Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

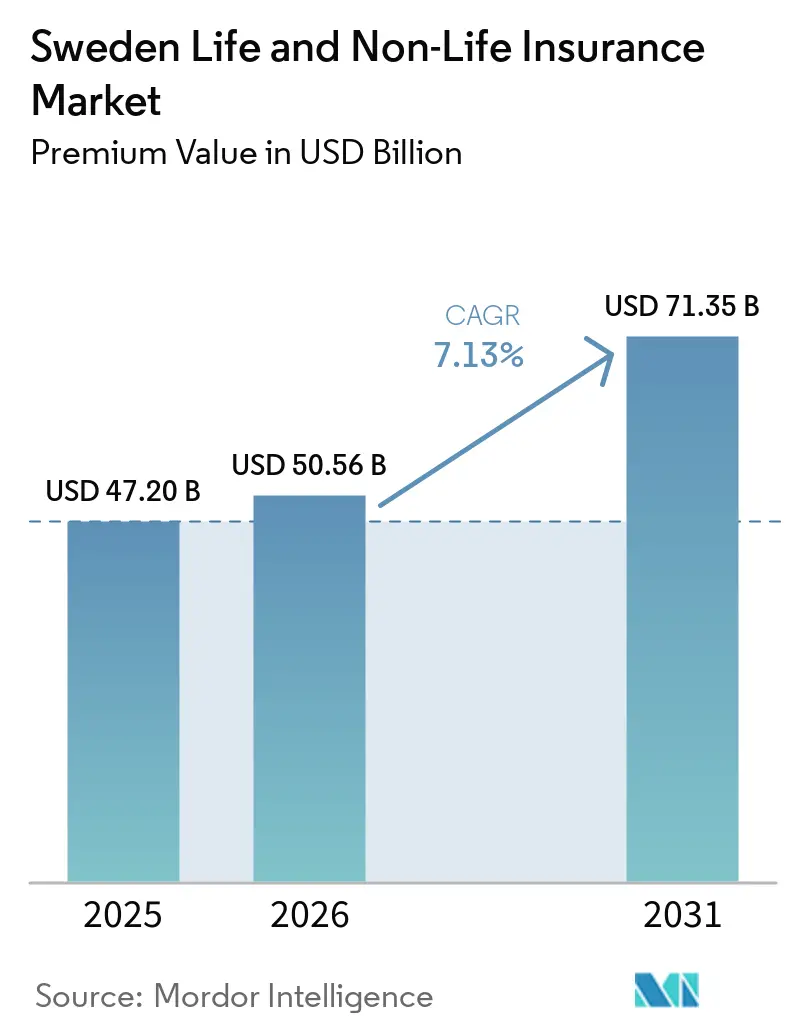

| Base Year Market Size (2025) | USD 47.20 Billion |

| Market Size (2026) | USD 50.56 Billion |

| Market Size (2031) | USD 71.35 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

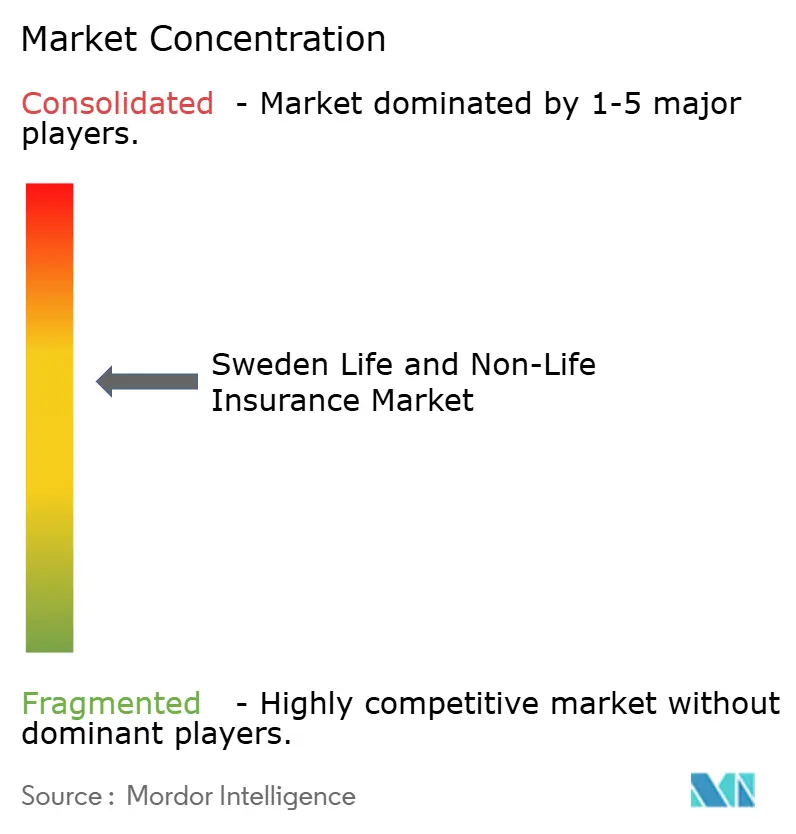

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Sweden Life And Non-Life Insurance Market size in terms of premium value is expected to grow from USD 47.20 billion in 2025 to USD 50.56 billion in 2026 and is forecast to reach USD 71.35 billion by 2031 at 7.13% CAGR over 2026-2031.

Sweden's life and non-life insurance market thrives on a robust foundation, bolstered by near-universal household insurance coverage, a strong digital infrastructure, and a stable macroeconomic backdrop. Traditional mutual insurers like Folksam and Länsförsäkringar grapple with nimble Insurtech challengers, such as Hedvig. These challengers leverage mobile-first user experiences and forge strategic affinity partnerships, driving the market's evolution. Key growth catalysts include the swift rise of unit-linked life insurance products, a surge in embedded insurance adoption via digital platforms, and a heightened demand for cyber-risk coverage, especially among SMEs wary of GDPR repercussions. Concurrently, challenges like climate-induced property losses and stringent Solvency II capital mandates push insurers towards data-centric pricing models, diversified investment strategies, and accelerated product innovation, ensuring they stay competitive in a rapidly shifting landscape.

Key Report Takeaways

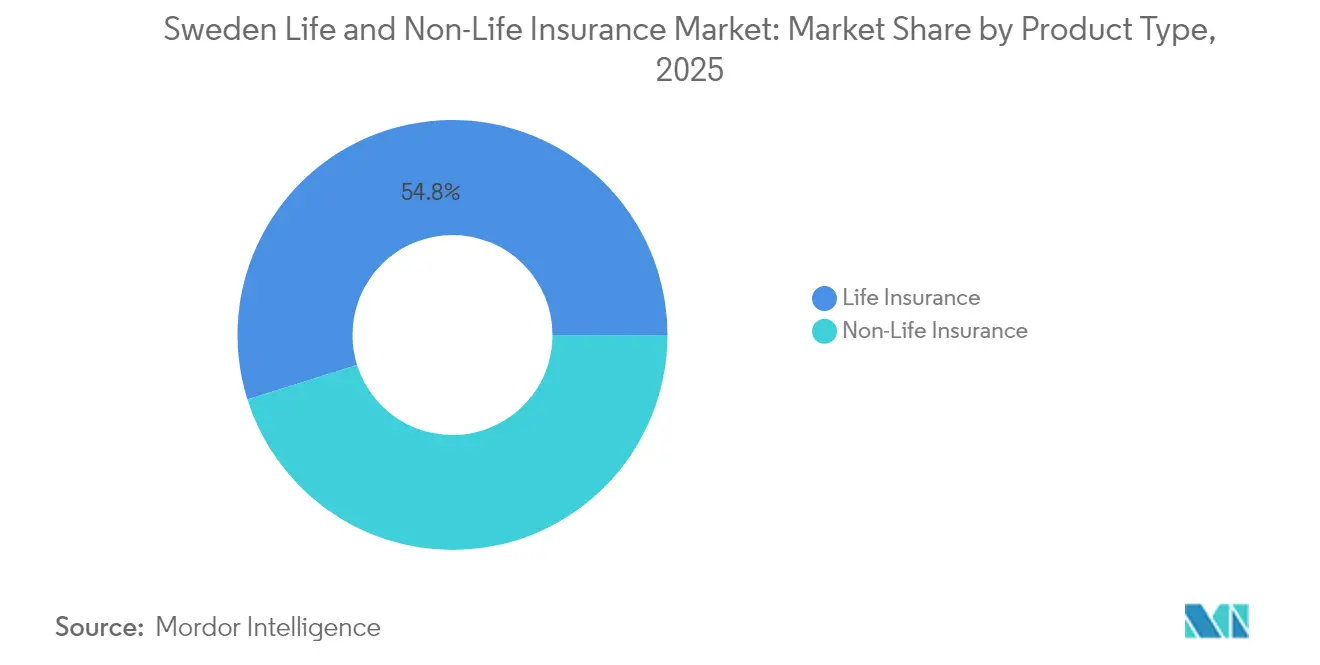

- By Product type, life insurance led with 54.84% revenue share in 2025, while unit-linked life is expanding at a 7.65% CAGR through 2031.

- By Distribution channel, direct sales captured 39.08% of the Sweden life and non-life insurance market share in 2025; embedded and affinity partnerships are projected to rise at an 11.11% CAGR till 2031.

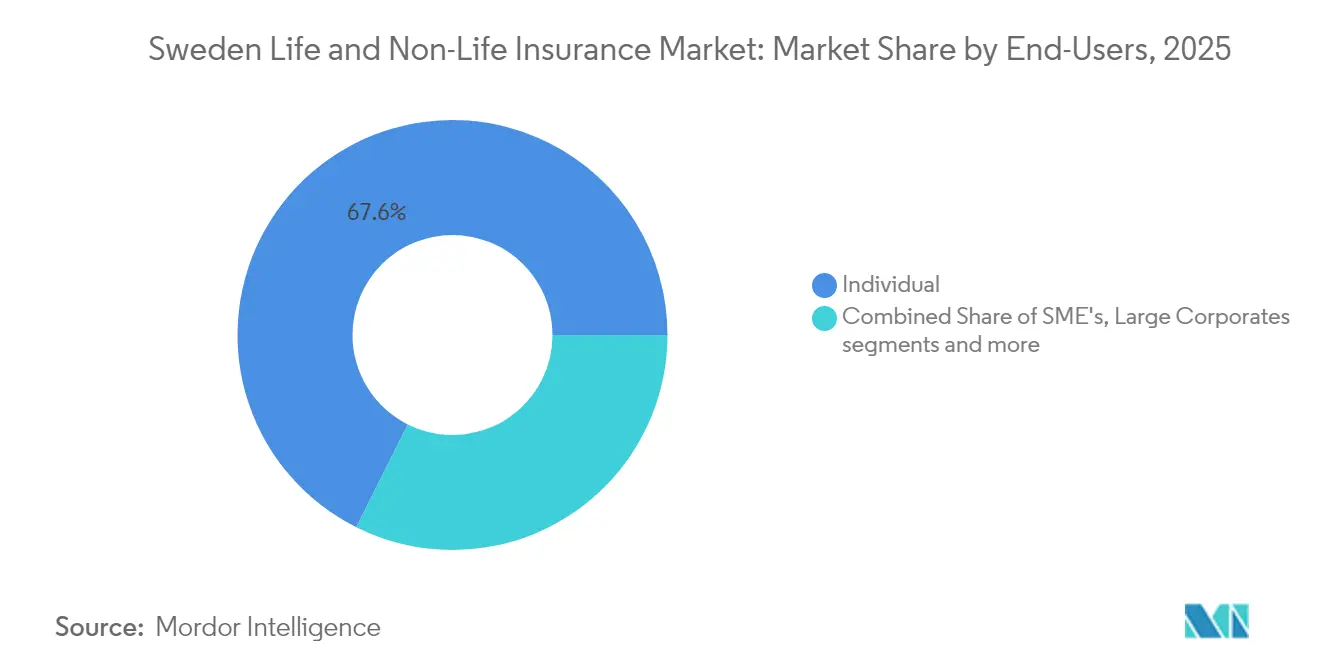

- By End-user, individual consumers held 67.62% of the Sweden life and non-life insurance market size in 2025, whereas SMEs posted the fastest 8.36% CAGR to 2031.

- By Premium type, regular premiums dominated with a 62.15% share in 2025, while single-premium products are forecast to grow at a 6.08% CAGR till 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid pension products amid premium-pension reform | +1.2% | Götaland & Svealand | Medium term (2-4 years) |

| Unit-linked life supported by prolonged negative rates | +1.5% | Urban centers nationwide | Short term (≤ 2 years) |

| Cyber-risk cover demand among SMEs | +0.8% | Stockholm & Gothenburg districts | Medium term (2-4 years) |

| Embedded insurance via neobanks and e-commerce | +1.1% | Digitally mature regions | Short term (≤ 2 years) |

| Ageing population fuelling long-term-care & funeral covers | +0.9% | Rural Norrland | Long term (≥ 4 years) |

| Electrification of vehicle fleet boosting e-mobility motor covers | +0.7% | Early adoption in Götaland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Hybrid Pension Products Amid Premium-Pension Reform

Hybrid schemes that blend guaranteed benefits with market-linked upside are gaining ground as Sweden consolidates its AP buffer funds, lowers administrative costs, and grants AP2 wider latitude to invest in unlisted assets until 2036[1]European Pensions editorial team, “Sweden Merges AP Funds to Unlock Private Market Exposure,” europeanpensions.net. Transfer activity is climbing—SEK 26 billion moved in Q1 2024 alone—as workers seek flexibility and potentially stronger returns. With 90% of employees holding occupational pensions that are now portable, insurers are redesigning products to meet demand for security plus growth. AMF’s conversion of SEK 5.6 billion of surplus into strengthened guarantees while still posting 7.1% returns illustrates how hybrid designs appeal in the Sweden life and non-life insurance market.

Growth of Unit-Linked Life Supported by Prolonged Negative Rates

Sweden's insurance landscape is evolving. Traditional life insurance products are losing their luster, thanks to a combination of prolonged low interest rates and tax policies. In 2024, a 1.086% yield tax on life policies, coupled with a robust equity market and persistently low bond yields, has hastened the shift towards unit-linked life insurance products. Unlike their traditional counterparts, these unit-linked products tie policyholders directly to market performance, sidestepping the return compression that plagues guaranteed offerings. For instance, AMF's unit-linked accounts boasted impressive returns of 13.9%, prompting a notable asset reallocation. Currently, assets in unit-linked funds stand at SEK 235.3 billion (USD 22.4 billion), while traditional life portfolios command SEK 613 billion (USD 58.4 billion).

Young savers, in particular, are gravitating towards these unit-linked products, drawn by the promise of higher long-term returns. With the Riksbank likely to maintain its policy rate around 2%, keeping bond yields below historical norms, this trend towards growth-focused unit-linked products is set to continue at least until 2025. This shift signals a broader transformation within Sweden's insurance market, extending beyond just the life insurance segment.

Rising Demand for Cyber-Risk Cover Among Swedish SMEs (GDPR Exposure)

As regulatory and financial pressures mount, small and mid-sized enterprises (SMEs) in Sweden are increasingly turning to cyber-risk coverage, driving momentum in the country's non-life insurance sector. The EU's General Data Protection Regulation (GDPR) imposes fines of up to 4% of annual turnover for data breaches, fueling a heightened demand for customized cyber insurance. In Sweden's digitally progressive economy, cyber policies have emerged as vital risk management instruments, particularly for SMEs. Annual premiums for these policies generally fall between SEK 5,000 and SEK 10,000 (USD 475–950) for every SEK 1 million (approximately USD 95,000) of coverage. Such pricing structures underscore the evolving nature of Sweden's cyber insurance market, where underwriters are increasingly incorporating IT-security scoring into their actuarial risk evaluations. As a result, cyber-risk coverage is set to become a cornerstone of non-life insurance portfolios, influencing product offerings and underwriting approaches throughout Sweden's insurance sector[2]Swiss Re Institute, “Insurance Digitalization Index 2024: Sweden Retains #2 Spot,” swissre.com.

Rapid Expansion of Embedded Insurance via Neobanks & E-commerce

In Sweden, neobanks and e-commerce platforms are spearheading the rapid rise of embedded insurance, reshaping both the life and non-life insurance markets. These platforms seamlessly weave real-time, customized policies into their digital checkout and payment processes. Thanks to Sweden's cutting-edge open-finance infrastructure and swift payment systems, these "just-in-time" insurance offerings not only boost customer conversions but also slash acquisition costs. A testament to this trend is SEB's strategic partnerships. Moreover, the Riksbank's ongoing e-krona pilot underscores Sweden's dedication to fluid digital transactions. This commitment paves the way for embedded insurance to solidify its position as a primary distribution model in the nation's insurance arena.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low interest-rate environment compressing guaranteed product margins | -1.8% | Nationwide | Short term (≤ 2 years) |

| Stringent Solvency II capital charges disadvantaging mutuals | -1.2% | Cooperative insurers | Medium term (2-4 years) |

| Climate-related property claims escalating combined ratios | -0.9% | Coastal & forest regions | Long term (≥ 4 years) |

| Price war via digital aggregators eroding profitability | -0.7% | Urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Interest-Rate Environment Compressing Guaranteed Product Margins

A decade of sub-2% bond yields has eroded spreads on traditional policies. Skandia’s 205% solvency ratio highlights the capital drag of maintaining guarantees under Solvency II while still delivering customer value. The yield-tax threshold forces investment teams to chase higher-risk assets or pivot toward unit-linked structures, accelerating the shift in the Sweden life and non-life insurance market.

Stringent Solvency II Capital Charges Disadvantaging Mutuals

Risk-based charges penalize real-estate-heavy and long-duration assets common among cooperatives. While Länsförsäkringar continues to command 30% of non-life premiums, smaller mutuals face consolidation or demutualization pressures. Upcoming recovery-and-resolution rules, effective 2025, add extra governance overhead, widening the capability gap between large incumbents and community-based players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Life Insurance Dominates Amid Unit-Linked Surge

Life cover retained a 54.84% share in 2025, yet the mix is tilting rapidly. Unit-linked life is rising 7.65% annually as policyholders favor equity participation over low-yield guarantees. Traditional annuity products feel the squeeze from the 1.086% yield tax and compressed bond spreads. Non-life lines remain buoyant even as property claims worsen; motor insurers are rolling out e-mobility packages to protect Sweden’s 60.7% EV fleet share in Q1 2025. Liability-type cyber and professional policies grow as GDPR exposure bites. Funeral and long-term-care lines gain traction with demographic ageing. The Sweden life and non-life insurance market size for unit-linked portfolios is forecast to expand at nearly twice the pace of with-profits contracts through 2030, underscoring a structural pivot in household savings behavior.

Meanwhile, motor, property, health supplement, and specialty covers keep non-life underwriting diverse. Loss ratios are being recalibrated through risk-based pricing using granular climate data sets, particularly after property-claim frequency doubled in 30 years. The Sweden life and non-life insurance market share of e-mobility motor policies is projected to exceed 20% of new vehicle covers by 2027 as Sweden phases out internal combustion sales.

By Distribution Channel: Direct Sales Lead While Embedded Partnerships Accelerate

Direct online portals secured 39.08% of gross written premiums in 2025, reflecting the population’s comfort with self-service platforms. Embedded and affinity routes, however, are scaling 11.11% per year as neobanks and marketplaces stitch insurance into checkout flows. The Sweden life and non-life insurance market size distributed via banks and retail pipelines could double by 2030 if open-finance APIs maintain momentum. Brokers still shepherd complex commercial placements, but price-comparison engines sap margin in commoditized motor and travel lines. Insurtechs, representing 60% of Nordic startups, supply white-label platforms that let incumbents deploy embedded propositions without full rebuilds.

Digital aggregators, while improving transparency, intensify premium pressure. Insurers respond with AI-driven underwriting, instant quote-bind capabilities, and loyalty programs that reward behavioral data sharing. As contextual offers spread, direct portals may lose volume, but most carriers hedge by participating in both channels.

By End-User: Individual Consumers Dominate While SME Segment Accelerates

Individuals contributed 67.62% of the 2025 premium, aided by 97% home-insurance penetration. Yet household debt above 180% of disposable income may temper wallet growth. SMEs, generating the fastest 8.36% CAGR, increasingly bundle cyber, property, and employee-benefit covers as digitalization and GDPR risk grow. Protector Forsikring’s pivot to SME accounts shows profitability potential, evidenced by an 85.5% combined ratio in 2024.

Large corporations and the public sector add scale but limited upside, having already optimized captive and brokered programs. The Sweden life and non-life insurance market share held by SMEs is projected to edge toward 34.72% by 2031, supported by a thriving entrepreneurial ecosystem and robust M&A volumes.

By Premium Type: Regular Premiums Lead While Single-Premium Products Gain Traction

Regular-pay contracts composed 62.15% of the 2025 inflow because payroll deduction and monthly budgeting remain convenient. Single-premium contracts, however, benefit from rising household wealth and tax-efficient wrappers in life policies, expanding at a 6.08% CAGR. AMF’s SEK 230 million distribution to pension savers in 2024 illustrates how lump-sum capital can be promptly deployed for member gains. The Sweden life and non-life insurance market size for single-premium policies is especially influenced by high equity participation, 90% of financial assets are invested rather than parked in deposits, encouraging affluent Swedes to channel windfalls into insurance wrappers.

Geography Analysis

Southern Götaland, home to Stockholm and Gothenburg, concentrates corporate headquarters, advanced infrastructure, and the Nordic region’s largest e-commerce hubs. As a consequence, it secures the majority of premium volume and serves as the main laboratory for embedded offers. Electric-vehicle insurance adoption is most pronounced here, aligning with a 60.7% regional EV penetration in early 2025. Svealand, Sweden’s administrative core, benefits from the AP-fund overhaul that streamlines occupational pensions and boosts life-insurance contributions.

Norrland, though sparsely populated, exhibits rising demand for long-term care and funeral policies because of its ageing demographic. Property insurers face higher forest-fire and weather-damage claims, driving premium growth yet challenging profitability after claim frequency doubled over 30 years. Digital channels mitigate distribution cost in remote areas, and affinity tie-ups with regional banks help carriers maintain market presence.

Regulatory oversight from Finansinspektionen remains uniform nationwide, but regional economic profiles shape pricing and product mix. Carriers with federated structures—such as Länsförsäkringar—leverage local underwriting autonomy to fine-tune rates, helping the group preserve its 30% non-life market share. As climate-risk and demographic pressures intensify, regional diversification offers a strategic hedge, reinforcing the Sweden life and non-life insurance market against localized shocks.

Competitive Landscape

The market is moderately concentrated. Mutual giants Folksam and Länsförsäkringar together serve over 7 million customers and write more than SEK 108 billion in annual premiums, yet digital insurgents steadily chip away at younger segments. IF P&C’s acquisition of Topdanmark underscores a Nordic consolidation wave that delivers scale economies and enriches data pools for claims automation.

Traditional incumbents invest heavily in AI underwriting, telematics, and API architectures to defend franchise value. Gjensidige posted a 43% rise in insurance service results in 2024 and kept its combined ratio below 84% by optimizing pricing and trimming Baltic exposure. Swedish insurtechs such as Hedvig, Lemonade-style Paydrive, and BNPL-enabled Cover contribute fresh UX paradigms, often partnering rather than competing head-to-head with incumbents.

Regulation favors strong balance sheets: Solvency II and the 2025 Recovery Directive raise the bar for governance and risk modeling. These requirements create barriers that protect large players but complicate life for smaller mutuals. As crypto-asset and ESG capital charges evolve, carriers that invest early in robust risk frameworks may widen the moat within the Sweden life and non-life insurance market.

Sweden Life and Non-Life Insurance Industry Leaders

Lansforsakringar

If Skadeforsakring

Folksam

Trygg hansa

Skandia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Gjensidige Forsikring ASA returned NOK 2.5 billion to customers and introduced cyber-insurance and home-alarm bundles tailored to Nordic households.

- January 2025: The EU Insurance Recovery and Resolution Directive took effect, obliging Swedish insurers to draft recovery plans by 2027.

- October 2024: Skandia’s assets under management climbed to SEK 860 billion, reflecting strong investment performance and a 108% funding ratio.

- November 2024: The Swedish Club imposed a 5% general rate increase on P&I covers owing to claims inflation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Swedish life and non-life insurance market as the annual gross written premium generated by licensed insurers that underwrite personal-risk or property-risk policies for households, small and mid-sized enterprises, large corporates, and the public sector. It includes pension-linked and unit-linked life contracts, traditional life, motor, property, liability, accident and health, travel, marine, and aviation lines that are sold through direct, broker, bancassurance, digital aggregator, and embedded partnerships across Gotaland, Svealand, and Norrland.

Scope exclusion: reinsurance transactions, cross-border Freedom of Services premium inflows, and purely occupational pension funds without an insurance license are not sized.

Segmentation Overview

- By Product Type

- Life Insurance

- Traditional Life & Annuity

- Unit-Linked Life

- Pension & Annuity Products

- Other Life (Funeral, LTC)

- Non-Life Insurance

- Motor Insurance

- Private Passenger Car

- Commercial Vehicle

- E-Mobility / EV-Specific

- Property Insurance

- Household (Home & Contents)

- Commercial Property

- Agricultural Property

- Liability Insurance

- General Liability

- Professional & Cyber Liability

- Accident & Health Insurance

- Personal Accident

- Supplementary Health

- Travel Insurance

- Marine, Aviation & Transport

- Motor Insurance

- Life Insurance

- By Distribution Channel

- Direct (Insurer Website / Branch)

- Brokers & Independent Agents

- Bancassurance

- Digital Aggregators & Comparison Sites

- Embedded & Affinity Partnerships

- By End-User

- Individual Consumers

- Small & Medium Enterprises (SMEs)

- Large Corporates & Public Sector

- By Premium Type

- Single Premium

- Regular Premium

- By Geography

- Gotaland

- Svealand

- Norrland

Detailed Research Methodology and Data Validation

Primary Research

Conversations with actuaries, digital brokers, bancassurance managers, and Insurtech founders across Stockholm, Gothenburg, and Malmo enabled us to validate penetration assumptions, average policy size shifts, and the speed at which embedded cover is cannibalizing traditional channels. Their on-the-ground insights closed data gaps and sharpened scenario probabilities.

Desk Research

We pulled foundational statistics from tier-one public sources such as Statistics Sweden, Insurance Sweden, the Swedish Financial Supervisory Authority, the Riksbank, and EIOPA, complemented by company filings and reputable press. Regulatory circulars, Solvency II quarterly disclosures, and household income surveys helped crystallize premium pools. Premium movement patterns were tracked through paid resources including D&B Hoovers for carrier financials and Dow Jones Factiva for transaction news. These sources illustrate market momentum; yet the list is illustrative, not exhaustive.

Market-Sizing and Forecasting

The market baseline is derived through a top-down reconstruction of gross written premiums reported to Finansinspektionen, which are then adjusted for currency, single-premium volatility, and non-licensed flows before being further filtered through sampled average premium per policy checks from insurer roll-ups. Key variables like household disposable income, vehicle registrations, mortgage growth, corporate cyber-loss incidence, and demographic aging feed a multivariate regression that forecasts premium growth. Select bottom-up validations (digital channel volume times typical take-rate, motor ASP times fleet size) align segment splits. Where carrier data lacked detail, we bridged gaps using three-year moving averages anchored to statutory returns.

Data Validation and Update Cycle

Outputs pass an anomaly screen against independent macro indicators; variances above 5 percent trigger re-checks with source owners. Senior analysts review every model before sign-off. We refresh annually and issue interim updates after material regulatory or catastrophic events, ensuring clients receive the latest view.

Why Mordor's Sweden Life and Non-Life Insurance Baseline Commands High Dependability

Published numbers often differ because firms pick varying scope boundaries, exchange rate assumptions, or refresh cadences.

Key gap drivers here include: some studies fold occupational pension assets into life cover, others report premium income in nominal SEK without currency adjustment, and a few apply optimistic investment return scenarios that inflate unit-linked growth. Mordor's disciplined segmentation, currency normalization, and yearly refresh narrow these gaps and give decision makers a steadier footing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 47.2 B (2025) | Mordor Intelligence | - |

| USD 48 B (2025) | Global Consultancy A | Projects premium trend only and omits channel splits |

| USD 53 B (2024) | Industry Association B | Includes occupational pensions and uses average SEK rate without FX sensitivity |

Taken together, the comparison shows that while headline figures cluster, Mordor's model is the only one that ties every segment back to verifiable statutory premiums and cross-checks them with real-world channel data, giving stakeholders a transparent and repeatable baseline for strategic planning.

Key Questions Answered in the Report

What is the projected size of the Sweden life and non-life insurance market by 2031?

The market is forecast to reach USD 71.35 billion by 2031, expanding at a 7.13% CAGR.

Which product category is growing fastest?

Unit-linked life insurance is the fastest-growing, with a 7.65% CAGR through 2031 as savers seek higher returns in a low-yield environment.

How are embedded insurance models affecting distribution?

Embedded and affinity channels are forecast to rise at 11.11% CAGR, integrating coverage into banking and e-commerce journeys and reshaping how policies reach customers.

Why are Swedish SMEs buying more cyber insurance?

Strict GDPR penalties and a sophisticated digital infrastructure make cyber-risk cover vital; premiums typically range from SEK 5,000-10,000 per million SEK of indemnity.

Page last updated on: