North America Lithium-ion Battery For Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

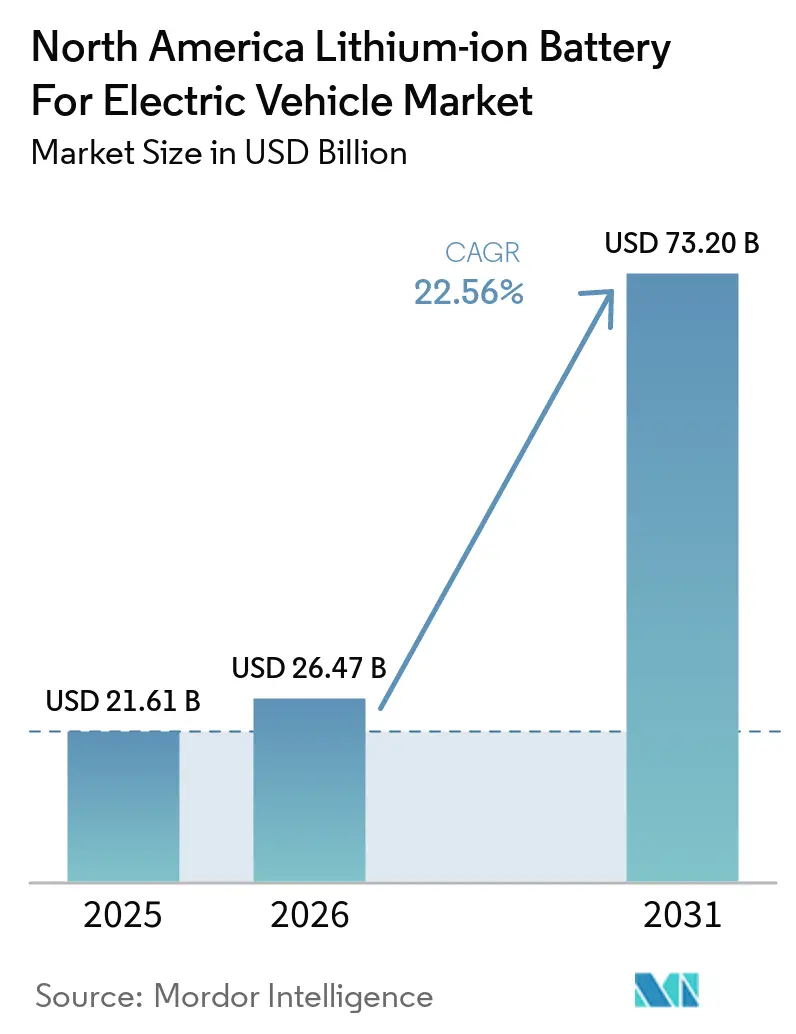

| Base Year Market Size (2025) | USD 21.61 Billion |

| Market Size (2026) | USD 26.47 Billion |

| Market Size (2031) | USD 73.20 Billion |

| Growth Rate (2026 - 2031) | 22.56% CAGR |

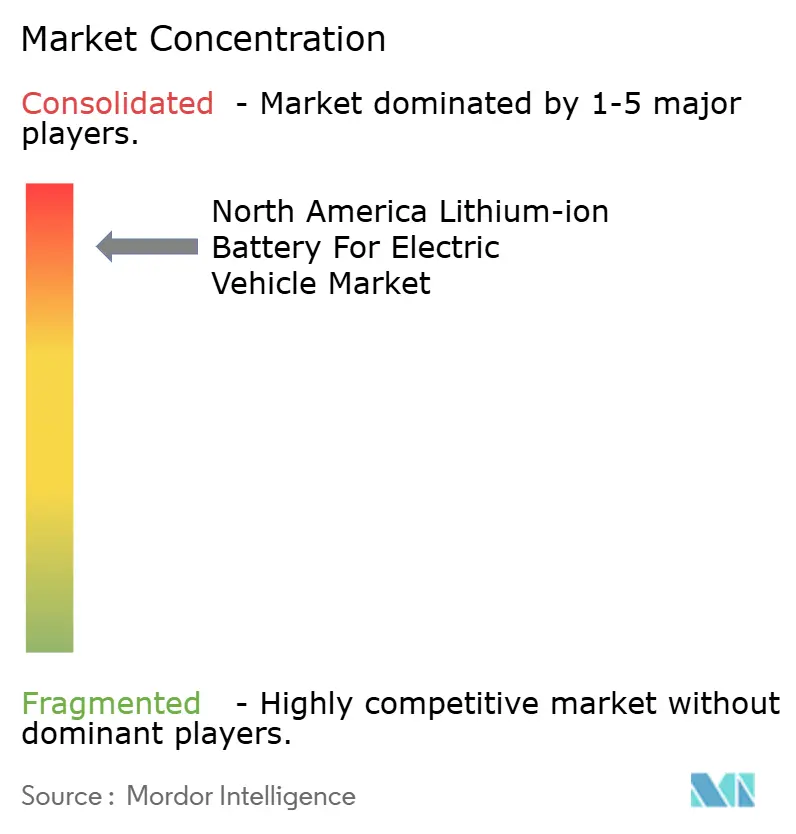

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Lithium-ion Battery For Electric Vehicle Market Analysis by Mordor Intelligence

The North America Lithium-ion Battery For Electric Vehicle Market size is projected to be USD 21.61 billion in 2025, USD 26.47 billion in 2026, and reach USD 73.20 billion by 2031, growing at a CAGR of 22.56% from 2026 to 2031. This growth is supported by a sharp fall in pack-level costs, which moved down to USD 95 to USD 115 per kWh in 2026, while Section 45X continues to support domestic cell and module output through per-kWh production credits.[1]Ray Cai and Jane Nakano, “A New Phase for the U.S. Battery Industry,” Center for Strategic and International Studies, csis.org The North America EV lithium-ion battery market is also changing because LFP is now moving into mass-market EV programs alongside NMC and NCA, which broadens the chemistry mix instead of leaving premium platforms as the only major demand base. The North America EV lithium-ion battery market is gaining another source of demand from medium and heavy trucks, where series production is lifting battery value per vehicle well above passenger car pack sizes. The United States remains the center of the regional supply chain, while Canada is strengthening cell production and materials processing, and Mexico is building around EV assembly and battery pack activity under USMCA-linked manufacturing flows. Competition remains moderate because the leading battery producers still account for a large share of regional output, but chemistry shifts, application shifts, and new plant ramps continue to keep share positions open inside the North America EV lithium-ion battery market.

Key Report Takeaways

- By battery chemistry, lithium-ion chemistries held 90.9% of revenue in 2025, while emerging chemistries are forecast to expand at 34.1% through 2031.

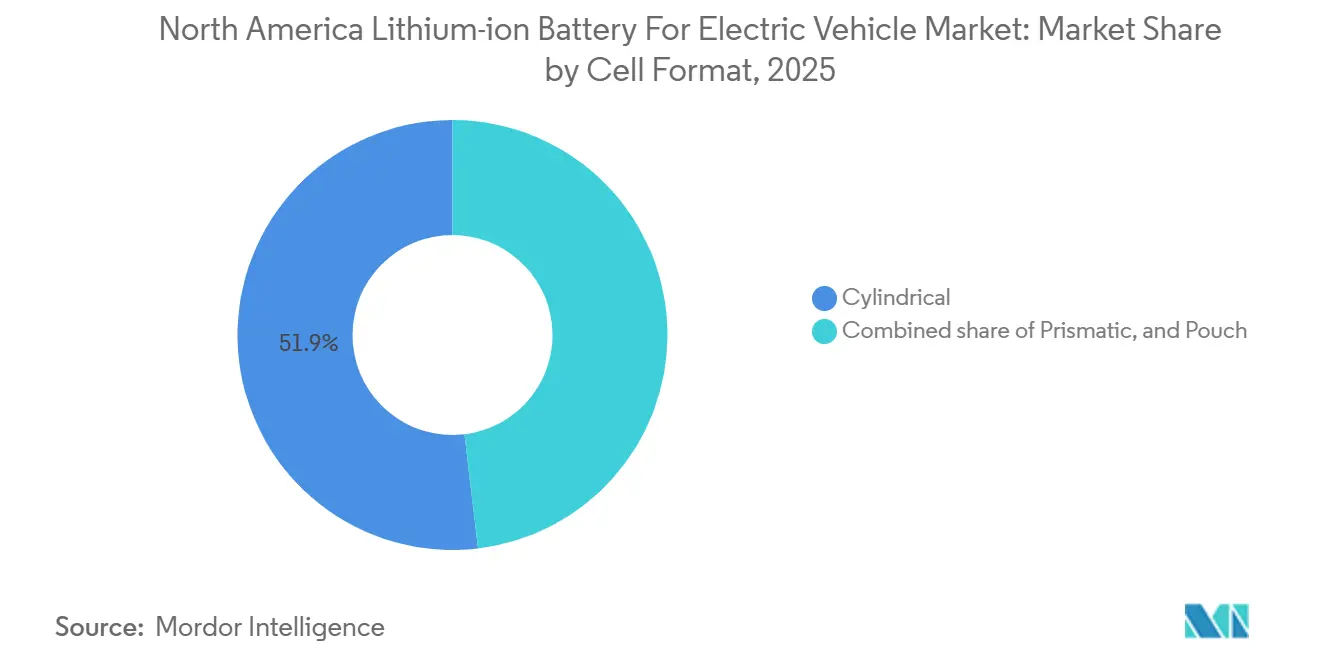

- By cell format, cylindrical cells held 51.9% of revenue in 2025, while prismatic cells are projected to grow at 25.3% through 2031.

- By propulsion, BEVs accounted for 63.2% of revenue in 2025 and are also forecast to record the highest CAGR at 23.1% through 2031.

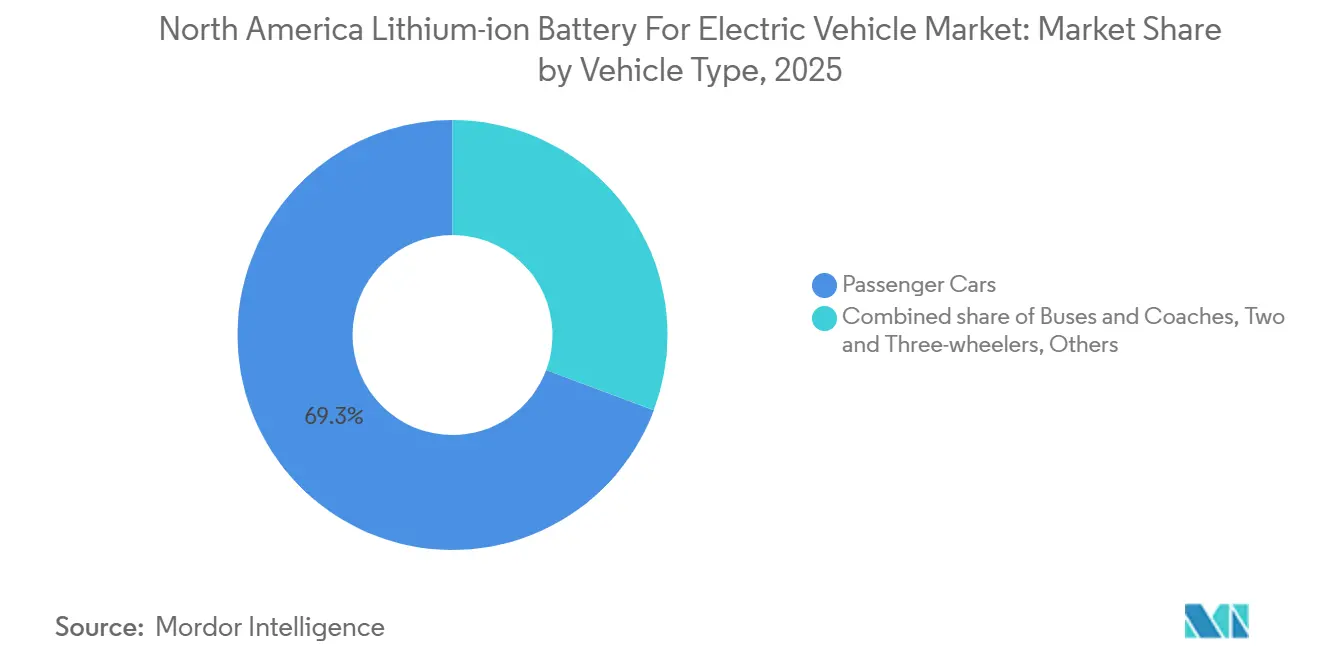

- By vehicle type, passenger cars held 69.3% of revenue in 2025, while medium and heavy trucks are projected to expand at 27.6% through 2031.

- By geography, the United States held 79.2% of revenue in 2025, while Mexico is forecast to grow at 30.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on lithium-ion battery for electric vehicle market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Lithium-Ion Battery Prices | +5.2% | Global, concentrated impact in US and Canada OEM supply chains | Short term (≤ 2 years) |

| Growing EV Model Availability and Purchase Incentives | +4.8% | United States, Canada, early spill-over to Mexico | Short term (≤ 2 years) to Medium term (2-4 years) |

| Scale-Up of North American Cell Manufacturing Capacity | +4.5% | US Midwest and Southeast, Ontario in Canada, Northern Mexico | Medium term (2-4 years) |

| OEM-Battery Maker Long-Term Offtake Agreements | +3.2% | US and Canada, linked to IRA domestic-content thresholds | Medium term (2-4 years) to Long term (≥ 4 years) |

| Breakthroughs in High-Silicon Anodes | +1.8% | US, especially California and Michigan, with spill-over to Canada | Long term (≥ 4 years) |

| Second-Life Battery Leasing Models for Fleets | +1.2% | US fleet corridors and major Canadian urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Prices Compressing Cost Barriers

The North America EV lithium-ion battery market is seeing its strongest cost support from the continued fall in battery pack prices. Pack-level costs fell from near USD 300 per kWh in 2018 to USD 95 to USD 115 per kWh in 2026, which improves vehicle affordability and eases pressure on automaker margins.[2]Ray Cai and Jane Nakano, “A New Phase for the U.S. Battery Industry,” Center for Strategic and International Studies, csis.org The benefit is still uneven because US-made LFP cells remain more expensive than the Chinese supply, even after production credits narrow part of the gap for local manufacturing economics. That cost spread is pushing the North America EV lithium-ion battery market toward wider LFP adoption in mid-range vehicles and work fleets, where price sensitivity is stronger than in premium passenger programs. GM has stated that shifting from NMC to LFP in part of its portfolio could lower battery cost by at least USD 6,000 per vehicle, which shows how chemistry choice now affects retail pricing as much as vehicle engineering. Lower new-cell prices are also making second-life reuse less attractive in some cost-sensitive fleet applications, which increases the appeal of direct recycling instead of long reuse chains for retired packs.

Growing EV Model Availability and Purchase Incentives Broadening Addressable Demand

The North America EV lithium-ion battery market is benefiting from a wider range of EV models across passenger and commercial categories. Electric medium and heavy-duty vehicle model availability rose from 24 models in 2019 to 161 models by 2025, which materially broadened purchasing options for fleet operators and public buyers. This wider product base is reinforcing battery demand because more duty cycles can now be matched with dedicated electric platforms rather than limited pilot models. California’s Advanced Clean Cars II rule and its adoption by additional states are keeping regulatory demand visible into the next decade, which reduces the risk of a short-lived demand spike in the North America EV lithium-ion battery market. The end of the Section 30D consumer credit in September 2025 changed the demand mix, yet commercial operators still retain access to leasing-related support, which has helped fleet electrification hold up better than expected. That shift matters because fleet demand usually involves larger batteries, repeat ordering behavior, and clearer replacement cycles than private retail demand, which gives the North America EV lithium-ion battery market a steadier volume base.

Scale-Up of North American Cell Manufacturing Capacity Creating Supply-Side Density

The North America EV lithium-ion battery market is being reshaped by the rapid expansion of domestic cell manufacturing capacity. Regional battery cell capacity is on track to reach 800 to 1,000 GWh annually by 2030 from nearly 120 GWh in 2025, which points to a far denser local supply base within a short period. Panasonic’s De Soto, Kansas, facility entered mass production in July 2025 with an initial annual capacity of 32 GWh and produces 70 batteries per second, which shows how large-format industrial scaling is moving from plan to execution.[3]“Panasonic Energy Begins Mass Production at New Automotive Lithium-Ion Battery Factory in Kansas, Aiming for Annual Capacity of 32 GWh to Accelerate U.S. Local Production,” Automotive World, automotiveworld.com The Accelera, Daimler Truck, and Paccar joint venture is also building a 21 GWh LFP factory in Mississippi for commercial vehicles, which shows that the North America EV lithium-ion battery market is no longer centered only on passenger car programs.[4]Ryan Gehm, “Betting Big on LFP Battery Cells for Electric Commercial Vehicles,” Mobility Engineering Technology, mobilityengineeringtech.com More local production shortens lead times, reduces freight exposure, and lowers dependence on imported cells that face very high duties when sourced from China. This build-out is improving supply visibility for OEMs, but it is also raising the need to keep plants flexible enough to switch across chemistries and applications when end-market demand changes.

OEM-Battery Maker Long-Term Offtake Agreements Locking in Supply Visibility

The North America EV lithium-ion battery market is increasingly organized around long-term supply contracts between automakers and battery manufacturers. These agreements reduce supply risk for OEMs and give battery makers the demand visibility needed to justify multi-billion-dollar plant investments. SK On’s March 2025 agreement to supply nearly 100 GWh of high-nickel batteries to Nissan from 2028 to 2033 shows how these contracts are now setting future capacity allocation years before production begins. LG Energy Solution’s December 2025 agreement with Mercedes-Benz serves the same purpose by linking future North American output to an identified customer base across several years. Section 45X strengthens this pattern because the tax benefit is claimed by the domestic manufacturer, which gives producers a clear reason to secure volume before expanding output. Another effect is that chemistry choices are being locked in well ahead of production, with premium and long-range programs still leaning toward high-nickel chemistries while cost-focused vehicles move toward LFP in the North America EV lithium-ion battery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Supply Bottlenecks for Class-1 Nickel | -2.8% | US-wide, concentrated in NMC-dependent cathode supply chains | Medium term (2-4 years) |

| Slow Permitting of New North American Lithium Projects | -1.8% | Western US, Manitoba, Quebec | Long term (≥ 4 years) |

| Recycling Regulatory Uncertainty Beyond California | -0.9% | US outside California, Canada outside Quebec | Medium term (2-4 years) |

| Thermal-Runaway Reputation Risk After High-Profile Fires | -1.2% | US and Canada, strongest in dense urban fleet deployments | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Supply Bottlenecks for Class-1 Nickel Constraining NMC Economics

The North America EV lithium-ion battery market remains exposed to imported Class-1 nickel, which keeps a key input risk in place for high-nickel cathode chemistries. The United States holds less than 3% of global nickel processing capacity, and its only operating nickel mine in Michigan was expected to cease production by the end of 2025, which raises dependence on external supply. Indonesia already dominates global nickel production, and much of that material is tied to Chinese-affiliated processing, which creates IRA eligibility problems under FEOC-related restrictions. As a result, the North America EV lithium-ion battery market is seeing a stronger cost case for LFP in mid-range applications, even when NMC still offers better energy density for premium models. Canada and the United States are trying to improve local supply links, but project timing and scaling remain uncertain enough that nickel will stay a constraint over the medium term.

Thermal-Runaway Reputation Risk Elevating Safety Engineering Requirements

The North America EV lithium-ion battery market still faces safety concerns tied to thermal-runaway incidents, especially in dense fleet and transit settings where a single event can affect adoption decisions. The US EPA is developing an Extended Producer Responsibility framework for batteries, and the active consultation process is creating compliance uncertainty for producers that have not yet aligned with expected end-of-life and safety obligations. California’s stewardship program, with producer participation required in approved plans by April 2027, is likely to shape how other states approach battery handling and reporting rules. This safety discussion is also affecting chemistry choices inside the North America EV lithium-ion battery market because fleet buyers are giving more weight to LFP in buses, delivery vehicles, and other duty cycles where pack-level thermal behavior matters. The issue does not stop adoption, but it raises engineering, certification, and insurance demands and therefore increases execution pressure on manufacturers that are scaling high-energy battery systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: LFP Gains Ground While NMC Keeps the Premium Position

Lithium-ion chemistries held 90.9% of revenue in 2025, which placed this segment at the center of the North America EV lithium-ion battery market size in the base year. The North America EV lithium-ion battery market still relies on NMC for premium passenger EVs because long-range platforms continue to prioritize high energy density. NCA also remains relevant in selected high-performance applications, especially where cylindrical formats and proven production lines already exist. LFP is expanding quickly in mid-range passenger vehicles and commercial platforms because its lower cost and stronger perceived safety profile match the needs of higher-volume programs. GM and LG Energy Solution are moving US capacity toward LFP production, which shows that announced plant plans are now being revised around practical cost targets rather than only technical range goals.

Lead-acid and nickel-metal-hydride chemistries still have small roles in mild-hybrid and auxiliary systems, but their position is weakening as low-voltage architectures increasingly shift toward lithium-ion support. Emerging chemistries held only a minimal revenue share in 2025, yet they are projected to expand at 34.1% through 2031, which makes them the fastest-growing chemistry group in the North America EV lithium-ion battery market. Nissan stated in April 2026 that its 23-layer solid-state prototype pack met charge and discharge benchmarks and remains aimed at a 2028 launch at a USD 75 per kWh pack cost, which keeps solid-state progress visible even before mass commercialization. At the same time, lithium-manganese-rich development at GM and Ford could broaden the future chemistry set before solid-state reaches large-scale production, which means the market is likely to remain mixed rather than settle around a simple two-chemistry structure

By Cell Format: Cylindrical Cells Lead While Prismatic Expands Faster

Cylindrical cells claimed 51.9% of the North America EV lithium-ion battery market share in 2025, which kept them in the lead across cell formats. The North America EV lithium-ion battery market has favored cylindrical formats because Panasonic built large-scale 2170 production in Nevada and then extended that base through De Soto, Kansas. Tesla’s 4680 cell strategy also supports this position because the format is tied to its heavy vehicle and pickup programs, which require high output and a proven domestic manufacturing path. Pouch cells still retain a role where custom packaging and platform-specific layouts matter, and several joint-venture programs continue to use them in passenger EV architectures. That said, the present lead for cylindrical cells does not remove the growing structural appeal of prismatic designs in the North America EV lithium-ion battery market.

Prismatic cells are forecast to expand at 25.3% through 2031, which makes them the fastest-growing format segment. This growth reflects three linked shifts, namely broader LFP adoption, increasing use of cell-to-pack designs, and rising commercial vehicle demand, where modular pack logic is easier to implement with prismatic cells. Volkswagen’s PowerCo plant in St. Thomas is being built around the Unified Cell in prismatic format with a targeted 90 GWh annual capacity, which gives the region a major future source of local prismatic output VW.CA. The upcoming USMCA review could further favor producers that already manufacture prismatic cells inside the trade bloc, because rules-of-origin compliance is becoming as important as pure manufacturing scale in the North America EV lithium-ion battery market.

By Propulsion: BEVs Hold the Core While EREVs Add a New Path

Battery electric vehicles accounted for 63.2% of the North America EV lithium-ion battery market size in 2025 and are forecast to grow at 23.1% through 2031, which keeps BEVs as both the largest and fastest-growing propulsion segment. The North America EV lithium-ion battery market remains anchored by BEVs because they carry much larger packs than HEVs and PHEVs, which lifts battery revenue per vehicle even when vehicle unit shares are less uneven. Regulatory support also matters because state-level zero-emission vehicle rules continue to create a predictable demand path for full battery electric models. PHEVs and HEVs still hold space in pickups and SUVs where towing, charging access, and range confidence remain important purchase factors. This keeps a diversified propulsion mix in place even as BEVs remain the main revenue engine for the North America EV lithium-ion battery market.

A notable development is the rise of the extended-range EV as a practical middle path between full BEVs and traditional hybrids. EREVs with battery capacity near 40 kWh can deliver long total driving range while using far less battery material than a pure BEV, which gives manufacturers another way to manage cost and consumer range concerns. SK On started mass production of Korea’s first EREV NCM pouch batteries in the second half of 2026, which shows that battery makers are already preparing for this architecture even if it remains small in North America today. The segment does not alter the near-term lead of BEVs, but it could absorb some demand from buyers who want electric driving with lower pack cost and less dependence on a dense charging network.

By Vehicle Type: Passenger Cars Lead While Heavy Trucks Accelerate

Passenger cars accounted for 69.3% of the North America EV lithium-ion battery market size in 2025, which reflects the earlier and broader electrification of personal mobility platforms. The North America EV lithium-ion battery market still draws most of its current revenue from passenger cars because they combine the highest production scale with the largest number of qualified battery supply programs. Light commercial vehicles add a second layer of demand as delivery fleets and work vehicles move into electrification, especially where daily routes are predictable, and depot charging is easier to manage. Buses and coaches remain smaller in value, but they have regulatory support in public transit programs, which gives them a steadier floor than many other commercial categories. This mix keeps current revenue concentrated in passenger vehicles even as commercial applications become more important across the North America EV lithium-ion battery market.

Medium and heavy trucks are projected to grow at 27.6% through 2031, which is the highest CAGR among vehicle types in this market. Tesla began series production of the Semi in April 2026 with an 822 kWh long-range pack, which sharply increases battery demand per unit compared with passenger EVs. Kenworth, Peterbilt, and Volvo are also expanding battery-electric truck offerings, which confirms that heavy-duty electrification is moving past the pilot phase and into commercial procurement cycles. As that shift continues, the North America EV lithium-ion battery market will see more value tied to a smaller number of very large packs, which changes both product planning and plant utilization across the supply chain.

Geography Analysis

The United States held 79.2% of the North America EV lithium-ion battery market share in 2025, which made it the clear center of regional demand and production. The North America EV lithium-ion battery market is most deeply rooted in the United States because the country has the largest gigafactory pipeline, the broadest OEM base, and the strongest mix of public support measures. Thirteen new US plants secured Department of Energy loan offers in 2024, and total domestic manufacturing capacity is on track to reach 800 to 1,000 GWh annually by 2030. A defining feature of the US market is that battery factories are now serving both EVs and stationary storage, which lets producers reallocate output when one demand stream softens. This helps preserve factory use and tax credit economics, but it also makes vehicle supply planning less certain in the North America EV lithium-ion battery market.

Canada holds a smaller share of demand, but its role in the North America EV lithium-ion battery market is becoming more important because it connects mineral processing, cathode materials, and new cell manufacturing. NextStar Energy in Windsor opened in early 2026 and became Canada’s first large-scale battery cell plant after passing 1 million cells in production. PowerCo’s St. Thomas gigafactory remains on track for 2027 production and is designed around prismatic cells at up to 90 GWh per year, which strengthens Canada’s future role in local supply. Canada is also building out upstream processing through projects such as Mangrove Lithium in British Columbia and the broader Bécancour battery cluster in Quebec, although some materials projects have faced cost overruns and schedule pressure.

Mexico is forecast to expand at 30.9% through 2031, which makes it the fastest-growing country in the North America EV lithium-ion battery market. The growth case is tied more to EV assembly and battery pack integration than to domestic cell production, because Mexico still does not manufacture lithium-ion cells at scale. BMW is investing nearly USD 900 million in San Luis Potosí for high-voltage battery assembly and EV output from 2027, while Kia committed USD 600 million in Nuevo León for EV manufacturing and related infrastructure. The main gap is still local cell supply, which means Mexico remains exposed to policy uncertainty and cross-border investment decisions even as it becomes more important to the regional manufacturing map.

Mordor Intelligence provides coverage of the lithium-ion battery for electric vehicle market across other key regional markets, including Asia, Middle East and Africa, and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to France and United Kingdom incorporating local coverage and market participation, as required.

Competitive Landscape

The North America EV lithium-ion battery market is moderately concentrated, with LG Energy Solution, Panasonic, SK On, Samsung SDI, and Ultium Cells as the major players. That structure gives the leading group real scale advantages in procurement, plant utilization, and customer access, but it does not close the field to shifts in chemistry or end-use focus. Korean suppliers remain central because they combine joint ventures with automakers and stand-alone capacity that can be redirected across programs when needed. Panasonic continues to anchor the cylindrical side of the North America EV lithium-ion battery market through Nevada and Kansas, where large-scale local output supports both established and next-generation formats. The balance of power is therefore shaped as much by manufacturing flexibility as by current market share.

A clear strategic move came from LG Energy Solution, which converted part of its Lansing plan toward LFP energy storage supply for Tesla’s Megapack program when stationary storage demand strengthened. Another came from SK On, which secured a long-term supply agreement with Nissan and tied future North American output to an identified customer program several years before start of delivery. Panasonic’s Kansas ramp is a third example because it expands local cylindrical output at a time when heavy vehicthe les and new cell sizes are raising the need for trusted volume production. These moves show that the North America EV lithium-ion battery market is being contested through capacity decisions, customer contracts, and chemistry positioning rather than through price alone.

There is also room for change below the top tier. Samsung SDI is positioning around prismatic LFP and storage-linked growth, while Solid Power and other development-stage players are trying to build relevance through next-generation cell platforms. The domestic gap in prismatic LFP supply remains notable, which means format specialization could still open space for newer entrants or expanding incumbents in the North America EV lithium-ion battery market. Smaller companies such as Microvast and Farasis are more likely to find traction in commercial fleets and specialized applications where product fit matters more than pure scale. As a result, leadership is visible but not fixed, and the competitive picture will continue to change as producers adjust to vehicle demand, storage demand, and chemistry transitions.

North America Lithium-ion Battery For Electric Vehicle Industry Leaders

Panasonic Holdings Corporation

LG Energy Solution Ltd.

Contemporary Amperex Technology Co. Limited

SK On

Samsung SDI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tesla began series production of the Class 8 Tesla Semi at Gigafactory Nevada, with the long-range variant featuring an 822 kWh battery pack using 4680 NCMA cells and volume targeting many thousands of units in 2026, with a 50,000-unit per year capacity long term. The USD 290,000 price point resets segment cost benchmarks for zero-emission Class 8 trucks.

- April 2026: The Canadian federal government supported Mangrove Lithium's inauguration of North America's first commercial electrochemical lithium refining facility in Delta, British Columbia, backed by up to CAD 21.9 million, which is approximately USD 15.9 million at 2026 exchange rates, from the Critical Minerals Research, Development and Demonstration Program. The facility targets output for nearly 25,000 EVs annually.

- February 2026: Canada's first large-scale battery plant, NextStar Energy in Windsor, Ontario, a nearly USD 5 billion facility now fully owned by LG Energy Solution after acquiring Stellantis' 49% stake, officially opened after reaching 1 million cells in production and creating 1,300 jobs .

- October 2025: PowerCo, Volkswagen's battery arm, began construction of first buildings at its USD 7 billion gigafactory in St. Thomas, Ontario, with foundation work underway using more than 32,000 cubic metres of concrete and production targeted for 2027 at up to 90 GWh annual capacity.

North America Lithium-ion Battery For Electric Vehicle Market Report Scope

A lithium-ion battery for electric vehicles (EVs) is a type of rechargeable battery commonly used to power electric cars and other electric transportation. Known for its high energy density, long cycle life, and lightweight design, this battery technology enables efficient storage and delivery of electrical energy. Lithium-ion batteries consist of cells containing an anode, cathode, separator, and electrolyte. These batteries offer a high power-to-weight ratio, excellent energy efficiency, and reduced self-discharge compared to other battery types, which make them a top choice for modern electric vehicles.

The North America Lithium-Ion Battery for EV Market is segmented into battery chemistry, cell format, propulsion, vehicle type, and geography. By battery chemistry, the market is segmented into lithium-ion, emerging chemistries, lead-acid, and nickel-metal-hydride batteries. By cell format, the market is segmented into cylindrical, prismatic, and pouch cells. By propulsion, the market is segmented into BEV, PHEV, and HEV. By vehicle type, the market is segmented into passenger cars, LCVs, medium and heavy trucks, buses, and two and three-wheelers. The report also covers the market size and forecasts for the lithium-ion battery for EV market across key countries in North America, including the United States, Canada, and Mexico. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Cylindrical |

| Prismatic |

| Pouch |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| United States |

| Canada |

| Mexico |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) | |

| Lead-acid | |

| Nickel-metal-hydride | |

| By Cell Format | Cylindrical |

| Prismatic | |

| Pouch | |

| By Propulsion | Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Hybrid Electric Vehicle (HEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks | |

| Buses and Coaches | |

| Two and Three-wheelers | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the expected value of the North America EV lithium-ion battery market by 2031?

The North America EV lithium-ion battery market is forecast to reach USD 73.20 billion by 2031 from USD 26.47 billion in 2026, at a 22.56% CAGR.

Which battery chemistry currently leads regional demand?

Lithium-ion chemistries, mainly NMC, NCA, and LFP, held 90.9% of revenue in 2025, which keeps them far ahead of other chemistry categories.

Why is LFP gaining traction in North America EV batteries?

LFP is gaining traction because lower pack costs and better safety perception matter more in mass-market cars, fleets, and commercial vehicles, especially as domestic producers shift planned capacity toward LFP programs.

Which country leads regional demand today?

The United States led with 79.2% of regional revenue in 2025 because it has the largest gigafactory base, the broadest OEM ecosystem, and the strongest policy support structure.

Which vehicle segment is growing the fastest?

Medium and heavy trucks are projected to record the highest CAGR at 27.6% through 2031, supported by rising commercial production and very large battery pack sizes per vehicle.

What is the main supply-side challenge for high-nickel batteries in North America?

Imported Class-1 nickel remains a major constraint because local processing capacity is limited and FEOC-related rules complicate access to some foreign supply chains.

Page last updated on: