Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

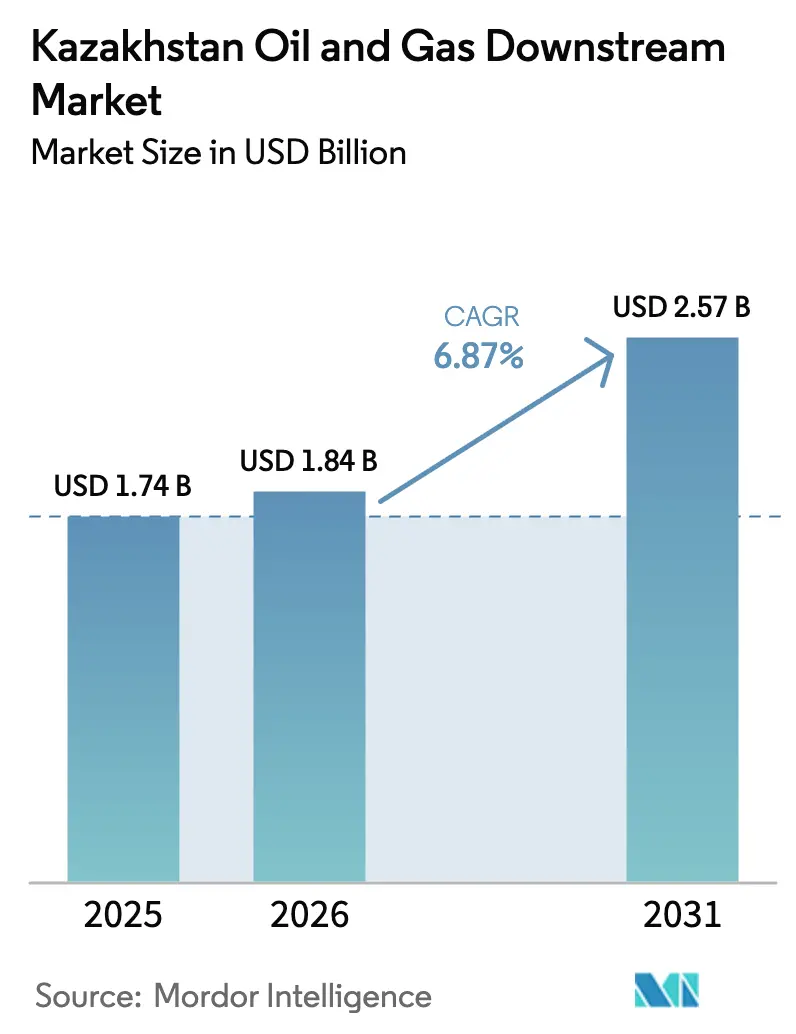

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 6.87% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan Oil And Gas Downstream Market Analysis by Mordor Intelligence

The Kazakhstan Oil And Gas Downstream Market size was valued at USD 1.74 billion in 2025 and is estimated to grow from USD 1.84 billion in 2026 to reach USD 2.57 billion by 2031, at a CAGR of 6.87% during the forecast period (2026-2031).

Capacity additions at Shymkent, Pavlodar, and Atyrau, the USD 7.4 billion Silleno polyethylene complex, and greater reliance on the Kazakhstan-China Pipeline fuel this growth even as CPC disruptions persist. Strong Euro-5 diesel and gasoline uptake, retail network build-outs in underserved oblasts, and an export pivot to China underpin revenue momentum. Rising petrochemical integration improves margin resilience against narrowing crack spreads, while mounting water stress and process-safety talent shortages restrain operating efficiency. Ongoing privatization of 50% stakes in Atyrau and Pavlodar should attract foreign technology partners, diluting state ownership but strengthening governance and energy-efficiency benchmarks.

Key Report Takeaways

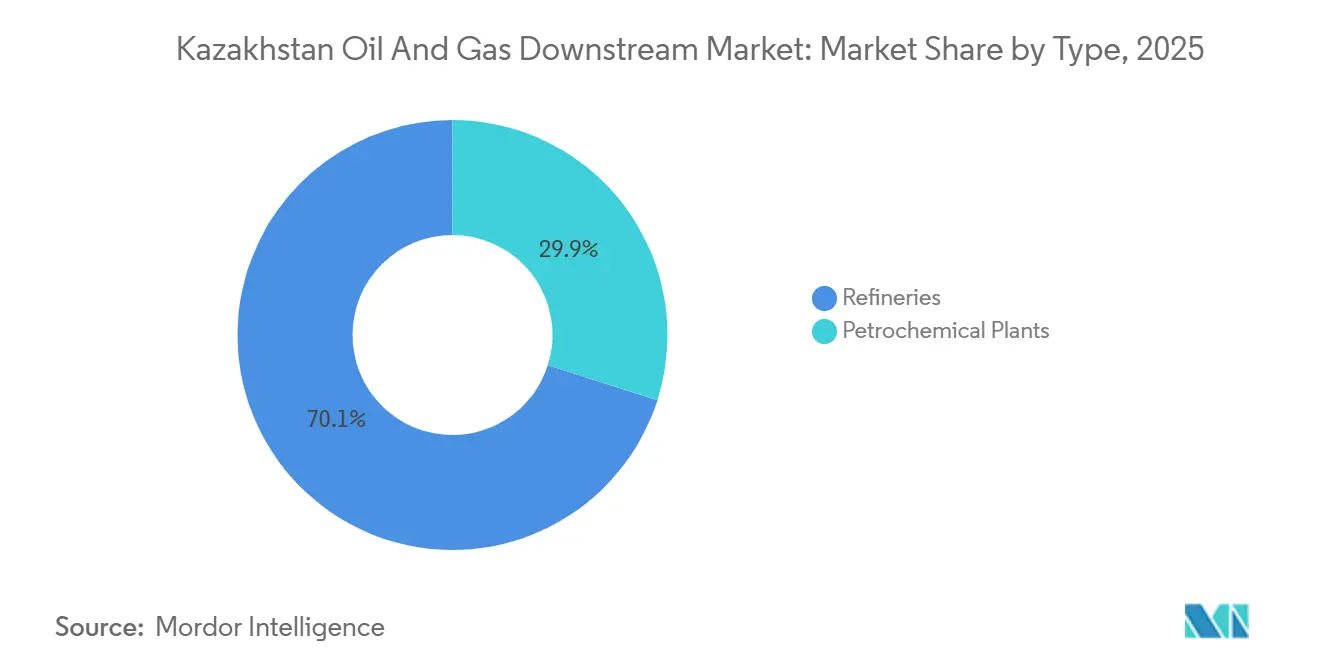

- By type, refineries accounted for 70.1% of the Kazakhstan downstream market share in 2025. Petrochemical plants are forecast to deliver the fastest growth, advancing at an 8.9% CAGR to 2031.

- By product type, refined petroleum products secured a dominant 67.5% share of the revenue in 2025, while petrochemicals are set to grow at an impressive 8.7% CAGR, extending through 2031.

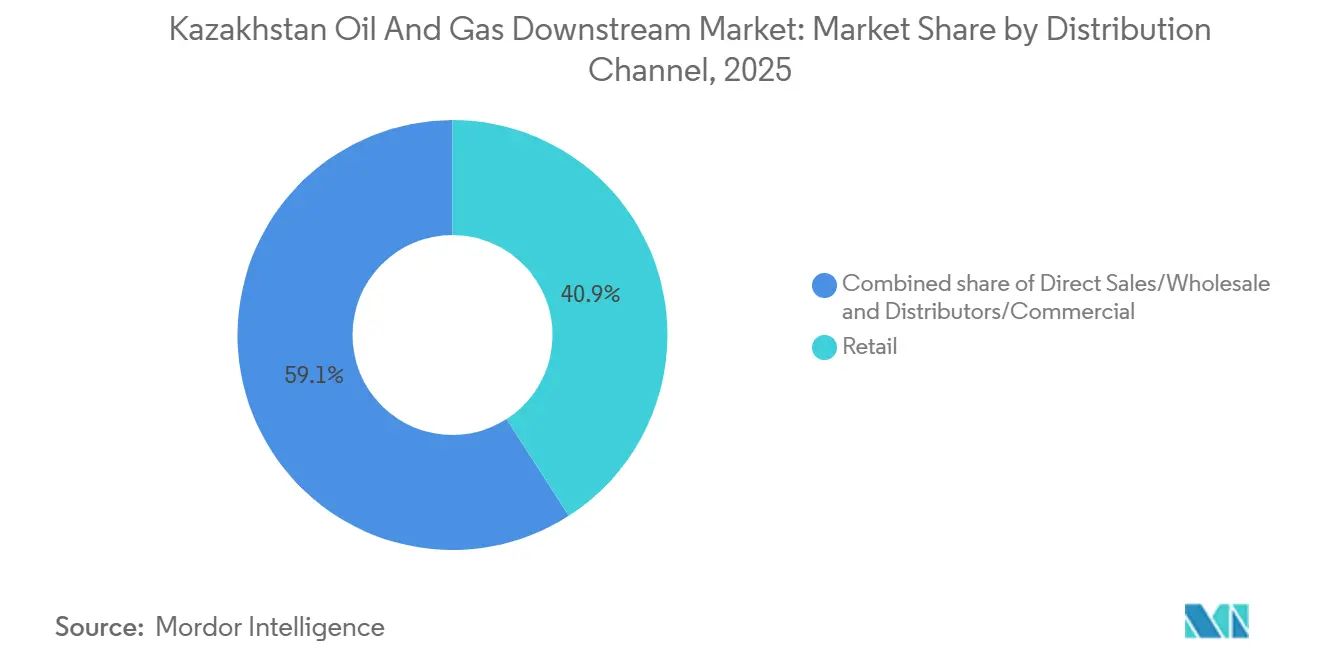

- By distribution channel, retail distribution channels captured 40.9% revenue share in 2025 and are projected to expand at a 7.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kazakhstan Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led refinery modernization | +1.8% | National, with primary gains in Shymkent, Pavlodar, Atyrau | Medium term (2-4 years) |

| Euro-5 fuel demand surge | +1.2% | National, spillover to Central Asia export markets | Short term (≤ 2 years) |

| Strategic export corridor to China & Central Asia | +1.5% | Western Kazakhstan (Atyrau), cross-border nodes to China | Long term (≥ 4 years) |

| Petrochemical complex build-out | +2.1% | Atyrau region, with distribution hubs in Almaty | Long term (≥ 4 years) |

| Blockchain fuel-quality pilot | +0.3% | Pilot phase in Almaty and Astana | Long term (≥ 4 years) |

| Bio-jet fuel (camelina feedstock) push | +0.4% | National, with early trials at Almaty International Airport | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led Refinery Modernization

Capacity upgrades at Shymkent, Pavlodar, and Atyrau collectively add 8.7 million t/y by 2028, ending diesel imports and enabling exports to Uzbekistan and Kyrgyzstan.[1]KazMunayGas, “Shymkent Expansion Press Release,” kmg.kz Shymkent’s expansion doubles throughput to 12 million t/y, lifts middle-distillate yields from 52% to 68%, and integrates delayed coking and hydrocracking units suited to regional trucking demand. Pavlodar’s 2027 upgrade boosts nameplate capacity to 8 million t/y and installs a catalytic reformer that achieves Euro-5 octane levels without imported additives. The March 2025 privatization tender seeks partners able to cut energy intensity 15% via heat integration and flare-gas recovery, consistent with the 2060 carbon-neutrality roadmap. This modernization contrasts with Turkmenistan’s Soviet-era refineries that run below 60% utilization due to sanctions and underinvestment.

Euro-5 Fuel Demand Surge

Nationwide Euro-5 mandates taking effect in January 2025 compelled hydrotreating investments that reduce sulfur from 500 ppm to 10 ppm. Atyrau restarted in October 2024 with a 1.2 million t/y hydrotreater supplying Euro-5 diesel to Aktobe and Mangystau. Russian Euro-5 imports, once 18% of consumption in 2024, vanished by mid-2025, unlocking arbitrage to Kyrgyzstan, where Euro-4 standards persist. Retailers realize a 12% price premium for Euro-5, spurring station upgrades and accelerating inventory turnover. Compliance also positions Kazakhstan to regain European buyers once CPC reliability improves, as EU refiners avoid high-sulfur grades under Fuel Quality Directive rules.

Strategic Export Corridor to China & Central Asia

CPC disruptions after September 2024 drone strikes redirected up to 8 million t/y of crude into the 20 million t/y Kazakhstan-China Pipeline, now running near capacity. Tengizchevroil’s Future Growth Project, online January 2025, adds 12 million t/y that flows exclusively east to Sinopec and PetroChina, raising China’s share of Kazakh exports to 62% in 2025. A November 2024 barter deal with MOL Group covering 85,000 t of CPC crude shows hedging moves to maintain European access amid geopolitical risk. Uzbekistan and Kyrgyzstan signed 2025 MOUs seeking 1.5 million t/y of diesel and jet fuel via rail and road, reinforcing regional market diversification.

Blockchain Fuel-Quality Pilot

The Ministry of Energy’s 2025 blockchain pilot logs refinery test results to an immutable ledger, cutting Euro-5 adulteration at 120 retail sites by 23% during trials.[2]World Bank, “Kazakhstan Water Stress Diagnostics,” worldbank.org National rollout slated for 2027 compels refiners and import terminals to integrate real-time SCADA data on viscosity and sulfur into batch IDs, creating a transparent chain of custody. Reduced tax evasion could lift annual excise revenue by USD 180 million, improving fiscal stability for downstream infrastructure upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Megaproject financing delays | -0.9% | National, concentrated in Atyrau and Mangystau regions | Medium term (2-4 years) |

| CPC pipeline disruptions | -1.1% | Western Kazakhstan, affecting Tengiz and Kashagan fields | Short term (≤ 2 years) |

| Process-safety talent shortage | -0.5% | National, acute at Atyrau, Pavlodar, Shymkent refineries | Long term (≥ 4 years) |

| Water stress at refinery hubs | -0.6% | Atyrau and Pavlodar regions along Ural and Irtysh rivers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Megaproject Financing Delays

KazMunayGas carried USD 14.7 billion in gross debt and a 2.8x debt/EBITDA ratio at end-2024, limiting equity for new builds and favoring brownfield upgrades with quicker payback. Silleno’s USD 5.2 billion debt package required Sinopec and SIBUR equity that reduced KazMunayGas’s stake to 40%, capping upside. Moody’s affirmed a Baa1 rating in January 2025, citing dividend extractions and price volatility, restricting cheap capital access. Local banks impose >150% collateral and 7-year tenors on smaller firms, delaying PTA and MEG units that would integrate the polyester chain.

CPC Pipeline Disruptions

September 2024 drone strikes halted CPC single-point moorings, forcing 8 million t/y to China and adding USD 12/bbl logistics costs, eroding producer netbacks and stalling expansion plans. War-risk insurance caps of USD 500 million have shareholders studying a USD 4 billion trans-Caspian route via Kuryk and Baku with a 5-year lead time. Substituting heavier Kumkol crude for premium Kashagan barrels at Atyrau and Pavlodar trims diesel yields by 3 percentage points, squeezing refinery gross margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refineries Anchor Capacity, Petrochemicals Drive Margin Shift

Refineries held 70.1% of the Kazakhstan downstream market share in 2025, anchored by 17 million t/y of combined capacity at Atyrau, Pavlodar, and Shymkent. Petrochemical plants, however, will outpace refineries, with an 8.9% CAGR through 2031 as the USD 3 billion Gas Separation Unit diverts 9 bcm/y of ethane-rich gas into polymer feedstock, slashing polyethylene cash costs to USD 620/t, 16% below European averages.[3]Tengizchevroil, “Gas Separation Unit Fact Sheet,” tengizchevroil.com Bitumen specialist CaspiBitum provides portfolio resilience by serving the USD 8 billion Nurly Zhol road program.[4]CaspiBitum, “Bitumen Capacity Statement,” caspibitum.kz

Petrochemical earnings grow faster than refinery profits, as Euro-5 hydrotreaters add USD 22/t in operating cost and retail caps crimp pass-through. The Kazakhstan downstream market size attributable to petrochemicals is therefore set to close the gap on fuels, even though refineries continue to dominate overall throughput. As imported Russian diesel faces tariffs from 2025 onward, refinery utilization will stay high, yet investment focus will tilt toward integrated cracker capacity where higher margins outweigh scale disadvantages versus GCC giants.

By Product Type: Petrochemicals Gain Share as Fuel Margins Compress

Refined fuels made up 67.5% of 2025 output, with diesel at 42% and gasoline at 31%. Jet fuel reached 1.8 million t in 2025; Shymkent supplied 60% and exported overland to Kyrgyzstan and Tajikistan. Lubricants expanded 9.2%, led by LUKOIL’s 100,000 t/y Almaty plant producing 800 SKUs. Petrochemicals, boosted by Silleno HDPE/LLDPE volumes and KPI polypropylene, will climb at an 8.7% CAGR, trimming fuels’ share below 60% by 2031. The Kazakhstan downstream market size for polymer products thus grows steadily on the back of low-cost associated-gas feedstock, underpinned by a 16-year dry-gas contract that shields producers from price shocks.

Higher Euro-5 compliance costs squeeze refining EBITDA margins from 11% in 2023 to 8% in 2025, while polyethylene margins remain structurally stronger on the USD 180/t feedstock advantage over European crackers. This profitability gap encourages KazMunayGas to channel capital toward chemicals, mirroring Saudi Aramco’s fuels-plus-chemicals co-location model.

By Distribution Channel: Retail Networks Expand into Underserved Corridors

Retail captured 40.9% of 2025 revenue as branded chains extended footprints along Almaty-Khorgos and Shymkent-Tashkent corridors in response to 18% annual growth in cross-border truck traffic. Helios plans 85 new sites by 2027, leveraging Euro-5 quality perception to price 12% above unbranded stations. Direct industrial sales comprised 35.2%, indexed to Urals plus USD 8/bbl, exposing margins to crude volatility. Distributors held 23.9%, servicing specialty lubes but battling counterfeit inflows via informal Russia-China trade routes.

The Kazakhstan downstream market benefits from 2025 rules mandating vapor recovery and e-payments, which forced under-capitalized independents out and shifted share to well-financed chains. Retail, therefore, enjoys a 7.5% CAGR forecast through 2031 versus mid-single-digit growth for wholesale channels. Blockchain certification should further strengthen branded retailers by raising compliance hurdles for gray-market operators.

Geography Analysis

Domestic demand absorbed 78% of refined products in 2025, driven by agriculture and trucking, with exports expected to rise to 30% by 2031 as petrochemical output scales. Atyrau generates 48% of the downstream value added, benefiting from Tengiz feedstock but constrained by water scarcity and engineering talent gaps. Pavlodar’s refinery leverages Omsk-Pavlodar crude inflows and supplies industrial Karaganda, yet Irtysh River stress and Chinese upstream diversions pose long-term risks. Shymkent sits near Uzbek and Kyrgyz borders and will export 2.5 million t/y of diesel and jet fuel once its 12 million t/y expansion is completed in 2028.

China’s share of Kazakh crude exports rose from 38% in 2023 to 62% in 2025 as the CPC route faltered. Silleno plans to ship 80% of 1.25 million t/y polyethylene through the 48-hour Khorgos dry-port corridor, beating Middle Eastern rivals on lead time. Central Asia, importing 1.2 million t of refined fuels in 2025, will nearly double volumes by 2030 under Belt-and-Road-driven road upgrades. Europe took only 1.8 million t of Kazakh crude in 2025 but remains a strategic hedge via MOL’s November 2024 trading pact.

Almaty lacks refining assets yet dominates lubricant logistics, dispatching LUKOIL’s 800 SKUs across the region. Mangystau contributes 12% of downstream output through CaspiBitum’s pavement-grade refinery, servicing the Nurly Zhol road initiative but lacking pipeline links to consumption hubs. Feasibility studies for a USD 4 billion trans-Caspian line to Baku aim to diversify export routes and reduce Russian dependence, though completion lies beyond 2030.

Competitive Landscape

The Kazakhstan downstream market is moderately concentrated: KazMunayGas controls 68% of refining while Tengizchevroil dominates upstream feedstock. Joint-venture models like the USD 7.4 billion Silleno plant pool KazMunayGas 40%, Sinopec 30%, and SIBUR 30% stakes, sharing risk and technology. A 16-year dry-gas agreement between Tengizchevroil and KazMunayGas PetroChem locks in 9 bcm/y at preferential rates, creating a feedstock moat versus stand-alone refiners. LUKOIL’s Almaty lubricant plant shows how specialty niches can deliver premium margins despite scale disadvantages.

MOL Group’s 2024 agreements with KazMunayGas signal new entrants leveraging European process know-how to unlock polypropylene potential. Technology gaps persist: Tengizchevroil shaved 18% from turnaround downtime via digital twins, whereas CaspiBitum still runs legacy DCS lacking predictive maintenance. The 2025 blockchain fuel-quality mandate favors integrated players with central labs; small distributors must invest in IT upgrades or exit. The Atyrau and Pavlodar refineries' 50% privatization will likely invite Honeywell or Axens process partners, accelerating energy-efficiency gains that currently trail GCC benchmarks by 12-15%.

Privatization dilutes state stake yet retains strategic oversight through KazMunayGas golden shares, balancing foreign capital needs with resource-nationalist sentiment. Competitive intensity is expected to rise as Sinopec and SIBUR capture polymer export channels and as MOL seeks crude security via partial vertical integration.

Kazakhstan Oil And Gas Downstream Industry Leaders

National Company KazMunayGas (KMG)

PetroKazakhstan Inc.

PJSC Lukoil Oil Company

Kazakhstan Petrochemical Industries LLP

KazTransOil JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kazakhstan unveiled ambitious plans to ramp up its oil refining capacity from the current 18 million tons to a target of 40 million tons annually by 2040. The strategy involves expanding existing facilities, such as Shymkent, and constructing a new plant with a capacity of 10 million tons.

- July 2025: Kazakhstan has rolled out an ambitious energy strategy, targeting a threefold increase in petroleum product exports by 2040. The plan envisions refined fuel volumes soaring to 39 million tons annually, a significant jump from the current 17 million. Notably, the export share is poised to rise to 30% of the nation's total output.

- May 2025: Kazakhstan's Ministry of Energy unveiled a roadmap, heralding a strategic pivot from exporting raw materials to producing high-value products. This ambitious plan, set to unfold by 2030, earmarks an investment of around USD 15 billion in the nation's oil and gas chemical sector.

- January 2025: Kazakhstan's government enacted a ban on the export of gasoline and diesel fuel via road and rail. This restriction, detailed in amendments to the joint order titled "On Some Issues of Export of Oil Products from the Territory of the Republic of Kazakhstan," received approval from key officials, including the Minister of Energy, the Chairman of the National Security Committee (KNB), and the Ministers of Finance and Internal Affairs.

Kazakhstan Oil And Gas Downstream Market Report Scope

The oil and gas downstream segment includes the distribution, sales, marketing, and retailing of oil and gas byproducts.

The Kazakhstan oil & gas downstream market is segmented by type, product type, distribution channel, and geography. By type, the market is segmented into refineries and petrochemical plants. By product type, the market is segmented into refined petroleum products, petrochemicals, and lubricants. By distribution channel, the market is segmented into direct sales/wholesale, distributors/commercial channels, and retail outlets. For each segment, market sizing and forecasts have been conducted on the basis of value (USD).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the current value of the Kazakhstan downstream market?

The Kazakhstan downstream market size stands at USD 1.84 billion in 2026 and is projected to reach USD 2.57 billion by 2031.

Which segment is growing the fastest in Kazakhstan’s downstream sector?

Petrochemical plants are the fastest-growing segment, advancing at an 8.9% CAGR through 2031 on the back of the Silleno polyethylene and KPI polypropylene investments.

How will Kazakhstan meet rising Euro-5 fuel demand?

Shymkent, Pavlodar, and Atyrau refineries are adding hydrotreaters and hydrocrackers that lift Euro-5 diesel and gasoline output, eliminating previous reliance on Russian imports.

What role does China play in Kazakhstan’s export strategy?

China receives 62% of Kazakh crude via the Kazakhstan-China Pipeline; it will also buy most polyethylene output once the Silleno plant comes online.

Why are water stress and talent shortages considered key risks?

Declining Ural and Irtysh river flows cap refinery water withdrawals, while a 1,200-engineer shortfall delays digital-twin and safety-system deployment, both of which could dampen forecast growth.

Page last updated on: