Kuwait Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

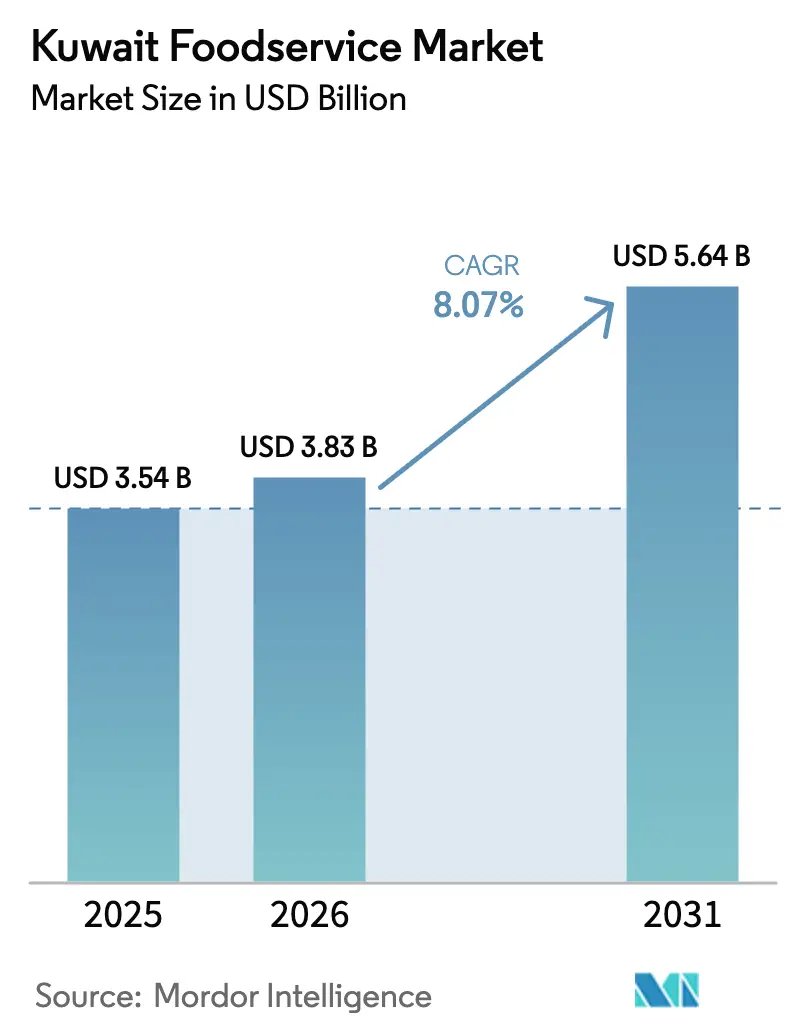

| Base Year Market Size (2025) | USD 3.54 Billion |

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

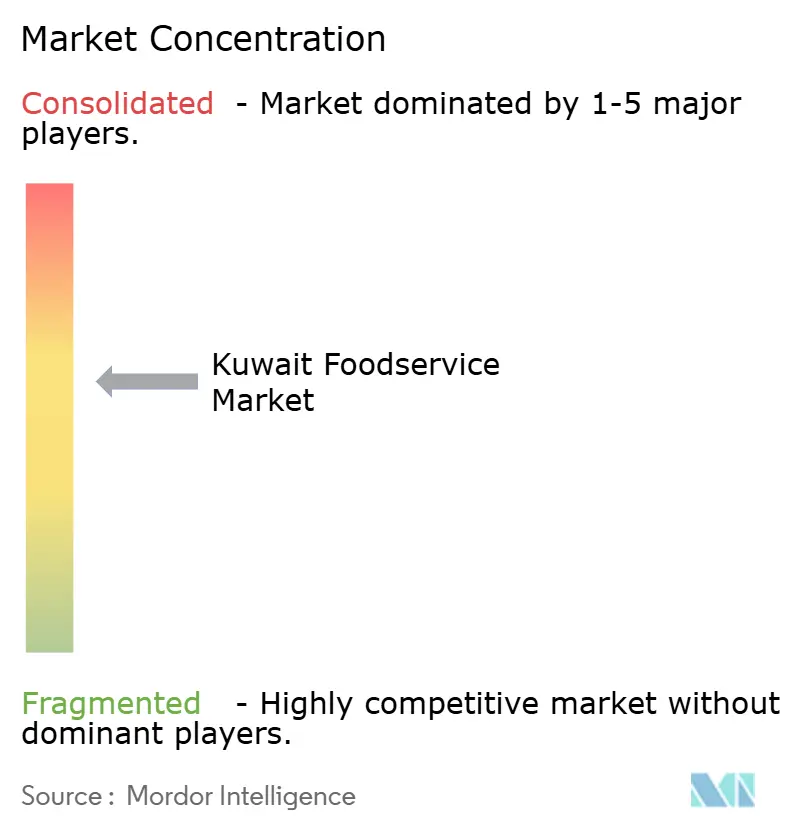

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Foodservice Market Analysis by Mordor Intelligence

The Kuwait foodservice market size is expected to increase from USD 3.54 billion in 2025 to USD 3.83 billion in 2026 and reach USD 5.65 billion by 2031, growing at a CAGR of 8.07% over 2026-2031. In Kuwait, affluent residents and a 70% expatriate base are driving a surge in dining demand, outpacing population growth. While quick-service restaurants lead the charge, the market is increasingly gravitating towards delivery formats. This shift is largely due to high real-estate costs, prompting operators to embrace asset-light kitchens and self-service technology. Major government initiatives, like Kuwait Entertainment City and 360 Kuwait, are positioning dining as a central attraction, extending visitor stays and boosting food-and-beverage spending. Digital ordering, already commanding a 73.9% penetration, is further amplified by loyalty programs and influencer marketing, seamlessly turning social interactions into sales. Additionally, the growing preference for convenience and time-saving options is further accelerating the adoption of delivery-led dining formats.

Key Report Takeaways

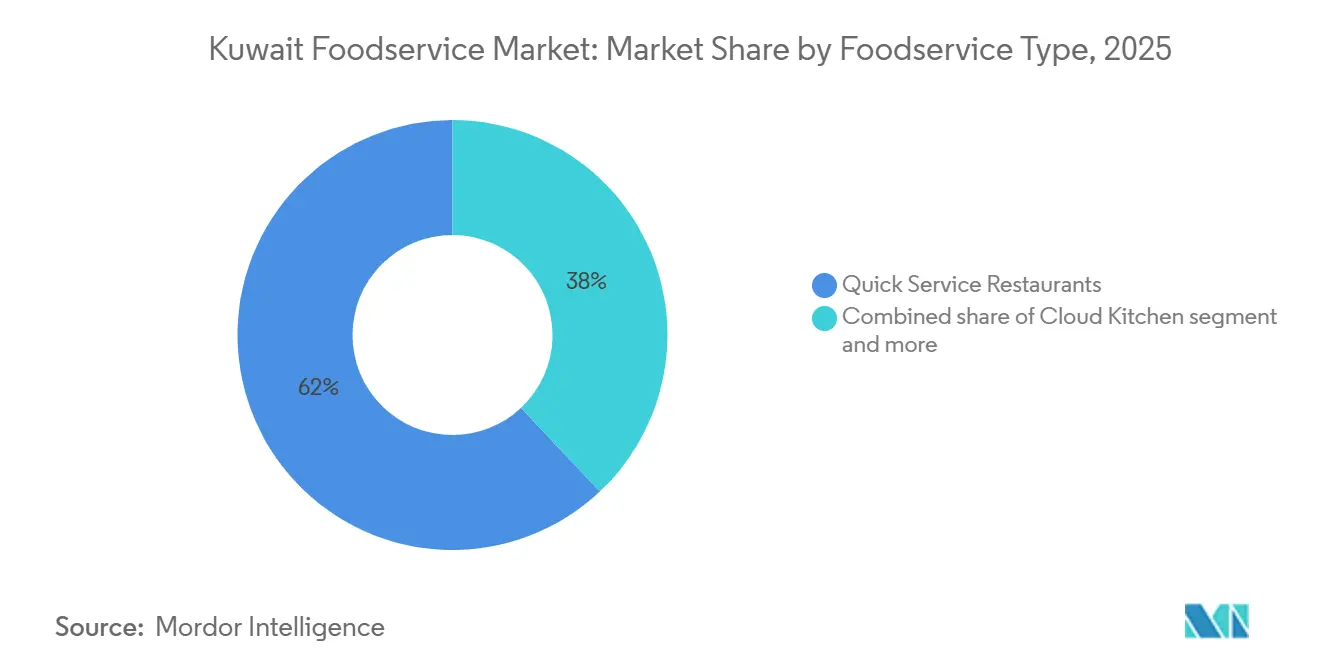

- By foodservice type, quick-service restaurants held 62.02% of the Kuwait foodservice market share in 2025, while cloud kitchens are projected to expand at an 8.74% CAGR through 2031.

- By outlet format, independents accounted for 70.35% of the Kuwait foodservice market size in 2025, whereas chained operators are forecast to grow at a 10.05% CAGR over 2026-2031.

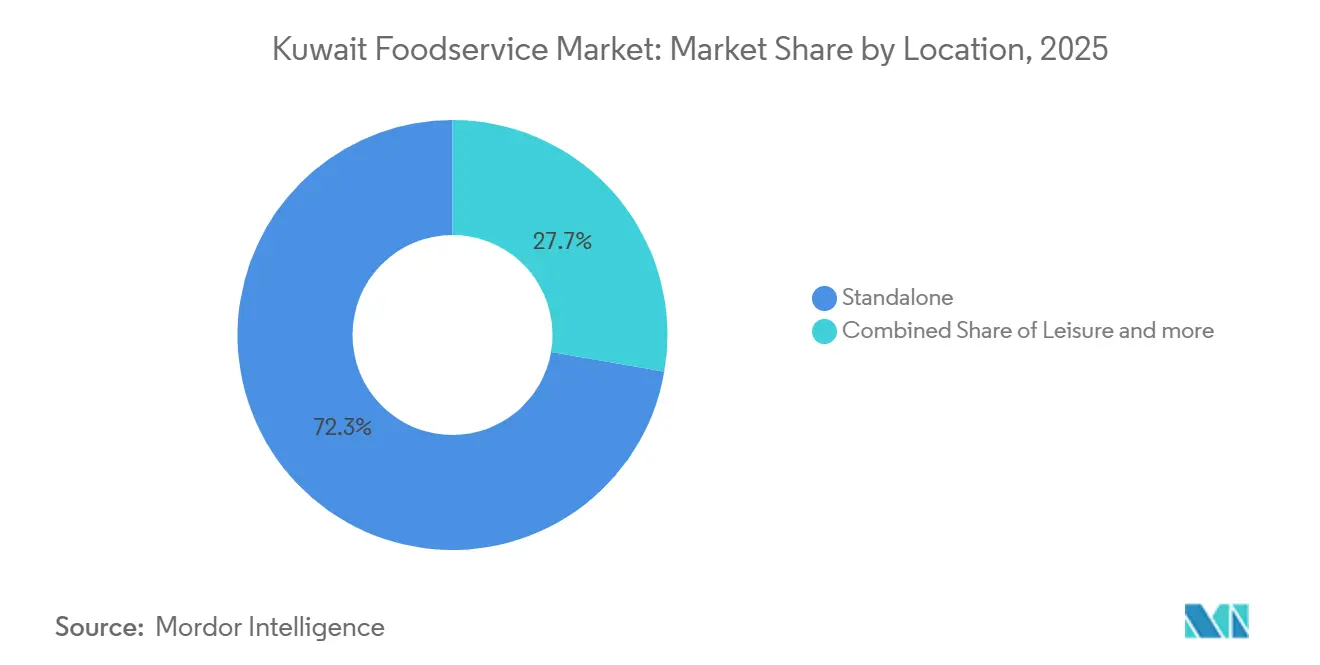

- By location, standalone outlets captured 72.28% of 2025 sales; leisure-based venues located in malls and theme parks are on track for a 10.41% CAGR to 2031.

- By service, dine-in transactions accounted for 51.10% of activity in 2025, while delivery orders are increasing at an 11.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of cloud kitchens | +1.5% | National, concentrated in Kuwait City, Salmiya, Hawalli | Medium term (2-4 years) |

| Diversification of cuisine and dining experiences | + 0.8% | National, with premium segments in Kuwait City, Avenues Mall, 360 Mall | Long term (≥ 4 years) |

| Expatriate-driven demand diversity | + 1.2% | National, particularly Farwaniya, Hawalli governorates with high expat density | Long term (≥ 4 years) |

| Expansion of leisure and entertainment venues | + 1.0% | National, early gains in Kuwait City, Sabah Al-Ahmad, Jaber Al-Ahmad | Medium term (2-4 years) |

| Government food-security initiatives shaping menus | + 0.6% | National, with pilot programs in Kuwait City | Long term (≥ 4 years) |

| Social-media and influencer amplification | + 1.1% | National, strongest in urban centers with 99.7% internet penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of cloud kitchens

Operators are sidestepping Kuwait's hefty monthly rents of USD 50 per square meter by decoupling production from retail spaces, a move that alleviates pressure on dine-in formats. In 2025, Kout Food Group showcased the power of technology by cutting delivery times by 20% through an AI-driven driver dispatch system, effectively tackling last-mile challenges. Talabat, harnessing its expansive network of 4,500 restaurants and a monthly user base of 600,000, is adeptly upselling prepared meals alongside grocery essentials, seamlessly merging the realms of foodservice and quick commerce. Thanks to Kuwait Municipality’s Smart License Project, permit cycles have been slashed from 45 to 30 days, easing the entry for experimental virtual brands. Leading the charge, Americana Restaurants and other major chains are rolling out self-service kiosks, capturing valuable first-party data that can be leveraged in ghost-kitchen operations. These advancements highlight the growing role of technology and innovation in reshaping Kuwait's foodservice market.

Expatriate-driven demand diversity

In Kuwait's foodservice market, no single cuisine holds sway, thanks to the significant presence of expatriate communities, notably Indians and Egyptians. By late 2024, expatriates made up about 68.6% of Kuwait's population, totaling approximately 3.3 million, according to Gulf Labour Markets, Migration and Population (GLMM) reports[1]Source: Gulf Labour Markets, Migration and Population (GLMM), "Kuwait: Population by nationality (Kuwaiti/ non-Kuwaiti) ", gulfmigration.grc.net. In 2024, Alshaya launched Chipotle in Kuwait, and within just 18 months, expanded it to three branches, underscoring the local appetite for Western fast-casual dining. To entice South Asian diners, operators are infusing global menus with vegetarian options and rich spices, knowing that authenticity brings them repeat patrons. Chefs, earning well above the 75 KWD minimum wage, are driving a trend towards specialization and the rise of multi-brand kitchens that optimize shared back-of-house labor. This blend of diverse tastes and high disposable incomes ensures a steady demand, even in the face of fluctuating fuel prices.

Expansion of leisure and entertainment venues

Set to debut in 2026, the USD 654 million Kuwait Entertainment City aims to attract 900,000 annual visitors, with dining as a central entertainment focus. 360 Kuwait is introducing 21 artisanal concepts alongside a Grand Hyatt and an arena, showcasing a mixed-use model designed to prolong guest stays. Al Kout Mall, boasting 360 outlets, allocates significant space to foodservice, recognizing that dining drives retail traffic. Coastal resorts, like the 330-room Hilton slated for a 2026 opening, are layering in lodging demand, enhancing evening transactions. Leisure destinations are also commanding premium rents, as their patrons willingly pay a premium for the added convenience. These developments highlight Kuwait's strategic focus on integrating entertainment, retail, and hospitality to boost economic growth.

Social-media and influencer amplification

In Kuwait, where internet penetration stands at 99.7% and Instagram boasts 3.5 million users, consumers are turning to online platforms to discover restaurants. Influencers like @q8foodies wield significant power, filling reservation books within hours and underscoring the digital buzz's role as a primary sales driver. Shake Shack experienced a staggering 600% surge in social media mentions, thanks to a limited-time flavor promotion amplified by influencers. This highlights how scarcity tactics can effectively drive in-store traffic. Meanwhile, delivery apps are capitalizing on their vast followings; for instance, Talabat, with its 1.1 million Instagram fans, is launching campaigns that cleverly avoid the costs of paid media. Additionally, restaurant chains are broadening their loyalty programs, not just to gather first-party data but also to retarget high-value customers, thereby reducing their reliance on high-commission aggregators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs (rent, labour, utilities) | -0.9% | National, most acute in Kuwait City, Salmiya, premium mall locations | Short term (≤ 2 years) |

| Stringent food-safety and import regulations | -0.5% | National, affecting all operators with imported ingredients | Medium term (2-4 years) |

| Infrastructure and urban-planning constraints | -0.4% | National, concentrated in older commercial districts | Long term (≥ 4 years) |

| Limited domestic agricultural production | -0.3% | National, affecting all operators dependent on fresh produce | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High operating costs

In Kuwait, average commercial rents of USD 50 per square meter are squeezing dine-in margins, pushing the foodservice market towards delivery-centric models. Mandatory benefits, adding roughly 12% to base wages, combined with salaries for senior kitchen staff that significantly surpass statutory minimums, are driving up fixed costs. With energy subsidies under scrutiny from the IMF, there's a looming threat of utility hikes, potentially inflating cooking and refrigeration expenses[2]Source: International Monetary Fund, "Fossil Fuel Subsidies," imf.org . Food inflation, recorded at 5.63% year-over-year in 2025, forced operators to grapple with either margin erosion or menu price hikes sensitive to consumer reactions. The 2026 decision to revoke 1,100 food-truck licenses not only eliminated low-overhead competitors but also dismantled a cost-effective entry point for budding entrepreneurs. These challenges are reshaping the competitive landscape of the Kuwait foodservice market.

Stringent food-safety and import regulations

Small import-reliant restaurants face increased documentation costs due to halal certification, Arabic labeling, and shelf-life limits[3]Source: United States Department of Agriculture, " Food and Agricultural Import Regulations and Standards Country Report," apps.fas.usda.gov . The Kuwait Conformity Assurance Scheme can delay laboratory tests by up to four weeks, tying up working capital and risking spoilage for perishables. Import licenses mandate local partners, posing challenges for foreign brands seeking direct control. While most premium inputs incur a 5% customs duty, staples enter duty-free, leading to uneven cost bases that influence menu pricing. Regulators' intervention on delivery-fee caps for February 2026 deliveries adds to the uncertainty for both platforms and restaurants. These challenges collectively impact the operational efficiency and profitability of businesses in the foodservice market. Additionally, navigating these regulatory and cost-related hurdles requires strategic planning and adaptability from market participants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Legacy Formats

In 2025, quick-service restaurants (QSRs) led Kuwait's foodservice market, securing a commanding 62.02% share. Established chains, such as Americana Restaurants, are capitalizing on economies of scale, deploying self-ordering kiosks across numerous outlets to boost both throughput and customer satisfaction. While labor pressures see chefs de cuisine earning about 175 KWD monthly, the demand for authentic menus among expatriates allows for a premium pricing strategy. These dynamics firmly establish QSRs as the volume leaders, ensuring profitability even in a competitive landscape. Additionally, technology platforms like Yum! Brands’ Byte, which is already operational in 25,000 stores worldwide, are enhancing margins through increased productivity. The continued investment in technology and operational efficiency is expected to further strengthen QSRs' dominance in the forecast period.

Cloud kitchens are emerging as the fastest-growing segment, boasting an impressive 8.74% CAGR. They are taking advantage of reduced rental costs and the ability to manage multiple virtual brands from a single site. This flexibility allows for swift menu adjustments in response to changing consumer tastes without significant capital investment. With urban delivery demands on the rise, cloud kitchens are strategically positioned in high-traffic areas, reducing overheads while increasing order volume. Their nimbleness enables them to capture market share from traditional outlets, especially as digital ordering becomes more prevalent. The growing preference for convenience and on-demand food delivery is expected to further accelerate the adoption of cloud kitchens in Kuwait.

By Outlet: Chained Operators Gain Ground Through Franchising

In 2025, independent operators, with their vibrant culinary entrepreneurship and localized appeal, dominated the Kuwait foodservice market, seizing 70.35% of the total revenue. Their strength lies in authentic, niche offerings that resonate with diverse expatriate communities, fostering loyalty in neighborhood settings. Yet, they grapple with increasing pressures from regulatory crackdowns on formats like food trucks, a challenge that hits smaller players without deep capital reserves. While independents boast broad market coverage, they find it challenging to achieve the scale efficiencies of their larger counterparts. This established position highlights their significance as the revenue backbone, even as trends of gradual consolidation loom. Despite these challenges, independent operators continue to innovate by introducing unique dining concepts to retain their competitive edge.

Chained outlets, on the other hand, are the market's rising stars, with projections of a 10.05% CAGR. This growth is largely driven by franchisors tapping into Kuwait's robust disposable incomes and its streamlined licensing processes. Portfolio groups such as M.H. Alshaya and Kout Food Group are at the forefront, leveraging centralized procurement and logistics for cost efficiencies that outpace standalone independents. As chains expand, the combined share of the top five players inches into the upper-moderate range, further fueling industry consolidation. With standardized operations and brand scalability, chains are strategically positioned to harness this growing demand, signaling a significant shift in the competitive landscape of Kuwait's foodservice sector. Additionally, their ability to adapt global trends to local preferences further strengthens their market position.

By Location: Leisure Venues Reshape Dining Geography

In 2025, standalone stores led Kuwait's foodservice scene, making up 72.28% of all outlets. Their deep roots in local neighborhoods and ability to adapt have fostered strong community loyalty. With lower overheads than pricier locales, these stores have become go-to spots for daily dining. Yet, they're now contending with a surge in experiential retail, which is luring in a more affluent crowd. While the sheer number of standalone outlets gives them a grip on the market, their growth is trailing behind these newer, busier venues. Still, this dynamic solidifies standalone stores as a cornerstone in the shifting landscape of consumer dining preferences. Their ability to cater to diverse consumer needs ensures their continued relevance despite emerging competition.

Dining outlets in malls and entertainment hubs are the rising stars, projected to grow at a robust 10.41% CAGR. Developers are increasingly anchoring these spaces with dining options to enhance the overall experience. In burgeoning areas like Sabah Al-Ahmad, pioneering chains are swiftly claiming prime spots, reaping benefits ahead of population booms. While landlords at hotspots like The Avenues and Al Kout Mall command top dollar in rents, they ensure a steady stream of foot traffic, catering predominantly to high-margin brands. Meanwhile, resorts and airports carve out a niche, capitalizing on the premium sales from business travelers seeking convenience. This trend underscores the growing allure of leisure dining in Kuwait's evolving foodservice landscape. The integration of dining with entertainment and retail further strengthens its appeal to a broader consumer base.

By Service Type: Delivery Surges on Digital Infrastructure

In 2025, dine-in transactions dominated the Kuwait foodservice market, accounting for 51.10% of the share. This stronghold is bolstered by Kuwait's vibrant social culture and its alcohol-free policies, both of which champion out-of-home gatherings and communal dining. The allure of the dine-in segment lies in its experiential nature; consumers often prioritize ambiance and social interaction especially during family meals and celebrations over mere convenience. To further cement this dominance, chains are optimizing seating layouts and introducing loyalty programs, encouraging repeat in-person visits. Even with the rise of digital ordering, the cultural significance of dine-in experiences resonates deeply with both expatriates and locals alike. This enduring preference for physical venues underscores dine-in's resilience, even as ordering habits evolve.

Meanwhile, the delivery segment is on a rapid ascent, boasting an impressive 11.25% CAGR. This surge is largely attributed to Kuwait's staggering average spend of USD 498 per user outpacing U.S. averages by more than double indicating both high order values and frequent usage. Prominent platforms such as Talabat, Deliveroo, and Cravez have seamlessly integrated into daily life, influencing menu designs and pricing strategies, all while adeptly navigating emerging fee caps. In response to platform commissions, chains are rolling out omnichannel loyalty programs, harnessing customer data to cultivate direct relationships. This strategic maneuvering positions delivery as a formidable contender, poised to challenge dine-in's supremacy, especially as urban consumers lean towards convenience and premium at-home dining. The trajectory of delivery underscores a significant platform-driven evolution in Kuwait's foodservice landscape.

Geography Analysis

Urban density, established retail corridors, and a wealthy clientele drive the concentration of foodservice outlets in Kuwait City, Salmiya, and Hawalli governorates. Meanwhile, the largest expatriate communities in Farwaniya and Hawalli fuel a demand for Indian, Egyptian, and Filipino cuisines, which are now being embraced by both multinational chains and nimble independent operators, often merging them into diverse portfolios. These trends highlight the growing cultural diversity within the Kuwait foodservice market, creating opportunities for innovative culinary concepts.

In Sabah Al-Ahmad and Jaber Al-Ahmad, government-backed infrastructure projects are birthing new commercial spaces. These early-stage ventures benefit from reduced rents, positioning them to expand in tandem with the evolving community. This development underscores the importance of strategic location selection for businesses aiming to capitalize on emerging urban hubs. Mixed-use developments, such as the USD 654 million Kuwait Entertainment City and 360 Kuwait, showcase the synergy between leisure design and the foodservice sector, optimizing real estate returns and capturing consumer spending. A surge in coastal visitors boosts demand for upscale seafront dining, and new airport concessions offer operators a chance to tap into transit passengers eager for global brands.

While the Smart License Project streamlines regulations and shortens launch times, older neighborhoods contend with zoning restrictions that limit density, inadvertently benefiting established players with pre-existing sites. With food trucks set to exit post-2026, there's an emerging opportunity for delivery-only kitchens to establish a foothold in suburbs where traditional retail spaces are limited. This shift could redefine the operational models of foodservice providers, emphasizing adaptability and innovation.

Competitive Landscape

The Kuwait foodservice market showcases a balanced landscape, where leading franchisees dominate global brands, while independent operators thrive with neighborhood and heritage concepts. In 2024, Americana Restaurants achieved sales of USD 305.95 million from 246 outlets in Kuwait. However, the company strategically redirected its capital towards faster-growing peers in the GCC, signaling a shift in focus within the Kuwaiti foodservice scene. Players like M.H. Alshaya, Kout Food Group, and Alghanim Industries, with their diverse multibrand portfolios, harness procurement advantages and swiftly adapt to changing market formats. This dynamic highlights the competitive interplay between established players and emerging trends in the market.

Digital prowess is becoming the key differentiator in the market. Kout Food Group leverages AI, Americana champions a cross-brand loyalty platform, and Yum! Brands introduces its Byte system. Together, these innovations underscore the role of data analytics and automation in reducing labor demands and boosting customer retention. Meanwhile, delivery aggregators are carving out a pivotal role in the Kuwaiti foodservice landscape by harnessing consumer data. However, with government-imposed fee caps, there's a hint of potential shifts in profit-sharing dynamics. The increasing reliance on digital tools is reshaping consumer engagement and operational efficiency across the sector.

Emerging trends point to opportunities in health-focused dining, suburban delivery centers (especially after the food-truck trend), and plant-based menus, all resonating with the growing awareness of lifestyle diseases. While stringent regulations on halal certifications and Arabic labeling act as protective barriers for established players, they simultaneously pose challenges for global entrants eyeing the market. These factors collectively shape the competitive environment, influencing both market entry strategies and long-term growth prospects.

Kuwait Foodservice Industry Leaders

-

Americana Restaurants

-

M.H. Alshaya Co.

-

Kout Food Group

-

Alghanim Industries

-

Yum! Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Keeta, the global arm of China's food delivery giant Meituan, has officially launched in Kuwait. This entry marks Meituan's bold stride into the bustling food delivery scene of the Middle East. With an eye on the local market, Keeta plans to harness its parent company's deep-rooted technological prowess in logistics and platform oversight.

- July 2025: Exotica Café, a fresh entrant in the culinary scene, has made its debut at the Salmiya Terrace Mall in Kuwait. Brought to life by the renowned regional brand Mughal Mahal, Exotica Café serves a unique fusion of modern Indian dishes and time-honored flavors. The establishment seeks to redefine the dining experience, offering patrons a blend of sophistication and casualness, setting it apart from typical Indian eateries.

- March 2025: In March 2025, Maimoon Caterers unveiled its inaugural cloud kitchen in Salmiya, Kuwait, focusing on Dawoodi Bohra cuisine. With ambitions to deliver not just in Salmiya but also in surrounding regions, this launch stands out as Kuwait's pioneering legalized cloud kitchen dedicated to this culinary tradition.

- February 2025: Pista House, a renowned Hyderabadi restaurant, has made its debut in Kuwait. Nestled on the ground floor of the Kuwait Continental Hotel, Pista House Kuwait is dedicated to serving an authentic taste of Hyderabad, all within a cozy ambiance perfect for family dining.

Kuwait Foodservice Market Report Scope

Cafes and Bars, Cloud Kitchen, Full Service Restaurants, and Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets and Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

| Cafes and Bars | By Cuisine | Cafes |

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| Foodservice Type | Cafes and Bars | By Cuisine | Cafes |

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| Outlet | Chained Outlets | ||

| Independent Outlets | |||

| Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms