Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

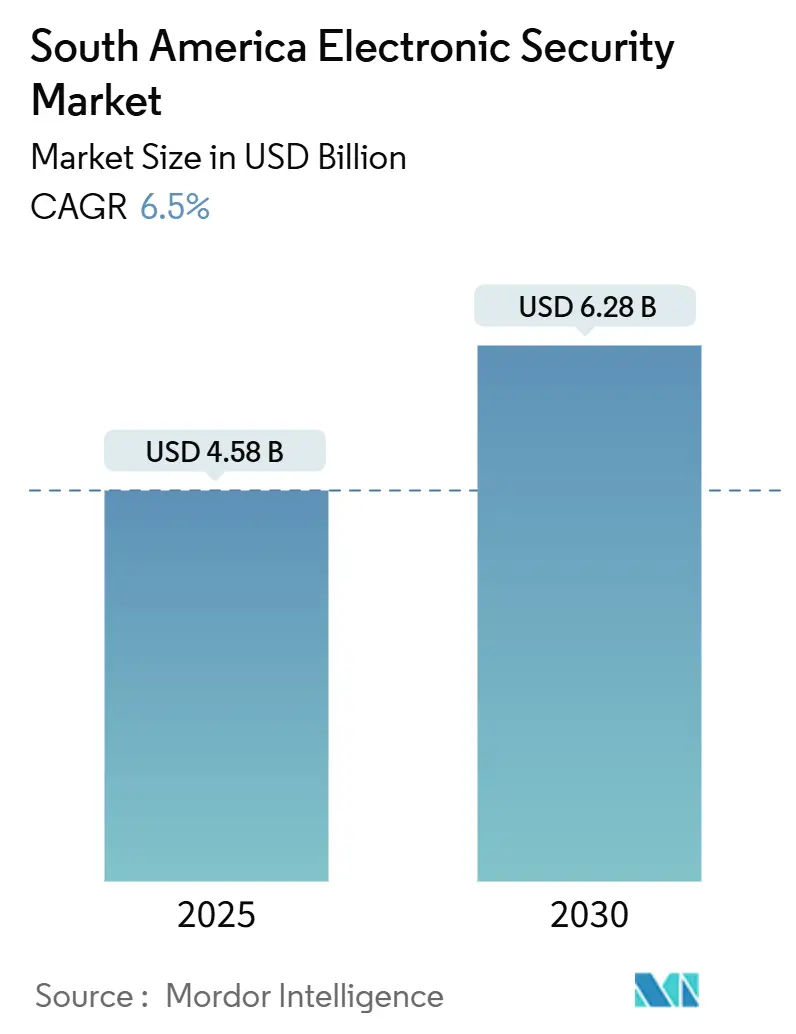

| Market Size (2025) | USD 4.58 Billion |

| Market Size (2030) | USD 6.28 Billion |

| Growth Rate (2025 - 2030) | 6.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Electronic Security Market Analysis by Mordor Intelligence

The South America electronic security market size reached USD 4.58 billion in 2025 and is projected to grow at a 6.50% CAGR to USD 6.28 billion by 2030. Heightened security awareness, government-funded safe-city programs, and a rapid shift from analog to IP-based surveillance are accelerating demand across public and private sectors. Municipal preparations for the 2026 FIFA World Cup, record federal procurement outlays, and e-commerce warehouse expansion are fueling large-scale infrastructure deployments. Vendors are embedding AI analytics at the edge to enable real-time threat detection, while cloud-native platforms gain traction as organizations seek operational flexibility and compliance with evolving data-sovereignty rules. Competitive intensity is rising as global manufacturers pursue strategic acquisitions and regional specialists introduce managed Security-as-a-Service models that offset the shortage of certified integrators.

Key Report Takeaways

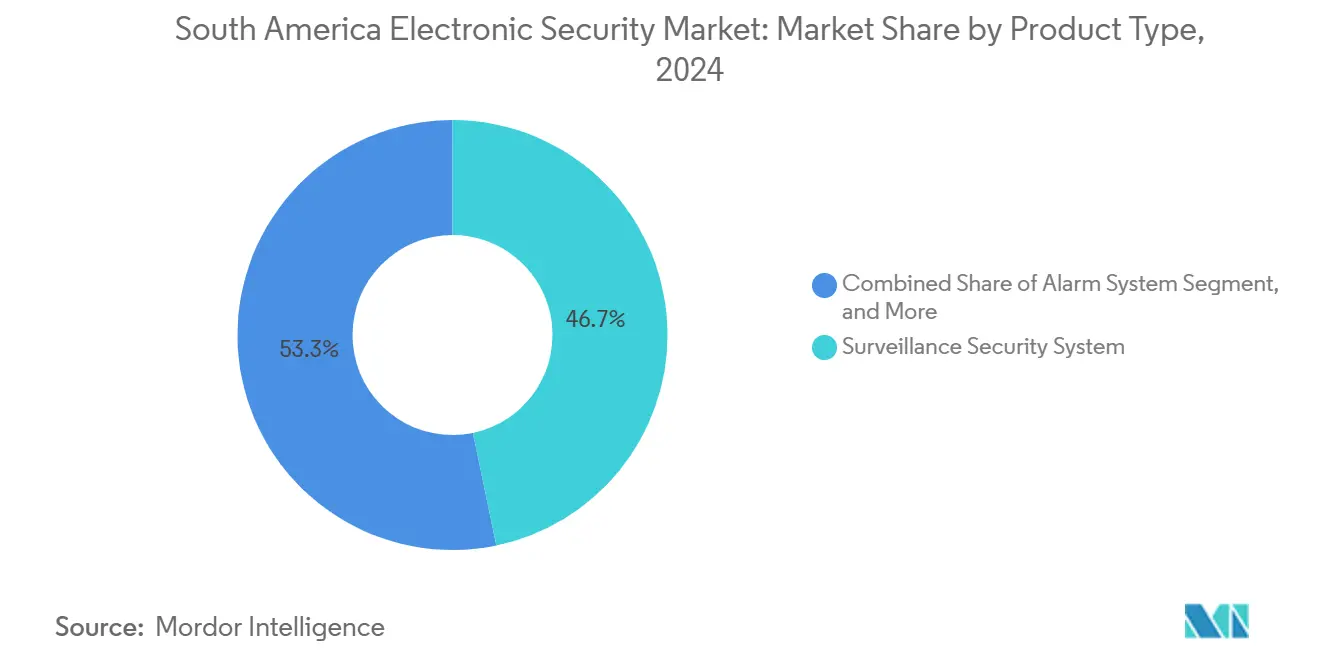

- By product type, surveillance security systems led with 46.73% revenue share in 2024 in the South America electronic security market, while integrated security platforms recorded the fastest 7.11% CAGR from 2025 to 2030.

- By end-user industry, the government and public sector commanded 28.62% of the South America electronic security market share in 2024; the transportation and Infrastructure Sector is forecast to expand at a 6.89% CAGR through 2030.

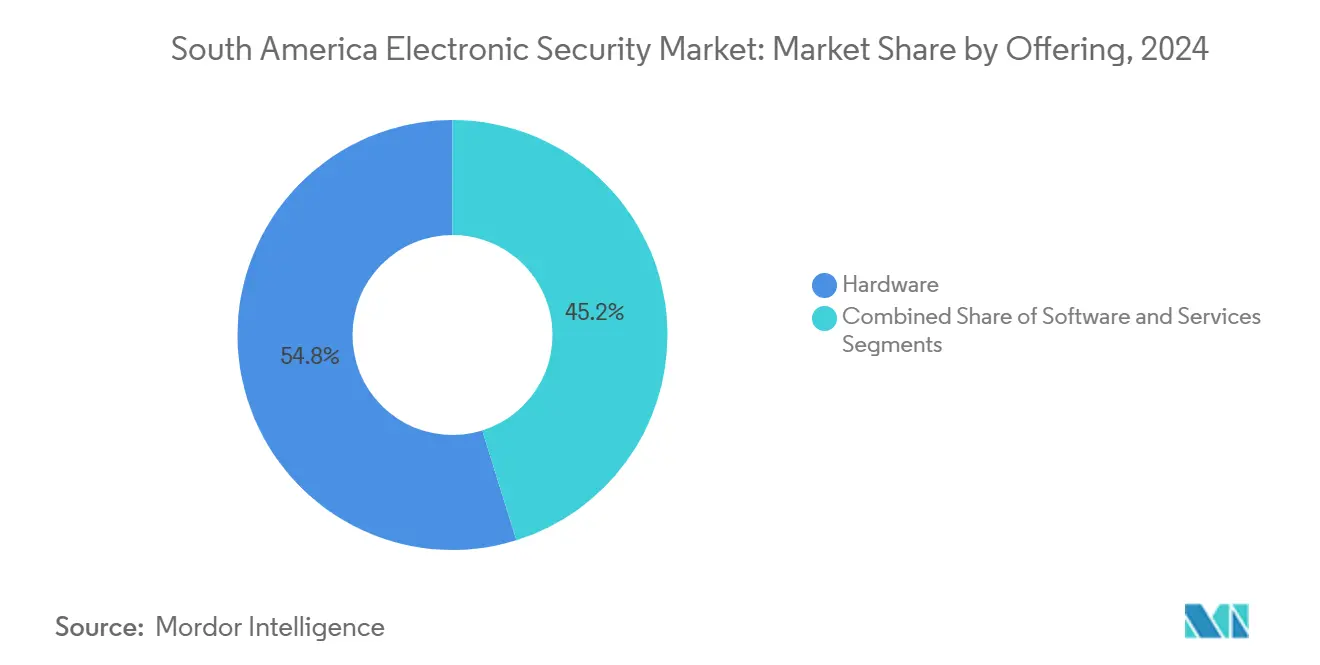

- By offering, hardware solutions accounted for 54.82% share of the South America electronic security market size in 2024, whereas Cloud Services are advancing at a 7.29% CAGR through 2030.

- By deployment mode, on-premises installations held a 67.92% share in 2024 of the South America electronic security market; cloud-based deployments are expected to exhibit the highest 7.34% CAGR through 2030.

- By country, Brazil led with 29.98% share in 2024 and is growing at 6.94% CAGR in the South America electronic security market, buoyed by USD 2.5 billion e-commerce infrastructure spending.

South America Electronic Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Surge in cloud-native access-control deployments | +1.2% | Global, with early adoption in Brazil and Chile |

| Government-funded safe-city video projects | +1.8% | Mexico, Brazil, Colombia core markets |

| Integration of AI analytics for real-time threat detection | +1.5% | APAC spillover to South America America, concentrated in urban centers |

| Migration from analogue to IP-based surveillance | +0.9% | Regional, with infrastructure gaps in Peru and Colombia |

| Expansion of e-commerce warehouses requiring security | +1.3% | Brazil, Mexico, Argentina logistics hubs |

| Upcoming 2026 FIFA World Cup stadium security upgrades | +0.8% | Mexico primary, with spillover to regional events |

| Source: Mordor Intelligence | ||

Government-Funded Safe-City Video Projects Drive Infrastructure Modernization

Regional authorities are directing unprecedented budgets toward city-wide surveillance as part of comprehensive public safety strategies. Brazil’s federal e-procurement portal processed 119,000 security purchases valued at BRL 217 billion in the first half of 2025, accelerating the adoption of integrated platforms that replace siloed point solutions.[1]Portal Nacional de Contratações Públicas, “Editais,” pncp.gov.br Colombia’s transport decree mandates cryptographic fare-collection safeguards across USD 17 billion road concessions, reinforcing demand for unified security architectures. [2]U.S. International Trade Administration, “Colombia Road Concession Programs,” trade.gov Standardized bidding frameworks now stipulate vendor certifications and interoperable APIs, narrowing qualification to firms that can deliver end-to-end solutions. These factors collectively drive volume shipments of high-resolution cameras, video management software, and edge AI appliances, supporting steady revenue growth for the South America electronic security market.

Cloud-Native Access-Control Deployments Reshape Market Architecture

Organizations across retail, logistics, and commercial real estate are migrating access-control workloads to SaaS platforms to minimize on-premises hardware and gain elastic scalability. LenelS2’s July 2024 launch of OnGuard Cloud marks a strategic pivot to recurring software revenue, while InVue’s chainwide rollout at Coppel retail stores confirms the enterprise's appetite for pay-as-you-go models. Honeywell’s USD 4.95 billion acquisition of Carrier’s Global Access Solutions unit equips the company with cloud-centric brands such as LenelS2 and Supra, fortifying its regional channel in anticipation of mounting SaaS demand. Brazilian enterprises are adopting hybrid architectures to meet LGPD data-localization mandates while leveraging cloud analytics, prompting managed service providers to establish tier-3 data centers in São Paulo and Rio de Janeiro. [3]Secretaria de Segurança da Informação e Cibernética, “OSIC 15/2024,” gov.br Mid-sized enterprises, which were historically priced out of sophisticated door controllers, now consume enterprise-grade features via monthly subscriptions, widening the addressable market and accelerating growth in the South America electronic security market.

AI Analytics Integration Enables Predictive Security Operations

Video data volumes are outpacing human monitoring capacity, making machine-learning analytics indispensable for threat prediction and anomaly detection. Argentina’s new AI security unit validates state-level commitment to computer-vision deployment, while Brazil’s draft AI Bill 2,338/2023 mandates risk assessments and time-bound incident disclosure for high-risk systems. Vendors respond with hybrid designs that perform sensitive facial-recognition computations on-premises yet offload pattern-matching workloads to cloud GPUs, balancing privacy compliance with analytical depth. Financial institutions integrate behavior analytics modules to flag atypical customer movement near ATMs, reducing fraud incidents. Stadium operators deploying crowd-density analytics ahead of the 2026 World Cup gain early-warning indicators of stampede risk, illustrating how AI elevates security from reactive surveillance to proactive situational awareness, thereby stimulating additional investment within the South America electronic security market.

E-Commerce Warehouse Expansion Creates Specialized Security Demand

Accelerating e-commerce adoption is spawning mega-fulfillment centers that need 24/7 perimeter protection, automated access control for autonomous forklifts, and real-time asset tracking. MercadoLibre’s USD 2.5 billion Mexico project and the doubling of Brazilian distribution centers to 21 sites by 2025 add 880,000 m² of high-value, security-sensitive floor space. Integrated platforms linking intrusion sensors, PTZ cameras, and cyber-hardened IoT gateways give logistics operators unified visibility across multi-tenant warehouses. Cloud dashboards push incident alerts to mobile devices, allowing roving guards to respond within minutes. Vendors offering consumption-based pricing capture mid-market operators that cannot afford capital-heavy builds, while systems integrators bundle IoT device management to shield connected conveyors and sorters from ransomware. These dynamics elevate demand for scalable, subscription-friendly solutions, reinforcing the positive outlook for the South America electronic security market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-country data-sovereignty rules | -0.8% | Regional, with strictest requirements in Brazil and Chile | Long term (≥ 4 years) |

| High import tariffs on security hardware | -1.1% | Brazil, Argentina primary impact with Mercosur variations | Medium term (2-4 years) |

| Shortage of certified security-system integrators | -0.9% | Regional, most acute in Peru and Colombia | Long term (≥ 4 years) |

| Rising cyber-attacks on IoT-connected cameras | -0.7% | Global impact with regional concentration in Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Country Data-Sovereignty Rules Fragment Market Approach

Divergent privacy and cybersecurity statutes require vendors to tailor deployment models country by country, thereby inflating costs and extending sales cycles. Chile’s Cybersecurity Framework Law, fully enforceable since March 2025, empowers ANCI to levy fines up to 40,000 UTM and demand three-hour incident reporting, compelling providers to maintain local data-replication nodes. [4]Library of Congress, “Chile: Framework Law on Cybersecurity Comes into Force,” loc.govBrazil’s LGPD requires localized storage of biometric identifiers, while OSIC 15/2024 urges adoption of post-quantum cryptography. These fragmented edicts inhibit standardized regional rollouts and diminish economies of scale, dampening near-term uptake of multi-tenant cloud services within the South America electronic security market.

Shortage of Certified Security-System Integrators Constrains Implementation

Skill gaps threaten timely project delivery for AI-enabled surveillance and hybrid architectures. OECD notes a 20-65% rise in cybersecurity talent demand across Chile, Colombia, and Mexico, while Peru needs 7,000-13,500 additional professionals by 2025. ConsorcioTec’s 100-member roster manages USD 100 million in annual technology purchases but cannot cover regional installation peaks. Enterprises compensate by outsourcing to managed service providers, yet this raises recurring costs and limits customization. Vendors respond with plug-and-play cloud suites that require minimal onsite expertise, but large infrastructure projects, airports, metros, critical energy, still depend on scarce, certified engineers, tempering the South America electronic security market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Converged Platforms Capture Rapid Share

Surveillance systems retained a 46.73% revenue lead in 2024, underscoring the centrality of video monitoring in regional security postures. Integrated platforms, however, are pacing a 7.11% CAGR, reflecting enterprise preference for single-pane management of cameras, doors, and intrusion detectors. The South America electronic security market size for integrated offerings is projected to surpass USD 2 billion by 2030, capturing deployments in logistics hubs and smart cities. Vendor consolidation accelerates as Honeywell merges LenelS2 and Onity capabilities to deliver turnkey suites. Brazilian retailers deploy unified dashboards that merge POS data with video analytics to flag suspicious transactions, demonstrating cross-system synergy. Perimeter intrusion detection enjoys niche demand in pipelines and power grids, but lags mainstream adoption due to cost. Alarm systems remain steady in residential high-rise retrofits, while access-control panels shift toward mobile credentials and biometric readers to meet pandemic-induced contactless guidelines.

Regulatory pressures spur convergence. Chile’s cybersecurity framework requires unified incident reporting streams, incentivizing IT and physical-security teams to share data lakes. Brazil’s federal procurement templates score higher for open-API architectures, favoring truly converged solutions. Vendors now ship edge appliances pre-licensed for video, access, and intrusion channels, shortening deployment timelines. This cross-functionality stimulates upsell cycles and cements integrated platforms as the growth engine of the South America electronic security market.

By End-User Industry: Transportation and Infrastructure Takes Growth Spotlight

Government and Public institutions held 28.62% share in 2024, buoyed by safe-city rollouts and critical-infrastructure hardening. Transportation and Infrastructure are racing ahead with a 6.89% CAGR, propelled by Colombia’s USD 17 billion road concessions and Peru’s airport modernization projects. The South America electronic security market share for transportation deployments is expected to rise three points by 2030 as biometric boarding gates, integrated CCTV-fare systems, and smart lane controls roll out. BFSI remains a technology-driven vertical, expanding thermal cameras and fraud analytics suites to counter the rising incidents of ATM skimming. Industrial manufacturers are adopting IoT-centric intrusion detection to protect operational technology, particularly amid heightened ransomware threats.

Omnichannel retailers are retrofitting warehouses with robotic surveillance drones, while healthcare operators are integrating drug-dispensing cabinets with access credentials to combat narcotics diversion. Residential smart-home penetration accelerates in metropolitan Brazil, leveraging wireless DIY kits. The hospitality sector rebounds post-pandemic, embedding thermal screening and mobile guest keys into renovation cycles. These varied vertical dynamics collectively add breadth and resilience to the South America electronic security market.

By Offering: Cloud Services Scale on Hybrid Backbones

Hardware dominated with a 54.82% revenue share in 2024; however, Cloud Services are growing at a rate of 7.29% annually through 2030. Hardware suppliers now bundle AI chips to run person-of-interest algorithms at the edge, lowering bandwidth costs. The South America electronic security market size for cloud subscriptions, covering VMS, access-control, and AI analytics, is forecast to double by 2029. Software licensing shifts toward consumption models; LenelS2 offers tiered feature sets aligned to door counts, converting capex into opex. Services revenue surges as enterprises outsource 24/7 monitoring and system patching to overcome skills shortages. Regional managed service providers partner with hyperscalers to co-locate video archives, ensuring compliance with LGPD and Chilean data laws without sacrificing latency.

Growing recognition of cyber-physical convergence propels the uptake of patch-management add-ons and vulnerability scanning. Vendors monetize over-the-air firmware updates that expand analytic libraries without truck rolls. This recurring-revenue orientation underpins margin expansion and propels cloud to become the fastest-growing slice of the South America electronic security market.

By Deployment Mode: Hybrid Cloud Emerges as Dominant Path

On-premises infrastructure still accounts for 67.92% of 2024 deployments, due to legacy investments and privacy considerations. Cloud-based rollouts, however, are climbing at a 7.34% CAGR as bandwidth availability improves and vendors certify regional data centers. Hybrid architectures are increasingly prevalent, with sensitive facial-recognition databases residing onsite, while metadata analytics run in the cloud for elasticity. Brazil spearheads hybrid adoption; banks leverage Amazon Web Services’ São Paulo region to process video metadata while retaining raw footage locally to comply with the LGPD. Chilean utilities pilot Google Cloud’s Santiago zone to host cybersecurity incident hubs, adhering to ANCI audit trails. Small enterprises opt for cloud-first VMS subscriptions that automatically scale during seasonal spikes, thereby lowering the total cost of ownership. These developments reinforce hybrid structures as the future growth vector within the South America electronic security market.

Geography Analysis

Brazil commanded 29.98% of regional revenue in 2024 and is advancing at a 6.94% CAGR, fueled by BRL 217 billion in public-sector tenders. Federal guidance OSIC 15/2024 encourages agencies to adopt post-quantum algorithms, prompting upgrades to legacy VPN gateways and key-management servers. Cyberattack volumes increased by 95% in 2025, according to TIVIT, propelling the uptake of managed security services.

Argentina, the second-largest market, benefits from Prosegur’s countrywide rollout of intelligent Security Operations Centers, enhancing cross-vertical analytics adoption. Economic stabilization measures help provincial governments fund safe-city retrofits. Chile stands out as a regulatory vanguard; ANCI’s three-hour breach mandate accelerates demand for cloud-native incident-response orchestration. The country’s upcoming data-protection statute, effective December 2026, further incentivizes the use of privacy-enhancing video redaction tools.

Colombia’s USD 17 billion fourth-generation road program underpins a surge in toll-lane surveillance, LPR cameras, and encrypted fare systems. Peru faces pronounced skills deficits; public tenders often mandate vendor-supplied training, boosting service revenue. Chinese OEM dominance in government bids sparks cybersecurity scrutiny, encouraging multinationals to tout zero-trust firmware.

The Rest-of-South-America cluster includes Uruguay’s USD 322 million market expanding on data-center builds, Paraguay’s hydro-power security revamps, and Bolivia’s airport-screening modernization. Cross-border regulatory harmonization remains low; thus integrators operate via country-specific subsidiaries to navigate import duties and data-localization clauses. Collectively, heterogeneous growth drivers across geographies diversify revenue streams, strengthening resilience of the South America electronic security market against localized slowdowns.

Competitive Landscape

Global heavyweights, including Hikvision, Dahua, Honeywell, and Johnson Controls, share the space with regionally entrenched companies such as Intelbras and Prosegur, resulting in a moderately concentrated arena. Honeywell’s USD 4.95 billion purchase of Carrier’s access business adds LenelS2, accelerating its cloud control offerings in South America. Intelbras, ranked high with USD 434.44 million revenue, posted 12.3% growth by penetrating mid-tier retail and residential segments.

Allied Universal’s spree of five acquisitions, Siete24 LTDA, Infotec SAS, Celar Security, Soltes Technology, and Triton, brings aggregate USD 490 million revenue under its umbrella, reinforcing a blended guarding-technology model. Genetec maintains a 13-year run as the Americas' VMS leader, growing 28% annually in access-control licenses by emphasizing cyber-hardening and unified SaaS.

Competitive focus shifts to AI differentiation; startups deliver computer-vision microservices deployable on NVIDIA Jetson modules, challenging incumbents’ monolithic suites. Regional compliance leadership also matters: vendors offering LGPD-ready audit logs or ANCI-compatible SIEM integrations secure bidding advantages. Mid-sized resellers consolidate to achieve scale, often via strategic alliances with telecom carriers that bundle security with 5G campus networks. Price pressure persists due to high import tariffs, prompting OEMs to localize assembly in Brazil’s Free Economic Zones to claim tax credits. Overall, rivalry intensifies yet incumbents maintain share through ecosystem lock-in and end-to-end portfolios, situating the South America electronic security market in a dynamic but orderly competitive phase.

South America Electronic Security Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Honeywell International Inc.

NEC Corporation

Bosch Sicherheitssysteme GmbH

Zhejiang Dahua Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Axis Communications launched the AXIS S1228 AI-Optimized Server with 28 licenses and 12 TB storage.

- April 2025: Allied Universal acquired Celar Security and Soltes Technology in Colombia, extending its South American presence through five deals totaling ~USD 490 million annual revenue.

- March 2025: Chile’s Cybersecurity Framework Law became fully enforceable, granting ANCI authority to impose fines up to 40,000 UTM for delayed incident reporting.

- February 2025: Honeywell unveiled plans to split into Automation, Aerospace Technologies, and Advanced Materials divisions, keeping security solutions within Automation.

South America Electronic Security Market Report Scope

Electronic security refers to a system that can be used to provide security and operate electronically. It performs security operations, surveillance, access control, alarming, and intrusion control for a facility or area.

The South America Electronic Security Market Report is Segmented by Product Type (Surveillance Security System, Alarm System, Access-Control System, Integrated Security Platform, and Perimeter Intrusion Detection System), End-User Industry (Government and Public, Transportation and Infrastructure, Industrial and Manufacturing, Banking, Financial Services and Insurance (BFSI), Hospitality and Leisure, Retail and E-commerce, Residential, Healthcare, and Other End-User Industries), Offering (Hardware, Software, and Services), Deployment Mode (On-Premises, Cloud-Based, and Hybrid), and Country (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Surveillance Security System |

| Alarm System |

| Access-Control System |

| Integrated Security Platform |

| Perimeter Intrusion Detection System |

By End-user Industry

| Government and Public |

| Transportation and Infrastructure |

| Industrial and Manufacturing |

| Banking, Financial Services and Insurance (BFSI) |

| Hospitality and Leisure |

| Retail and E-commerce |

| Residential |

| Healthcare |

| Other End-user Industries |

By Offering

| Hardware |

| Software |

| Services |

By Deployment Mode

| On-Premises |

| Cloud-Based |

| Hybrid |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Surveillance Security System |

| Alarm System | |

| Access-Control System | |

| Integrated Security Platform | |

| Perimeter Intrusion Detection System | |

| By End-user Industry | Government and Public |

| Transportation and Infrastructure | |

| Industrial and Manufacturing | |

| Banking, Financial Services and Insurance (BFSI) | |

| Hospitality and Leisure | |

| Retail and E-commerce | |

| Residential | |

| Healthcare | |

| Other End-user Industries | |

| By Offering | Hardware |

| Software | |

| Services | |

| By Deployment Mode | On-Premises |

| Cloud-Based | |

| Hybrid | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the 2025 value of the South America electronic security market?

It was USD 4.58 billion in 2025, reflecting ongoing urban-security investments.

How fast will the market grow through 2030?

Forecasts indicate a 6.50% CAGR, taking the value to USD 6.28 billion by 2030.

Which segment is growing the quickest?

Integrated Security Platforms are the fastest-growing product segment at 7.11% CAGR.

Why is Brazil dominating regional demand?

Brazil combines substantial public procurement reforms and USD 2.5 billion in private e-commerce infrastructure spending.

How are cloud services influencing buyer decisions?

Cloud-native platforms reduce upfront costs and address skills shortages, driving the strongest 7.29% CAGR among offerings.

Page last updated on: