South America Wire And Cable Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

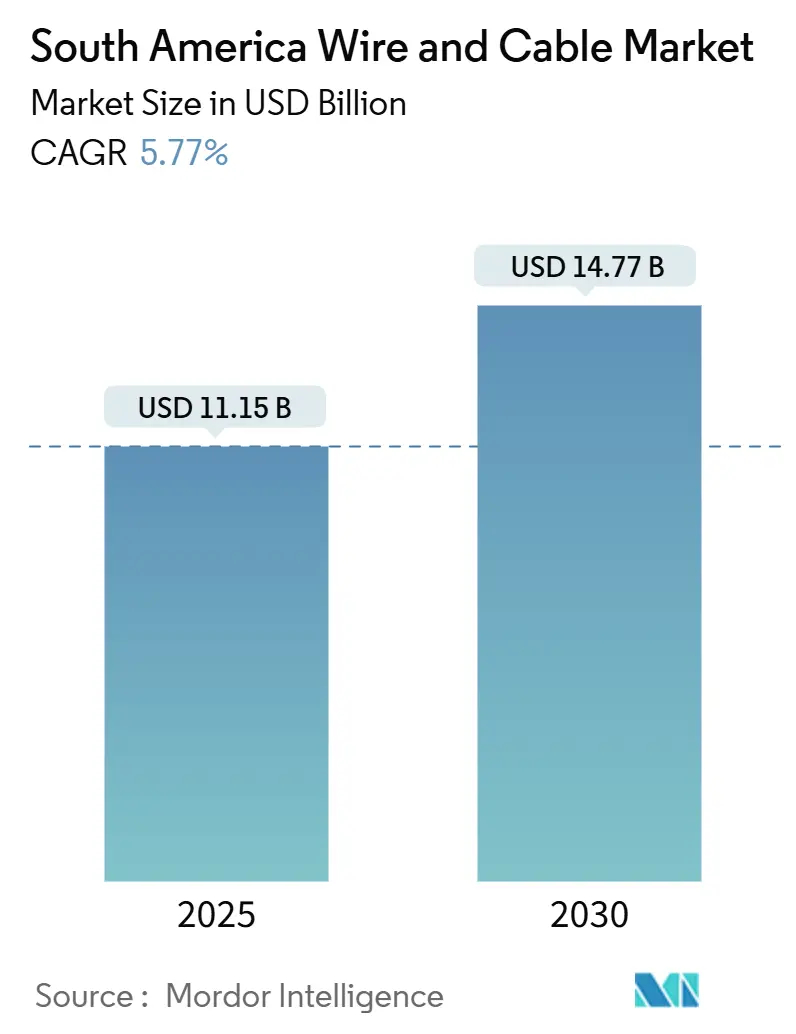

| Market Size (2025) | USD 11.15 Billion |

| Market Size (2030) | USD 14.77 Billion |

| Growth Rate (2025 - 2030) | 5.77% CAGR |

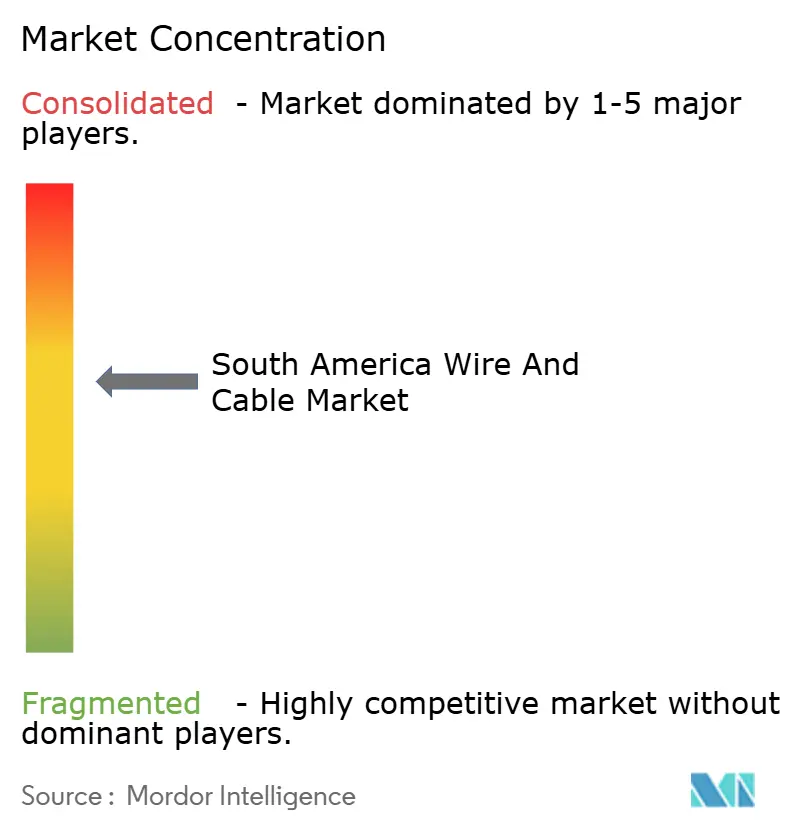

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Wire And Cable Market Analysis by Mordor Intelligence

The South America Wire And Cable Market size is estimated at USD 11.15 billion in 2025, and is expected to reach USD 14.77 billion by 2030, at a CAGR of 5.77% during the forecast period (2025-2030). Construction activity, ongoing power-grid upgrades, and aggressive fiber-to-the-home programs underpin current demand, while renewable integration and mobile backhaul densification add new revenue layers. Currency depreciation in Brazil and Argentina inflates imported raw-material costs, yet multilateral lending and private capital keep large projects on track. European incumbents face growing competition from regional makers, and hyperscale cloud companies are building their own trans-continental fiber systems that reshape the competitive landscape. Sub-segment momentum is clearest in fiber optics and extra-high-voltage lines, both essential for digital capacity and long-distance renewable transmission.

Key Report Takeaways

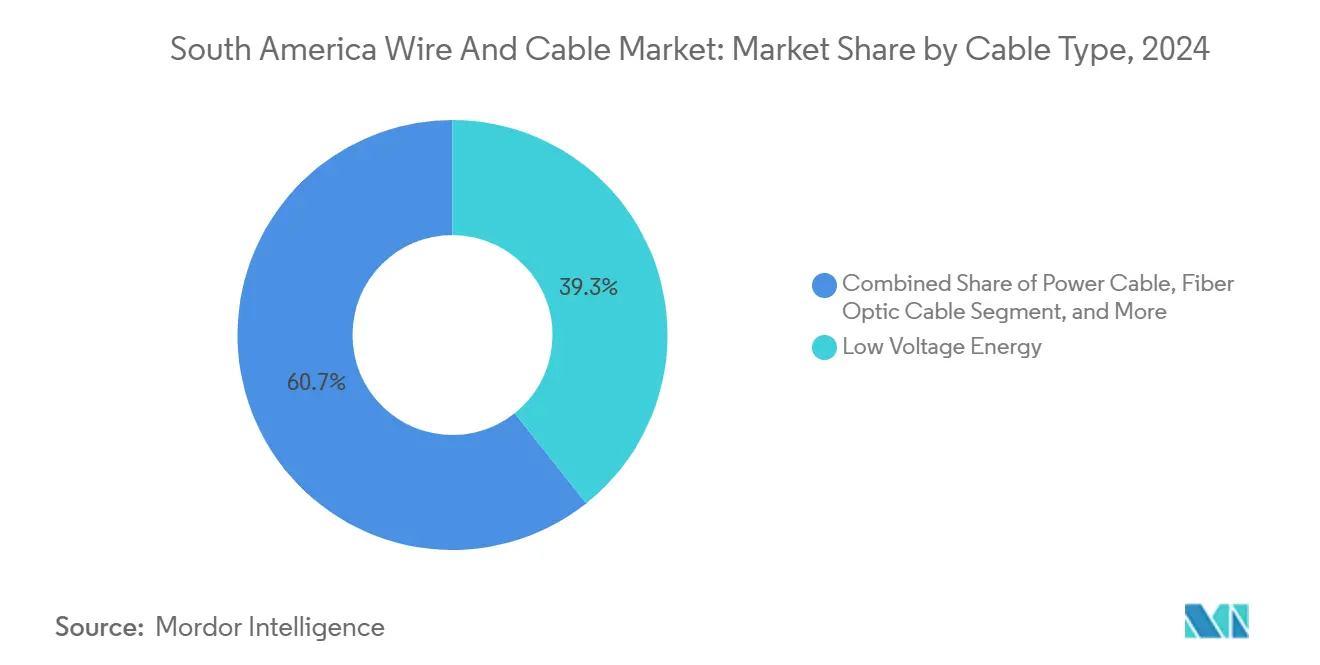

- By cable type, low-voltage energy cables held 39.32% of the South America wire and cable market share in 2024, while fiber optic cables are forecast to rise at a 7.61% CAGR to 2030.

- By voltage rating, low-voltage products accounted for 44.91% of the South America wire and cable market size in 2024, and extra/ultra-high-voltage is the fastest-growing sub-segment at a 7.61% CAGR to 2030.

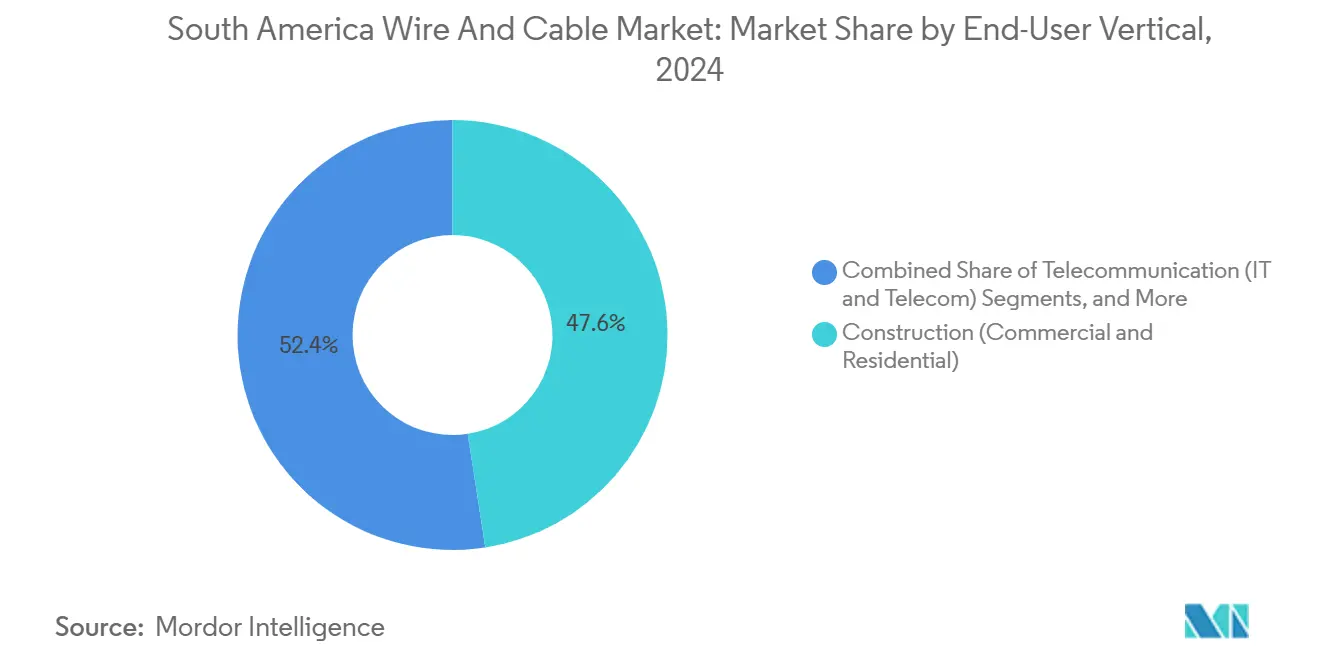

- By end-user vertical, the construction sector captured a 47.56% revenue share in 2024; power infrastructure is projected to register the highest CAGR of 8.85% through 2030.

- By country, Brazil led with a 47.74% revenue share in 2024 and is expected to expand at a 7.19% CAGR through 2030.

Proportional positioning is established by comparing regional contributions against the global total, including that of South america. The wire and cable market share in our global report expresses these relative weights.

South America Wire And Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging utility-scale renewable energy projects | +1.5% | Brazil, Chile, Argentina core markets | Medium term (2-4 years) |

| Rising fiber-to-the-home (FTTH) roll-outs | +1.2% | Brazil, Colombia, Chile urban centers | Short term (≤ 2 years) |

| Government-backed transmission and distribution upgrades | +0.8% | Regional, with concentration in Brazil, Argentina | Long term (≥ 4 years) |

| 4G/5G backhaul densification in secondary cities | +0.9% | Brazil, Colombia, Peru expanding coverage | Medium term (2-4 years) |

| Green hydrogen corridor build-outs | +0.6% | Chile, Brazil, Uruguay coastal regions | Long term (≥ 4 years) |

| Lithium-ion gigafactory investments in Chile and Argentina | +0.5% | Chile, Argentina mining regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Utility-Scale Renewable Energy Projects

Utility developers continue to commission large solar and wind assets across South America, and almost every new megawatt requires matching high-voltage export capacity. ENGIE secured a 30-year concession to build 1,000 km of lines across five Brazilian states, generating USD 252 million in regulated annual revenue.[1]ENGIE, “ENGIE Secures New Bid in Brazil,” engie.comCurtailment reached 2.4 TWh in Chile during 2023, prompting the energy ministry to fast-track grid reinforcements and tariff reallocations.[2]Argus Media, “Chile Battles On With Energy Transition,” argusmedia.comThe parallel requirement for optical ground wire (OPGW) makes every new line a dual-purpose asset that also boosts rural telecom reach.

Rising Fiber-to-the-Home Roll-Outs

Carriers are deploying fiber at an unprecedented pace. Claro Brasil earmarked USD 7.7 billion for 5G and fiber upgrades between 2024 and 2029, while América Móvil is executing a comparable plan across its regional footprint. Neutral-host specialist V.tal is coupling a USD 1 billion data-center roll-out with last-mile fiber, ensuring wholesale bandwidth for smaller ISPs. Peru’s Amazon basin saw Global Fiber Peru connect 400 isolated communities in 2025, replacing costly satellite links. A skills shortage is the only near-term brake; the World Economic Forum estimates digital-workforce training must scale 250% to meet operator schedules.

Government-Backed Transmission and Distribution Upgrades

National regulators continue to auction large grid packages that guarantee long-term returns for cable suppliers. Brazil’s program alone has lifted ENGIE’s local footprint to nearly 8,000 km of lines. Cross-border schemes, such as the Ecuador-Peru 500 kV intertie, aim to stabilize power flows and reduce fossil fuel backup. Colombia’s USD 19.4 billion Turbo-Cupica railway also includes substantial electrical works, although the rainforest terrain may delay its execution. Policy now requires two independent tele-protection channels per line, increasing the fiber count per circuit and raising the cable value per kilometer.

4G/5G Backhaul Densification in Secondary Cities

Mobile operators are expanding advanced coverage beyond primary metropolitan areas. TIM Brasil’s 2025 expansion contract with Nokia typifies the new wave of investment, spurred by fiscal incentives that reward the sunset of 2G/3G networks and the refarming of spectrum. Studies of the 2024 flooding in Rio Grande do Sul showed legacy 2G/3G sites outperformed 4G/5G in extreme weather, encouraging operators to engineer redundant paths that ultimately raise fiber-kilometer demand. Rural deployments often blend FTTH spurs with cell-site backhaul, maximizing trenching efficiencies and driving multi-service cable orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper and aluminum prices | -0.7% | Regional, with highest impact in import-dependent markets | Short term (≤ 2 years) |

| Currency-driven import cost inflation | -0.4% | Argentina, Brazil primary exposure | Short term (≤ 2 years) |

| Project delays from political transitions | -0.5% | Regional, with concentration in Argentina, Peru, Colombia | Medium term (2-4 years) |

| Skills gap in high-density fiber deployment | -0.3% | Brazil, Colombia, Chile urban expansion areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Aluminum Prices

Cable makers faced sharp swings in conductor costs during 2025 as mining disruptions and smelter outages tightened supply. LME copper ranged from USD 7,900 to USD 9,800 per ton, eroding contract margins and complicating project finance. Aluminum tracked a different path because energy-price spikes constrained smelter output, creating material-substitution dilemmas for design engineers. Suppliers are now offering higher-fill-factor conductors and leaner alloy blends to limit metal intensity without sacrificing ampacity.

Currency-Driven Import Cost Inflation

The Brazilian real lost 9.5% against the USD in calendar 2025, while Argentina’s peso devalued almost 50%, lifting dollar-priced inputs across the board. Import exposure is acute for specialty insulators, semiconductor tapes, and certain high-voltage accessories that regional plants do not yet produce. Developers are negotiating escalation clauses and turning to local content, but retooling takes time and capital. Exchange-rate risk also raises the cost of servicing hard-currency debt, pressuring project balance sheets even when demand fundamentals stay strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Fiber Optics Drives Digital Infrastructure

Low-voltage energy products represented 39.32% of 2024 revenue in the South America wire and cable market, while fiber optic cables are projected to grow at a 7.61% CAGR through 2030. The premium capacity of modern fiber supports both FTTH and data-center interconnect needs across densely populated corridors. Neutral-host network build-outs and submarine-branch landings propel the South America wire and cable market. Prysmian’s ECO CABLE program, which covers roughly 30% of its telecom portfolio, appeals to operators with greenhouse-gas targets, helping the brand retain its specification preference on new tenders. Meta’s 24-pair Project Waterworth highlights the increasing importance of high-fiber-count designs that require advanced manufacturing and testing processes.

Power, signal, and legacy coaxial cables continue to capture renovation and industrial orders; yet, bandwidth hunger keeps shifting capital budgets toward fiber. Construction standards now mandate empty conduits for future fiber drops in new buildings across Brazil and Chile, further locking in long-term demand. As an aging copper plant gets decommissioned, recovery and recycling programs return conductor metal to the supply chain, partially offsetting raw-material volatility.

By Voltage Rating: Ultra-High Voltage Gains Momentum

Low-voltage lines, ≤1 kV, captured 44.91% of the 2024 revenue, reflecting expansive housing programs and small commercial builds. Extra- and ultra-high-voltage (>220 kV) is the fastest-growing class, with a 7.61% CAGR, because long-distance renewable corridors require fewer but larger lines, each laden with premium insulation and monitoring accessories. The South America wire and cable market share for extra-high-voltage reached 9.4% in 2024 and is expected to top 12% by 2030. ENGIE’s 1,000 km Brazilian concession demonstrates the financial viability of such projects, with USD 252 million in regulated annual income, which funds heavy conductor sections and OPGW pairs.

Medium-voltage (1-35 kV) remains the backbone of urban distribution and mining operations, while high-voltage (35-220 kV) feeders link load centers to generation hubs. Regional regulators now stipulate temperature-resistant, low-sag conductors for high-ampacity spans in desert and tropical zones, driving upgrades even when the nominal voltage remains unchanged. Suppliers delivering turnkey kits, cable, joints, fiber, and hardware enjoy higher margins and secure framework agreements that extend beyond a single voltage class.

By End-User Vertical: Power Infrastructure Accelerates

Construction contributed 47.56% of 2024 turnover, but power utilities are the fastest-growing customers with an 8.85% CAGR to 2030, underpinned by battery storage, green hydrogen clusters, and cross-border interconnectors. The South America wire and cable market size tied to power infrastructure is expected to expand by almost USD 1.9 billion over the outlook period. Chile’s planned 2 GW storage tender and Uruguay’s coastal hydrogen pipelines illustrate the growing mix of direct-current links and higher-ampacity alternating-current feeders that drive demand for specialized cables.

Telecommunications remains a strong second pillar as 5G densification overlaps with FTTH corridors. Wholesale carriers prefer 288-fiber and 432-fiber cables for rural duct-sharing schemes, which reduces the per-home pass cost and allows for future capacity leases. Industrial automation, rail electrification, and defense projects round out the order book, providing diversity that shields manufacturers from cyclicality in any single vertical.

Geography Analysis

Brazil generated just under half of all 2024 revenue and is pacing the regional league table with a 7.19% CAGR through 2030. Claro’s USD 7.7 billion multi-year plan, combined with Meta’s Project Waterworth, makes the country a top destination for telecom-grade fiber.[3]Globo, “Meta Vai Instalar 50 Mil Km de Cabos Submarinos,” g1.globo.comPersistent grid bottlenecks continue to boost extra-high-voltage demand, and regulators now bundle fiber capacity into every new concession. Currency weakness inflates input costs, yet also encourages onshore manufacture of conductors and accessories, thereby improving domestic value capture.

Argentina offers high-margin niches in lithium-ion gigafactory supply chains and Patagonian wind export lines. Rio Tinto’s USD 2.5 billion lithium outlay increases demand for medium-voltage and control cables, while cross-border conversions with Chile require hybrid aluminum-copper designs adapted to Andean altitudes. Peso volatility complicates imports, but reverse-sourcing agreements with Brazilian foundries provide a partial hedge.

Chile positions itself as an energy transition laboratory with legislation that reallocates tariffs to accelerate grid reinforcement. Google’s 14,800 km trans-Pacific cable will land near Valparaiso, sparking terrestrial backhaul projects worth tens of millions of dollars. The move aligns with extensive green hydrogen corridors that run from the Atacama desert to export terminals, each demanding high-temperature, chemically resistant cabling.

Colombia and Peru advance telecommunications roll-outs and rural electrification. The CSN-1 cable activated partial service in 2025, reducing latency for Andean cloud workloads and catalyzing terrestrial fiber spurs. Rest-of-region markets, including Paraguay and Uruguay, adopt similar models, securing multilateral loans that require open-access wholesale frameworks, thereby expanding addressable fiber demand.

Mordor Intelligence examines the wire and cable market across diverse other regional markets as well, including North America and Europe, while also offering granular country-level perspectives for India and Mexico and more.

Competitive Landscape

The market is moderately concentrated. Prysmian, Nexans, Grupo Condumex, and Cobrecon account for roughly 45% of sales, while scores of local firms supply building wire and niche assemblies. Hyperscalers break the historic carrier consortium model by owning entire submarine systems, as seen in Meta’s Project Aquila, not Project Waterworth. Cable makers respond by offering turnkey manufacturing, along with optical repeaters and landing gear, to remain relevant in direct-procurement scenarios.

Product differentiation now leans on sustainability. Prysmian’s ECO CABLE label quantifies lifecycle impact, winning specification preference from operators with Net Zero targets. Nexans pilots its Mobiway POP solution in Colombia, allowing electricians to transport reels safely and trim installation time, a critical advantage in labor-tight markets.

Regional suppliers invest in aluminum drawing and compound extrusion to localize materials, cushioning currency shocks. Joint ventures with resin and steel makers aim to meet new green-hydrogen fire-resistance specifications, while lithium-ion factories in the Southern Cone require large, cross-sectionally flexible conductors for battery racks. Barriers to entry remain high because utilities and submarine operators insist on rigorous type-testing and long warranties.

South America Wire And Cable Industry Leaders

Prysmian S.p.A

Nexans S.A.

Furukawa Electric Co., Ltd.

Fujikura Ltd.

LS Cable & System Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Google and Chile have inked a deal for a 14,800 km trans-Pacific cable landing in Valparaiso, slated for service in 2027.

- April 2025: Brazil’s regulator cleared SpaceX to add 7,500 Starlink satellites, boosting ground-station and backhaul cable needs.

- February 2025: Meta announced Project Waterworth, a 50,000 km submarine cable system with 24 fiber pairs linking Brazil to five continents.

- September 2024: ENGIE won a 30-year concession to build 1,000 km of high-voltage lines across Brazil, securing USD 252 million in annual revenue.

South America Wire And Cable Market Report Scope

A cable consists of more insulated wires wrapped in a single jacket that permits them to pass through, whereas a wire is a single conductor. The scope of the study encompasses various forms of wire and cable installations deployed in essential end-user facilities, including telecommunications, construction, and power infrastructure.

The South America Wire and Cable Market Report is Segmented by Cable Type (Low Voltage Energy, Power Cable, and More), Voltage Rating (Low Voltage ≤1 KV, Medium Voltage 1-35 KV, High Voltage (35-220 kV), Extra/Ultra-High Voltage (>220 kV)), End-User Vertical (Construction, Telecommunication, Power Infrastructure, Other End User Verticals (BFSI, Railway, Defense and Military, Industrial, Medical, Others), and by Country (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Low Voltage Energy |

| Power Cable |

| Fiber Optic Cable |

| Signal and Control Cable |

| Other Cable Types (Coaxial, Telecom and Data Cables) |

| Low Voltage (≤1 kV) |

| Medium Voltage (1-35 kV) |

| High Voltage (35-220 kV) |

| Extra/Ultra-High Voltage (>220 kV) |

| Construction (Commercial and Residential) |

| Telecommunication (IT and Telecom) |

| Power Infrastructure (Energy and Power, Automotive) |

| Other End User Verticals (BFSI, Railway, Defense and Military, Industrial, Medical, Others) |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Cable Type | Low Voltage Energy |

| Power Cable | |

| Fiber Optic Cable | |

| Signal and Control Cable | |

| Other Cable Types (Coaxial, Telecom and Data Cables) | |

| By Voltage Rating | Low Voltage (≤1 kV) |

| Medium Voltage (1-35 kV) | |

| High Voltage (35-220 kV) | |

| Extra/Ultra-High Voltage (>220 kV) | |

| By End-user Vertical | Construction (Commercial and Residential) |

| Telecommunication (IT and Telecom) | |

| Power Infrastructure (Energy and Power, Automotive) | |

| Other End User Verticals (BFSI, Railway, Defense and Military, Industrial, Medical, Others) | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America wire and cable market in 2025?

The sector is valued at USD 11.15 billion in 2025.

What is the expected CAGR for South American wire and cable demand to 2030?

Demand is forecast to grow at 5.77% annually through 2030.

Which cable type is expanding fastest across South America?

Fiber optic cables show the highest growth, with a 7.61% CAGR during 2025-2030.

Why are ultra-high-voltage cables gaining momentum?

Large renewable corridors require long-distance transmission lines above 220 kV, driving demand.

How concentrated is supplier competition?

The top five players hold about half of total revenue, indicating moderate concentration.

What main factor restrains near-term growth?

Volatile copper and aluminum prices compress margins and complicate project budgets.

Page last updated on: