Beta Blockers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.5 Billion |

| Market Size (2031) | USD 14 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

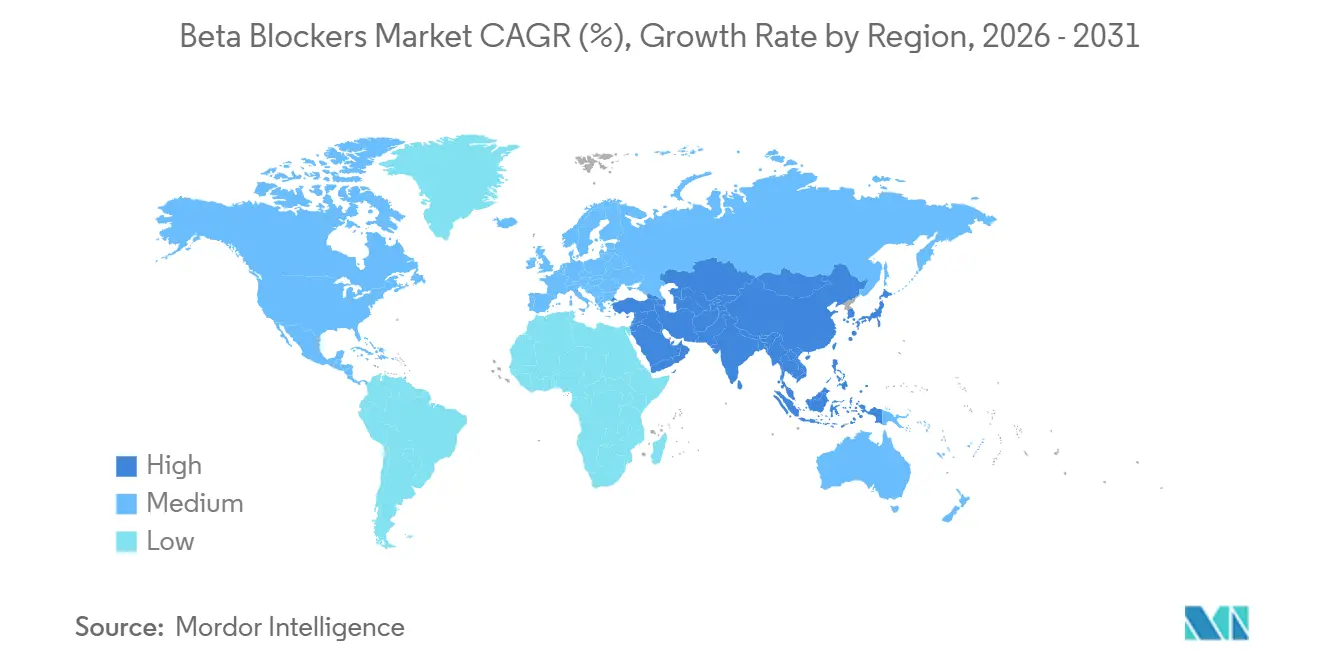

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Beta Blockers Market Analysis by Mordor Intelligence

The Beta Blockers Market size is projected to be USD 11 billion in 2025, USD 11.5 billion in 2026, and reach USD 14 billion by 2031, growing at a CAGR of 4.01% from 2026 to 2031.

Demand remains anchored in heart failure, atrial fibrillation, and post-myocardial infarction protocols, but recent hypertension and glaucoma guideline revisions are shifting first-line volume toward other drug classes. Uptake of ultra-short-acting intravenous agents, extended-release tablets, and fixed-dose combinations is broadening the addressable patient pool while mitigating adherence gaps. Supply dynamics are influenced by intermittent sterile injectable shortages, single-source active pharmaceutical ingredient (API) disruptions, and aggressive generic tendering that compresses margins while keeping prices accessible in emerging economies. Manufacturers that can safeguard uninterrupted supply, secure hospital contracts, and differentiate with innovative formulations are positioned to capture incremental value as the beta blockers market navigates both therapeutic headwinds and procedural tailwinds.

Key Report Takeaways

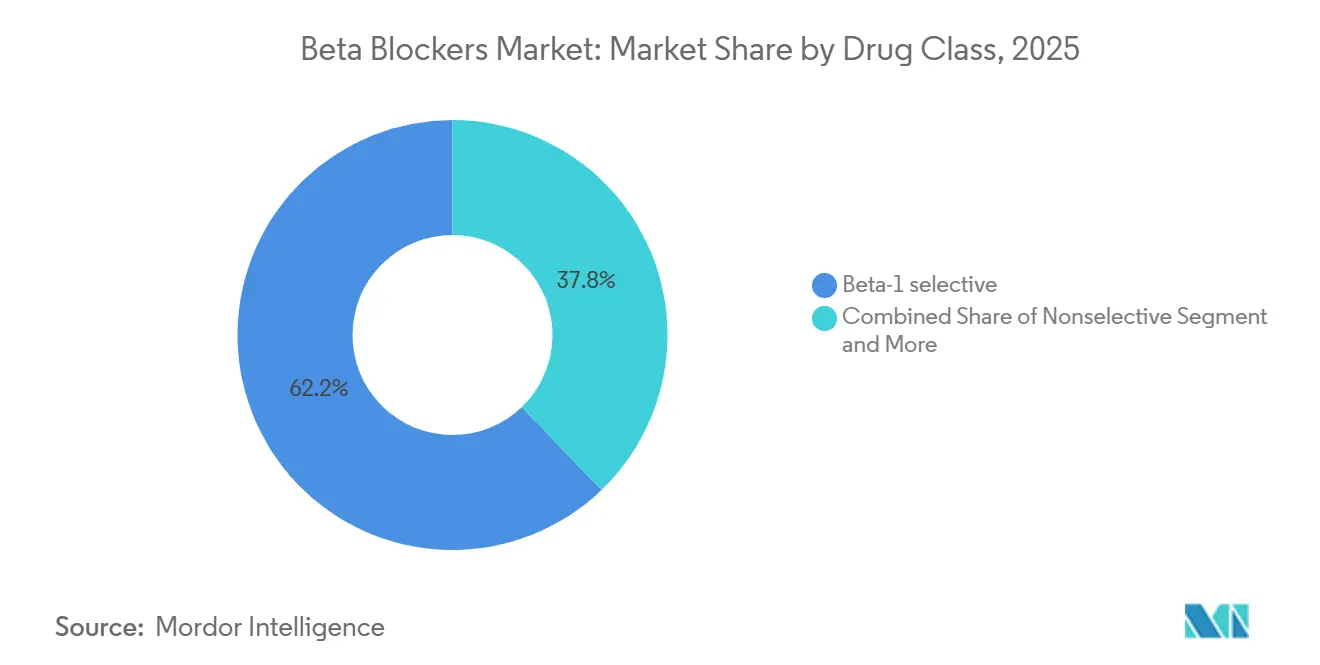

- By drug class, beta-1 selective agents led with 62.18% revenue share in 2025, and are expected to grow at 4.35% by 2031; nonselective and combined alpha-beta subclasses trailed but continue to serve niche indications.

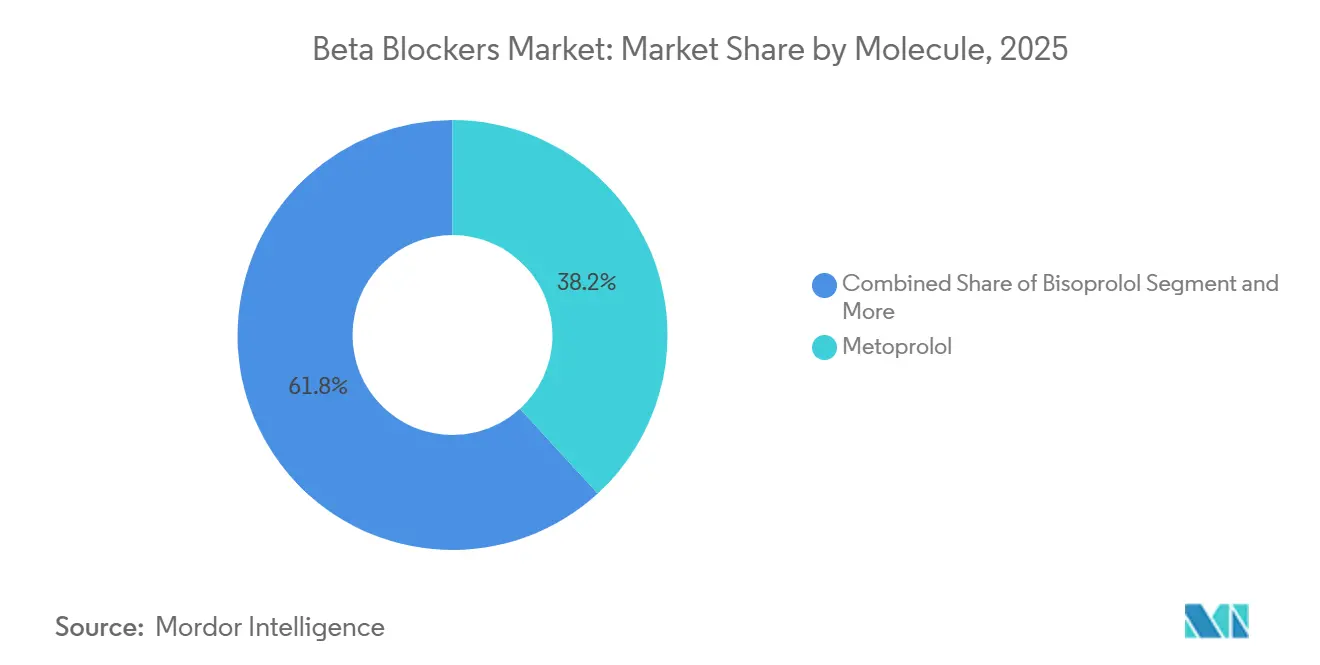

- By molecule, metoprolol held 38.19% of the beta-blocker market share in 2025, while nebivolol posted the highest projected CAGR of 4.28% through 2031.

- By route of administration, oral formulations accounted for 78.19% of the beta blockers market size in 2025 and are advancing at a 4.02% CAGR through 2031.

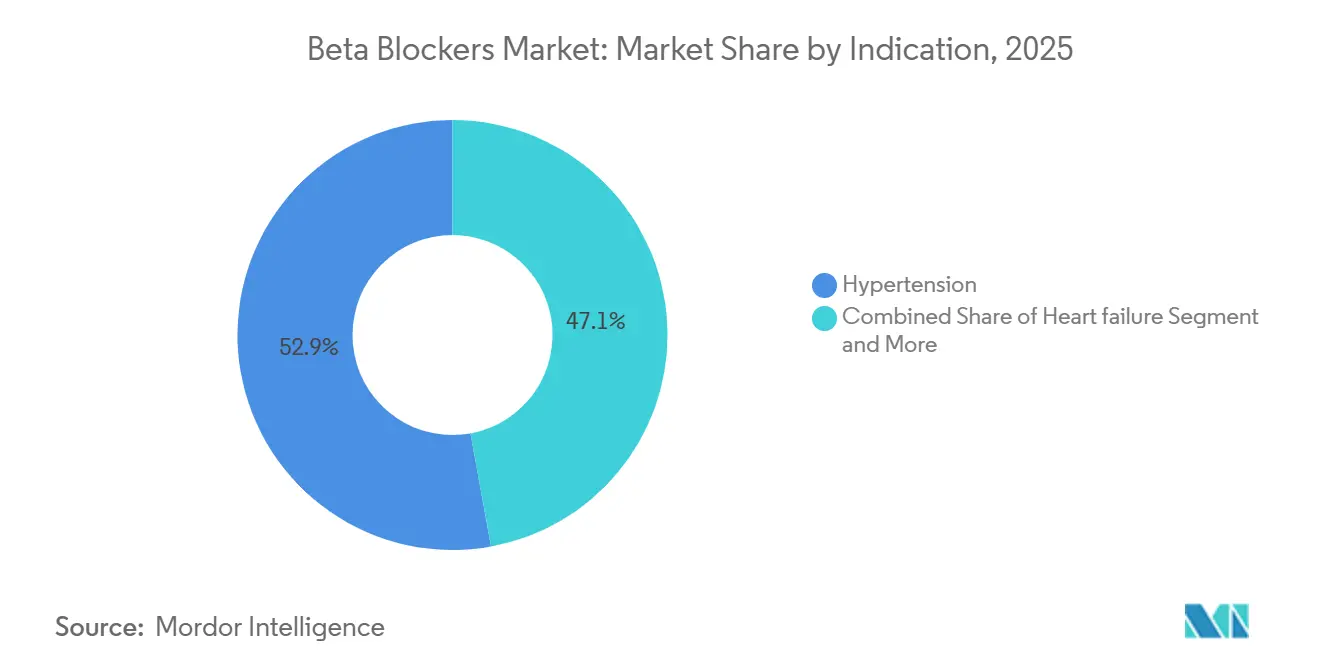

- By indication, angina and ischemic heart disease are forecast to expand at a 4.32% CAGR between 2026-2031, outpacing hypertension, even though the latter retained a 52.87% volume share in 2025.

- By distribution channel, hospital pharmacies accounted for 52.80% of units in 2025, yet online and e-pharmacies are growing fastest at a 4.19% CAGR on the back of telemedicine-enabled chronic-care models.

- By geography, North America held 33.18% of the beta blockers market share in 2025, yet Asia-Pacific is expected to advance at 4.30% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Beta Blockers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foundational role in HFrEF, AF rate control, and post-MI care is maintained in leading guidelines | +1.2% | Global, with the strongest adherence in North America and Western Europe | Long term (≥ 4 years) |

| Hypertension and ischemic heart disease prevalence sustaining chronic beta-blocker prescriptions | +1.0% | Global, particularly Asia-Pacific and the Middle East & Africa, due to the rising CVD burden | Long term (≥ 4 years) |

| Growing glaucoma and ocular hypertension pool supporting ophthalmic beta-blocker demand | +0.3% | North America, Europe, and aging populations in Japan and South Korea | Medium term (2-4 years) |

| Expansion of ultra-short-acting IV beta-1 blockers (esmolol, landiolol) in ICU/perioperative settings | +0.5% | North America, Europe, and advanced hospital systems in APAC | Medium term (2-4 years) |

| ER/CR and fixed-dose combinations improving adherence and persistence | +0.4% | Global, with early adoption in North America and Europe, spreading to APAC | Short term (≤ 2 years) |

| Portal hypertension prophylaxis broadening noncardiac use of nonselective beta blockers | +0.2% | Global, with concentrated use in regions with high hepatitis B/C prevalence (APAC, MEA) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Foundational Role in Heart Failure and Post-Infarction Care Anchors Long-Term Demand

Guidelines from the Japanese Circulation Society in 2025 maintained Class I recommendations for beta blockers alongside renin-angiotensin and sodium-glucose cotransporter-2 inhibitors, reinforcing universal inclusion in quadruple therapy [1]Japanese Circulation Society, “JCS/JHFS 2025 Guideline on Heart Failure,” j-circ.or.jp. Landmark trials such as MERIT-HF continue to inform reimbursement audits that link hospital payments to beta-blocker prescription rates in North America and Europe. The European Society of Cardiology’s 2024 atrial-fibrillation guideline still positions beta blockers ahead of calcium-channel blockers for rate control in impaired left-ventricular function. Mortality benefits after acute coronary syndrome remain robust, sustaining formulary preference in emergency pathways. As a result, long-term utilization in heart-failure and post-myocardial-infarction patients continues to outweigh the volume lost from uncomplicated hypertension.

Cardiovascular Disease Burden Sustains Chronic Prescribing Despite Guideline Shifts

World Health Organization statistics place global cardiovascular deaths at 19.8 million in 2022, with hypertension and coronary disease leading the etiology. The American Heart Association 2025 update cited 122.4 million U.S. adults with hypertension, populations in which beta blockers remain either preferred add-ons or first-line for compelling indications. Real-world registries from India show beta-blocker penetration exceeding 75% across major cardiovascular admissions, validating continued physician reliance even where local guidelines lag European and U.S. revisions. These prevalence dynamics, especially in Asia-Pacific and MEA, underpin sustained baseline demand and compensate for the gradual pullback in initial hypertension prescriptions

Ultra-Short-Acting Intravenous Formulations Expand Critical-Care Utility

The U.S. FDA cleared landiolol in 2025 for perioperative and intensive-care arrhythmia control, providing a four-minute half-life alternative to esmolol’s nine minutes. Landiolol enables beat-by-beat titration during structural-heart procedures, advancing its use in hybrid operating rooms across Europe and Japan. Esmolol shortages logged in the FDA drug-shortage database during 2024-2025 spurred hospitals to dual-source contracts and accelerated formulary reviews for landiolol. Critical-care societies now recommend ultra-short-acting beta-1 agents ahead of amiodarone for rapid rate control, citing a lower toxicity profile [2]European Society of Cardiology, “2024 ESC Guidelines on Atrial Fibrillation,” escardio.org. The procedural growth of minimally invasive valve and rhythm interventions is therefore broadening the beta blockers market in acute settings.

Extended-Release Formulations and Fixed-Dose Combinations Lift Adherence Metrics

A multicenter adherence analysis published in 2024 reported 78% 12-month persistence with once-daily metoprolol succinate versus 62% with the twice-daily tartrate formulation, leading to fewer emergency visits. Similar gains were observed with extended-release bisoprolol in elderly patients with heart failure. Single-pill regimens that pair beta blockers with renin-angiotensin inhibitors achieved blood-pressure targets in the majority of patients, outperforming free combinations by 14 percentage points. The FDA’s approval of sprinkleable metoprolol succinate capsules further opens pediatric and dysphagic adult segments. Formulation innovation is therefore a pivotal lever for manufacturers seeking to gain a share of the beta blockers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deprioritization as first-line in uncomplicated hypertension in updated guidelines | -0.8% | Global, most pronounced in Europe and North America where guideline adherence is high | Short term (≤ 2 years) |

| Prostaglandin analogs favored as first-line in glaucoma, lowering beta-blocker initiation | -0.3% | North America, Europe, and Japan with advanced ophthalmology infrastructure | Medium term (2-4 years) |

| Global generic price erosion and tendering pressure compress margins | -0.4% | Global, with acute impact in Europe, Latin America, and government-tendered markets in APAC | Short term (≤ 2 years) |

| Sterile injectable shortages and API supply risks constrain hospital availability | -0.2% | North America and Europe, where hospital formularies rely on single-source injectables | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Guideline Revisions Narrow First-Line Hypertension Use

The 2024 European Society of Cardiology hypertension guideline removed beta blockers from standard first-line therapy in patients without compelling cardiac indications [3]American Academy of Ophthalmology, “Preferred Practice Pattern: Primary Open-Angle Glaucoma 2024,” aao.org. The 2025 American Heart Association update echoed this stance after meta-analyses showed superior stroke prevention with renin-angiotensin and calcium-channel inhibitors. Clinical-decision-support platforms across Europe and the United States implemented the change within months, immediately influencing prescribing behavior in primary care settings. Although Asia-Pacific and MEA countries have not yet updated local algorithms, multinational companies report lower hypertension-only initiation rates in mature markets, trimming near-term growth in the beta blockers market.

Prostaglandin Analogs Capture First-Line Glaucoma Share

The American Academy of Ophthalmology’s 2024 guidance promoted prostaglandin analogs as first-line therapy for primary open-angle glaucoma, relegating topical beta blockers to an adjunctive role. A systematic review in 2025 confirmed superior intraocular pressure reduction with once-daily prostaglandins compared with twice-daily beta blockers. Reimbursement formularies subsequently prioritized latanoprost and newer dual-mechanism drops, compressing sales of topical beta-blockers, particularly in North America, Europe, and Japan. As ophthalmology accounts for lesser share of the beta blocker market, the impact is modest but material for manufacturers reliant on timolol revenues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Cardioselective Agents Dominate on Safety and Tolerability

Cardioselective molecules such as metoprolol, bisoprolol, and nebivolol captured 62.18% of 2025 revenue, and this share of the beta blockers market is projected to expand at a 4.35% CAGR through 2031. Cardioselectivity mitigates the risk of bronchospasm in patients with reactive airway disease, thereby widening the eligible heart-failure and post-infarction populations. Nebivolol’s nitric-oxide stimulation lowers peripheral resistance, driving its status as the fastest-rising molecule within the class. Nonselective agents retain relevance in portal hypertension prophylaxis and ophthalmology, while carvedilol and labetalol serve heart failure and emergent hypertensive crises, respectively.

Physician preference for cardioselective therapy is also guided by payer quality metrics that benchmark bronchospasm-related readmissions. European narrow-spectrum reimbursement lists grant small price premiums for bisoprolol based on the CIBIS-II mortality record, whereas North American formularies emphasize interchangeability, reinforcing high generic substitution rates. As outcome-based reimbursement spreads to emerging economies, the performance edge of cardioselective drugs is expected to secure steady expansion in the beta blockers market.

By Route of Administration: Oral Formulations Lead, Intravenous Gains in Acute Care

Oral tablets accounted for 78.19% of 2025 prescriptions, representing the largest share of the beta blocker market in chronic therapy. Once-daily extended-release designs reduce peak-to-trough variability, enhancing tolerability and adherence. Intravenous formulations are recording a 4.21% CAGR, driven by the perioperative and intensive-care requirements for rapid on-off hemodynamic control. Hospitals increasingly favor landiolol for its ultra-short profile when managing heart rate during transcatheter interventions.

Topical ophthalmic solutions are declining in stand-alone use but remain part of fixed-dose prostaglandin combinations. Regulatory barriers are comparatively higher for IV and combination products, as bioequivalence studies must confirm immediate systemic availability or additive efficacy. Manufacturers that can navigate these pathways hold an advantage in differentiated, higher-margin sub-segments of the beta blockers market.

By Indication: Hypertension Largest, Angina Fastest-Growing

Hypertension still accounted for 52.87% of dispensed volume in 2025, but is contracting in relative terms due to guideline downgrades. In contrast, angina and ischemic heart disease show the highest segmental CAGR of 4.32%, elevating their contribution to overall beta blocker market growth. Secondary prevention after myocardial infarction continues to require long-term beta-blocker therapy, and registries indicate adherence rates above 80% at one year when extended-release formulations are used.

Heart-failure guidelines worldwide enforce beta-blocker inclusion in quadruple therapy. Arrhythmia management supports IV utilization, while propranolol maintains steady off-label demand in migraine prophylaxis, although CGRP antagonist encroachment is visible among privately insured cohorts. These mixed dynamics imply that manufacturers must balance volume strategies in hypertension with value strategies in specialty cardiovascular niches.

By Distribution Channel: Hospital Pharmacies Dominant, E-Pharmacies Accelerating

Hospital pharmacies supplied 52.80% of 2025 units, driven by acute coronary, surgical, and critical care use of injectable and immediate-release products. Group-purchasing organizations negotiate deep discounts, forcing generic producers to compete on scale and reliability rather than price alone. Retail chains handle most refill traffic for chronic indications, but online and e-pharmacies are accelerating fastest at 4.19% CAGR.

Digital prescriptions linked to automatic delivery and reminder services are especially attractive to rural patients and younger cohorts. Compliance with serialization rules under the EU Falsified Medicines Directive and U.S. DEA regulations is essential for e-pharmacies to maintain consumer confidence. Traditional brick-and-mortar outlets are responding by integrating telepharmacy consultations, signaling convergence across channels within the beta blockers market.

By Molecule: Metoprolol Leads, Nebivolol Fastest-Growing

Metoprolol captured 38.19% of revenue in 2025, split between succinate extended-release for maintenance therapy and tartrate for emergent indications. Its inclusion on essential medicines lists guarantees tenders in low- and middle-income countries, sustaining baseline volumes. Nebivolol is expanding at a 4.28% CAGR, driven by vasodilatory benefits that attenuate fatigue and erectile dysfunction symptoms associated with older agents.

Bisoprolol dominates European heart-failure programs, carvedilol retains a foothold in combined alpha-beta niches, and esmolol plus landiolol drive the IV subsegment. Manufacturers that can ensure uninterrupted API supply, especially for metoprolol succinate, will maintain leadership as government tenders grow stricter on delivery penalties.

Geography Analysis

North America generated 33.18% of 2025 revenue, aided by Medicare Part D coverage, heart-failure quality metrics, and high penetration of extended-release formulations. The Centers for Medicare & Medicaid Services financially reward hospitals that meet beta-blocker prescription benchmarks, ensuring stable institutional demand. Canada’s provincial formularies preferentially reimburse generics, compressing brand premiums.

Asia-Pacific is the fastest-growing region, with a 4.30% CAGR. India’s ROBUST registry recorded metoprolol use in over three-quarters of cardiovascular discharges, and China’s volume-based procurement lists metoprolol at prices below USD 0.05 per tablet, an environment favoring vertically integrated firms. Japan and South Korea show rising heart-failure prevalence, but prostaglandin analogs are cannibalizing topical beta-blocker sales in glaucoma.

Europe’s market is mature and price-sensitive due to parallel trade and aggressive tendering, yet volumes remain resilient thanks to national heart-failure initiatives. German physicians retain loyalty to Concor bisoprolol, while the United Kingdom’s National Health Service mandates generic substitution. Southern European austerity continues to channel prescriptions toward the lowest-cost suppliers. Middle East & Africa and South America lag in share but show potential as insurance coverage widens through public-private partnerships.

Competitive Landscape

The beta blockers market is highly fragmented. Generic giants—Viatris, Teva, Sandoz, Sun Pharmaceutical, Aurobindo, Dr. Reddy’s, Cipla, Lupin, Torrent, Zydus, and Hikma—dominate volume through low-cost APIs and large fill-finish plants. Branded specialists such as Baxter (esmolol), AOP Health (landiolol), Merck KGaA (bisoprolol Concor), and Menarini (nebivolol) defend higher-margin niches via formulation patents or hospital exclusivity contracts.

Viatris reported a February 2026 fire at its Nashik, India, site, coupled with an existing FDA import alert on Indore, collectively disrupting USD 370 million of metoprolol and bisoprolol revenue and causing regional spot-price volatility. Baxter’s multi-site sterile network helped backfill esmolol shortages logged in the FDA database during 2024-2025, highlighting supply resilience as a competitive lever. An industry consortium is transferring metoprolol succinate API production to the United States by 2026, potentially realigning North American sourcing patterns toward domestic suppliers.

Emerging challengers from India and China are gaining European market authorization for extended-release generics, undercutting incumbents in tenders and pushing consolidation among midsize firms. Strategic white space exists in pediatric sprinkle formulations, fixed-dose combos with SGLT2 inhibitors, and ultra-short-acting injectables tailored for structural-heart interventions. Competitors that couple regulatory compliance with differentiated technology are set to command above-average growth inside the beta blockers market.

Beta Blockers Industry Leaders

Viatris Inc

Teva Pharmaceutical

Sandoz

Sun Pharmaceutical

Dr. Reddy’s Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cytokinetics, Incorporated, presented new clinical data reinforcing the profile of MYQORZO (aficamten) at the European Society of Cardiology (ESC) Heart Failure 2026 Congress.

- November 2025: AstraZeneca reported positive Phase 3 results in 2025 for baxdrostat, a novel aldosterone synthase inhibitor for treating hypertension.

- June 2025: Cadila Pharmaceuticals launched Biscado (Bisoprolol) in India to address high blood pressure and chronic heart failure.

- February 2025: Dr. Reddy’s Laboratories and Emcure Pharmaceuticals merged their generic injectables businesses to create a leading global player in that segment.

Global Beta Blockers Market Report Scope

As per the scope of the report, beta blockers, also known as beta-adrenergic blocking agents, are a class of medications primarily used to manage various cardiovascular conditions by blocking the effects of stress hormones like adrenaline (epinephrine) and noradrenaline. By binding to beta receptors throughout the body, these drugs slow the heart rate and reduce the force of heart muscle contractions, effectively lowering blood pressure and decreasing the heart's oxygen demand.

The beta blockers market is segmented by drug class, molecules, route of administration, indication, distribution channel, and geography. Based on drug class, the market is segmented into beta-1 selective, nonselective, and combined alpha/beta. By molecules, the market is segmented into metoprolol, bisoprolol, atenolol, nebivolol, carvedilol, and others. By route of administration, the market is segmented into oral, intravenous, and ophthalmic (topical). By Indication, the market is segmented into hypertension, heart failure (HFrEF), arrhythmias (AF/SVT rate control), angina & ischemic heart disease, and other indications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, online / E-pharmacies.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Beta-1 Selective |

| Nonselective |

| Combined Alpha/Beta |

| Metoprolol |

| Bisoprolol |

| Atenolol |

| Nebivolol |

| Carvedilol |

| Others |

| Oral |

| Intravenous |

| Ophthalmic (topical) |

| Hypertension |

| Heart failure (HFrEF) |

| Arrhythmias (AF/SVT Rate Control) |

| Angina & Ischemic Heart Disease |

| Other Indications |

| Hospital pharmacies |

| Retail Pharmacies and Drug Stores |

| Online / E-pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Beta-1 Selective | |

| Nonselective | ||

| Combined Alpha/Beta | ||

| By Molecule | Metoprolol | |

| Bisoprolol | ||

| Atenolol | ||

| Nebivolol | ||

| Carvedilol | ||

| Others | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Ophthalmic (topical) | ||

| By Indication | Hypertension | |

| Heart failure (HFrEF) | ||

| Arrhythmias (AF/SVT Rate Control) | ||

| Angina & Ischemic Heart Disease | ||

| Other Indications | ||

| By Distribution Channel | Hospital pharmacies | |

| Retail Pharmacies and Drug Stores | ||

| Online / E-pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the beta blockers market, and how fast is it growing?

The beta blockers market size stood at USD 11.5 billion in 2026 and is on track to reach USD 14.0 billion by 2031 at a 4.01% CAGR.

Which drug class leads global revenue?

Beta-1 selective agents such as metoprolol and bisoprolol controlled 62.18% of 2025 sales, owing to superior safety in airway disease.

Why are intravenous beta blockers gaining momentum?

Ultra-short-acting injectables like landiolol enable rapid titration during surgery and critical care without long systemic exposure, driving a 4.21% CAGR in the IV segment.

How have hypertension guidelines affected beta blocker demand?

European and U.S. guidelines published in 2024-2025 removed beta blockers from first-line uncomplicated hypertension therapy, trimming initiation rates in primary care.

Page last updated on: