Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

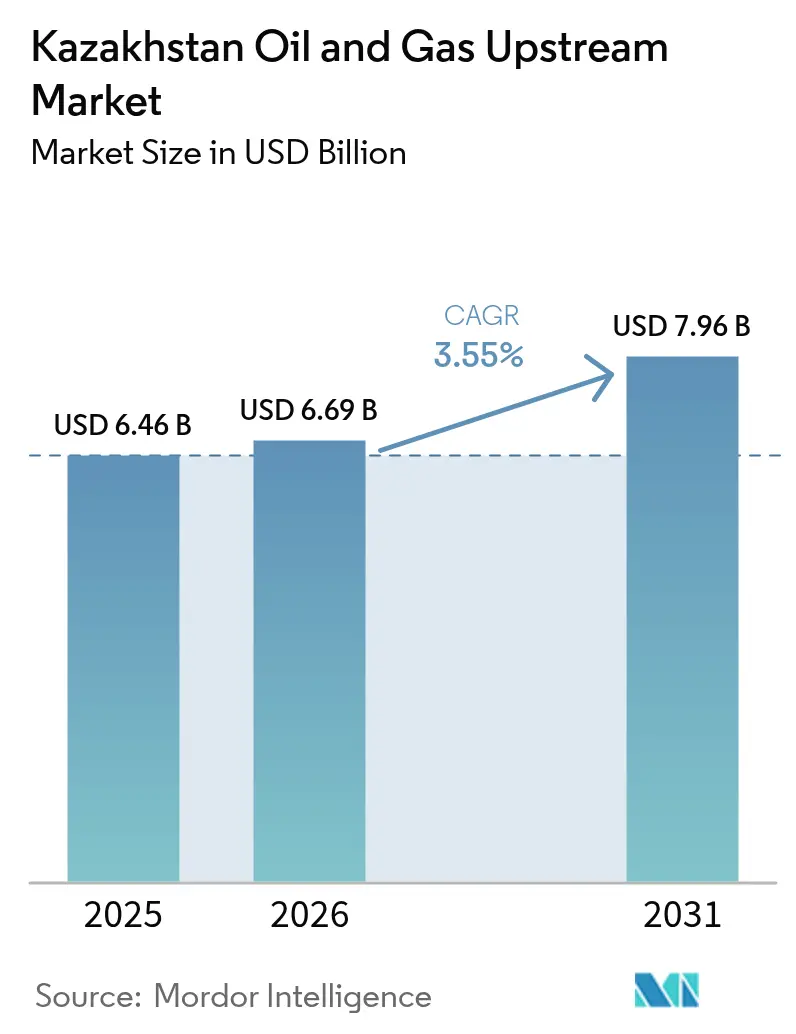

| Base Year Market Size (2025) | USD 6.46 Billion |

| Market Size (2026) | USD 6.69 Billion |

| Market Size (2031) | USD 7.96 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Kazakhstan Oil And Gas Upstream Market size was valued at USD 6.46 billion in 2025 and estimated to grow from USD 6.69 billion in 2026 to reach USD 7.96 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031).

A sustained pivot toward offshore megaprojects, rapid adoption of enhanced recovery methods, and gradual diversification of export routes underpin this growth despite persistent sulfur-handling costs and aging onshore infrastructure. Offshore assets already account for 83.8% of 2024 revenues and post the fastest 5.5% growth, while Chevron’s USD 48 billion Tengiz upgrade, Kashagan Phase 2, and larger China-bound pipelines carry the expansion momentum. Crude oil keeps its 70.2% volume dominance; however, associated gas is accelerating as four processing plants add 8.4 bcm of capacity between 2026 and 2030. Conventional wells still account for 95% of activity, but unconventional tight plays are growing at a rate of 5.3% annually, driven by new tax relief and digital twin analytics.

Key Report Takeaways

- By location of deployment, offshore commanded 83.18% of the Kazakhstan oil and gas upstream market share in 2025 and is projected to expand at a 5.25% CAGR through 2031.

- By resource type, crude oil led with a 69.58% share of the Kazakhstan oil and gas upstream market size in 2025, while natural gas is forecast to grow at a 4.85% CAGR to 2031.

- By well type, conventional operations accounted for a 94.32% share in 2025; unconventional wells are expected to register the highest 5.05% CAGR over 2026-2031.

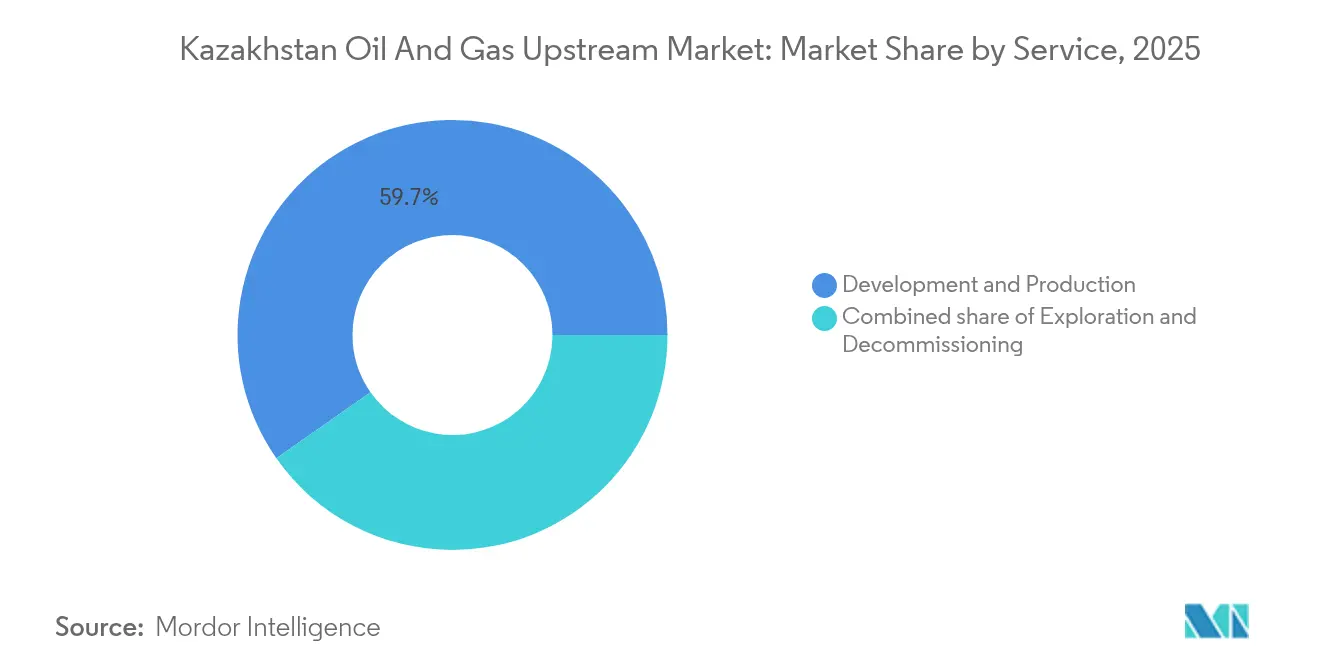

- By service, development and production services held a 59.72% share in 2025, whereas decommissioning services posted the strongest 5.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kazakhstan Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price recovery boosting E&P budgets | +1.2% | Atyrau, Mangystau | Short term (≤ 2 years) |

| Kashagan Phase-2 ramp-up | +0.9% | Offshore Caspian Sea | Medium term (2-4 years) |

| Enhanced oil-recovery tax incentives | +0.7% | National | Medium term (2-4 years) |

| China-bound trunk pipeline expansions | +0.6% | West Kazakhstan-Xinjiang | Long term (≥ 4 years) |

| Digital twin adoption for sour-gas fields | +0.3% | Karachaganak, Tengiz, Kashagan | Medium term (2-4 years) |

| Low-carbon CCS pilots unlocking deeper reservoirs | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-price recovery boosting E&P budgets

Exploration and production budgets increased by 18% in 2024, as Brent remained above USD 75 per barrel. Capital inflows accelerated drilling at Uzen, resulting in 5,900 tonnes of extra output in Q1 2024. Chevron fast-tracked Tengiz completion on similar price support.[1]Chevron Corporation, “Tengiz Future Growth Project Update,” chevron.com Yet compliance with OPEC+ quotas capped national production at 1.7 million bpd, exposing the Kazakhstan oil and gas upstream market to price volatility.

Kashagan Phase-2 ramp-up

Phase 2 lifts Kashagan capacity from 370,000 bpd to 450,000 bpd by 2027 through the installation of new wellhead platforms and the addition of 3.5 bcm of gas processing. Sour-gas-resistant steel and real-time corrosion monitoring reduce downtime by 60% compared to 2022-2023. Break-even costs decreased from USD 45 to USD 32 per barrel following efficiency gains.

Enhanced oil-recovery tax incentives

The 2024 Enhanced Contract Model halves the corporate tax for CO2-EOR and polymer flooding, reducing Tengiz's payback from nine to six years.[2]Ministry of Energy of Kazakhstan, “Enhanced Contract Model,” energy.gov.kz Karachaganak pilots lift recovery to 48% while locking in 2.1 million t CO₂ each year.

China-bound trunk pipeline expansions

China's capacity is expected to reach 20 million tons in 2024 and rise to 25 million tons by 2027, reducing reliance on the Russian route from 85% in 2024 to a forecasted 75% by 2030.[3]CNPC, “Kazakhstan-China Pipeline Expansion,” cnpc.com.cn New pumps and thicker pipe grades prevent quality penalties that once shaved USD 3 per barrel off netbacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sulfur-content processing costs | -0.8% | Kashagan, Karachaganak, Tengiz | Medium term (2-4 years) |

| Aging onshore infrastructure | -0.6% | Mangystau, Atyrau | Long term (≥ 4 years) |

| Export-route dependency on Russian pipelines | -0.4% | National | Medium term (2-4 years) |

| Water-stress-related social opposition | -0.3% | Mangystau, Aral basin | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High sulfur-content processing costs

Hydrogen sulfide levels of 15-19% inflate development costs 25-35% above global averages.[4]Eni S.p.A., “Kashagan H₂S Challenges,” eni.com Operators spend USD 400 million each year replacing corroded pipe at Kashagan, while Tengiz stores 600,000 t of elemental sulfur annually.

Aging onshore infrastructure

More than 35,000 km of pipelines, averaging 30 years old, require USD 20 billion in upgrades by 2030. Recent spills in Mangystau intensified regulatory scrutiny and raised operating costs by 15-20%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore supremacy drives technical innovation

Offshore assets generated USD 5.37 billion, or 83.18% of the Kazakhstan oil and gas upstream market size in 2025, and are forecasted to grow at a 5.25% CAGR through 2031. Kashagan, Tengiz’s carbonate shelf, and the Kalamkas-Sea cluster headline this push toward deeper, higher-pressure reservoirs. Continuous technology transfer from global majors brings sour-gas-resistant alloys and real-time corrosion surveillance to the Caspian Sea projects. Investments of USD 6 billion are earmarked for Kalamkas-Sea and Khazar, underscoring enduring confidence despite caustic gas and ice-prone waters.

Onshore operations remain vital, but they contribute only USD 1.09 billion, or 16.82%, of the Kazakhstan oil and gas upstream market in 2025. Aging Soviet-era gathering lines and rising water stress curb onshore growth to a 2.65% CAGR. Nonetheless, smart-workover programs at Uzen and Zhetybai, coupled with CO₂-EOR tax relief, extend field life and prevent abrupt decline.

By Resource Type: Crude oil dominance faces natural gas acceleration

Crude oil supplied 69.58% of 2025 revenue, translating to USD 4.49 billion within the Kazakhstan oil and gas upstream market size, and is set for a 3.65% CAGR through 2031. Tengiz’s expansion is already delivering 260,000 bpd by mid-2025, while Kashagan Phase 2 targets 450,000 bpd. Premium Mangistau and Buzachi grades enjoy widening Asian refinery demand.

Natural gas, worth USD 1.97 billion in 2025, climbs 4.85% annually as four processing plants add 8.4 bcm capacity. Karachaganak’s 4 bcm increment and new fiscal incentives for associated-gas utilization reduce flaring and propel export potential to China.

By Well Type: Conventional foundations enable unconventional growth

Conventional activity captured 94.32% of 2025 spending, yet grows a moderate 3.35% CAGR. Extended-reach laterals now exceed 8,000 meters, unlocking attic oil left behind in carbonate reefs.

Unconventional wells, a 5.68% slice today, become the agility playbook, registering a 5.05% CAGR as the Enhanced Contract Model slashes tax by half. Tight plays in the Chu-Sarysu Basin exhibit initial rates of 150-200 bpd after multi-stage fracs, and AI-driven geosteering reduces drilling costs by 20%.

By Service: Development leadership yields to decommissioning growth

Development and production services accounted for 59.72% of 2025 revenue, but decelerated to a 3.62% CAGR once large projects reached a plateau. AI-enabled drilling, exemplified by KazMunayGas’s ABAI system, helps maintain healthy margins.

Decommissioning, now at 14.20%, is expected to accelerate at a 5.4% CAGR as 2,500 wells face retirement by 2030. Cost estimates of USD 150,000-300,000 per well, combined with tight remediation rules, spur early provisioning by majors.

Geography Analysis

The Atyrau and Mangystau corridor generated 77.23% of the national output in 2025, equivalent to USD 4.99 billion of Kazakhstan's oil and gas upstream market size. Tengiz and Kashagan expansions lift the corridor's production CAGR to 3.9% through 2031. Upstream operators benefit from nearby CPC and Kazakhstan-China pipeline hubs, though USD 15 billion in pipeline renewal remains urgent.

Kyzylorda and Aktobe together accounted for 15.39% of 2025 revenue and registered a 4.0% CAGR, as deeper formations and tight plays attract capital. Karachaganak's gas upgrade adds 4 bcm handling, reducing prior reinjection bottlenecks. Regulatory flexibility, including tax holidays in frontier areas, stimulates seismic and appraisal activity.

Eastern and northern provinces represent the remaining 7.38% but gain longer-term interest as seismic coverage improves. Infrastructure gaps are narrowing with the planned construction of rail-to-pipeline terminals and potential Trans-Caspian links to western export routes.

Competitive Landscape

The five largest operators—KazMunayGas, Chevron, Eni, Shell, and TotalEnergies—control roughly 65% of productive capacity, giving the Kazakhstan oil and gas upstream market a moderately concentrated profile. CNOOC’s USD 2.1 billion joint venture around Tengiz and MOL Group’s broad alliance demonstrate that international interest remains high despite geopolitical tensions. Technology remains the prime differentiator: digital twins, high-alloy steels, and CO₂-EOR deliver measurable efficiency gains. New entrants include AI-specialist service companies that cut drilling downtime and secure contracts across sour-gas fields. Environmental stewardship is becoming a competitive moat as ISO 14001 certification accelerates permitting in water-stressed areas.

Kazakhstan Oil And Gas Upstream Industry Leaders

National Company JSC (KazMunayGas)

Chevron Corporation

Karachaganak Petroleum Operating B.V.

Eni S.p.A.

PJSC Gazprom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: KazMunayGaz, Kazakhstan's state-run oil and gas firm, inked an exploration partnership with China's CNOOC International.

- January 2025: Chevron’s Tengiz Future Growth Project produced first oil, confirming 260,000 bpd capacity by June 2025

- November 2024: MOL Group and KazMunayGas signed a cooperation agreement on EOR projects in Mangystau.

- February 2024: Kazakh authorities have taken over a privately held venture, paving the way for the next phase of the USD 50 billion-plus Kashagan project, led by Eni, which is located offshore in Kazakhstan.

Kazakhstan Oil And Gas Upstream Market Report Scope

The Kazakhstan oil and gas upstream market report include:

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decommissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decommissioning |

Key Questions Answered in the Report

What is the projected value of the Kazakhstan oil and gas upstream market by 2031?

It is forecast at USD 7.96 billion, rising from USD 6.69 billion in 2026.

Which segment records the fastest growth through 2031 in Kazakhstan?

Offshore developments expand at a 5.25% CAGR, led by the Kashagan Phase-2 program.

How significant is natural gas in Kazakhstan's upstream portfolio?

Natural gas represents 30.42% of 2025 revenue and grows 4.85% annually on new processing capacity.

What tax incentives support mature-field recovery in Kazakhstan?

The 2024 Enhanced Contract Model halves corporate tax for projects deploying CO?-EOR, polymer flooding and related techniques.

How is Kazakhstan reducing reliance on Russian export routes?

Capacity on the Kazakhstan-China Pipeline climbs to 25 million t by 2027, lowering Russian route dependency from 85% to about 75% by 2030.

What is the outlook for decommissioning services?

They hold 14.20% share today and rise 5.4% annually through 2031 as 2,500 wells need abandonment by 2030.

Page last updated on: