Size and Share of Japan Sapphire Crystal Growth Equipment Market for LED Substrates

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

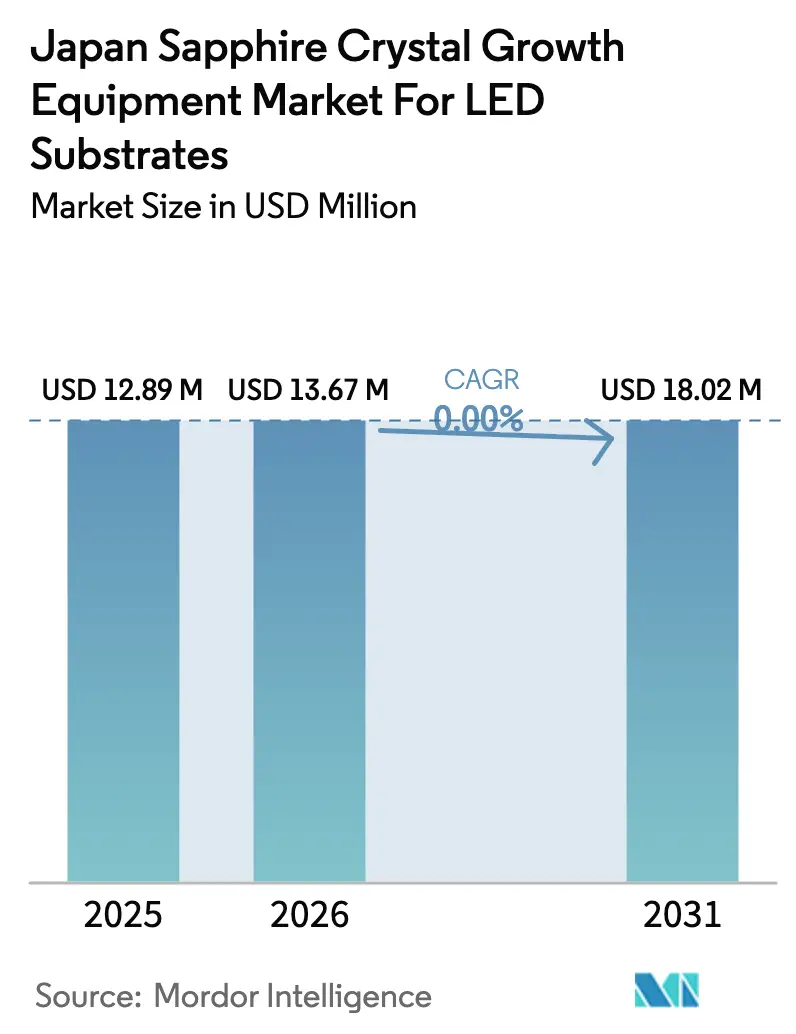

| Base Year Market Size (2025) | USD 12.89 Million |

| Market Size (2026) | USD 13.67 Million |

| Market Size (2031) | USD 18.02 Million |

| Growth Rate (2026 - 2031) | 0.00% CAGR |

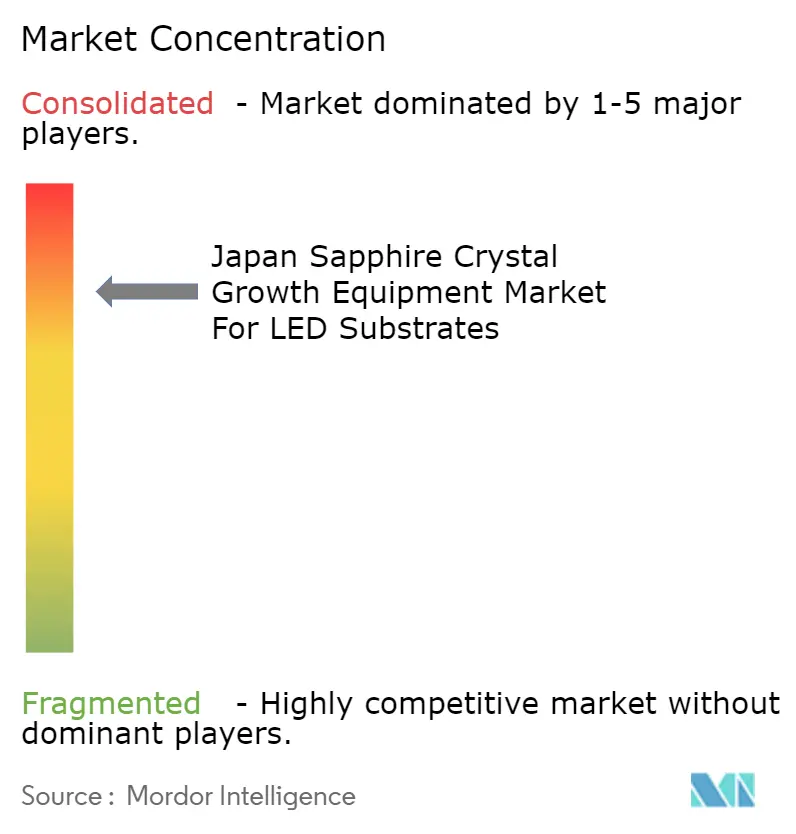

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Japan Sapphire Crystal Growth Equipment Market for LED Substrates by Mordor Intelligence

The Japan sapphire crystal growth equipment market for LED substrates industry size is expected to increase from USD 12.89 million in 2025 to USD 13.67 million in 2026 and reach USD 18.02 million by 2031, growing at a CAGR of 5.68% over 2026-2031. Strong display-panel demand for mini-LED and micro-LED back-lighting is widening the domestic order book for large-diameter, low-defect sapphire furnaces, even as general-lighting demand plateaus. Equipment spending is heavily skewed toward Kyropoulos and Czochralski furnaces that can yield 6-inch and 8-inch boules with stable thermal gradients, while integrated metrology and AI-driven control modules push yields higher and labor dependency lower. Energy-cost volatility and tight iridium and molybdenum supply chains still weigh on smaller epitaxial houses, but government subsidies and vertical-integration moves by local component makers are trimming effective payback horizons for new tool installs.

Key Report Takeaways

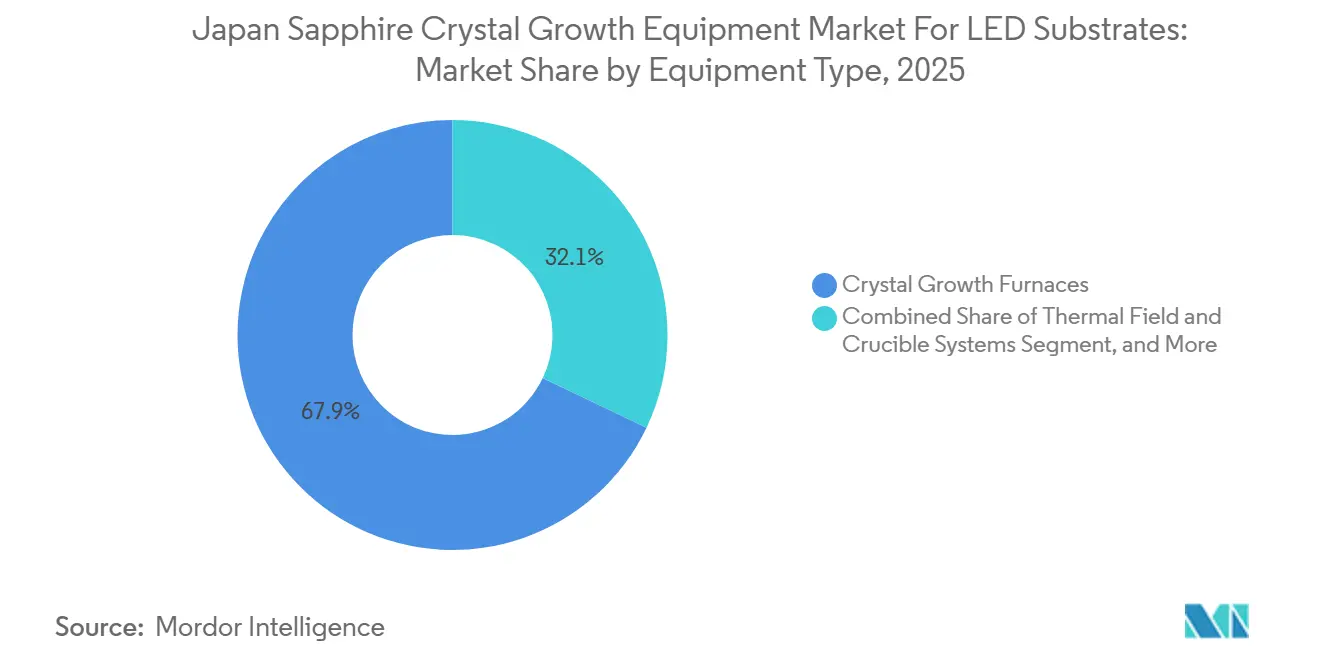

- By equipment type, crystal growth furnaces led with 67.91% revenue share in 2025; growth automation and process control systems are projected to expand at a 6.17% CAGR through 2031.

- By growth technology, the Kyropoulos method held 58.73% share of the Japan sapphire crystal growth equipment market for LED substrates industry in 2025, while the Czochralski method is forecast to grow at a 6.24% CAGR to 2031.

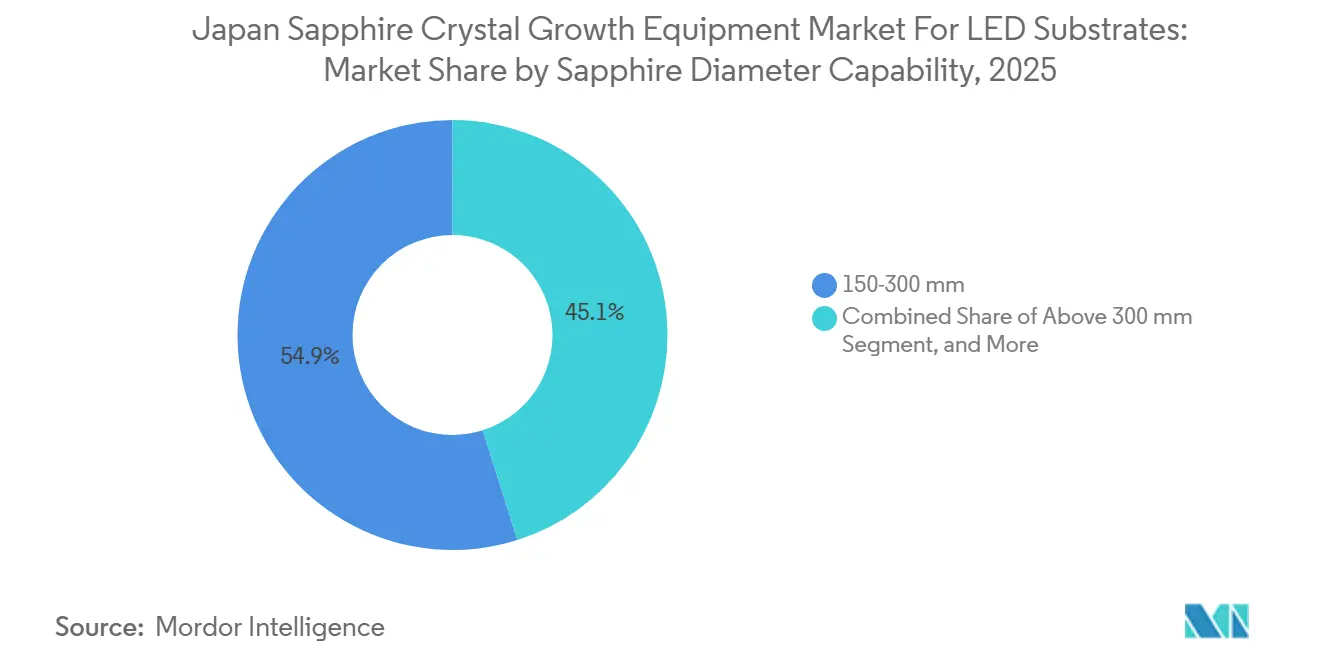

- By sapphire diameter capability, 150-300 mm systems accounted for 54.88% share of the Japan sapphire crystal growth equipment market for LED substrates industry size in 2025 and above-300 mm platforms are advancing at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Japan. The sapphire crystal growth equipment for led substrates market share in our global report expresses these relative weights.

Insights and Trends of Japan Sapphire Crystal Growth Equipment Market for LED Substrates

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Mini- and Micro-LED Back-lighting in High-Resolution Displays | +1.8% | Japan, spillover to South Korea and Taiwan | Medium term (2-4 years) |

| Government Incentives for Domestic LED Supply-Chain Localization | +1.2% | National, concentrated in Kyushu and Tohoku | Long term (≥ 4 years) |

| Mainstream Adoption of 6-Inch Wafer Lines by Japanese LED IDMs | +1.0% | National, early gains in Tokushima and Yamaguchi | Short term (≤ 2 years) |

| Efficiency Gains from Furnace Automation and AI-Based Process Control | +0.9% | Global, Japan early adopter | Medium term (2-4 years) |

| Shift Toward 8-Inch Sapphire Wafers in Consumer-Electronics Flash LEDs | +0.7% | Japan and Greater China | Long term (≥ 4 years) |

| Emergence of GaN-on-Sapphire Power Devices in EV Chargers | +0.5% | Domestic EV component suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Mini- and Micro-LED Back-lighting in High-Resolution Displays

Premium television, notebook, and automotive OEMs moved from edge-lit to mini-LED architectures during 2025, multiplying the number of die-level emitters per panel and pushing sapphire-wafer pullers to run longer campaigns. Commercial micro-LED pilots now target sub-100 µm die sizes grown on 6-inch c-plane sapphire, eliminating color filters and thick encapsulants for thinner displays with higher contrast. Osaka University demonstrated europium-doped GaN red LEDs on sapphire that approach 10% external quantum efficiency, allowing monolithic full-color stacks without die-transfer steps. Orbray responded with high-flatness 6-inch substrates that show total-thickness variation below 10 µm, accelerating adoption at Tokushima and Yamaguchi fabs.[1]Orbray, “Sapphire Single-Crystal Substrate Specifications,” orbray.com Electric-vehicle cockpits, which house multiple high-resolution displays, add an auto-grade reliability requirement that further anchors domestic sapphire demand.

Government Incentives for Domestic LED Supply-Chain Localization

Tokyo earmarked roughly USD 870 million in 2024 for compound-semiconductor R&D hubs, with dedicated lines for wide-band-gap devices grown on sapphire.[2]Ministry of Economy, Trade and Industry, “Semiconductor and Compound Semiconductor R&D Support Programs,” meti.go.jp Subsidies lower crystal-growth furnace payback from seven to about four years for small epitaxial houses, while workforce programs rebuild a talent pool hollowed out during the 2010s offshoring wave. Security concerns heightened urgency when China briefly restricted gallium and germanium exports in 2023; policymakers now target 30% local sapphire-wafer self-sufficiency by 2030, implying annual furnace installations 15-20% above historical norms.

Mainstream Adoption of 6-Inch Wafer Lines by Japanese LED IDMs

Japan’s top LED makers finished a two-year shift from 4-inch to 6-inch sapphire in 2025. The larger format delivers 2.25× usable area, helping blunt an 8-12% annual ASP slide in commodity lighting chips. Orbray scaled edge-defined film-fed growth (EFG) to meet 6-inch demand, supplying 1.3 mm-thick wafers with sub-15 µm total-thickness variation. Furnace vendors captured the resulting replacement cycle; Kyropoulos tools built for 4-inch boules could not meet thermal-field specs for 6-inch, prompting wholesale upgrades and pushing the Japan sapphire crystal growth equipment market for LED substrates toward fresh capital outlays despite flat end-market units.

Labor shortages intensified as veteran furnace operators retired in greater numbers than new graduates entered crystal engineering. Linton Crystal Technologies inserted AI-driven facet detection into Czochralski pullers in 2024, trimming scrap by 3-5 points and slashing manual interventions by roughly half.[3]Linton Crystal Technologies, “AI-Based Facet Detection for Czochralski Growth,” lintoncrystal.com PVA TePla partnered with Sentech in 2025 to mount optical metrology heads inside growth chambers, giving real-time stress maps without pausing the run.[4]PVA TePla AG, “H1 2025 Financial Results,” pvatepla.com Reinforcement-learning loops now tune heater power to match diameter set-points within ±0.5 mm, a critical enabler for 8-inch sapphire where thermal budgets are unforgiving.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses | -1.1% | National, acute in Kyushu and Shikoku | Short term (≤ 2 years) |

| Volatility in LED End-Market Demand Post-2025 Lighting Retrofit Peak | -0.9% | Export-oriented Japanese makers | Medium term (2-4 years) |

| High Energy Costs for >2000 °C Thermal Fields in Japan | -0.6% | High-tariff prefectures | Medium term (2-4 years) |

| Supply Risk of Molybdenum and Iridium Crucible Materials | -0.4% | Imports from Russia and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses

Premium Kyropoulos and Czochralski tools carry list prices ranging from USD 300,000 to USD 1.5 million, and custom large-boule systems exceed USD 2 million, placing them out of reach for many domestic specialty producers. Each furnace needs 10-20 days per pull, capping annual output near 18 runs and stretching payback horizons beyond five years unless utilization stays above 85%.[5]XKH Semitech, “Kyropoulos Furnace Capacity and Specifications,” xkhsemitech.com Japan lacks a mature leasing market for sapphire equipment, so smaller firms must either self-fund or rely on high-interest project loans, both of which constrain working capital. Some plants respond by outsourcing wafers to low-cost Chinese suppliers, sacrificing lead-time control and custom orientation options. This restraint directly slows the refresh cycle for modern, automation-ready furnaces that could lift yields and cut power use.

Volatility in LED End-Market Demand Post-2025 Lighting Retrofit Peak

General-lighting replacements peaked in 2025, and unit volumes have since flattened, pushing average selling prices down 8-12% per year for commodity blue chips. Export-heavy Japanese IDMs now face shorter visibility on purchase orders, making them cautious about locking capital into additional sapphire capacity. The temporary oversupply created during the 2024 build-ahead phase triggered a destocking wave that idled several Kyropoulos lines for multiple months. At the same time, emerging micro-LED and automotive segments are still in pilot production, generating insufficient wafer pull to offset lost lighting volumes. The gap between waning retrofit demand and future display ramps leaves furnace vendors navigating a two-to-three-year booking vacuum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Modules Redefine Value Creation

Crystal growth furnaces commanded 67.91% of the Japan sapphire crystal growth equipment market for LED substrates industry market share in 2025, underscoring their position as the largest single capital item. Thermal-field and crucible kits form the next cost block, with molybdenum replacements priced near USD 500 per piece and iridium containers fetching premium quotes on 99.99% purity needs.[6]Furuya Metal, “Iridium Crucibles for Sapphire Crystal Growth,” furuyametals.co.jp Growth-automation and process-control systems, while starting from a smaller base, are projected at a 6.17% CAGR because AI vision and in-chamber metrology cut scrap and operator minutes. Large integrated device manufacturers buy turnkey furnace-plus-automation bundles to raise throughput per clean-room square meter, whereas small specialty houses often continue with manual pullers to contain cash burn.

Competitive dynamics vary by buyer profile. Western vendors dominate high-end projects that demand tight diameter tolerances, while cost-focused Chinese suppliers court peripheral prefectures with 30-40% lower ticket prices. As labor shortages deepen, automation spending should capture an incrementally larger slice of the Japan sapphire crystal growth equipment market for LED substrates industry market size, even if the absolute number of new furnaces rises only modestly. Over the forecast horizon, software and sensor upgrades are expected to deliver more incremental value than hardware wattage alone, reshaping vendor qualification criteria.

By Growth Technology: Czochralski Pullers Close the Gap

The Kyropoulos method held 58.73% of the Japan sapphire crystal growth equipment market for LED substrates industry market share in 2025 because its slow-cool profile yields low threading dislocation densities that boost LED external quantum efficiency. It remains the default for 6-inch production due to proven yield curves and well-understood thermal models. Czochralski pullers, however, are poised for a 6.24% CAGR as AI diameter control and cleaner iridium crucibles achieve ±0.5 mm uniformity on 8-inch boules. Hybrid frames that toggle between the two modes are emerging, letting fabs hedge format risks without duplicating capital.

Edge-defined film-fed growth continues to serve optical parts producers that need net-shape ribbons, while heat-exchanger systems win orders where void-free optics justify longer growth times. The growing mix shift toward Czochralski should lift demand for real-time melt monitoring and higher-power induction heaters, widening the accessory revenue pool. As display and flash-LED markets swing to larger wafers, Kyropoulos is expected to hold baseline volumes, but software-rich Czochralski lines will capture most incremental additions to the Japan sapphire crystal growth equipment market for LED substrates industry market size.

By Sapphire Diameter Capability: Above-300 mm Tools Lead Expansion Curve

Equipment rated for 150-300 mm boules delivered 54.88% of the Japan sapphire crystal growth equipment market for LED substrates industry market size in 2025, reflecting the recently completed transition to 6-inch processing across many domestic LED fabs. Orbray’s epi-ready wafers, featuring sub-0.3 nm surface roughness and less than 15 µm total-thickness variation, set the reference standard in this diameter band and continue to anchor mid-scale demand. These tools offer a balanced trade-off between material yield and manageable thermal-gradient control, ensuring consistent puller utilization in commodity and specialty lighting.

Above-300 mm platforms are forecast to expand at a 6.31% CAGR through 2031 as micro-LED and smartphone flash-LED developers migrate to 8-inch wafers that yield roughly 2.8× more dies than a 6-inch. The larger format magnifies stress management challenges, so suppliers embed reinforcement-learning loops that modulate heater power in real time and minimize boule cracking. Up-to-150 mm systems now cater mainly to R&D and deep-ultraviolet niches and are expected to trend flat as the industry consolidates around larger substrates. Consequently, next-generation puller orders will skew toward high-power, tightly insulated chambers, positioning >300 mm capacity as the primary growth engine for the Japan sapphire crystal growth equipment market for LED substrates industry market share over the forecast horizon.

Geography Analysis

Kyushu commands the largest Japan sapphire crystal growth equipment market for LED substrates industry market share because its long-standing semiconductor parks host most of the nation’s installed Kyropoulos and Czochralski lines. The cluster benefits from shared high-purity gas networks, proximity to power-device fabs and a pool of furnace technicians trained since the early 2000s. Prefectural grants further reduce the effective purchase price of automation modules, encouraging fast adoption of AI vision tools. As a result, Kyushu fabs post higher furnace-utilization ratios than peers in other regions, sustaining steady demand for crucible replacements and control-software upgrades. Local governments now market the area as a one-stop ecosystem for sapphire substrates, reinforcing its pull on new investments.

Tohoku is the fastest-growing regional node, supported by Ministry of Economy, Trade and Industry subsidies that cover a portion of crystal-growth tool costs. Newly built R&D hubs in Miyagi and Fukushima offer shared pilot lines where equipment makers demonstrate automation features under real production loads. These trial programs shorten qualification cycles for next-generation pullers and attract mid-sized epitaxial houses looking to expand beyond 6-inch wafers. The Japan sapphire crystal growth equipment market size in Tohoku is therefore expected to rise more quickly than the national average through 2031, even though its absolute base remains smaller than Kyushu’s.

Tokushima and Yamaguchi retain strategic weight because they host vertically integrated LED leaders that grow sapphire, run epitaxy and perform final device packaging on contiguous campuses. Their plants were early movers to 6-inch wafers and now pilot 8-inch boules, creating an ongoing replacement cycle for above-300 mm furnace frames. In contrast, Shikoku and selected Chugoku prefectures contain several small specialty epi-houses that delay tool upgrades until capital grants become available, limiting short-term order flow. Nationwide, high electricity tariffs continue to shape site-selection logic, pushing new pullers toward regions with stable grid prices and preferential rate programs, yet overall geographic dispersion remains tight around the three core clusters.

Mordor Intelligence examines the sapphire crystal growth equipment market for led substrates across diverse other regional markets as well, including Asia, while also offering granular country-level perspectives for China and Taiwan and more.

Competitive Landscape

The vendor field shows moderate concentration; the five largest suppliers account for roughly one-half of annual furnace shipments, leaving meaningful headroom for mid-tier challengers. European specialists PVA TePla and ECM Greentech dominate premium bids by pairing thermal-field modelling with inline optical metrology that trims scrap. Ferrotec leverages in-house heaters, vacuum seals and SiC crucible liners to ship turnkey Czochralski packages on shorter lead times than rivals, an edge that resonates with Japanese fabs pursuing rapid 6-inch-to-8-inch transitions. Chinese entrants Luoyang Kunsheng and Shanghai Xinkehui compete heavily on price, often undercutting incumbents by 30-40% but facing longer qualification runs inside quality-sensitive integrated device manufacturers. Overall, buyer choice splits along capability lines: tier-one IDMs value yield and service depth, while cost-focused niche houses weigh capital savings more heavily.

Strategic moves illustrate how suppliers protect or expand share. In 2025 PVA TePla embedded optical-stress sensors directly into Kyropoulos chambers, allowing real-time feedback that improves boule uniformity and reduces manual diameter checks. That same year Ferrotec opened its Ishikawa No. 3 plant, adding 13,000 m² of ceramic-part capacity and tightening its control over heater and crucible supply. Linton Crystal Technologies released an AI facet-detection software module that cuts operator interventions by about half, aligning with Japan’s shrinking labor pool. ECM Greentech partnered with a local utility to pilot a low-carbon resistance-heating element, seeking to lower electricity draw at 2,000 °C setpoints and ease customer concerns over power costs. These actions show vendors shifting emphasis from sheer hardware scale to software, energy and vertical integration.

Emerging disruptors focus on footprint and flexibility. TekSiC’s induction-heated Xforge furnace launched in 2025 with a compact design that suits space-constrained suburban fabs and claims up to 20% lower energy consumption than conventional resistance units. Several mid-size Japanese machinery firms now advertise dual-purpose frames capable of growing either sapphire or silicon-carbide boules, helping fabs smooth utilization swings across product cycles. At the same time, component specialists push modular upgrades, such as smart gas mixers and reinforcement-learning control boards, that bolt onto existing furnaces and defer full line replacements. Collectively, these innovations suggest that future competitive gains will hinge less on high-temperature metallurgy alone and more on holistic cost-of-ownership packages that knit hardware, software and consumables into integrated stacks.

Leaders of Japan Sapphire Crystal Growth Equipment Market for LED Substrates

Ferrotec Holdings Corporation

Dai-ichi Kiden Co., Ltd.

Crystal Systems Corporation

ECM Greentech S.A.

Thermal Technology LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: PVA TePla and imec entered a multi-year program to co-develop inline metrology for wide-band-gap substrates, extending tool-plus-inspection packages to Japanese LED fabs.

- January 2026: Yole Group projected SiC front-end utilization near 50% in 2025, prompting some sapphire tool vendors to tout dual-use furnaces; Chinese firms already hold about 40% of SiC wafer output.

- July 2025: Ferrotec inaugurated its Ishikawa No.3 facility, adding Class 1,000 cleanrooms for ceramic parts used in sapphire pullers.

- June 2025: PVA TePla, Siltronic and the Leibniz Institute expanded an AlN-crystal project whose thermal-field lessons feed back into Kyropoulos upgrades.

Scope of Report on Japan Sapphire Crystal Growth Equipment Market for LED Substrates

The Japan Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and Growth Automation and Process Control Systems), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and Czochralski Method), and Sapphire Diameter Capability (Up to 150 mm, 150-300 mm, and Above 300 mm). The Market Forecasts are Provided in Terms of Value (USD).

| Crystal Growth Furnaces |

| Thermal Field and Crucible Systems |

| Growth Automation and Process Control Systems |

| Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) |

| Heat Exchanger Method |

| Czochralski Method |

| Up to 150 mm |

| 150-300 mm |

| Above 300 mm |

| By Equipment Type | Crystal Growth Furnaces |

| Thermal Field and Crucible Systems | |

| Growth Automation and Process Control Systems | |

| By Growth Technology | Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) | |

| Heat Exchanger Method | |

| Czochralski Method | |

| By Sapphire Diameter Capability | Up to 150 mm |

| 150-300 mm | |

| Above 300 mm |

Key Questions Answered in the Report

Which restraint most limits new furnace purchases among small Japanese epitaxial houses?

The high upfront cost of Kyropoulos and Czochralski tools, often topping USD 1 million, stretches payback periods beyond five years.

How is end-market volatility after the 2025 retrofit peak affecting equipment orders?

LED price erosion and inventory corrections have delayed new tool bookings, creating a two-to-three-year gap before micro-LED ramps scale.

Why are automation modules gaining traction in Japan's sapphire tool mix?

AI vision and inline metrology cut scrap and labor needs, vital in a market facing skilled-operator shortages.

Which growth technology is expected to gain share through 2031?

Czochralski pullers, supported by iridium crucibles and diameter-control AI, are projected for a 6.24% CAGR.

What regional clusters attract the most new furnace installations?

Kyushu and Tohoku prefectures lead because of robust semiconductor infrastructure and METI subsidy programs.

How are vendors addressing energy-cost concerns at 2000 °C process windows?

New induction-heated and better-insulated furnace frames promise up to 20% lower electricity draw, improving total cost of ownership.

Page last updated on: