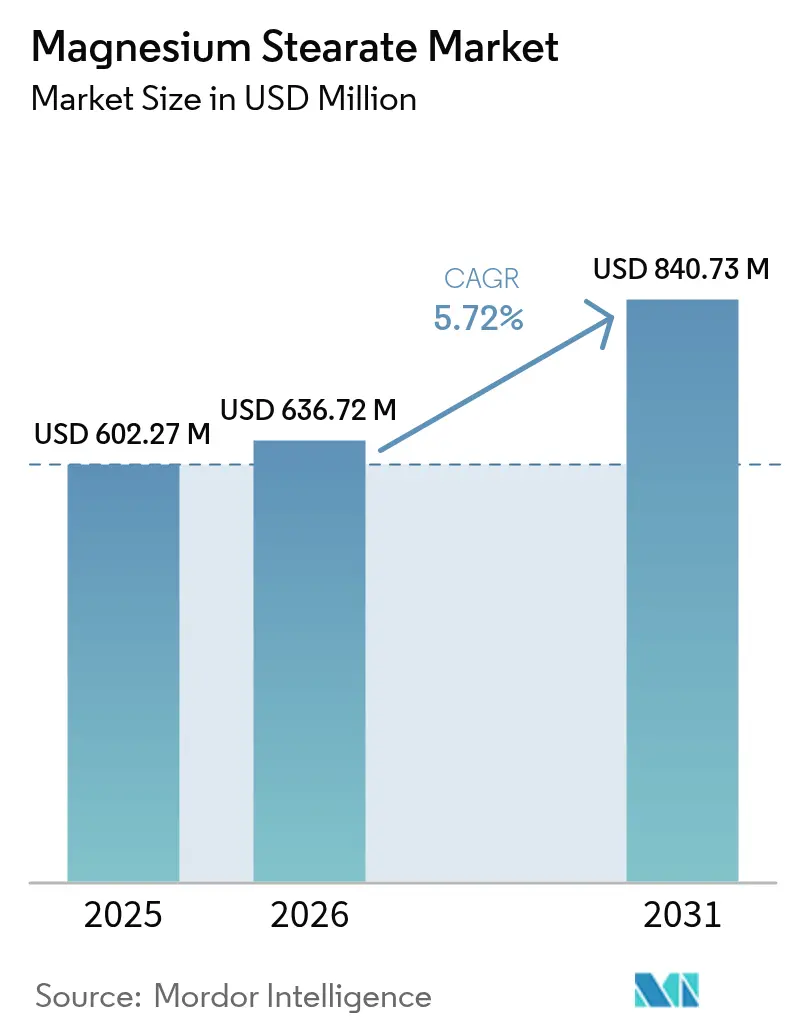

| Market Size (2026) | USD 636.72 Million |

| Market Size (2031) | USD 840.73 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

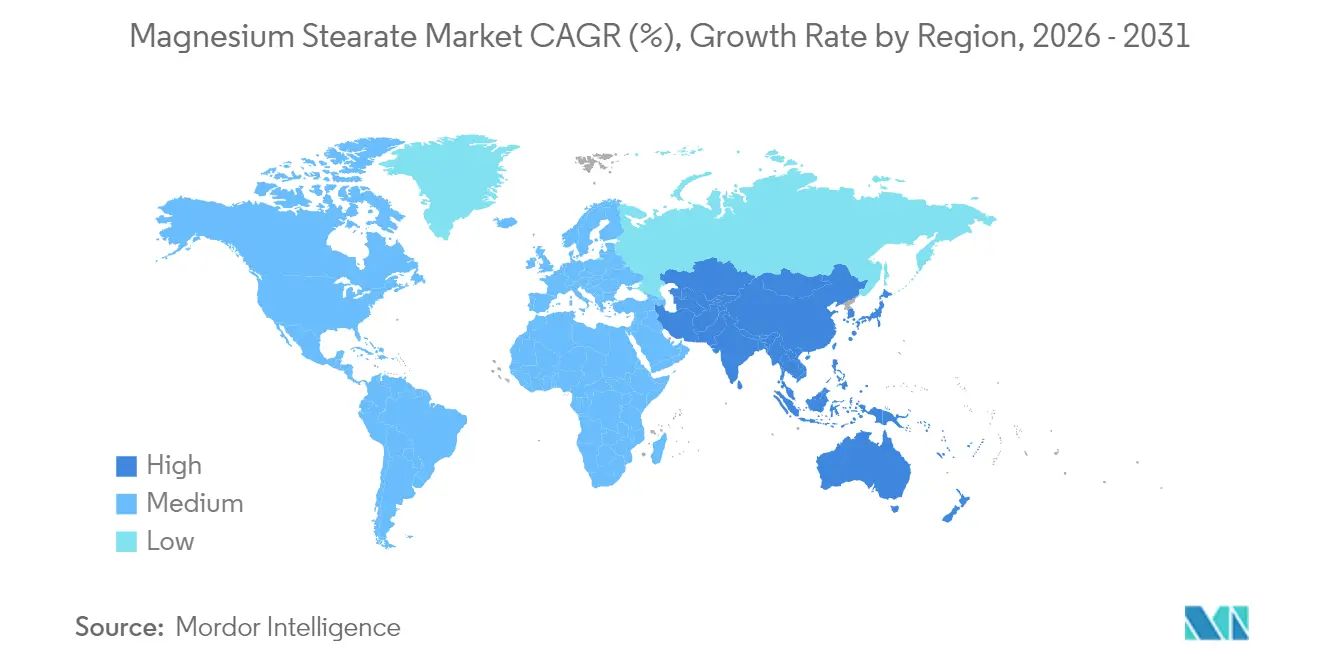

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

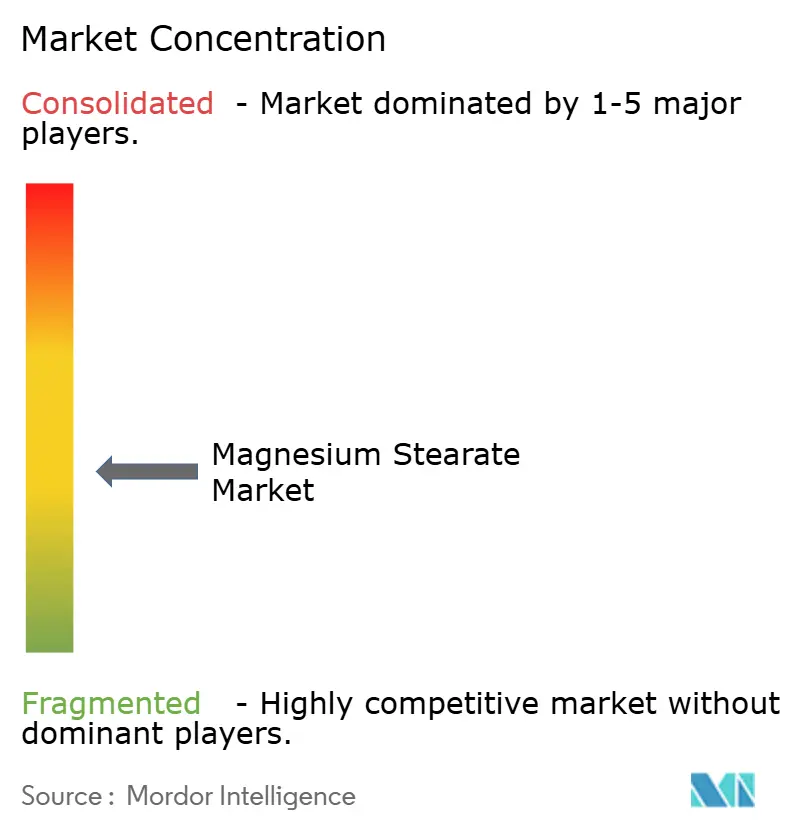

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Stearate Market Analysis by Mordor Intelligence

The Magnesium Stearate market size is expected to grow from USD 602.27 million in 2025 to USD 636.72 million in 2026 and is forecast to reach USD 840.73 million by 2031 at 5.72% CAGR over 2026-2031. Current growth momentum mirrors the compound’s entrenched role in pharmaceutical compression, personal care binding, anti-caking food systems, and polymer heat stabilization. Heightened investment in continuous oral-solid-dose manufacturing, especially across North America and Europe, keeps demand buoyant as equipment makers specify excipients that sustain lubrication under high-throughput conditions. Clean-label imperatives have simultaneously pushed suppliers to introduce plant-based or palm-free grades, adding premium-priced alternatives without displacing core volumes. Asia-Pacific’s expanding generic production and rising per-capita medicine intake anchor bulk consumption, while the advent of electric-vehicle wire harnesses opens a small yet strategically significant outlet for stearate-stabilized PVC. Competitive intensity revolves around analytical consistency, fatty-acid-chain verification, and traceability programs that reassure quality-focused buyers.

Key Report Takeaways

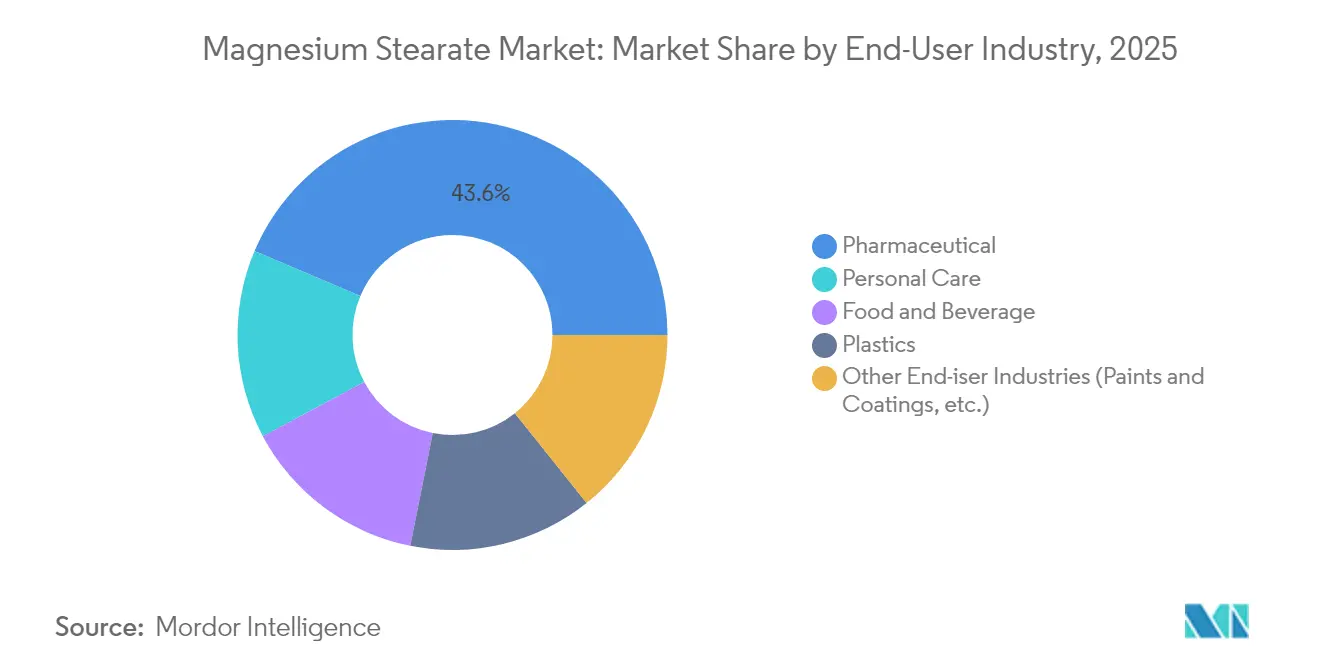

- By end-user industry, the pharmaceutical segment held 43.62% of the Magnesium Stearate market share in 2025, whereas personal care is forecast to advance at a 6.12% CAGR to 2031.

- By geography, Asia-Pacific dominated with 41.12% revenue share in 2025 and is set to post the fastest 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Magnesium Stearate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Continuous-manufacturing Lines in Solid-dose Pharma | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Emergence of Vegan/palm-free Grades Targeting Clean-label Nutraceuticals | +0.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Rising Intake of Oral Solid Dosage Forms in Low-income Economies | +1.5% | APAC core, with secondary impact in MEA | Short term (≤ 2 years) |

| Polyvinyl Chloride (PVC) Heat-stabilization Demand in Electric-vehicle Wire Harnesses | +0.7% | Global, with early gains in China, Germany, United States | Medium term (2-4 years) |

| Rapid Expansion of Cosmetic Pressed-powder Lines | +0.9% | Global, with concentration in North America & APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Continuous-manufacturing Lines in Solid-dose Pharma

Large producers such as Pfizer and Eli Lilly now run commercial continuous-manufacturing assets that blend, compress, and coat tablets in integrated skids, eliminating stoppages that once masked excipient variability. Magnesium stearate market participants able to guarantee narrow particle-size distributions and stable fatty-acid ratios secure preferred-supplier status because any deviation escalates the risk of lubrication overshoot that damages tensile strength. Regulators back the switch by shortening approval review times for continuous plants, further entrenching high-specification excipient demand. Continuous processing magnifies every input’s contribution to critical-quality attributes, encouraging tier-one buyers to pare their vendor lists to firms with robust in-line analytical tools.

Emergence of Vegan / Palm-free Grades Targeting Clean-label Nutraceuticals

Consumers scrutinize excipient origins as closely as active ingredients, prompting nutraceutical formulators to abandon animal-derived or palm-based stearates where feasible. Suppliers such as Biogrund commercialized CompactCel LUB, a vegetable-sourced grade that matches traditional lubrication yet aligns with vegan labeling and Roundtable on Sustainable Palm Oil commitments [1]Product Team, “CompactCel LUB Technical Data Sheet,” biogrund.com. While functional equivalence lowers reformulation hurdles, manufacturers still validate flow, compressibility, and dissolution in pilot runs, sustaining testing revenues for analytical houses. Retailers amplify momentum by mandating excipient transparency for store-brand supplements, nudging even cost-sensitive private-labelers toward certified vegan inputs.

Rising Intake of Oral-Solid-Dosage Forms in Low-income Economies

Expanded public insurance and generic substitution across India, Indonesia, Nigeria, and Vietnam has lifted annual tablet volumes and, by extension, lubricant consumption. Local producers favor well-characterized materials that regulators readily accept, keeping the magnesium stearate market entrenched in price-sensitive bids. Government procurement often awards to facilities meeting WHO pre-qualification, a standard that implicitly rewards suppliers with global pharmacopeia conformity. Demand spikes, however, can reveal quality-variance risks among micro-scale stearate mills, compelling multinational buyers to dual-source from audited, higher-cost vendors to ensure uninterrupted supply.

Rapid Expansion of Cosmetic Pressed-powder Lines

Korean beauty (K-beauty), Japanese beauty (J-beauty), and premium United States makeup brands have multiplied pressed-powder launches that rely on magnesium stearate for silky feel, sebum absorption, and pan integrity. Laboratories optimize stearate concentration to balance adhesion with brush pickup, making surface area and crystal morphology decisive purchase criteria. Growth in this niche benefits distributors capable of stocking cosmetic-grade certifications and offering micro-pulverized variants suitable for air-cushion compacts. Higher value per kilogram than pharmaceutical grades offsets volume limitations and raises margins for specialists serving color-cosmetics houses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Palm-oil Traceability Regulations Increasing Input Costs | -0.9% | Global, with concentration in EU & North America | Medium term (2-4 years) |

| Adoption of Sodium Stearyl Fumarate as a High-performance Clean-label Alternative | -1.1% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Quality-variance Risk From Micro-scale Suppliers | -0.6% | APAC core, with secondary impact in MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Palm-oil Traceability Regulations Increasing Input Costs

The European Union’s deforestation regulation and parallel the United States Customs audits oblige stearate producers to document every tonne of palm-derived stearic acid. Compliance entails satellite monitoring, isotopic fingerprinting, and blockchain recordkeeping, driving procurement overheads that smaller mills struggle to absorb. Analytical mandates from bodies like the Malaysian Palm Oil Board have raised testing frequency, adding laboratory capital expense and elongating lead times [2]J. Tan et al., “Palm-oil Traceability Using Isotopic Techniques,” mdpi.com . Larger multinationals, however, recoup costs by marketing certified-sustainable excipients at premiums to personal-care brands prioritizing ethical sourcing.

Adoption of Sodium Stearyl Fumarate as a High-performance Clean-label Alternative

In moisture-sensitive modified-release tablets, formulators pivot to sodium stearyl fumarate to avoid prolonged disintegration that magnesium stearate may cause at higher shear energies. Peer-reviewed trials show fumarate lubricants retain mechanical strength while cutting disintegration time by up to 30%. The additive’s hydrophilic nature also simplifies wet-granulation processing. Yet its higher cost and limited availability constrain adoption to value-added therapies or markets where quick dissolution is critical, tempering overall displacement of existing stearate demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Pharmaceutical Dominance Drives Market Stability

In 2025, pharmaceutical applications accounted for 43.62% of the Magnesium Stearate market revenue, underscoring decades of regulatory acceptance and cost-efficient performance. Tablets, capsules, and granules integrate the excipient at concentrations usually below 2%, yet cumulative volumes remain high due to sheer output of oral-solid doses. Because reformulating legacy products demands new bioequivalence dossiers, brand and generic manufacturers retain existing stearate grades, insulating this segment from short-term substitution risk. Meanwhile, the personal care business, anchored by pressed-powder and dry shampoo launches, shows the fastest trajectory at a 6.12% CAGR. This growth adds premium-priced, cosmetic-grade volumes, albeit from a smaller base.

Food and beverage formulators employ the powder as an anti-caking and flow agent in icing sugar, baking mixes, and powdered drink bases. Even at low inclusion rates, dependable moisture control renders magnesium stearate indispensable where conveyor throughput and consumer pour-ability intersect. Plastics processors have carved a niche in heat-stabilized Polyvinyl Chloride (PVC), particularly for electric-vehicle wiring that experiences higher under-hood temperatures. Although representing a modest slice, this outlet diversifies revenue streams and lowers reliance on pharmaceutical cycles. Collectively, these patterns safeguard the broader magnesium stearate market against demand shocks in any single vertical.

Geography Analysis

Asia-Pacific led with 41.12% revenue in 2025 and is on track for a 6.01% CAGR through 2031, making it the linchpin of the magnesium stearate market. China’s magnesium-metal capacity surged 24.5% in 2024, surpassing 1.02 Million tonnes and cushioning regional raw-material supply. Concurrently, India’s contract-development and manufacturing organizations ramped tablet output for exports to Africa and Latin America, further lifting lubricant demand. Southeast Asian nations benefit as both consumption and secondary processing hubs, with Vietnam and Indonesia offering cost-advantaged blending services that feed neighboring Association of Southeast Asian Nations (ASEAN) markets.

North America remains a technology pacesetter, hosting several Food and Drug Administration (FDA)-approved continuous-manufacturing plants that set stringent excipient specification benchmarks. Buyers insist on full United States Pharmacopeia (USP), European Pharmacopoeia (EP), and Japanese Pharmacopoeia (JP) monograph compliance, compelling vendors to maintain harmonized documentation packs. Clean-label advocacy is more pronounced in the United States, where natural-product retailers blacklist animal-derived stearates, nudging suppliers toward certified vegan lines. Europe mirrors these quality demands and intensifies sustainability scrutiny, compelling palm-supply chain audits and life-cycle assessments before purchasing decisions.

South America, the Middle East, and Africa collectively contribute a smaller but rising parcel of global uptake. Brazil’s Agência Nacional de Vigilância Sanitária (ANVISA) fast-track for generic approvals fuels tablet output, while Saudi Arabian and South African public tenders prioritize local sourcing where feasible. However, fragmented local production capacity often lacks advanced analytical instruments, creating opportunity for multinational suppliers offering turnkey quality services. Despite lower volume, these geographies offer risk diversification and long-run upside as healthcare spend per capita climbs.

Competitive Landscape

The Magnesium Stearate Market is moderately fragmented, with the top five producers, such as Baerlocher GmbH, Merck KGaA, Valtris Specialty Chemicals, Peter Greven GmbH & Co. KG, and FACI Corporate S.p.A. accounting for a significant global revenue. Baerlocher GmbH leverages vertical integration in metal soaps to deliver consistent fatty-acid profiles. Merck KGaA maintains premium standing via stringent Current Good Manufacturing Practice (cGMP) stewardship and multi-compendial dossiers updated across International Council for Harmonization (ICH) regions. Tier-two competitors differentiate through regional proximity and bespoke particle-size tailoring, appealing to cosmetic formulators seeking unique sensory attributes. Strategic partnerships intensify as customers demand co-development support. Excipient makers invest in application labs to simulate continuous-mixing shear, enabling predictive lubrication modeling.

Magnesium Stearate Industry Leaders

Baerlocher GmbH

Valtris Specialty Chemicals

Merck KGaA

Peter Greven GmbH & Co. KG

FACI Corporate S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Evonik Industries AG expanded capacity at its Darmstadt site using solvent-free micronization for producing RESOMER (polymer) powders, a technology that can support ultra-fine magnesium stearate.

- October 2022: Roquette Frères completed its acquisition of Crest Cellulose, an Indian firm specializing in excipients for the pharmaceutical and nutraceutical sectors. Animal-free excipients manufactured by Crest include MICROCEL microcrystalline cellulose and Roquette Magnesium Stearate. This strategic move not only bolsters Roquette Frères' operational capabilities but also positions the company to cater to a broader clientele across India, Asia, and beyond.

Global Magnesium Stearate Market Report Scope

Magnesium stearate is a simple salt that is produced using mineral magnesium and saturated fat stearic acid. It is majorly used as a nutritional supplement in the food & beverage industry and in several pharmaceutical applications. The market is segmented by end-user Industry and geography. By end-user industry, the market is segmented into pharmaceutical, food & beverage, personal care, plastics, and other end-user industries. The report also covers the market size and forecasts for the Magnesium Stearate Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD Million).

| Pharmaceutical |

| Food & Beverage |

| Personal Care |

| Plastics |

| Other End-iser Industries (Paints & Coatings, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By End-User Industry | Pharmaceutical | |

| Food & Beverage | ||

| Personal Care | ||

| Plastics | ||

| Other End-iser Industries (Paints & Coatings, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the magnesium stearate market?

The market is valued at USD 636.72 Million in 2026 and is forecast to reach USD 840.73 Million by 2031.

Which end-user industry dominates demand?

Pharmaceutical manufacturing leads with a 43.62% revenue share in 2025, driven by the excipient’s role in tablet lubrication.

Which region is growing the fastest?

Asia-Pacific posts the highest 6.01% CAGR to 2031 due to expanding generic drug production and abundant magnesium supply.

Why are clean-label grades gaining traction?

Vegan and palm-free formulations meet consumer transparency expectations and help brands comply with evolving sustainability standards.

What alternative lubricant threatens market share?

Sodium stearyl fumarate offers faster disintegration and cleaner labeling for certain modified-release tablets, posing niche competition.

Page last updated on: