Size and Share of China Sapphire Crystal Growth Equipment Market For LED Substrates

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

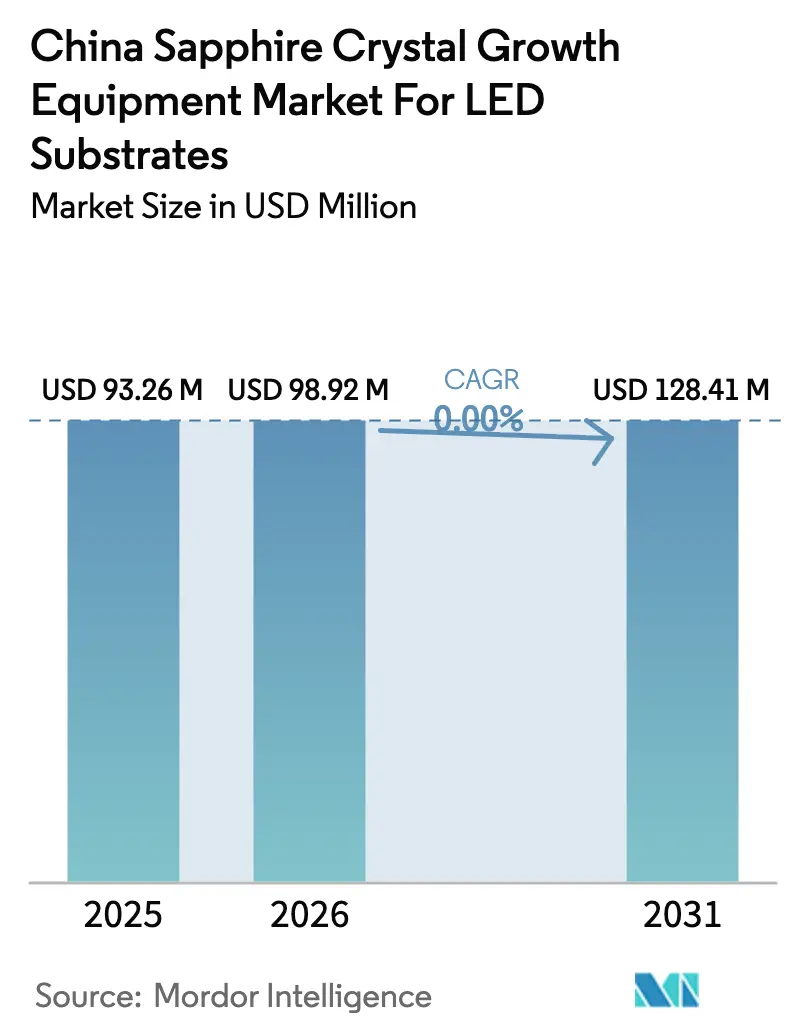

| Base Year Market Size (2025) | USD 93.26 Million |

| Market Size (2026) | USD 98.92 Million |

| Market Size (2031) | USD 128.41 Million |

| Growth Rate (2026 - 2031) | 0.00% CAGR |

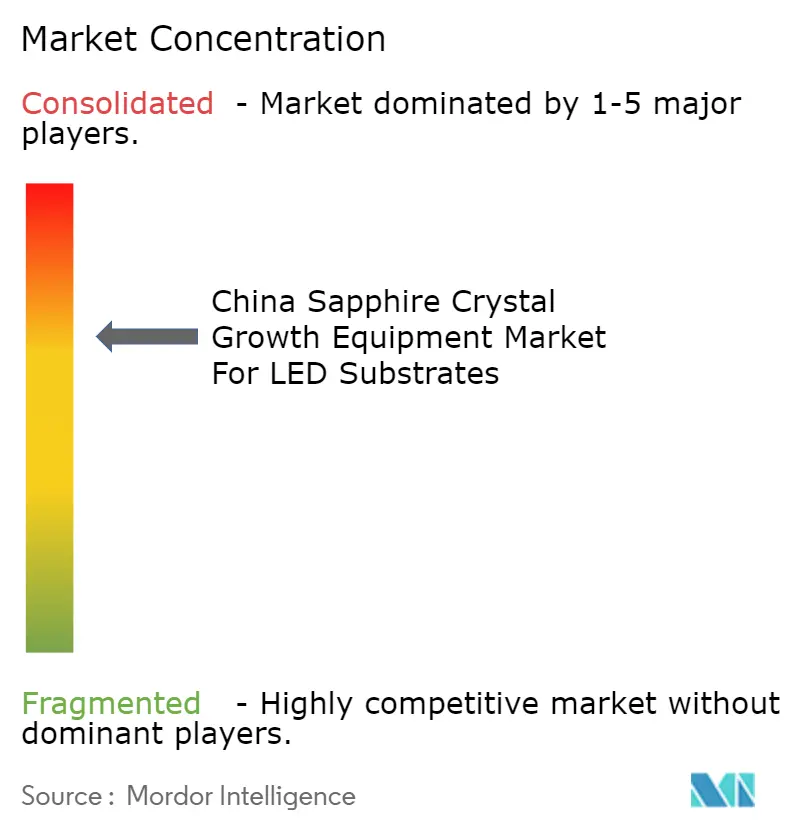

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of China Sapphire Crystal Growth Equipment Market For LED Substrates by Mordor Intelligence

The China sapphire crystal growth equipment market for LED substrates industry size was valued at USD 93.26 million in 2025 and is estimated to grow from USD 98.92 million in 2026 to reach USD 128.41 million by 2031, at a CAGR of 0% during the forecast period (2026-2031). Government directives that require at least 50% domestic content in new semiconductor fabs, together with the RMB 344 billion (USD 49.8 billion) Big Fund Phase 3 allocation, are redirecting procurement toward Chinese suppliers of Kyropoulos, Czochralski and edge-defined film-fed-growth (EFG) furnaces. Demand is further underpinned by Mini-LED backlighting investments for televisions and automotive displays, by provincial 14th Five-Year Plans that list sapphire substrates as strategic materials, and by the integration of artificial-intelligence process control that trims cycle time and improves yield. Environmental audits on high-temperature furnaces and volatility in high-purity alumina feedstock prices, however, temper near-term expansion and incentivize upgrades that cut emissions and material waste.

Key Report Takeaways

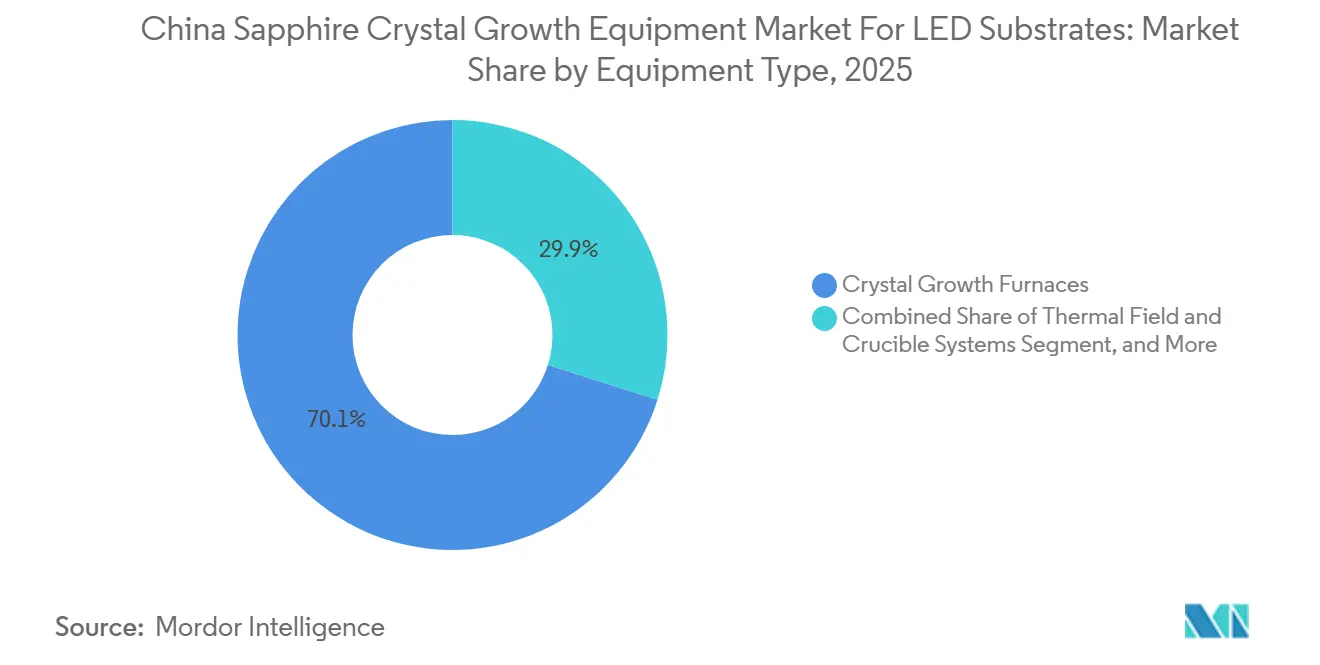

- By equipment type, crystal growth furnaces held 70.13% of the China sapphire crystal growth equipment market for LED substrates industry share in 2025.

- By growth technology, the Kyropoulos method commanded 57.82% share of the China sapphire crystal growth equipment market for LED substrates industry size in 2025.

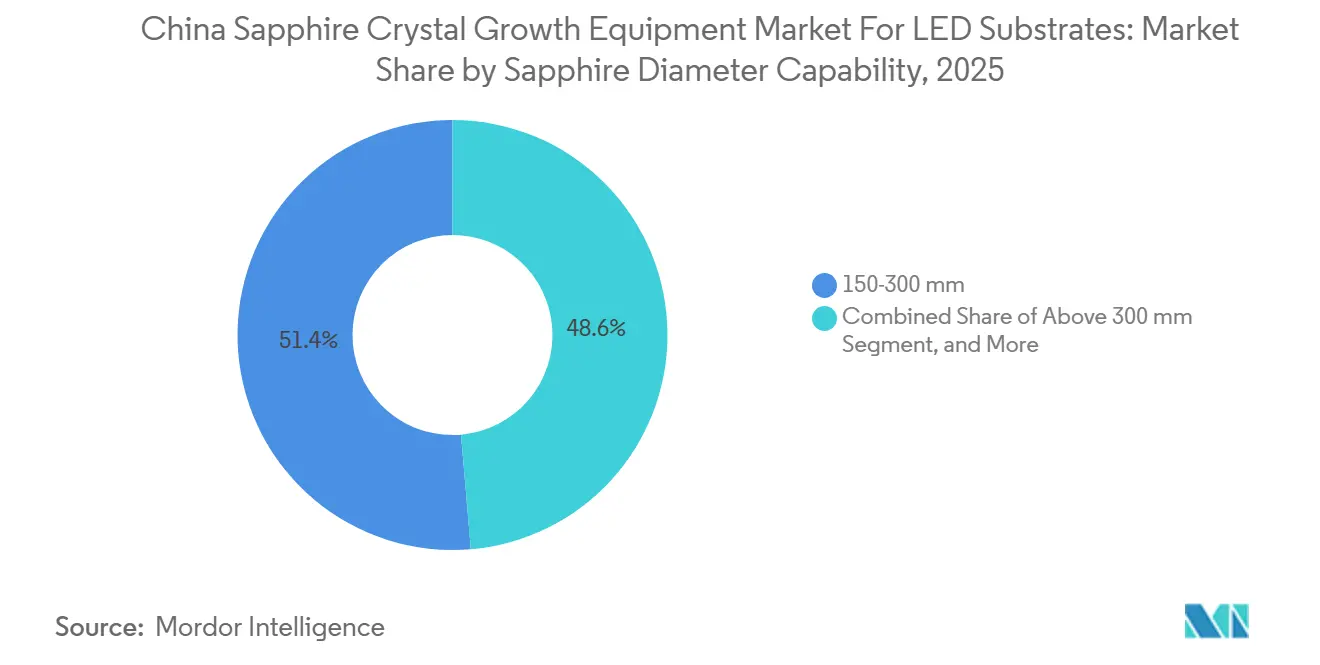

- By diameter capability, 150-300 mm systems accounted for 51.36% of the 2025 China sapphire crystal growth equipment market for LED substrates industry size, while above-300 mm systems are forecast to expand at a 6.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China contributes to a system defined not by any single country or region but by the interaction of many. The global sapphire crystal growth equipment for led substrates market data by Mordor Intelligence represents that combined structure.

Insights and Trends of China Sapphire Crystal Growth Equipment Market For LED Substrates

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Mini-LED backlighting investments | +1.2% | National clusters in Zhejiang, Jiangsu, Guangdong | Medium term (2-4 years) |

| Subsidies for domestic equipment localization | +1.5% | National | Short term (≤ 2 years) |

| Rising adoption of large-diameter (above 300 mm) sapphire ingots | +0.9% | Zhejiang and Shaanxi | Long term (≥ 4 years) |

| Surge in smart-lighting urban projects | +0.6% | Beijing, Shanghai, Chongqing, Wuhan | Medium term (2-4 years) |

| Export-oriented capacity expansion by Chinese LED makers | +0.7% | Factories serving Southeast Asia and South America | Medium term (2-4 years) |

| Integration of AI-based process control in growth furnaces | +0.5% | Leading equipment makers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Mini-LED Backlighting Investments

Television and automotive display makers are shifting from edge-lit to direct-lit Mini-LED architectures that require many more chips per panel, driving a matching surge in sapphire substrate demand. Leading LED manufacturers validated 6-inch and 8-inch wafers during 2025 pilot runs, which pushed equipment tenders for Kyropoulos and Czochralski furnaces capable of lower dislocation densities.[1]36氪 Newsdesk, “Unilumin to invest RMB 600 million in Micro and Mini-LED base,” 36kr.com Patterned sapphire substrates that boost light-extraction efficiency by nearly one-third further raise equipment requirements because they add laser patterning and plasma etch steps to the production line. Vendors able to bundle crystal growth, patterning and polishing solutions capture larger wallet share as vertically integrated LED makers prefer one-stop procurement. Consequently, Mini-LED investment pipelines continue to anchor near-term tool orders across coastal manufacturing clusters.

Export-Oriented Capacity Expansion by Chinese LED Makers

Beijing’s December 2025 rule that at least half of semiconductor tools in approved projects must be sourced domestically drives a structural shift in bidding criteria. Crystal growth equipment makers that pass technology certification gain immediate access to centrally funded orders, while imported systems without local value-add lose price competitiveness after tariff equivalencies and extended delivery lead times. The Big Fund’s earmark for compound semiconductor materials further cushions working-capital needs, enabling smaller substrate producers to swap 4-inch lines for 6-inch platforms without prohibitive upfront cash outlay.[2]Hendrik Bork, “China’s semiconductor equipment surge and the next wave in EDA,” All-About-Industries, all-about-industries.com Parallel provincial grants and tax credits accelerate retrofit timetables, locking in a near-term demand bulge for China-made furnaces, control software and consumable‐grade crucibles.

Rising Adoption of Large-Diameter (Above 300 mm) Sapphire Ingots

Twelve-inch sapphire ingots supply roughly 2.3 times the chip area of an 8-inch wafer, lowering per-die cost in high-volume Mini-LED and emerging Micro-LED applications.[3]PVA Crystal Growing Systems, “Systems Overview,” pvatepla-cgs.com Domestic furnace builders showcased 300 mm ingots in 2025 customer demos, while new computational-fluid-dynamics and neural-network algorithms stabilized the melt-solid interface, lifting usable crystal yield. Still, crucible thermal-expansion mismatches and radial-temperature-gradient control remain barriers, confining mass adoption to vertically integrated producers that can amortize higher R&D and tooling spend. For equipment suppliers, retrofit kits that let customers upgrade heater assemblies and insulation for larger diameters offer a pragmatic bridge until full 12-inch lines achieve cost parity.

Export-Oriented Capacity Expansion by Chinese LED Makers

Chinese LED companies are adding substrate and chip capacity to serve lighting and display demand in Southeast Asia and South America, reducing reliance on tariff-exposed finished-lamp exports. San’an Optoelectronics’ USD 239 million acquisition of Lumileds in August 2025 provides automotive reliability certifications and global OEM channels, compelling upstream sapphire suppliers to scale output in sync with new module programs. Offshore wafer facilities in Penang and other ASEAN locations continue to specify China-made furnaces and control software because of cost advantages and existing service relationships.[4]Malaysian Investment Development Authority, “SuperSiC breaks ground on new manufacturing facility in Penang,” mida.gov.my Export-linked expansion, therefore, sustains equipment demand even when domestic display cycles moderate. Vendors that offer remote diagnostics and multilingual support gain an edge with these geographically distributed fabs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in high-purity alumina prices | -0.4% | Nationwide exposure to bauxite supply | Short term (≤ 2 years) |

| Technical barriers in scaling Kyropoulos furnaces beyond 12-inch | -0.3% | Advanced equipment developers | Long term (≥ 4 years) |

| Stringent environmental audits on high-temperature furnaces | -0.2% | Key air-quality control zones | Medium term (2-4 years) |

| Slow retrofit cycles among Tier-2 LED wafer houses | -0.2% | Jiangxi, Anhui, Fujian clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in High-Purity Alumina Prices

High-purity alumina accounts for a sizable share of sapphire boule cost, so sudden price spikes quickly erode wafer-house margins. Bauxite supply disruptions in 2025 exposed the fragility of the refining chain, lifting spot quotes and forcing several substrate makers to delay furnace purchases.[5]Fundamental Business Insights and Consulting, “High Purity Alumina Market Size and Forecasts 2026-2035,” fundamentalbusinessinsights.com Larger producers cushioned the shock with long-term offtake contracts and in-house refining pilots, yet smaller firms lacked that hedge and trimmed operating rates. Equipment vendors felt the knock-on effects of order lumpiness and extended payment terms, which complicated factory scheduling. Sustained feedstock volatility, therefore, weighs on near-term demand and encourages vertical integration that diverts capital away from new crystal growth tools.

Technical Barriers in Scaling Kyropoulos Furnaces Beyond 12 Inch

Increasing crucible diameter beyond 300 mm intensifies radial temperature gradients, which amplifies stress rings and elevates crack risk in the outer boule. Material choices pose another hurdle, because molybdenum and tungsten crucibles contaminate melts at high power while iridium options carry prohibitive cost. These constraints lengthen process qualification cycles and raise scrap rates, deterring Tier-2 fabs that already face tight capital budgets. As a result, many producers postpone moves to 12 inch and larger formats, limiting uptake of next-generation Kyropoulos systems.[6]Andrew Novoselov, “Growth of Large Sapphire Crystals: Lessons Learned,” Journal of Crystal Growth, sciencedirect.com Until new insulation schemes and adaptive heater controls stabilize large melts, furnace upgrades will proceed in cautious increments rather than fleetwide leaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Gains Ground While Furnaces Retain Core Share

Sales of crystal growth furnaces represented 70.13% of the China sapphire crystal growth equipment market for LED substrates industry in 2025. Retrofit demand centers on heater redesigns and crucible upgrades that enhance throughput without full chassis replacement, preserving the installed base. Growth-automation and process-control systems are projected to rise at a 6.21% CAGR, a faster clip than the overall market, as wafer houses deploy AI modules that shorten seeding cycles and standardize operator skill variability. Pollution-control and electrified heating retrofits also gain traction as emission rules tighten, opening another revenue stream within the thermal-field subsystem niche.

Growth-automation and process-control modules are on track to lift their contribution to the sapphire crystal growth equipment market size as wafer houses retrofit legacy furnaces instead of buying new frames. Tool makers package closed-loop thermal management, in-situ defect imaging and predictive maintenance software as bolt-on kits that install during scheduled shutdowns, preserving production continuity. Longer-life crucibles and low-NOx heater assemblies are bundled into these upgrades, giving customers a single contact for both hardware and software. This integrated offer compresses payback to less than two years for most mid-volume fabs, a period that aligns with provincial subsidy windows and supports recurring revenue for vendors through software licenses and consumable replenishment.

By Growth Technology: Kyropoulos Dominates, Czochralski Captures Quality-Driven Niches

The Kyropoulos process held 57.82% share of China sapphire crystal growth equipment market for LED substrates industry market size in 2025, underlining its cost-performance sweet spot for mainstream LED substrates. The method’s forgiving thermal gradient and high yield per melt keep ownership cost low, sustaining its base even as larger-diameter ambitions mount. In contrast, the Czochralski segment, forecast to expand 6.38% CAGR through 2031, leans on premium demand from Micro-LED and power-device makers that pay for ultra-low dislocation densities. Edge-defined film-fed growth furnaces continue to serve specialty optical window producers but remain a minor slice of revenue.

As Mini-LED and emerging Micro-LED nodes tighten dislocation tolerances, buyers allocate a growing share of the sapphire crystal growth equipment market size to Czochralski and hybrid platforms that deliver higher optical uniformity. Suppliers respond with modular heaters, necking algorithms and real-time melt monitoring that let operators switch between Kyropoulos and Czochralski recipes without full requalification. Edge-defined film-fed growth systems remain in niche optics but benefit from the same control upgrades, extending their service life and broadening application reach. Flexible multi-method tools therefore hedge customer risk against demand swings while raising average selling price for equipment makers.

By Sapphire Diameter Capability: 12-Inch Transition Accelerates

Equipment supporting 150-300 mm boules contributed 51.36% to 2025 revenue, reflecting the dominance of 6-inch and 8-inch wafer throughput in active LED fabs. Above-300 mm tools, however, are on track for a 6.63% CAGR as vertically integrated giants pilot 12-inch ingots for future display nodes. China sapphire crystal growth equipment market for LED substrates industry market size growth in this segment is fueled by phased upgrade kits that swap heater assemblies and crucibles without reengineering the entire furnace shell, trimming capex per incremental diameter step.

Retrofit kits that convert existing 8-inch furnaces to 12-inch capacity lower capital hurdles and help above-300 mm tools expand their share of the sapphire crystal growth equipment market share. The kits include reinforced heater zones, advanced insulation panels and AI-driven gradient control that compensates for larger thermal mass. Early adopters report wafer yield gains that offset higher crucible cost within four production quarters, validating the economic case for diameter migration. As 12-inch compatible MOCVD reactors move from pilot to volume release, equipment builders expect a steady pull for large-diameter upgrades through the second half of the decade.

Geography Analysis

Zhejiang, Jiangsu and Shaanxi provinces generated the bulk of domestic shipments of the China sapphire crystal growth equipment market for LED substrates in 2025, reflecting well-established clusters that pair equipment makers with substrate and epitaxy lines. Zhejiang hosts the nation’s largest furnace producer and supports dense supplier networks for crucibles, heaters and diamond wire, which reduces lead time and logistics cost for local buyers. Jiangsu benefits from proximity to Shanghai finance hubs, allowing swift access to working capital that speeds retrofit decisions. Shaanxi leverages research institutes in Xi’an to provide simulation expertise and skilled labor, helping local firms pilot advanced thermal field designs.

Western expansion centers on Chongqing, where a vertically integrated sapphire campus anchors the largest LED materials base outside the coastal belt. Provincial incentives in the municipality cut utility tariffs and property taxes, attracting auxiliary suppliers of insulation, graphite and precision tooling. That policy mix diversifies geographic risk for equipment vendors and improves service coverage for inland wafer plants. Nearby Sichuan and Guizhou provinces have started feasibility studies for joint sapphire and silicon carbide parks, signaling future demand nodes.

Inner Mongolia, Yunnan and Ningxia use their renewable power surpluses to court crystal growth projects that need stable low-cost electricity. Each province lists sapphire substrates as a priority in its 14th Five-Year blueprint, offering grant packages that offset up to 20% of furnace capex for qualifying lines. Hubei’s Micro-LED initiative in Wuhan further broadens the map by tying photonics research to automotive supply chains, which promises follow-on orders for mid-diameter and large-diameter equipment. Collectively, these moves create a multi-polar market where service proximity and provincial incentives shape sales traction as much as product specifications.

The sapphire crystal growth equipment market for led substrates is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia. This is complemented by country-specific insights for Taiwan and Japan, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The domestic field remains moderately concentrated, with Zhejiang Jingsheng, Naura Technology and Chongqing Silian shipping a combined share a little above 60% in 2025. Jingsheng operates more than 1,000 furnaces and recently began producing diamond wire, a move that strengthens vertical integration and locks in recurring consumables revenue. Naura’s February 2026 alliance with China Youyan accelerates joint development of sputtering targets and rare-earth materials, enhancing its ability to bundle front-end and compound-materials tools in a single bid. Chongqing Silian leverages its western manufacturing base to win government LED projects that favor local sourcing, complementing coastal deployments led by its rivals.

International suppliers such as GT Advanced Technologies and PVA TePla maintain beachheads through premium Czochralski and edge-defined film-fed systems, often secured by multi-year service contracts that guarantee uniformity for specialty optics lines. Their footprint, however, faces erosion as domestic vendors close technology gaps and offer faster maintenance response. Mid-tier Chinese entrants use flexible engineering teams to customize heater zones and software interfaces, targeting Tier-2 fabs that require small batch volumes and quick delivery. This agile approach chips away at the long-tail market still held by import brands.

Software has emerged as the new battleground. Vendors embedding artificial-intelligence modules that predict heater wear and auto-adjust thermal gradients command higher annual service fees yet deliver measurable yield gains. Environmental compliance adds another competitive lever, because provinces in the Beijing-Tianjin-Hebei and Yangtze River Delta zones penalize high-NOx furnaces. Suppliers offering low-emission heater retrofits and integrated abatement skid packages therefore win replacement cycles ahead of schedule, gradually reshaping share toward firms that match cost leadership with sustainability credentials.

Leaders of China Sapphire Crystal Growth Equipment Market For LED Substrates

Zhejiang Jingsheng Mechanical & Electrical Co., Ltd.

Chongqing Silian Optoelectronics Science & Technology Co., Ltd.

GT Advanced Technologies Inc.

PVA TePla AG

Crystal Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Zhejiang Jingsheng started construction of a diamond-wire production line in Zhejiang to supply slicing consumables and deepen vertical integration.

- March 2026: Naura Technology and China Youyan signed a strategic pact to co-develop sputtering targets and rare-earth process materials, accelerating localization of upstream inputs.

- January 2026: Xinlian Integrated and partners committed RMB 3.0 billion (USD 0.43 billion) to a Micro-LED photonics plant in Wuhan, targeting automotive lighting applications.

- December 2025: San’an Optoelectronics acquired Lumileds for USD 239 million, securing automotive OEM channels and raising demand for high-grade sapphire substrates.

Scope of Report on China Sapphire Crystal Growth Equipment Market For LED Substrates

The China Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and Growth Automation and Process Control Systems), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and Czochralski Method), and Sapphire Diameter Capability (Up to 150 mm, 150-300 mm, and Above 300 mm). The Market Forecasts are Provided in Terms of Value (USD).

| Crystal Growth Furnaces |

| Thermal Field and Crucible Systems |

| Growth Automation and Process Control Systems |

| Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) |

| Heat Exchanger Method |

| Czochralski Method |

| Upto 150 mm |

| 150-300 mm |

| Above 300 mm |

| By Equipment Type | Crystal Growth Furnaces |

| Thermal Field and Crucible Systems | |

| Growth Automation and Process Control Systems | |

| By Growth Technology | Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) | |

| Heat Exchanger Method | |

| Czochralski Method | |

| By Sapphire Diameter Capability | Upto 150 mm |

| 150-300 mm | |

| Above 300 mm |

Key Questions Answered in the Report

What is the projected compound annual growth rate for China's sapphire crystal growth equipment through 2031?

The segment is forecast to expand at a 5.36% CAGR between 2026 and 2031.

How much revenue is the segment expected to generate by 2031?

It is projected to reach USD 128.41 million in 2031.

Which equipment category commands the biggest share of sales?

Crystal growth furnaces led with 70.13% of 2025 revenue.

Which crystal-growth method is showing the fastest expansion?

The Czochralski method is projected to grow at a 6.38% CAGR through 2031.

What drives interest in 12-inch sapphire systems?

A 12-inch wafer provides about 2.3× the chip area of an 8-inch wafer, cutting cost per LED chip and aligning with existing 300 mm processing lines.

Where are the primary production clusters located?

The key hubs are Zhejiang, Jiangsu and Shaanxi, with emerging bases in Chongqing and Hubei.

Page last updated on: