Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

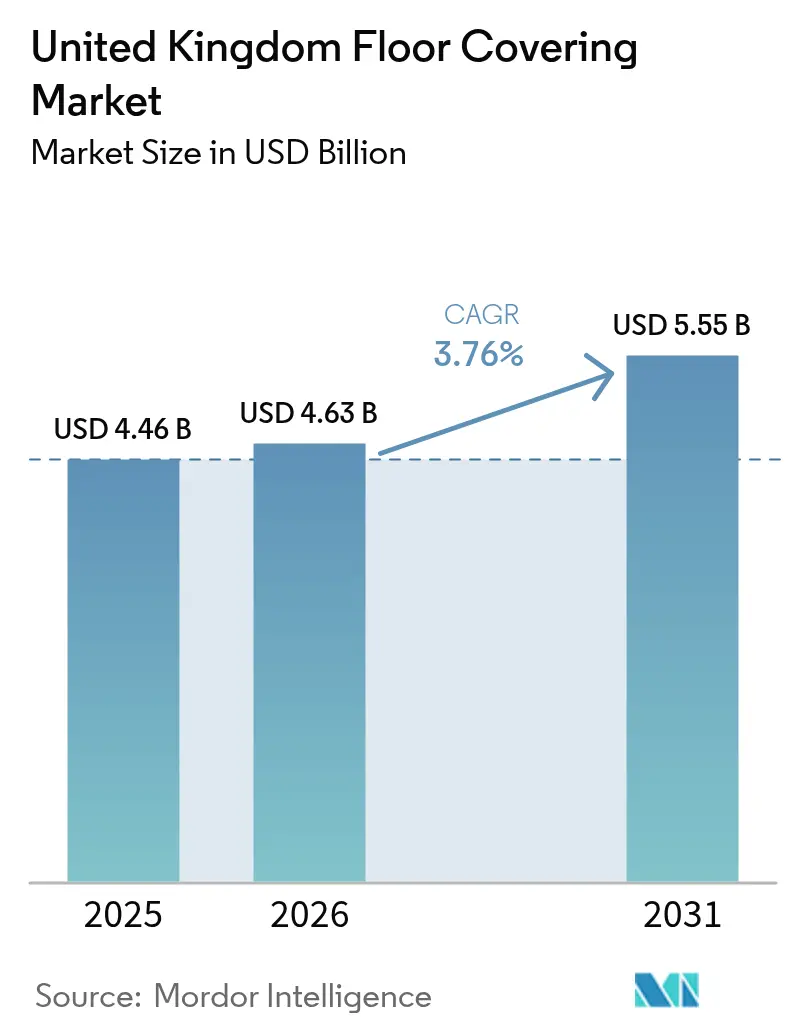

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 4.63 Billion |

| Market Size (2031) | USD 5.55 Billion |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

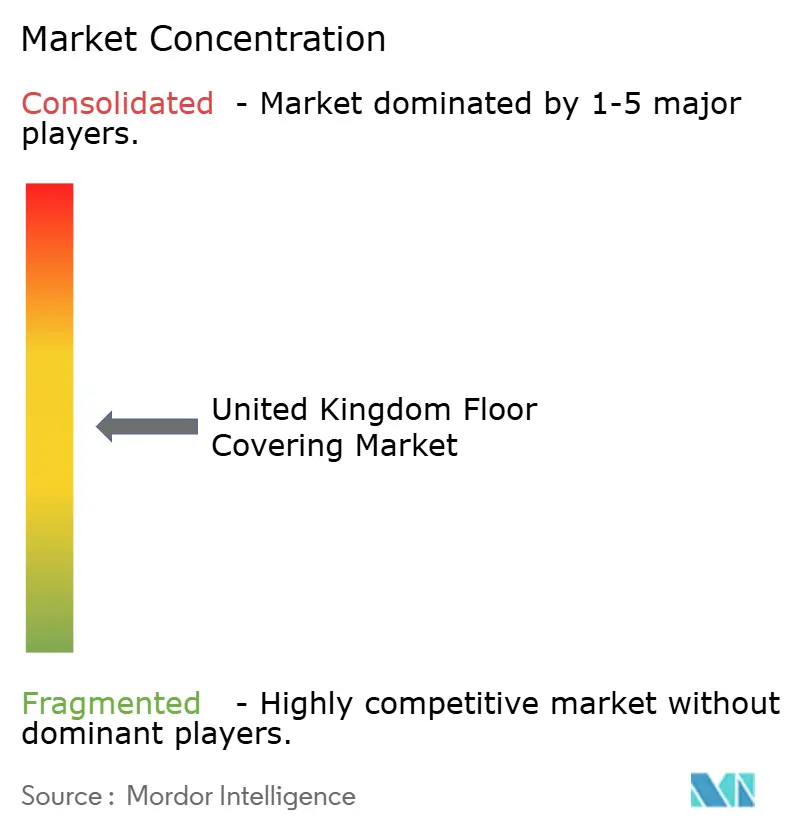

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Floor Covering Market Analysis by Mordor Intelligence

The United Kingdom floor covering market size reached USD 4.46 billion in 2025 and is projected to increase to USD 4.63 billion in 2026, advancing to USD 5.55 billion by 2031 at a 3.8% CAGR. Growth in 2026 reflects measured expansion as net-zero housing retrofits, care-home refurbishments, and hybrid-office redesigns align with digital procurement and specification, which is changing product choices and supplier positions[1]Editorial Team, “Warm Homes Plan and Retrofit Priorities,” Federation of Master Builders, fmb.org.uk . National retrofit programs that address 20 million uninsulated floors and the Warm Homes Plan to upgrade 5 million homes are directing attention to hard-surface solutions that balance thermal performance with low embodied carbon, in line with compliance with the Future Homes Standard 2025. Digital specification workflows tied to BIM and NBS are now common, with sustainability targets frequent in project briefs, which favors suppliers with Environmental Product Declaration-ready portfolios and robust product data. These shifts support resilient formats such as LVT in healthcare and office refurbishments and reinforce competitive advantage for brands that integrate EPDs, BIM objects, and take-back programs into bids for public projects where embodied carbon is evaluated with cost.

Key Report Takeaways

- By product type, non-resilient floor covering led with 43.0% of the United Kingdom floor covering market share in 2025, while resilient floor covering is forecast to expand at a 5.9% CAGR through 2031.

- By construction type, new construction held 53.8% of the United Kingdom floor covering market share in 2025, while renovation and replacement is projected to record the highest CAGR at 4.9% through 2031.

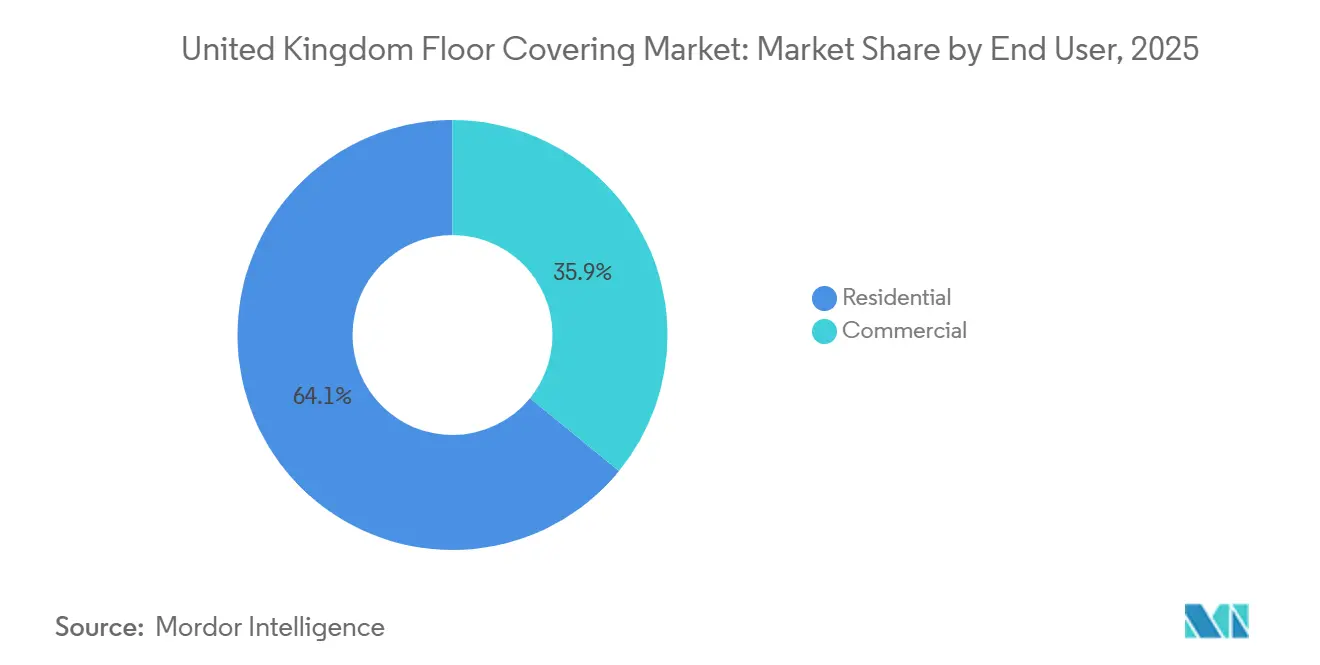

- By end user, residential accounted for a 64.0% share in 2025 and is expected to advance at a 4.4% CAGR through 2031.

- By distribution channel, B2C retail accounted for 66.1% in 2025 and is projected to grow at a 5.1% CAGR through 2031.

- By geography, England led with 71.6% revenue share in 2025, while Scotland is forecast to expand at a 5.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-Zero Housing Retrofit Programs Are Accelerating Flooring Upgrades | +1.2% | England and Scotland, with spillover to Wales and Northern Ireland, in social housing | Medium term (2-4 years) |

| Shift From Carpet to Hard-Surface Floors for Hygiene and Low Maintenance | +0.9% | Global, with a concentration on healthcare-dense England and an aging population in Scotland | Short term (≤ 2 years) |

| Healthcare And Care-Home Refurbishments Favoring Safety and Resilient Floors | +0.8% | England, Scotland, Wales, healthcare estates, and care sites | Medium term (2-4 years) |

| Hybrid-Work Office Redesigns Boost Acoustic and Modular Flooring | +0.6% | England urban cores, Scotland Tier 1 cities | Short term (≤ 2 years) |

| Embodied-Carbon Procurement and EPD Requirements Are Reshaping Material Choices | +0.7% | National, early gains in London, Manchester, and Edinburgh public projects | Long term (≥ 4 years) |

| BIM- And NBS-Driven Digital Specification Increasing Wins for Spec-Ready Brands | +0.5% | National, concentrated in public and large commercial projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Net-Zero Housing Retrofit Programs Accelerating Flooring Upgrades

A large housing stock with uninsulated floors is driving coordinated retrofit activities that trigger secondary flooring replacement when insulation works expose subfloors or when homeowners choose to improve finishes during the same project window. The Warm Homes Plan to upgrade millions of homes is channeling demand toward hard-surface systems that couple thermal performance, moisture tolerance, and compatibility with underfloor heating in line with Future Homes Standard 2025 goals for lower operational emissions. In practice, local programs are bundling walls, loft, and floor insulation with compliant coverings, which is improving throughput for manufacturers that can document U-value contributions and embodied carbon in EPDs at the tender stage[2]Editorial Team, “Sustainability and EPD Guidance for Flooring,” Contract Flooring Association, cfa.org.uk. Public clients are pushing for verifiable low-carbon materials, so suppliers with published cradle-to-grave carbon figures and take-back schemes are strengthening bids and reducing risk in framework competitions. These forces are expanding the addressable market for resilient and engineered wood solutions across social landlords and owner-occupiers, which is supportive of the United Kingdom floor covering market over the medium term. Funding continuity after current spending windows will affect the pace of annual installations, but the direction of travel remains supportive of thermally efficient hard surfaces in the United Kingdom floor covering market.

Shift from Carpet to Hard-Surface Floors for Hygiene and Low Maintenance

Post-pandemic design choices and infection control practices in clinical settings are reinforcing the move from broadloom to seamless, resilient, and modular hard surfaces that clean quickly and reduce allergen reservoirs. Open-plan homes and pet-friendly households are also choosing LVT and laminate for easy upkeep and compatibility with underfloor heating, reshaping the United Kingdom floor-covering market toward hard surfaces in ground-floor living spaces. Leading brands have refreshed their rigid-core and click-install LVT collections to improve installation speed and water resistance, while preserving wood and stone aesthetics that appeal to residential and boutique commercial buyers. Healthcare and care settings favor seamless safety vinyl and coving to minimize dirt traps and support deep cleaning protocols required by infection prevention teams, which further expand resilient volumes in the United Kingdom floor covering market[3]Editorial Team, “Slip Resistance Assessment Tools and Guidance,” Health and Safety Executive, hse.gov.uk . As these preferences settle into long-term specifications, carpet remains important in bedrooms and select hospitality use cases, but it yields share to hard surfaces in high traffic and clinical zones within the United Kingdom floor covering market. Manufacturers are tailoring antimicrobial, acoustic, and slip-resistant properties to meet these needs, aligning product roadmaps with compliance and maintenance priorities in 2026.

Healthcare and Care-Home Refurbishments Favoring Safety and Resilient Floors

Compliance with Building Regulations Part M and HSE slip resistance guidance is pushing operators toward safety vinyl and resilient systems with antimicrobial performance and integral cove skirting, making these settings a steady buyer group even as broader construction slows. Demographic aging is increasing the volume and complexity of care provision, lifting demand for surfaces that reduce fall risk and enable effective cleaning in shared spaces and wet rooms in the United Kingdom floor covering market. NHS estate upgrades and diagnostic hub rollouts must manage heavy footfall and chemical exposure, so they specify commercial-grade resilient systems with durable surfaces supported by United Kingdom-based technical services. Resilient collections with acoustic underlayers that achieve 18 to 19 dB impact sound reduction are also being selected for education and assisted living, helping facilities meet acoustic guidelines typically used in schools and now adopted by many project teams. Suppliers that can bundle EPDs, BIM objects, and maintenance protocols into submission packs are improving prequalification scores for healthcare frameworks, which is material for winning multi-site rollouts in the United Kingdom floor covering market. This compliance-anchored procurement pattern stabilizes resilient volumes and reduces sensitivity to cyclical swings, sustaining specification momentum through 2026.

Embodied-Carbon Procurement and EPD Requirements Reshaping Material Choices

Whole-life carbon assessments and embodied carbon reporting are now embedded in many council and central government projects, shifting decisions toward products with third-party-verified EPDs and lower cradle-to-grave emissions. Framework and tender documents often ask for A1-A3 carbon figures and for verification of renewable energy in manufacturing, which advantages suppliers with published data and United Kingdom-made ranges that support delivery and disclosure in the United Kingdom floor covering market. Manufacturers that disclose low embodied carbon for resilient and carpet tile backings or that supply carbon-negative wood and linoleum lines are seeing increased shortlisting in university, council, and NHS projects. Product development investments in bio-attributed inputs and circular polymers are yielding EPDs that track lower supply-chain emissions, helping unlock BREEAM credits and corporate net-zero targets among institutional clients. EPD-ready portfolios also reduce administrative burden for contractors and architects by simplifying documentation and aligning designs to planning requirements that call out material circularity and biodiversity net gain objectives. This procurement filter is expected to strengthen over time, further rewarding disclosure-ready brands in the United Kingdom floor covering market as local authorities refine embodied carbon caps in refurbishments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sluggish Housing Transactions Lengthening Residential Replacement Cycles | -0.8% | England and Wales mortgage-dependent markets; Scotland is less exposed | Short term (≤ 2 years) |

| Budget Constraints and Delays in Public Capital Projects | -0.6% | National, acute in local authorities with tighter reserves | Medium term (2-4 years) |

| UKCA Marking and VOC Emissions Compliance Are Raising Import and Testing Costs | -0.4% | National, disproportionate impact on import-reliant suppliers | Medium term (2-4 years) |

| Landfill Tax and Waste Rules Are Increasing Disposal Costs for Uplifted Flooring | -0.3% | England and Wales; separate regimes in Scotland and Northern Ireland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sluggish Housing Transactions Lengthening Residential Replacement Cycles

Transaction activity in 2026 remains subdued relative to pre-pandemic levels, which is delaying pre-sale refreshes and post-purchase upgrades that usually drive a share of residential flooring demand in the United Kingdom floor covering market[4]Editorial Team, “UK Mortgage Market and Household Finance,” UK Finance, ukfinance.org.uk . Higher mortgage rates are discouraging first-time buyers and movers, lengthening replacement cycles, and reducing impulse upgrades tied to ownership changes. This pattern weighs on volumes at large B2C retailers and independents that rely on active home movers, while online platforms that offer rapid delivery capture a greater share of the smaller active buyer pool. Regional differences matter because Scotland’s conveyancing system and household finances have moderated the decline, supporting steadier transaction-linked home purchases in key urban markets. Replacement cycles are stretching for carpet and some entry-level hard surfaces as households defer discretionary refits, shifting the mix toward higher-warranty products that justify longer service life in the United Kingdom floor covering market. This near-term demand drag is mitigated in part by retrofit programs and essential replacements, but it will still cap upside in 2026.

Budget Constraints and Delays in Public Capital Projects

Procurement delays and profile shifts in public budgets are slowing installations in schools, hospitals, and civic buildings, which pushes award and fit-out timelines into later years in the United Kingdom floor covering market. Local authorities managing inflation-linked overruns are deferring non-urgent flooring replacements in part of their estate, which creates a backlog that could unwind when funding windows stabilize. Central allocations in 2025 and 2026 prioritized urgent capacity increases in healthcare and special education, leaving fewer resources for maintenance of existing assets. Suppliers targeting public work face longer tender-to-order cycles and greater value engineering to meet tight budgets, compressing margins and increasing bid attrition. Contractors are prioritizing higher-margin projects with secured funding, such as healthcare and private data centers, leaving parts of the education and office refurbishment segments underserved. The result is a slower public segment in 2026 with a pipeline that supports a later release of deferred flooring demand in the United Kingdom floor covering market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Resilient Floors Outpace Legacy Categories

Non-resilient floor covering held a 43.0% share in 2025, reflecting enduring demand for ceramic, porcelain, and engineered wood in core applications, while resilient floor covering is the fastest-growing segment, with a 5.9% CAGR from 2026 to 2031. LVT adoption in healthcare, care, and hybrid office settings is driving this trajectory, as antimicrobial performance, acoustic comfort, and low maintenance are now prioritized in specifications for large projects in the United Kingdom floor covering market. Resilient sheet vinyl holds its own in social housing and industrial spaces where budgets are tight, while click-install LVT is gaining share through installation speed and realistic designs that suit refits. Rubber and cork remain niche but present growth vectors in gyms, play areas, and sustainability-led residential schemes that value impact absorption and bio-based content. Linoleum is rebuilding relevance in low-carbon school projects because of its biogenic content and hygiene credentials, which pair with United Kingdom-made lines that can document renewable energy and shorter logistics. These preferences favor resilient platforms that can meet acoustic, safety, and hygiene checklists in the United Kingdom floor covering market.

Carpet and rugs account for a material share of installed floors, yet the structural tilt toward hard surfaces for hygiene and upkeep continues to pressure broadloom in high-traffic and clinical settings. Premium carpet maintains traction in luxury residential and boutique hospitality through distinct patterns and textures that serve as feature elements rather than default finishes for entire floors. Within non-resilient porcelain tiles, new capacity commitments strengthen the supply of large formats for commercial lobbies and transport hubs, consolidating their share in heavy-wear zones. Engineered wood expands within the wood category due to its dimensional stability under underfloor heating and because some ranges carry carbon-negative EPDs that appeal to low-carbon briefs. Laminate remains relevant in rental and budget new builds where replacement speed is critical, while rigid-core LVT captures value at similar price points, offering superior water tolerance in the United Kingdom floor covering market. Non-resilient categories remain core to kitchen, bath, and entry areas, while resilient families capture most growth vectors anchored in compliance, acoustics, and low maintenance.

By Construction Type: Renovation Gains as New Build Stalls

Renovation and replacement is the fastest-growing segment, with a 4.9% CAGR from 2026 to 2031, while new construction held a 53.8% share in 2025 as completions and build-to-rent activity sustained base volumes. Mortgage constraints and cautious buyers are reinforcing an upgrade-in-place mindset that keeps homeowners in their properties longer, improving EPC ratings and comfort, which boosts demand for click-install LVT and laminate selected through retail channels in the United Kingdom floor covering market. Social housing landlords are also running fabric-first retrofits to reach EPC Band C, which brings subfloor preparation and flooring replacements into scope in many properties. Commercial refurbishments reflect hybrid work demand for modular, acoustically friendly floors that install quickly and enable configuration changes, sustaining resilient, modular carpet momentum in office, learning, and healthcare facilities. New-construction deliveries have been slower, but per-unit flooring spend has risen in some developments as buyers prefer hard surfaces in key rooms rather than full carpet packages. The United Kingdom floor covering market benefits from this specification uplift even as groundbreakings moderate.

Looking ahead, renovation projects have fewer regulatory triggers than new builds, which helps with approvals and execution speed for time-sensitive commercial and public assets. Public frameworks will continue to release deferred maintenance, especially in education and healthcare, where flooring reaches end of life, and project teams can use take-back or reuse to meet circularity aims. Housebuilder strategies are mixed, with some emphasizing amenity and premium finishes to support value in slower-selling schemes, including wider use of LVT in kitchens, bathrooms, and hallways. Private landlords are also investing in thermal upgrades to meet energy standards, which often entail underfloor insulation and new coverings that withstand higher tenant turnover. The United Kingdom floor covering market will continue to balance unit-volume drivers and per-unit specification upgrades as the cycle evolves through 2026. Renovation mix and digital procurement will determine which suppliers capture the most resilient share gains.

By End User: Residential Dominance with Commercial Resilience

Residential accounted for 64.0% of the 2025 value and is projected to expand at a 4.4% CAGR through 2031, supported by owner-occupier retrofits, PRS upgrades to meet MEES, and social housing programs that bundle floor insulation with new coverings. Product decisions in residential areas emphasize ease of cleaning, compatibility with underfloor heating, and acoustic control for multi-dwelling units, which favor LVT, laminate, and engineered wood in high-use spaces in the United Kingdom floor covering market. Social landlords are standardizing on resilient specifications in wet rooms and high-wear zones to extend replacement cycles and simplify maintenance, while deploying take-back options when available to align with circular goals. Owner-occupiers rely more on retail channels for product selection and installation services, while renters benefit from landlord-led upgrades that manage lifecycle costs and ensure compliance. These patterns anchor residential as the largest end user while shifting the mix toward resilient formats that meet hygiene and sustainability expectations. The United Kingdom floor covering market continues to adapt assortments and services to match these residential needs.

Commercial demand holds a sizable share and grows at a steady pace, such as hybrid offices, hospitality, and select retail formats invest in refurbishments that prioritize durability and acoustics. Healthcare and education, often procured via public frameworks, are among the fastest-growing commercial segments as service provision expands and modernizes, requiring resilient, modular systems documented through EPDs and BIM data. Industrial floors are more polarized, with many facilities using concrete or coatings, while cleanroom, food, and pharma sites demand specialized ESD and chemical-resistant solutions that command premium pricing. Public assets face funding constraints in 2026, but multi-year frameworks provide visibility and eventual release of deferred flooring in schools and civic buildings. These factors unevenly distribute growth, but they still support a consistent pipeline for brands positioned in resilient, modular categories in the United Kingdom floor covering market. End-user diversification remains important for revenue stability because residential cycles can move in the opposite direction from parts of commercial activity.

By Distribution Channel: Retail Holds but B2B Quality Premiums Persist

B2C retail channels commanded a 66.1% share in 2025 and are projected to grow at a 5.1% CAGR to 2031, driven by online hubs, specialty store service, and home center convenience for DIY-oriented purchases. Online platforms that combine digital browsing with regional warehouses and next-day delivery are expanding reach to homeowners and small trade accounts, improving availability and compressing lead times in the United Kingdom floor covering market. Home centers maintain a share among DIY shoppers by bundling adhesives, underlays, and tools, while specialty stores maintain a premium service niche that includes in-home consultations and curated designs. Direct-to-consumer models from design-led brands introduce further choice and put margin pressure on intermediaries by pairing factory ordering with certified fitting networks. This retail dynamism sustains the core channel as transaction volumes ebb, because digital pricing and logistics lower search and switching costs for buyers. The United Kingdom floor covering market will see continued online penetration alongside resilient specialty service models.

B2B contractors and dealer channels hold the remaining share and grow more slowly, but serve as specification influencers that can lift gross margins through technical support and project credit. National housebuilders source directly from select manufacturers under volume deals, while regional contractors and shopfitters rely on trade distributors for logistics, training, and data sheets that simplify compliance in tenders. Public sector procurement through frameworks favors suppliers that can document EPDs, deliver social value, and meet digital maturity standards, which pulls direct relationships with manufacturers into a larger share of awards. B2B growth reflects the broader slowdown in commercial starts, but its strategic weight is high because early engagement with architects and MEP teams can lock in decisions on complex projects. Dealers and manufacturers maintain trade discount structures and field support because these investments drive pull-through and repeat specification in the United Kingdom floor covering market. Over 2026, B2B will remain essential for complex refurbishments and institutional projects even as retail absorbs more residential flows.

Geography Analysis

England accounted for 71.6% of the value in 2025, supported by dense construction activity, office refurbishments, and higher discretionary spending on premium surfaces in major metropolitan areas. Population concentration and large real estate stocks in London and the Southeast underpin baseline demand, while retrofit programs in northern city regions channel resilient volumes into social housing portfolios. Office markets in London, Manchester, and Leeds continue to favor acoustic modular solutions for hybrid layouts, which support resilient and modular carpet selections. Planning conditions that address acoustic performance in office-to-residential conversions are encouraging higher-grade solutions in remaining commercial floors. Retail and hospitality fit-outs vary by submarket, with outlet and convenience formats typically using durable, cleanable coverings in high-traffic settings. England’s growth pace moderates relative to Scotland due to housing liquidity constraints and slower recovery in central office occupancy, yet specifications per unit lean toward hard surfaces in key rooms. These factors keep the United Kingdom floor covering market anchored in England with a strong emphasis on resilient performance and disclosure-ready documentation.

Scotland is projected to post the fastest growth, with a 5.1% CAGR through 2031, as fintech and life sciences investments in Edinburgh and Glasgow feed a steady pipeline of fit-outs and refurbishments. Public programs with robust energy standards are accelerating social housing insulation and associated floor replacements, while commercial tenants prioritize acoustic comfort and wellness features in new developments. Care settings are upgrading to safety vinyl and coved installations to meet stringent infection control and slip-resistance objectives, often more demanding than English guidance. Engineered wood and cork benefit from higher thermal performance targets and embodied carbon objectives in Scottish policy, which guides material choice in residential and public assets. Modular systems dominate Grade A office fit-outs due to flexibility and speed, while resilient lines serve wet areas and high-wear corridors. Suppliers are investing in Scottish architect engagement because the region’s early adoption of digital and carbon disclosure standards informs later English patterns. This creates a visible channel for product innovation to influence the United Kingdom floor covering market.

Wales and Northern Ireland remain smaller contributors but grow steadily on the back of urban revitalization and mixed-use regeneration in Cardiff, Swansea, Belfast, and Derry. Public-private projects in leisure and hospitality specify durable LVT and porcelain for shared spaces to meet safety and maintenance requirements, as defined by Building Regulations and HSE guidance. Budget constraints slow down some public refurbishments, yet stable owner-occupier bases and selective private investments maintain a consistent floor of demand for core categories. Cross-border trade considerations affect Northern Ireland more directly, making United Kingdom-made lines more appealing to certain buyers with tight timelines. Social housing retrofit programs in Wales support floor upgrades, with insulation projects bundled, though at a different scale than in England, where volumes are spread across fewer hubs. Retail channels in both regions rely more on specialty service and targeted logistics to match decentralized demand. These dynamics combine to create disciplined but steady opportunities for suppliers positioned to serve compliance and maintenance-focused specifications in the United Kingdom floor covering market.

Competitive Landscape

The United Kingdom floor covering features several large brands with strong disclosure, manufacturing, and specification capabilities alongside a long tail of importers and specialists that compete on design, service, or price in defined niches. Competitive differentiation is focusing on circular services and digital specifications, where takeback, reuse, and public and corporate buyers now value EPD integration. United Kingdom-based production supports speed and customization for urgent healthcare and education work, which is a critical advantage for framework projects with compressed lead times. Victoria PLC’s ceramics investments add capacity for large-format porcelain that meets heavy-wear commercial needs, reinforcing scale economies in distribution and product mix depth. Design-led specialists sustain premium positioning through curated visuals and direct service that bypasses some retail intermediaries to reach end customers.

Strategic moves highlight capital commitments, sustainability positioning, and go-to-market innovation. Victoria PLC commissioned a Spanish ceramics line to expand output and improve margins in higher-value formats, with commercial sales expected in 2026. Forbo manufactures select carpet tile ranges in the United Kingdom with verified renewable energy, aligning with public tenders seeking low embodied carbon without reliance on offsets. Shaw’s circular platforms and reuse partnerships illustrate how take-back services are becoming procurement differentiators as waste costs rise and clients plan for EPR scenarios. Tarkett’s ReStart program similarly underpins circular commitments and supports embodied carbon claims through verified pathways. On the channel side, Likewise Group has scaled multichannel hubs that combine digital ordering with regional warehouses, improving service levels for retail and trade customers across the United Kingdom floor covering market. These moves show how product, sustainability, and channel strategies integrate to secure specification and repeat business.

Suppliers with in-house technical teams shorten approval cycles, help clients meet Building Bulletin and healthcare guidance, and reduce tender risk for contractors. The widest moats form where brands combine disclosure-ready EPDs, take-back options, BIM objects, and a proof point in the United Kingdom manufacturing, which together lift framework scores and reduce switching in the United Kingdom floor covering market. Niche innovators still find space through distinctive visuals or specialized performance, such as ESD or chemistry-resistant surfaces, but they face higher documentation expectations in 2026. The overall narrative is a steady consolidation of advantages among vertically integrated, disclosure-ready, and digitally fluent players in the United Kingdom floor covering market.

United Kingdom Floor Covering Industry Leaders

Victoria PLC

James Halstead PLC (Polyflor)

Forbo Flooring Systems

Tarkett UK

Karndean Designflooring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Brintons Carpets launched the Self Expression Winter 2026 Collection (Plaid Collection) by Senior Designer Cherise Porretto, celebrating personal heritage through intricate plaid designs that blend traditional motifs with contemporary color palettes, reinforcing the brand's position in premium residential and hospitality carpet segments, where design provenance commands pricing premiums.

- January 2026: Karndean Designflooring launched LooseLay designs at SURFACES 2026, adding 10 wood and stone-inspired designs, including Hawaiian koa and Italian marble, and announced three new Design Aesthetics (Senti, Luma, Dopa•Mine) for spring 2026 launch, targeting residential and boutique commercial projects where installation speed and design flexibility drive specification decisions.

- January 2026: IVC Commercial launched a dedicated housing website for sheet vinyl floors targeting social and affordable housing contractors, streamlining product selection and technical specification for high-volume projects where procurement efficiency and compliance documentation are critical to framework agreement participation.

- November 2025: Victoria PLC commissioned the V4 Spanish ceramics line after two years of development and EUR 31 million capital expenditure, achieving 5.0 million sqm annual capacity with expected incremental EUR 15 million EBITDA at full capacity, with commercial sales starting January 2026, positioning the company as a regional ceramics hub for large-format tiles in commercial and high-end residential applications.

United Kingdom Floor Covering Market Report Scope

Floor covering is applying finish material to form a walking surface. It is made from textiles, felts, resins, rubber, or other natural or artificial substances.

The United Kingdom floor covering market is segmented into material type, end-user, and distribution channel. By material type, the market is sub-segmented into carpet and area rugs, non-resilient flooring, and resilient flooring. By end user, the market is sub-segmented into residential and commercial. By distribution channel, the market is sub-segmented into contractors, specialty stores, home centres, and other distribution channels.

The report offers market size and forecasts in value (USD) for all the above segments.

By Product Type

| Carpet and Rugs | |

| Resilient Floor Covering | Vinyl Sheets & VCT |

| Luxury Vinyl Tiles (LVT) | |

| Linoleum | |

| Rubber Flooring | |

| Cork Flooring | |

| Non-Resilient Floor Covering | Ceramic & Porcelain Tile |

| Natural Stone | |

| Hardwood | |

| Engineered Wood | |

| Laminate |

By Construction Type

| New Construction |

| Renovation & Replacement |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Home Centers |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors/Dealers |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Type | Carpet and Rugs | |

| Resilient Floor Covering | Vinyl Sheets & VCT | |

| Luxury Vinyl Tiles (LVT) | ||

| Linoleum | ||

| Rubber Flooring | ||

| Cork Flooring | ||

| Non-Resilient Floor Covering | Ceramic & Porcelain Tile | |

| Natural Stone | ||

| Hardwood | ||

| Engineered Wood | ||

| Laminate | ||

| By Construction Type | New Construction | |

| Renovation & Replacement | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Home Centers |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors/Dealers | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the United Kingdom floor covering market?

The United Kingdom floor covering market size was USD 4.46 billion in 2025 and is projected to reach USD 5.55 billion by 2031 at a 3.76% CAGR through 2031.

Which product categories are leading the growth in the United Kingdom floor covering market?

Resilient formats, especially LVT, drive growth due to hygiene, acoustic, and maintenance benefits, while non-resilient formats remain the largest by share, led by ceramic, porcelain, and engineered wood.

How are retrofit programs affecting demand in the United Kingdom floor covering market?

Net-zero and warmth-focused retrofit programs are prompting flooring upgrades that align with thermal performance and low embodied carbon goals under the Future Homes Standard 2025.

Which end-user segments are most important in 2026?

Residential remains the largest segment and is set to grow at a 4.4% CAGR, while healthcare, education, and office refurbishments sustain steady commercial demand.

What role do EPDs and embodied carbon play in procurement?

EPDs and low embodied carbon disclosures are now common bid requirements, advantaging manufacturers with verified data and take-back programs across public and institutional projects.

Page last updated on: