Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

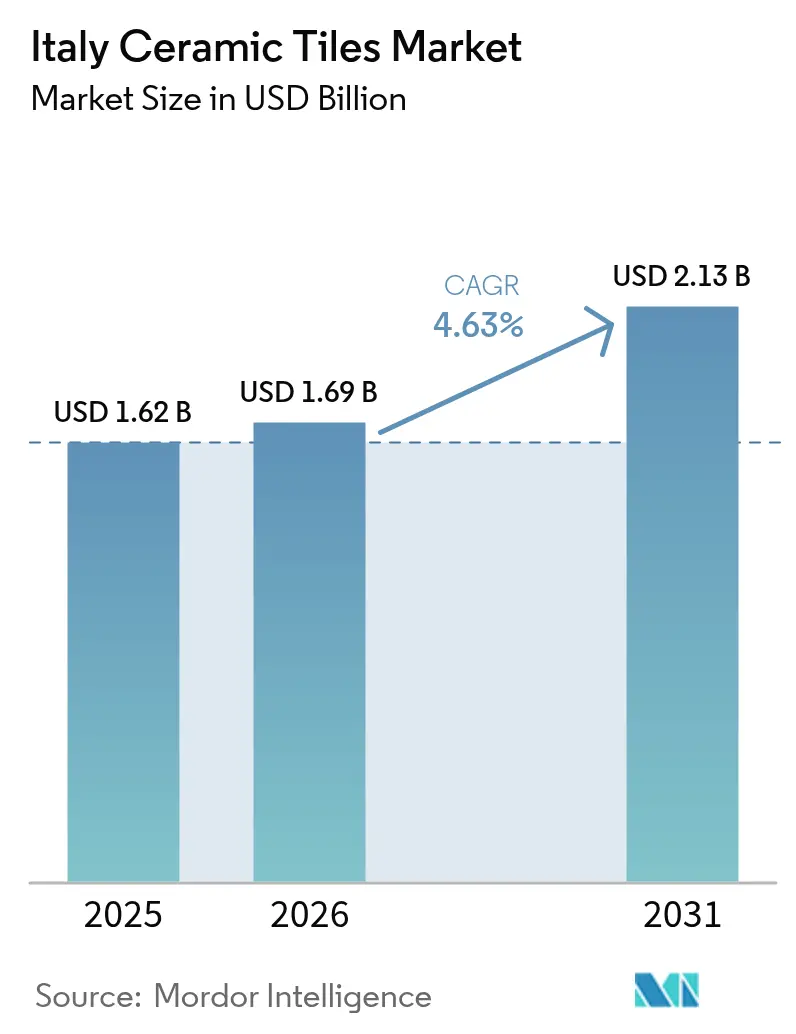

| Base Year Market Size (2025) | USD 1.62 Billion |

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

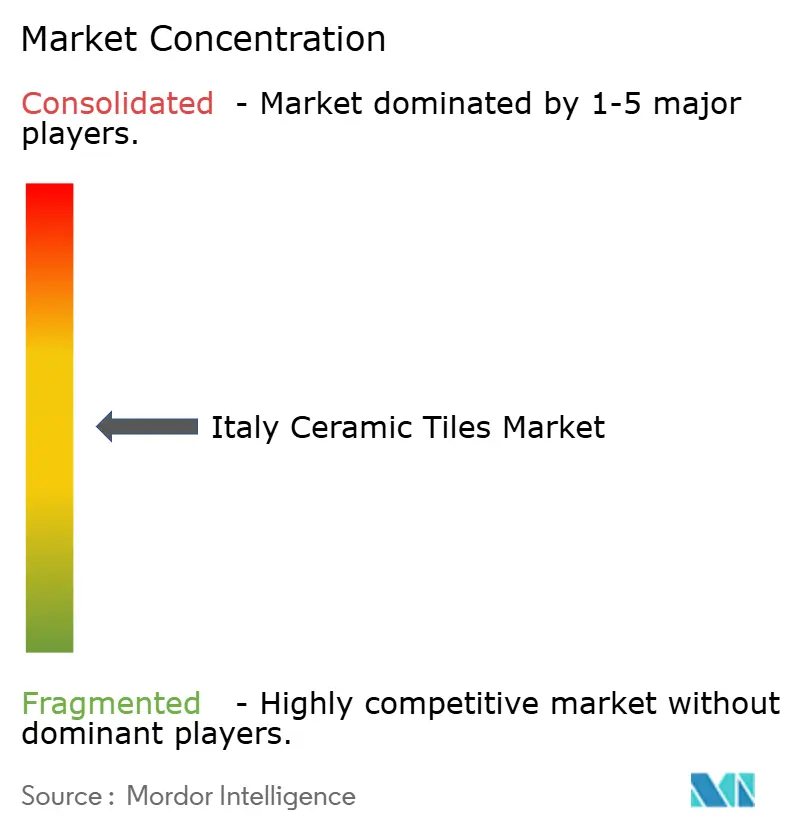

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Ceramic Tiles Market Analysis by Mordor Intelligence

The Italy ceramic tiles market size is expected to grow from USD 1.62 billion in 2025 to USD 1.69 billion in 2026 and is forecast to reach USD 2.13 billion by 2031 at 4.63% CAGR over 2026-2031. Consistent renovation activity, premium large-format adoption, and digital-printing customization lift average selling prices as manufacturers counter energy-intensive cost structures. Fiscal incentives such as the Bonus Bagno 2025 spur bathroom upgrades, while the work-from-home shift channels household spending toward interior improvement. Northwest Italy’s production cluster anchors domestic supply, yet Central Italy records the fastest regional growth on the back of historic property refurbishments. Rising energy costs and competition from luxury vinyl tile (LVT) alternatives temper the otherwise steady expansion.

Key Report Takeaways

- The Italy ceramic tiles market stands at USD 1.62 billion in 2025 and is projected to reach USD 2.13 billion by 2031, reflecting a 4.63% CAGR.

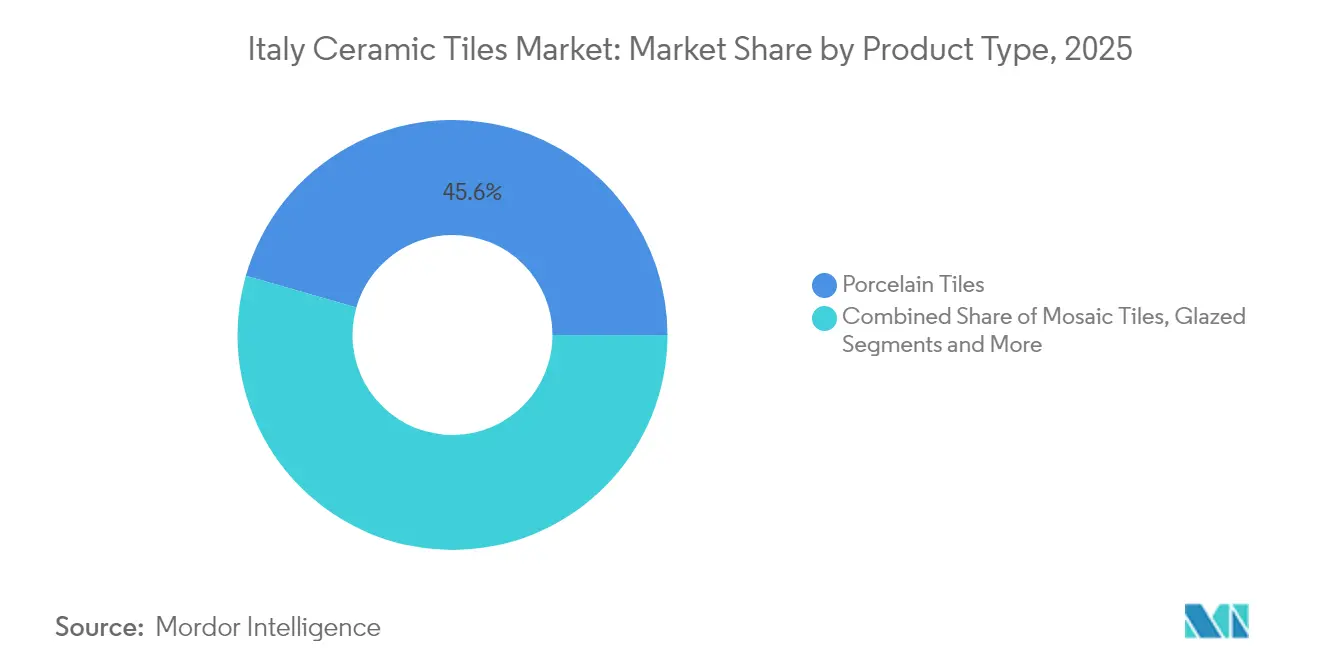

- By product type, porcelain tiles lead national demand with 45.55%of the Italy ceramic tiles market share in 2025, while mosaic tiles record the fastest 5.02% CAGR through 2031.

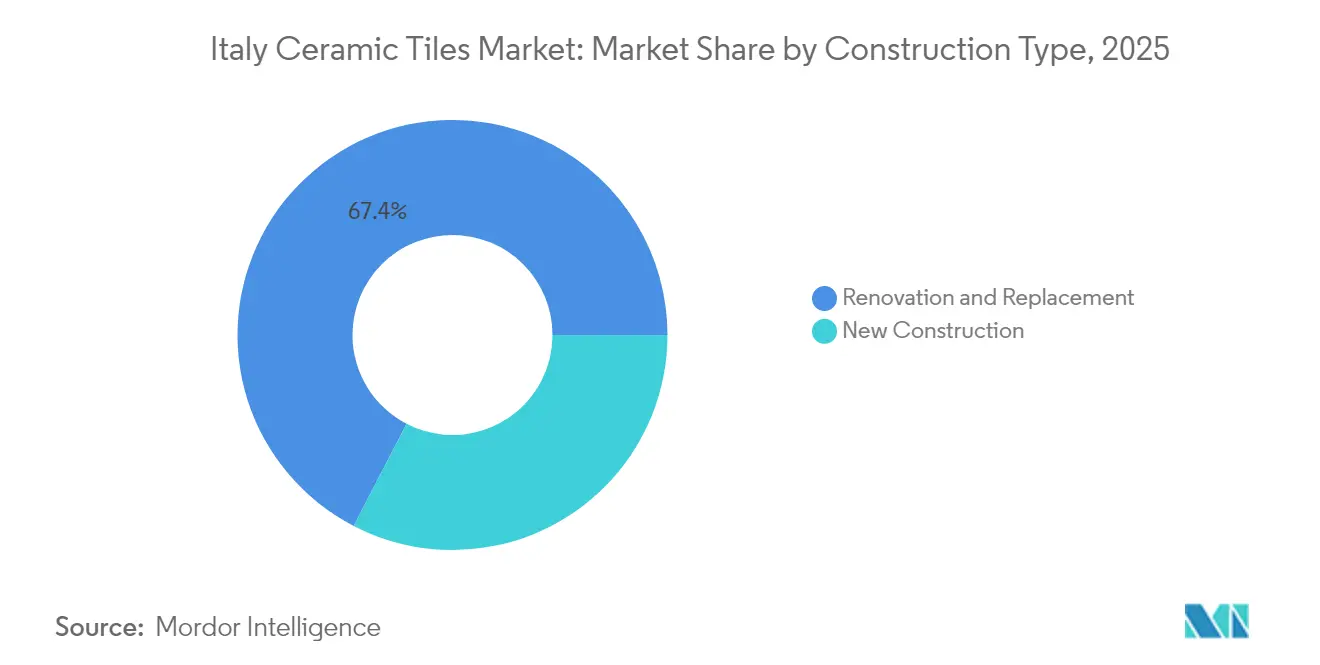

- By end-user, renovation drives 67.40% of overall sales, supported by the Bonus Bagno 2025 program that offers 50% tax deductions on bathroom upgrades up to EUR 48,000 per property.

- By Construction Type, Renovation and Replacement drive 67.40% of Italy's ceramic tile market share in 2025, and Online Retail is the fastest growing construction type at 6.29% CAGR.

- By distribution channel, Home Improvement & DIY Stores rise 40.45% Italy's ceramic tile market share in 2025, and online retail is the fastest-growing distribution channel at 6.29% CAGR as visualization apps and doorstep delivery reshape buyer journeys.

- By Geography, Northwest Italy retains 33.75% Italy's ceramic tile market share to the Sassuolo production cluster, yet Central Italy posts the highest 5.18% CAGR on the back of historic building refurbishments and tourism projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for energy-efficient renovations | 1.2% | National, strongest in Northwest and Central Italy | Medium term (2-4 years) |

| Aging residential building stock driving renovation activity | 1.8% | National, concentrated in urban areas | Long term (≥ 4 years) |

| Export-aligned domestic production boosting local brand equity | 0.7% | Northwest Italy primarily, spillover to Northeast | Long term (≥ 4 years) |

| Consumer preference for large-format porcelain slabs | 1.1% | National, premium segments in major cities | Medium term (2-4 years) |

| Work-from-home trend elevating home-improvement spending | 0.9% | National, stronger in Northern regions | Short term (≤ 2 years) |

| Digital-printing customization enabling premium pricing | 0.8% | National, manufacturing centers in Emilia-Romagna | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Energy-Efficient Renovations

The Bonus Bagno 2025 program grants 50% tax deductions on bathroom upgrades up to EUR 48,000, directly lifting ceramic tile demand in renovation projects[1]Source: Gruppo Più, “Bonus Bagno 2025 Guidelines,” gruppopiu.it. Structured payment and documentation rules favor professional installers and formal retail channels. Uptake is strongest in Northern Italy where property values justify premium finishes and higher renovation budgets. The scheme’s alignment with EU green-home directives further accelerates energy-efficient refurbishments that bundle thermal and aesthetic upgrades. As compliance processes grow more transparent, predictable cycles of bathroom remodeling underpin mid-term market stability. Property owners increasingly view ceramic tile installations as dual-purpose investments that satisfy both regulatory compliance and design enhancement objectives. The program's documentation requirements, including invoice retention and permit compliance, favor established tile retailers and professional installation services over informal market channels.

Aging Residential Building Stock Driving Renovation Activity

Italian housing completed during post-war reconstruction now hits its 15-20-year maintenance window, driving predictable replacement cycles for ceramic finishes. Urban centers combine older housing with higher disposable income, facilitating premium tile adoption despite economic headwinds. Homeowners increasingly elevate design quality alongside structural fixes, lifting average transaction values. Accessibility retrofits in multi-storey buildings enlarge bathroom surface areas, boosting square-meter demand. These factors extend growth momentum beyond new-build volatility. The shift from functional to design-driven renovations reflects changing homeowner priorities, favoring premium materials over basic replacements. Accessibility compliance requirements in aging buildings create additional tile replacement opportunities, particularly in bathroom and common area applications where slip resistance and maintenance considerations drive material selection.

Consumer Preference for Large-Format Porcelain Slabs

Slabs measuring up to 160 × 320 cm with 3.5 mm thickness offer seamless looks that resonate with contemporary design. Production complexity creates high entry barriers, keeping margins healthy for leading Italian brands. Specialized handling and installation skills concentrate value across the supply chain, rewarding certified installers. Expanded use on counters and façades enlarges addressable demand beyond floors and walls. Domestic producers gain an edge because shipping constraints hamper imported competition in this oversized category. The concentration of export-oriented production in Northwest Italy creates regional economic multiplier effects that strengthen local market dynamics. Global supply chain disruptions have highlighted the value proposition of domestic production, reducing lead times and customization flexibility compared to imported alternatives.

Work-From-Home Trend Elevating Home-Improvement Spending

Hybrid work increases daily use of kitchens, bathrooms, and living areas, prompting households to renovate. Budgets formerly allocated to office leases redirect to residential comfort improvements, with tiles selected for durability and easy cleaning. Video meetings heighten awareness of interior aesthetics, driving upgrades that showcase premium finishes on camera. Northern Italy’s knowledge economy hubs display the strongest renovation spend linked to remote work. As flexible work patterns become permanent, this driver sustains long-term volume and value growth. The weight and handling challenges of large-format tiles favor local production over imports, strengthening domestic manufacturers' competitive positioning. Design flexibility through digital printing on large surfaces enables mass customization that commands significant price premiums over standard format alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices raising kiln operating costs | -1.4% | National, concentrated in manufacturing regions | Short term (≤ 2 years) |

| Competition from luxury-vinyl-tile (LVT) alternatives | -0.9% | National, strongest in residential segments | Medium term (2-4 years) |

| Skilled tile-layer labour shortages in key regions | -0.6% | Regional, acute in Northern Italy | Medium term (2-4 years) |

| Stricter silica-dust regulations increasing installation costs | -0.4% | National, affecting installation practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Prices Raising Kiln Operating Costs

Energy accounts for roughly 30% of production costs, exposing manufacturers to gas-price swings[2]Source: Cerame-Unie, “Energy Cost Impacts on European Ceramic Production,” cerame-unie.eu. Kilns must run continuously, limiting flexibility to throttle output during price spikes. Although 28 firms have installed cogeneration units to trim bills, capital intensity delays widespread adoption. Higher costs flow into selling prices, risking demand softness when home budgets tighten. Long-term hydrogen-fired kilns promise relief but need further validation. Regional energy price variations within Italy create competitive imbalances between manufacturing locations, potentially influencing long-term production geography. Alternative energy sources and hydrogen kiln technologies represent long-term solutions but require substantial infrastructure investments and technological validation. The correlation between energy costs and ceramic tile pricing creates consumer resistance during periods of rapid cost increases, potentially constraining demand growth during energy market volatility.

Competition from Luxury-Vinyl-Tile (LVT) Alternatives

LVT products mimic stone visuals at lower install cost and lighter weight, tempting price-sensitive homeowners. Acoustic comfort and rapid installation bolster LVT adoption in offices and retail. Ceramic producers counter with thin-gauge porcelain that reduces weight while retaining durability, but training installers adds expense. Consumer education on hygiene and lifespan advantages remains critical to defend share. Southern regions with tighter budgets show the highest susceptibility to LVT substitution. The development of thin-gauge ceramic tiles represents the industry's response to LVT competition, offering reduced weight and installation complexity while maintaining ceramic performance characteristics. Regional preferences vary significantly, with Northern Italy's design consciousness providing greater resistance to LVT substitution compared to price-sensitive Southern markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Innovation

Porcelain tiles held 45.55% of the Italy ceramic tiles market share in 2025, reflecting their ≤0.5% water absorption and frost resistance. Digital printing delivers stone or wood aesthetics while preserving ceramic durability, pushing premium positioning. Large-format porcelain slabs expand architectural uses from floors to countertops, raising average selling prices. Mosaic tiles log the fastest 5.02% CAGR on design trends that favor textural detail in high-end bathrooms. Recycled-glass and thin-gauge innovations deepen sustainability credentials and open façade opportunities.

Glazed ceramics retain demand among budget-oriented buyers yet face LVT pressure in entry ranges. Handmade and decorative categories cater to luxury renovations that value artisanal heritage, supporting export success. Iron-rich clay formulations widen raw-material sourcing and mitigate reliance on Ukrainian supplies. Up to 63% recycled content collections signal progress toward circularity. Collectively, product diversity enables manufacturers to address mainstream renovation while extracting value from niche design projects. The handmade segment preserves traditional craftsmanship techniques that differentiate Italian products in global luxury markets. Regulatory compliance with crystalline silica content averaging 21% in porcelain stoneware drives research into alternative formulations that maintain performance while reducing health exposure risks

By Application: Floor Segment Leads Growth

Floor coverings captured 61.02% of the Italy ceramic tiles market size in 2025 and are projected to grow at a 4.95% CAGR through 2031. Seamless large-format floors reduce grout lines and maintenance, increasing appeal for open-plan interiors. Slip-resistant finishes expand outdoor and hospitality deployment across Italy’s varied climates. Wall applications rise on lightweight panels that simplify retrofits in historic buildings. Roofing retains niche relevance through terracotta traditions and preservation rules. Digital printing technologies enable floor tiles to achieve realistic wood, stone, and fabric textures that expand design possibilities while maintaining ceramic performance advantages. Installation efficiency improvements, including click-lock systems and adhesive innovations, reduce labor costs and installation time for floor applications.

Digital textures let floor tiles replicate hardwood while outperforming it on wear and moisture resistance. Ultra-thin panels ease wall overlays without structural reinforcement, lowering project costs. Hydronic floor heating pairs well with porcelain’s thermal conductivity, boosting comfort upgrades. Antimicrobial glazes attract healthcare and food-service refurbishments seeking hygiene compliance. Together, these technical attributes secure flooring’s lead while allowing cross-category spillovers. Outdoor flooring applications benefit from porcelain's frost resistance and low water absorption properties that ensure long-term performance in Italy's varied climate conditions. The integration of antimicrobial surface treatments addresses hygiene concerns in commercial floor applications, particularly in healthcare and food service environments.

By End-User: Residential Renovation Drives Demand

The residential segment captures 54.35% market share in 2025 with the highest growth rate at 5.08% CAGR for 2026-2031, driven by aging housing stock, government renovation incentives, and work-from-home trends that prioritize domestic environment improvements. Remote work elevates interior quality expectations, translating into premium tile selections. Commercial demand rebounds in hospitality and retail as tourism normalizes, but price sensitivity remains. Healthcare, education, and transport hubs specify technical porcelains with antimicrobial and high-load ratings. Transport hubs, including airports, metro stations, and bus terminals, require extreme durability and slip resistance that porcelain tiles deliver through technical specifications and testing protocols.

Retailers leverage in-store design labs to convert homeowners seeking personalized surfaces. Hotels upgrade spa and lobby areas with large slabs that project luxury branding. Offices prioritize easy-clean floors that meet new wellness standards. Education projects weigh durability against budget limits, often picking standard porcelain. Transport terminals demand extreme wear and slip resistance, preserving a niche for thick-profile stoneware. Transport hub applications require compliance with accessibility standards and extreme weather resistance for both interior and exterior installations. The commercial segment's recovery from pandemic impacts drives renovation activity that favors ceramic tiles' hygiene advantages and long-term performance characteristics.

By Construction Type: Renovation Market Maturity

Renovation and replacement projects dominate with 67.40% market share in 2025 and maintain strong growth at 4.79% CAGR through 2031, reflecting Italy's mature construction market where upgrade cycles drive sustained demand beyond new building activity. Mature housing stock enters 15-20-year refresh windows, guaranteeing sustained tile consumption. Thin-gauge products reduce structural loads, making them ideal for retrofits without slab removal. Government tax credits target refurbishments rather than new construction, further tilting the mix. New-build projects still opt for integrated large-format floors to cut long-term maintenance. The complexity of renovation installations, including substrate preparation and existing material removal, creates opportunities for specialized installation services and premium pricing. Government incentive programs specifically targeting renovation activity, including the Bonus Bagno 2025 initiative, provide sustained demand drivers independent of broader construction cycles.

Renovation installers specialize in dust-controlled cutting to respect occupied dwellings. Owners channel discretionary budgets into higher-quality surfaces when walls are already open for plumbing updates. Predictable replacement cycles aid factory capacity planning and raw-material procurement. Builders specify click-lock systems on greenfield projects to shorten schedules. The dual-channel dynamic lets producers balance steady renovation volumes with sporadic new-build spikes. Renovation market maturity creates predictable replacement cycles that support long-term demand forecasting and capacity planning for manufacturers. The segment's premium pricing potential reflects homeowners' willingness to invest in quality materials during discretionary upgrade projects rather than emergency replacements.

By Distribution Channel: Digital Transformation Accelerates

Home-improvement chains held a 40.45% share in 2025 by offering broad displays and add-on installation services. Online platforms, however, post the quickest 6.29% CAGR to visualization apps and doorstep delivery. Specialist showrooms court architects with exclusive collections and sample libraries. Direct contractor sales streamline bulk orders on commercial sites via digital portals. Omnichannel strategies merge e-commerce convenience with tactile product inspection.

Online retailers invest in robust packaging that withstands parcel networks while limiting breakage. Brick-and-mortar chains enable web orders with store pickup to capture digital shoppers. Boutique showrooms host design workshops that influence high-margin selections. Contractors benefit from jobsite drop-offs that cut handling costs and schedule delays. Integration of augmented reality boosts confidence in color and pattern choices, reducing returns. Installation service integration across channels creates additional revenue opportunities while addressing consumer concerns about tile laying complexity. Regional channel preferences vary significantly, with Northern Italy showing higher online adoption rates while Southern regions maintain stronger preferences for traditional retail relationships.

Geography Analysis

Northwest Italy controlled 33.75% of 2025 revenue, anchored by the Sassuolo district where more than 80% of national output concentrates. Proximity to European export lanes and dense supplier networks underpins manufacturing efficiencies. Twenty-eight local firms operate cogeneration units that tame energy expenses and emissions. Leading brands such as Marazzi, Florim, and Gruppo Concorde drive continuous process upgrades that ripple across smaller peers. The cluster’s global reputation reinforces premium pricing at home and abroad. The region benefits from higher disposable incomes and design consciousness that support premium product adoption rates above national averages. Tourism infrastructure development, including hotel renovations and cultural facility upgrades, provides commercial market opportunities that complement residential demand patterns.

Northeast Italy maintains solid share through diversified capacity and Central European market access. Experienced labor and mid-scale factories excel in custom orders that large players bypass. Central Italy enjoys the fastest 5.18% CAGR as historic city renovations and tourism projects demand high-spec tiles. Rome and Florence renovations favor artisanal aesthetics aligned with preservation guidelines. Regional disposable incomes sustain premium purchases beyond simple functional replacements. The region benefits from higher disposable incomes and design consciousness that support premium product adoption rates above national averages. Tourism infrastructure development, including hotel renovations and cultural facility upgrades, provides commercial market opportunities that complement residential demand patterns.

Southern regions and islands trail in revenue yet hold untapped potential amid infrastructure and tourism expansion. Mediterranean climates reward ceramic durability and thermal inertia in resort developments. EU structural funds finance public building upgrades that specify slip-resistant surfaces. Emerging local clay extraction reduces logistics costs for future plants. As distribution networks strengthen, the South could narrow the gap with northern counterparts. The development of local distribution networks and installation service capabilities supports market expansion in previously underserved areas. Clay deposits in Southern Italy, including Plio-Pleistocene formations near Tricarico, provide raw material opportunities for local production development. Tourism sector recovery drives renovation activity in hospitality facilities that require durable, attractive flooring and wall solutions suitable for high-traffic environments.

Competitive Landscape

The Italy ceramic tiles market increasingly depends on manufacturers' ability to balance technological innovation with environmental responsibility. Companies must continue investing in digital manufacturing capabilities while developing sustainable production processes to meet evolving regulatory requirements and consumer preferences. The ability to offer customized solutions and quick-to-market designs will become increasingly important as the market shifts toward made-to-order production models. Manufacturers need to strengthen their direct-to-consumer channels while maintaining traditional distribution relationships, requiring sophisticated omnichannel strategies and enhanced digital capabilities.

Market leaders must focus on developing anti-bacterial and health-conscious product lines to address growing consumer awareness of hygiene factors. Companies need to maintain strong research and development capabilities to continue advancing in areas like digital printing, surface treatments, and material innovations. Success will also depend on manufacturers' ability to manage rising energy costs and environmental regulations while maintaining production efficiency.

The development of strong brand identities and design leadership will remain crucial for competing in premium market segments, where Italian manufacturers face increasing competition from other European producers. Building robust export networks while maintaining domestic market share will require a careful balance of resource allocation and market positioning strategies. The integration of architectural ceramics and ceramic wall covering solutions will further enhance the aesthetic appeal and functionality of products, catering to evolving consumer demands.

Italy Ceramic Tiles Industry Leaders

Marazzi Group

Florim S.p.A.

Gruppo Concorde

Panaria Group

Atlas Concorde

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Cosentino confirmed a USD 270 million U.S. plant using 100% renewable energy and 99% water reuse.

- July 2025: Mirage launched ReGea tiles with 63% recycled content, including photovoltaic glass.

- March 2025: Daltile, Marazzi, and American Olean earned KBIS 2025 booth honors for comprehensive design displays.

- February 2025: Ceramics of Italy announced its first KBIS showcase, bringing 15 Italian manufacturers to Las Vegas.

Italy Ceramic Tiles Market Report Scope

Clays and other natural resources, such as sand, quartz, and water, are combined to create ceramic tiles. They are generally utilised as bathroom wall and kitchen floor surfaces in homes, businesses, restaurants, and other establishments.The report provides a comprehensive background analysis of the Italy ceramic tiles market, including an assessment of the parent market, emerging trends in segments and regional markets, significant changes in market dynamics, and a market overview. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across various key points in the value chain. The Italy Ceramic Tiles Market is segmented By Product (Glazed, Porcelain, Scratch Free, Other Products), By Application (Floor Tiles, Wall Tiles, Other Applications), By Construction Type (New Construction, Replacement, and Renovation), and By End User (Residential, Commercial). The report offers the market sizes and forecasts in value (USD million) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Northwest Italy |

| Northeast Italy |

| Central Italy |

| South & Islands |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Northwest Italy | |

| Northeast Italy | ||

| Central Italy | ||

| South & Islands | ||

Key Questions Answered in the Report

How large is the Italy ceramic tiles market in 2026?

The Italy ceramic tiles market size stands at USD 1.69 billion in 2026.

What CAGR is expected for Italian ceramic tile sales through 2031?

Revenue is projected to grow at a 4.63% CAGR between 2026 and 2031.

Which product type leads national demand?

Porcelain tiles retain leadership with 45.55% market share due to durability and design range.

Why is Central Italy the fastest-growing region?

Historic building renovations and tourism projects drive a 5.18% CAGR in Central Italy.

Page last updated on: