M2M Connections Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.91 Billion |

| Market Size (2031) | USD 59.44 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

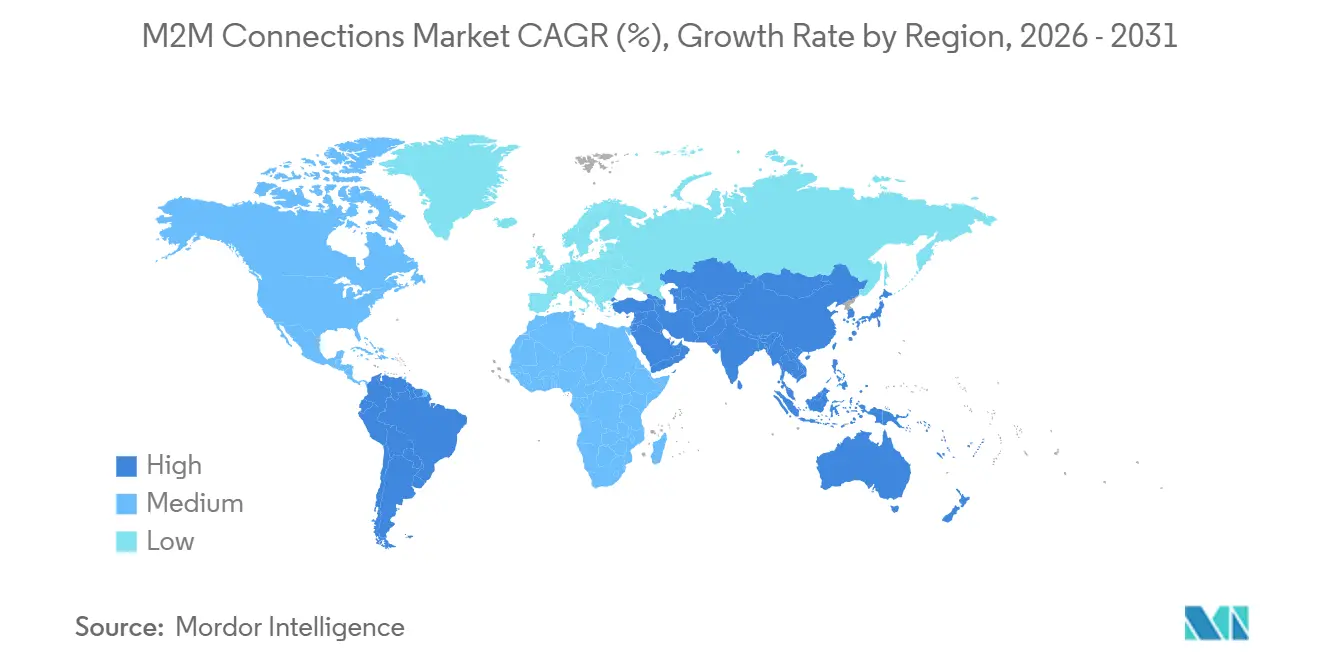

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

M2M Connections Market Analysis by Mordor Intelligence

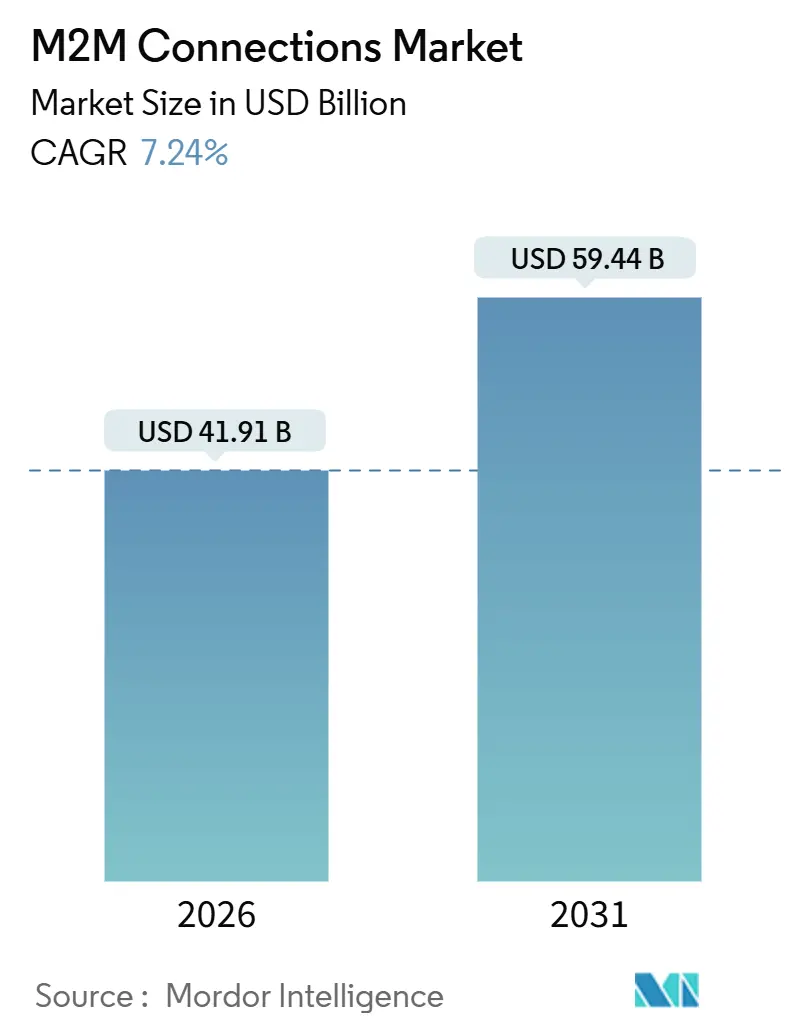

The M2M connections market size stands at USD 41.91 billion in 2026 and is forecast to reach USD 59.44 billion by 2031, expanding at a 7.24% CAGR. Demand is rising as enterprises pair denser cellular footprints with edge processing, eSIM provisioning, and cloud-native device management. These advances cut recurring connectivity costs, unlock use cases that once failed due to latency or power constraints, and spur new revenue models for operators and module suppliers. Wireless links dominate because they eliminate trenching expenses in remote sites, while cloud-hosted control planes streamline firmware updates and analytics. Competition is intensifying as hyperscale clouds bundle connectivity with application services, prompting mobile network operators to add integrated edge compute and verticalized solutions. Security hardening and protocol convergence remain critical priorities as device counts scale into the tens of billions.

Key Report Takeaways

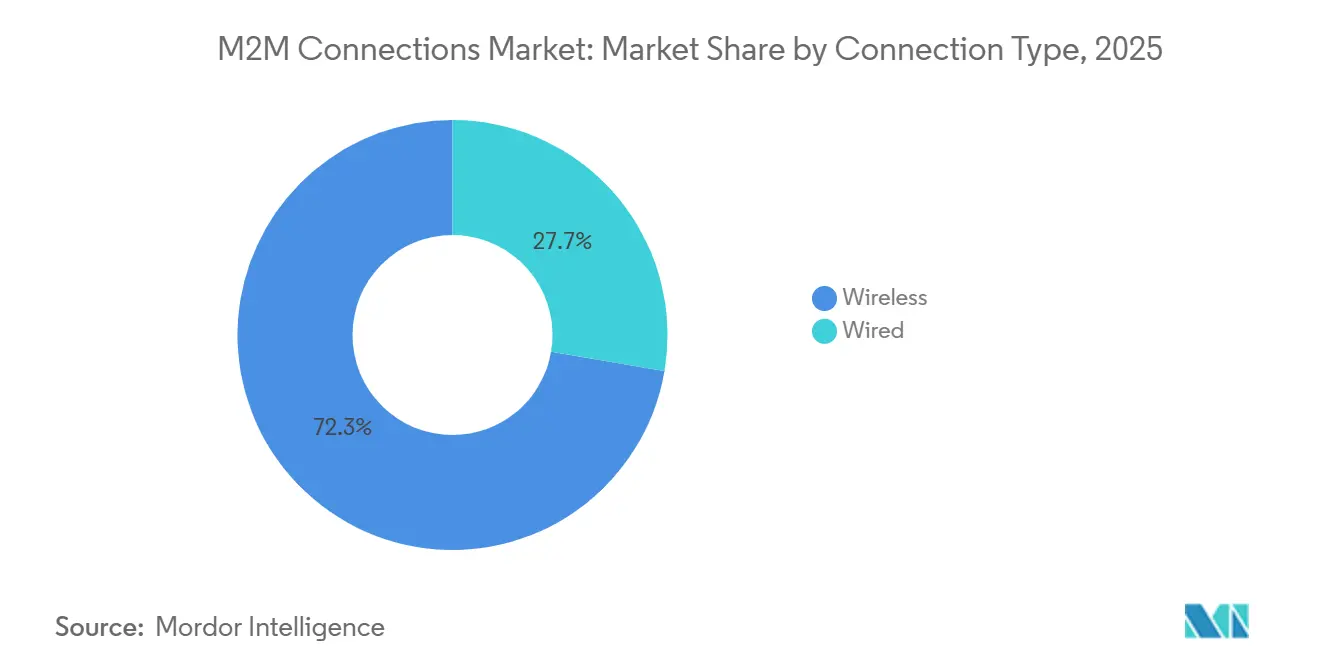

- By connection type, wireless dominated with 72.33% of the M2M connections market share in 2025 and is set to grow at a 7.66% CAGR through 2031.

- By technology, cellular accounted for 47.19% of the market share in 2025, while low-power wide-area networks are forecast to grow at an 8.41% CAGR through 2031.

- By deployment model, cloud deployment accounted for 56.89% of revenue in 2025 and is projected to register the highest 7.83% CAGR through 2031.

- By end-user industry, automotive led with 23.47% share in 2025, whereas healthcare is poised for the fastest 8.89% CAGR through 2031.

- By geography, Asia-Pacific captured 33.82% of 2025 volume, while the Middle East is expected to post the swiftest 8.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global M2M Connections Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT Devices Across Industries | +1.8% | Global, with concentration in Asia-Pacific manufacturing hubs and North American logistics networks | Medium term (2-4 years) |

| Increasing Number of Mobile Connections and Smartphone Penetration | +1.3% | Asia-Pacific core, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Growing Adoption of Telematics in Automotive and Transport | +1.5% | North America and Europe for passenger vehicles; Asia-Pacific for commercial fleets | Medium term (2-4 years) |

| Integration of eSIM Technology Enabling Massive M2M Scalability | +1.2% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Rise of Private 5G Networks for Industrial M2M Applications | +1.0% | North America and Europe industrial corridors; emerging in Asia-Pacific special economic zones | Long term (≥ 4 years) |

| Emerging Demand for Real-Time Edge Analytics Reducing Latency | +0.9% | Global, concentrated in urban centers with dense edge infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of IoT Devices Across Industries

Industrial firms are embedding sensors in once-isolated equipment to collect telemetry that feeds predictive maintenance programs, trimming unplanned downtime and energy waste. Manufacturer subsidies and falling module prices, now below USD 5 for NB-IoT chipsets, make connectivity viable for low-value assets. Retail chains run smart shelves that trigger restocks automatically, and pipeline operators outfit thousands of kilometers of infrastructure with pressure sensors that detect leaks within minutes. Momentum is strongest in heavy industry, mining, and petrochemicals, where every hour of outage carries six-figure losses.[1]Bosch Global, “Industry 4.0 and Private 5G Networks,” bosch.com Equipment makers now ship connectivity-ready machines by default, accelerating the installed base and stimulating recurring service revenue for operators and analytics vendors.

Increasing Number Of Mobile Connections And Smartphone Penetration

Rapid smartphone adoption in emerging markets lowers the marginal cost of adding M2M endpoints by allowing carriers to reuse existing LTE and 5G capacity. India’s Department of Telecommunications requires every new tower to support NB-IoT and LTE-M, expanding rural coverage for agriculture sensors.[2]Department of Telecommunications India, “National IoT Policy Framework 2024,” dot.gov.in Technicians now provision gateways via Bluetooth and NFC on handheld devices rather than proprietary laptops, cutting installation times from hours to minutes. China Mobile’s OneLink platform added 180 million connections in the 12 months ending September 2024, proving the scalability of app-based onboarding. Logistics fleets mirror this shift, as drivers pair smartphones with vehicle units to upload telematics without dedicated scanners, reinforcing the flywheel effect for operator economics.

Growing Adoption Of Telematics In Automotive And Transport

Automakers embed cellular modules to push over-the-air software updates, perform remote diagnostics, and enable usage-based insurance. General Motors generated USD 2.1 billion in subscription revenue from its OnStar service in 2024.[3]General Motors, “2024 Annual Report,” gm.com European Union mandates on eCall have seeded more than 50 million connected cars, which now support stolen-vehicle tracking and predictive maintenance. Commercial fleets achieve up to 20% fuel savings by mining telematics for route optimization. United States regulators funded USD 300 million in cellular V2X pilots that cut intersection collisions and reinforced connectivity demand. Electric vehicles further amplify telematics penetration, as battery health monitoring requires persistent data uplinks to avoid thermal events.

Integration of eSIM Technology Enabling Massive M2M Scalability

eSIM decouples hardware from carrier selection, allowing remote profile downloads that slash supply-chain complexity. GSMA’s 2024 Remote SIM Provisioning update adds post-quantum cryptography, enabling devices to switch carriers over-the-air while maintaining security. IDEMIA and Qualcomm commercialized an integrated SIM chipset that frees 40% of board space, critical for wearables and implants where miniaturization is paramount. Automotive manufacturers bundle multi-year connectivity that roams seamlessly across borders, and utilities rely on eSIM to meet data-localization mandates by activating domestic profiles on install. Together, these capabilities remove friction and pave the way for billions of incremental endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Security Concerns in M2M Communications | -0.9% | Global, acute in Europe due to GDPR enforcement and North America due to sector-specific regulations | Short term (≤ 2 years) |

| Lack of Global M2M Standards and Interoperability | -0.7% | Global, fragmentation most severe in application layer protocols | Medium term (2-4 years) |

| Scarcity of IPv4 Address Space and Delays in IPv6 Transition | -0.5% | North America and Europe legacy networks; emerging markets less constrained | Long term (≥ 4 years) |

| Supply-Chain Disruptions for Specialized M2M Chipsets | -0.6% | Global, concentrated impact in automotive and industrial sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy And Security Concerns In M2M Communications

Weak authentication and outdated firmware expose critical infrastructure. CISA issued 23 industrial control advisories in 2024, citing hardcoded credentials and insecure bootloaders. A botnet hijacked 40,000 routers after manufacturers shipped devices with default passwords, underscoring provisioning lapses. Healthcare regulators demand end-to-end encryption for insulin pumps and cardiac monitors, raising compliance costs and delaying launches. Enterprises are adopting zero-trust architectures, but retrofitting cryptographic hardware onto legacy sensors remains cost-prohibitive for low-value assets. Certification regimes such as IEC 62443 add 10-15% to the bill of materials, squeezing margins.

Lack Of Global M2M Standards And Interoperability

Divergent protocols force manufacturers to support multiple firmware branches, inflating R&D overhead. MQTT, CoAP, and LwM2M use incompatible message formats, so gateways must translate traffic, introducing latency and failure points. OneM2M offers a common service layer, yet adoption lags as vendors race to market with proprietary stacks. Vehicle makers lock diagnostic data behind closed interfaces, fragmenting aftermarket services. Industrial automation remains siloed because PLC suppliers use proprietary buses that prevent best-of-breed sensor integration. Cross-border logistics suffer when devices cannot authenticate with local networks during roaming, leading to blind spots in global tracking.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connection Type: Wireless Extends Its Lead On Flexibility

Wireless links accounted for 72.33% of the M2M connections market in 2025 and are on track for a 7.66% CAGR through 2031. Mining companies in Australia and Chile cover sprawling pits with LTE-M, connecting autonomous haul trucks without costly fiber runs. Smart agriculture favors wireless because sensors and weather stations spread across fragmented acreage cannot justify trenching. Satellite fills coverage gaps for pipelines and maritime assets, with Iridium and Globalstar offering narrowband service where terrestrial signals fade.

Total cost of ownership keeps tilting toward wireless as module prices drop 40% between 2022 and 2024, while skilled-labor shortages drive up wired-installation costs. Wired Ethernet still holds its ground in building automation, where power-over-Ethernet simplifies provisioning and eliminates battery maintenance. Hybrid topologies are emerging, aggregating wired sensor clusters into cellular backhaul to balance reliability and cost, but the overall momentum remains firmly behind wireless in the M2M connections market.

By Technology: Cellular Holds Share While LPWA Leads Growth

Cellular connections secured 47.19% of the M2M connections market share in 2025, driven by ubiquitous LTE and 5G networks that support high-bandwidth video and real-time tracking. NB-IoT and LTE-M extend battery life for meters and environmental monitors, propelling LPWA toward the fastest 8.41% CAGR to 2031. China Mobile alone manages more than 1.47 billion IoT lines, the majority of which are on NB-IoT.

Short-range radios like Bluetooth Low Energy and Zigbee dominate wearables and smart home clusters within 100 meters of a gateway. LoRaWAN occupies a middle ground for city-scale deployments where cellular data plans incur unsustainable recurring fees, with Amsterdam and Singapore running public networks that host parking and air-quality sensors. Satellite technologies remain indispensable for maritime, aviation, and remote pipelines, reinforcing a multi-modal landscape that chipset vendors now address with integrated radios capable of dynamic network selection.

By Deployment Model: Cloud Platforms Capture Majority Share

Cloud deployments held 56.89% of 2025 revenue and will retain leadership at a 7.83% CAGR through 2031. Amazon Web Services IoT Core and Microsoft Azure IoT Hub together hosted more than 500 million devices in 2024. Enterprises choose the cloud to avoid up-front server purchases and gain global redundancy for firmware distribution.

On-premises installations persist in defense, critical infrastructure, and sites with patchy internet connectivity. Hybrid models are rising as manufacturers deploy edge gateways for real-time analytics while synchronizing summaries to cloud data lakes. PCI-compliant payment networks keep transaction logic local to shield cardholder information, batching encrypted records to central vaults during off-peak windows. Cloud providers now offer managed edge containers that blur lines between deployment models, advancing scalability and operational simplicity across the M2M connections market.

By End-User Industry: Automotive Dominates, Healthcare Accelerates

Automotive applications captured 23.47% of the 2025 volume as connected-service bundles became standard in new vehicles. Remote diagnostics, infotainment updates, and eCall safety mandates create durable demand for cellular modules. Meanwhile, healthcare is the fastest-growing sector, with an 8.89% CAGR, thanks to expanded reimbursement for cellular glucose monitors and cardiac rhythm devices in the United States.

Retail chains deploy M2M point-of-sale terminals that sync inventory across brick-and-mortar and e-commerce channels, reducing stockouts by 25%. Oil and gas firms instrument wells and pipelines to detect leaks more quickly, thereby mitigating environmental fines. Logistics providers outfit containers with GPS and temperature sensors to safeguard the cold chain for pharmaceuticals. Diverse vertical adoption secures a broad demand base that underpins the M2M connections market.

Geography Analysis

Asia-Pacific accounted for 33.82% of global connections in 2025, driven by state mandates for smart cities and utilities. China’s vast installed base is complemented by India’s National IoT Policy, which aims to reach 500 million devices by 2027 and offers subsidies to module makers. Japan trials vehicle-to-infrastructure use cases over 5G standalone networks, while South Korea funds private 5G testbeds that anchor factory automation.

North America and Europe show slower connection growth yet richer revenue per line as enterprises focus on value-added analytics and stringent security certifications. The European Union’s Radio Equipment Directive, effective January 2025, requires all devices to support secure software updates, raising compliance hurdles but boosting trust in connected endpoints. In the United States, FirstNet provides priority lanes for public-safety M2M traffic, tallying 5 million devices by mid-2024.

The Middle East projects the highest CAGR of 8.91% through 2031, fueled by Saudi Arabia’s NEOM deployment of 1 million sensors and Dubai’s smart infrastructure, which cut energy use by 30%. South America sees concentrated adoption of precision agriculture in Brazil and Argentina, aided by subsidies from the Brazilian Ministry of Agriculture. Africa lags in rural coverage, but urban NB-IoT rollouts in South Africa and Egypt are enabling metering and fleet management.

Regulatory Landscape

Regulation for M2M connectivity is tightening around device security, SIM/eSIM provisioning, and supply-chain trust, increasing compliance burdens for operators and device makers alike. In the European Union, the Radio Equipment Directive security provisions effective January 2025 (including secure update requirements) create mandatory cybersecurity-by-design expectations for connected endpoints, while the EU Cyber Resilience Act continues toward full implementation via risk-based product classifications and certification pathways.

In the United States, FCC actions are expanding beyond spectrum and licensing into broader security and market-access controls. The FCC finalized foreign-adversary control attestation requirements that became effective June 9, 2026, and FCC-related Covered List restrictions tightened market access for certain equipment following 2026 Federal Register actions, reinforcing a compliance-driven procurement environment. In Asia-Pacific, regulators are sharpening IoT controls around permanent roaming, licensing, and SIM registration (often extending identity verification), and India has also advanced its critical M2M services framework through TRAI recommendations (April 2025), adding obligations for service continuity, lawful intercept readiness, and lifecycle governance.

Value Chain Analysis

The M2M connections value chain begins with chipset and module suppliers, covering cellular, LPWA, and multi-mode designs that also support satellite. It then moves through secure identity components (SIM/eSIM, eUICC, remote provisioning), device OEMs and integrators, and connectivity providers (MNOs and IoT MVNOs), before reaching cloud and device-management platforms that handle provisioning, security, firmware updates, and analytics. Hyperscale cloud platforms and operator control planes act as an orchestration layer as enterprises scale cloud deployment for fleet-wide management, while security certification regimes and secure-update requirements increasingly influence device BOM decisions and time to market.

Partnership activity shows the chain converging around integrated connectivity, security, and multi-bearer coverage. In 2025, GCT Semiconductor partnered with Globalstar to develop two-way satellite messaging and IoT modules, and it also partnered with Giesecke+Devrient on an SGP.32-compliant eSIM solution, underscoring tighter coupling between radio chipsets and remote SIM provisioning. Connectivity distribution is also becoming more regional, including alliances such as emnify and M2MDataGlobal launching a dedicated SIM offering in Latin America. On the supply side, procurement volatility has been amplified by reported silicon capacity reallocation toward AI-server components, pressuring module availability and pushing OEMs and service providers toward more flexible sourcing and pricing structures.

Competitive Landscape

Market concentration is moderate: the top five operators manage roughly 45% of global connections. Hyperscale clouds bundle connectivity with application services, compressing operator margins and forcing carriers to verticalize. Verizon’s ThingSpace marries connectivity, edge compute, and device management for industrial and fleet customers. Vodafone’s platform spans 190 countries with 175 million lines, leveraging roaming agreements for automotive and logistics deployments.

Module makers are consolidating as Telit absorbed Thales’s M2M business, giving the combined entity a 30% share in automotive telematics modules. Qualcomm filed 47 patents in 2024 around integrated SIM and multi-mode radio designs, underscoring a pivot toward tighter hardware-software integration. Satellite disruptors such as Swarm Technologies, now under SpaceX, offer USD 5 monthly plans for remote assets, undercutting legacy satellite pricing by 80%.

Private 5G gains momentum as Deutsche Telekom and Ericsson connected 8,000 sensors at BMW’s Leipzig plant with 5 millisecond latency, illustrating the push for deterministic industrial networks. Orange Business Services released a multi-IMSI SIM that roams across 180 countries, simplifying fleet operations. As vertical solutions multiply, smaller regional carriers and module suppliers face scale disadvantages, foreshadowing further consolidation in the M2M connections market.

M2M Connections Industry Leaders

AT&T Inc.

Cisco Systems Inc.

Huawei Technologies Co., Ltd.

Intel Corporation

Ericsson AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is the migration path from legacy LTE IoT categories (including Cat-1 and Cat-1bis) toward 5G-era, cost-optimized device profiles that preserve operator-grade manageability. Enhanced RedCap (eRedCap), defined in 3GPP Release 18, is positioned as a practical replacement tier for mid-bandwidth sensors and trackers, offering better power and complexity economics than full 5G while retaining standardized operator support. Module availability from 2026 creates a clear commercialization window for device OEM refresh cycles.

Managed IoT connectivity is also drawing new capital structures and consolidation that can broaden geographic reach and expand platform capabilities. In May 2026, Telenor and Verdane agreed a 50/50 joint ownership structure for Telenor Connexion (valued at SEK 7.5 billion), indicating momentum for operator-linked IoT units that can scale beyond domestic footprints through dedicated investment capacity. In July 2026, M2M Services announced an investment from Atlantic Park (General Atlantic) to support global expansion and M&A, reinforcing the role of specialist aggregators in bundling connectivity, lifecycle management, and compliance services for multinational deployments. In parallel, 3GPP standardization work on Ambient IoT (Release 19 updates finalized at RAN#111 in March 2026) extends the opportunity set for ultra-low-power and potentially battery-less tracking use cases, which remain constrained today by maintenance and power budgets.

Recent Industry Developments

- May 2026: AT&T expanded its collaboration with Wiliot to scale deployments of Wiliot's Physical AI platform for enterprise supply chains. The engagement shifts toward a systems integration and device certification model, with AT&T managing design, installation, asset tagging, and ongoing maintenance. This tightens the linkage between connectivity and field execution for large IoT rollouts.

- March 2026: AT&T announced commercial integration of the Cisco Mobility Services Platform, including IoT Control Center and Converged Core services, into AT&T's 5G Standalone network. Bringing IoT control-plane capabilities closer to 5G SA features such as slicing supports more operator-managed QoS and policy control for vertical M2M deployments.

- April 2024: The FCC adopted the framework for a voluntary IoT Labeling Program that uses the Cyber Trust Mark, aligning participating products with recognized security baselines and testing paths. The program provides a visible security signal for connected devices, influencing procurement criteria and pushing vendors toward more consistent secure-update and vulnerability management practices.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the M2M connections market covers paid and active connectivity links that let machines, sensors, and gateways exchange data without human involvement. Coverage includes both wired and wireless networks, plus the supporting connectivity platforms that manage or enable those active links.

Scope exclusions: We exclude consumer-only device pairing without a managed connection, and we also exclude unrelated IT services that do not directly enable or manage M2M connectivity.

Segmentation Overview

- By Connection Type

- Wired

- Wireless

- By Technology

- Cellular Connections

- Low Power Wide Area (LPWA)

- Short Range

- Metropolitan Area Network (MAN)

- Wide Area Fixed

- Satellite

- By Deployment Model

- On-Premise

- Cloud

- Hybrid

- By End-User Industry

- Retail

- Banking and Financial Institutions

- Telecom and IT

- Healthcare

- Automotive

- Oil and Gas

- Transportation

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public and official references to anchor the demand and supply side of connectivity, such as ITU indicators, OECD telecom statistics, FCC releases, and national telecom regulators and spectrum agencies. We also reviewed standards and ecosystem signals from bodies such as 3GPP and GSMA, plus cybersecurity and device guidance documents from agencies such as NIST where relevant to adoption timing.

To connect the market model to real-world spending, we cross-checked company filings, investor presentations, reputable press, and association websites to understand pricing trends and deployment plans by vertical. In parallel, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to validate product direction and the pace of technology shifts. These desk sources are illustrative, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work relied on interviews and surveys with telecom operators, connectivity platform teams, module and device ecosystem participants, and enterprise users across key verticals such as automotive, utilities, healthcare, retail, and industrial operations. Because adoption differs by geography and network maturity, the respondent input was used to verify connection growth rates, typical pricing ladders, and the timing of technology migrations that desk research cannot fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 16% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing began with a top-down build where connection volumes by region and major end-use were reconstructed from telecom indicators, device adoption cues, and the technology mix. Value was then estimated using an average revenue per connection (ARPC) approach. The ARPC logic was shaped by inputs such as the share of cellular versus LPWA and short-range, the shift from 2G and 3G to LTE-M, NB-IoT, and 5G, typical data plan tiers, and the portion of connections that run on cloud or hybrid deployments.

To keep the totals realistic, we checked the top-down outputs with selective bottom-up approximations, including sampled price-per-connection ranges, channel checks on enterprise contract structures, and supplier-side roll-ups where public disclosures allowed. Where bottom-up visibility was limited, such as smaller private players or bundled connectivity inside wider deals, we used ranges from interviews and applied conservative penetration caps before finalizing totals. Forecasts were produced using scenario analysis supported by a regression view on drivers like connected device growth, network coverage expansion, and vertical digitization timing, and then aligned to expert consensus on pricing pressure and mix changes.

Data Validation & Update Cycle

After the first model run, outputs were compared against independent signals such as telecom subscriber and IoT connection indicators, technology shipment direction, and regional rollout timing, then mismatches were investigated prior to sign-off. When a variance was larger than expected, we revisited assumptions and re-contacted experts to confirm whether the change was structural or largely timing noise.

We use a multi-step internal review to keep logic, units, and currency handling consistent across regions and years. Reports are refreshed annually, and interim updates are made when major events materially change adoption, pricing, or network availability. Before delivery, a final analyst pass ensures clients receive the latest updated view.

Mordor Intelligence's M2m Connections Market Size Compared With Other Published Estimates

Published market values for M2M connections can look far apart because each study makes different choices on what counts as a connection, which technologies are grouped together, and which revenue streams are included. Timing also plays a role, since base years, currency conversion points, and the assumed speed of LTE-M, NB-IoT, and 5G migration can shift totals.

A common gap comes from mixing hardware and software revenues into the same total as connectivity value, or counting device shipments instead of active connections, which can inflate the spending number in early years. Another driver is how wired connections are treated, since some estimates narrow the scope to cellular-only links while others include short-range and fixed wide-area connectivity. The table shows the spread, and it is largely explained by counting wired and wireless connection types across the stated technology set, then validating ARPC ranges with operator and enterprise checks, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.91 B (2026) | |

| Industry Research Group A | USD 30.50 B (2024) | Uses an earlier base year and may reflect a narrower value capture where pricing is anchored to conservative ARPC levels and selected application pools, which can understate newer LPWA and cloud-managed connection value. |

| Market Advisory B | USD 23.92 B (2024) | Includes broader component lines such as hardware and software along with connectivity services, and differences in what is treated as an active connection versus a shipped device can shift the total when compared across years. |

Overall, the comparison points to three practical reasons for differences, which are year selection, what revenue lines are counted, and how connection activity is defined across technologies. By keeping the inputs tied to observable connection growth and cross-checking price assumptions with field feedback, the final number stays traceable to clear variables and repeatable steps that can be re-tested as the market evolves.

Key Questions Answered in the Report

What is the global size of the M2M connections space in 2026 and its projected compound growth to 2031?

It stands at USD 41.91 billion in 2026 and is projected to expand at a 7.24% CAGR to reach USD 59.44 billion by 2031.

Which connection type is most widely adopted today and what drives its dominance?

Wireless links hold 72.33% share because they avoid trenching costs, simplify deployment in remote sites, and benefit from falling module prices.

Which end-user segment is registering the fastest expansion through 2031?

Healthcare posts the highest 8.89% CAGR as remote patient monitoring devices secure regulatory clearance and reimbursement.

Why are low-power wide-area technologies attracting rapid uptake?

NB-IoT and LTE-M enable battery-powered sensors to run for about 10 years, so utilities and municipalities favor them for metering and environmental monitoring.

How does eSIM improve large-scale device rollouts?

Remote profile provisioning lets enterprises ship hardware globally and switch carriers over-the-air, removing physical SIM logistics and cutting inventory complexity.

What security concern poses the greatest short-term risk to growth?

Weak authentication and unpatched firmware expose devices to botnets, as highlighted by 23 CISA advisories on industrial gateways in 2024.

Page last updated on: