Size and Share of Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 159.78 Million |

| Market Size (2026) | USD 170.63 Million |

| Market Size (2031) | USD 227.06 Million |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates by Mordor Intelligence

The Asia-Pacific sapphire crystal growth equipment market for LED substrates industry size is expected to grow from USD 159.78 million in 2025 to USD 170.63 million in 2026 and is forecast to reach USD 227.06 million by 2031 at a 5.88% CAGR over 2026-2031. Robust panel investments in Mainland China, steady demand from Korea and Taiwan, and renewed capacity planning in Southeast Asia continue to anchor capital spending. Government stimulus programs in China, Taiwan, and Japan shorten payback cycles for qualifying tool purchases, while panel makers’ migration to 8-inch sapphire drives demand for larger, more automated furnaces. Crystal-growth automation that minimizes operator-dependent seeding variability is emerging as a preferred add-on, especially among fabs chasing micro-LED readiness. Currency and commodity cost swings remain a swing factor, but rising mini-LED penetration in televisions, monitors, and automotive displays provides a firm demand floor for sapphire substrates.

Key Report Takeaways

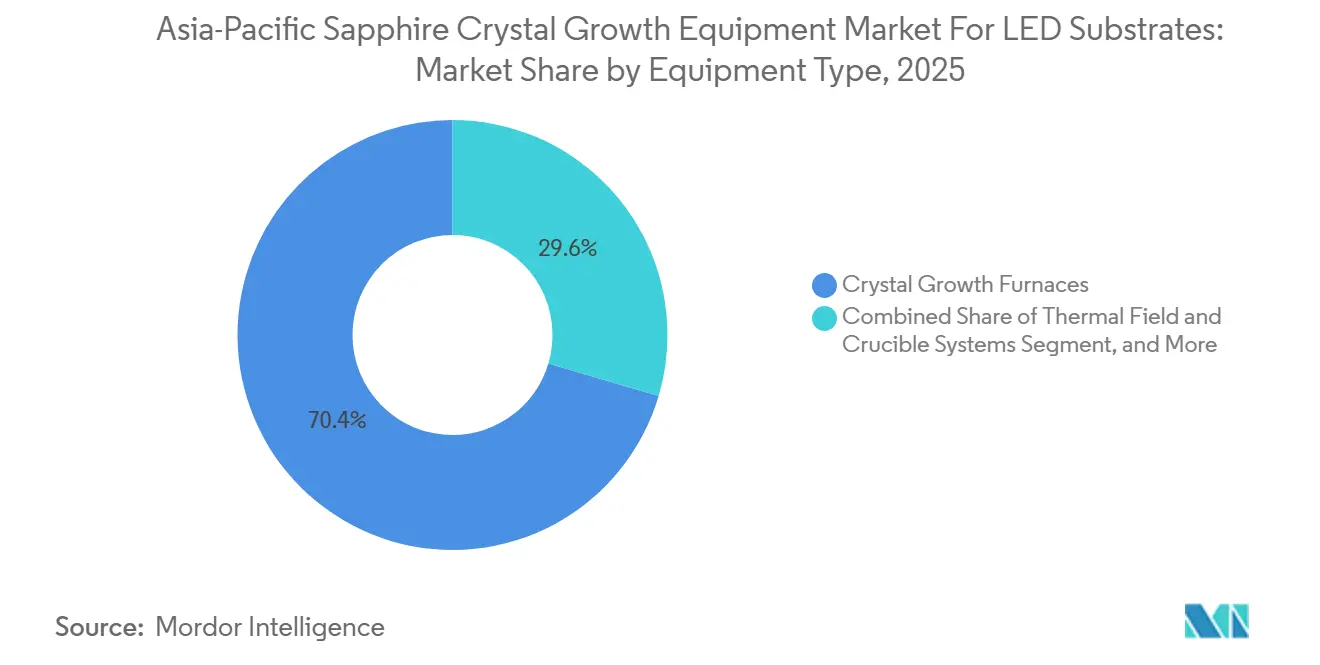

- By equipment type, crystal growth furnaces held 70.42% revenue share of the Asia-Pacific sapphire crystal growth equipment market for LED substrates industry in 2025, while growth automation and process-control systems are projected to expand at a 6.17% CAGR through 2031.

- By growth technology, the Kyropoulos segment led with 58.96% of the APAC sapphire crystal growth equipment market for LED substrates industry share in 2025, whereas the Czochralski segment is forecast to grow at 6.58% CAGR to 2031.

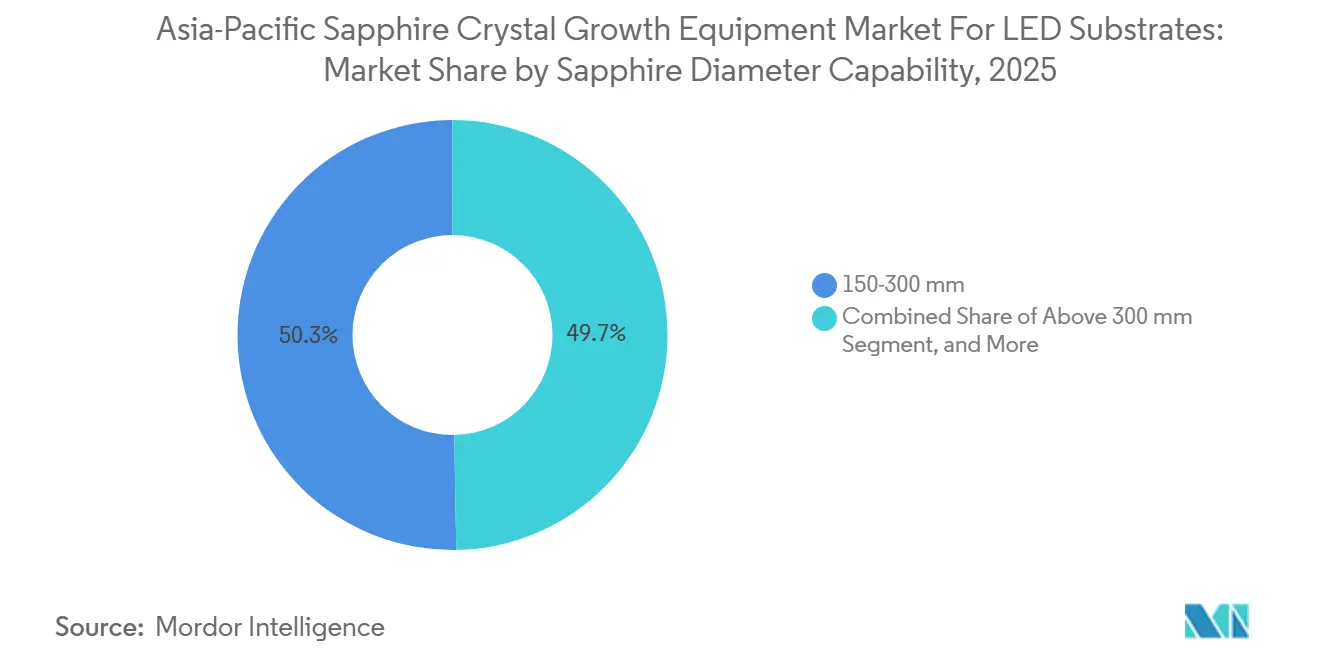

- By diameter capability, 150-300 mm tools accounted for 50.28% of the Asia-Pacific sapphire crystal growth equipment market for LED substrates industry size in 2025, and above-300 mm tools are poised to advance at a 6.72% CAGR over 2026-2031.

- By geography, China commanded 58.37% revenue share in 2025, while Rest of Asia-Pacific is set to record the fastest 6.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on sapphire crystal growth equipment for led substrates market by Mordor Intelligence reflects how these regional layers combine into a single system.

Insights and Trends of Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of mini-LED backlighting capacity in Mainland China | +1.8% | China, spillover to Taiwan and Korea | Medium term (2-4 years) |

| Ongoing migration to 8-inch sapphire wafers in display LED supply chains | +1.2% | China, Taiwan, Japan | Medium term (2-4 years) |

| Government subsidies for domestic LED equipment vendors in China and Taiwan | +1.0% | China and Taiwan | Short term (≤ 2 years) |

| Increasing adoption of micro-LED in wearables and AR devices | +0.9% | Global, early roll-out in China and Korea | Long term (≥ 4 years) |

| Rising demand for high-efficiency lighting in smart-city initiatives | +0.6% | China, Japan, Taiwan, Southeast Asia | Medium term (2-4 years) |

| Localization policies favoring indigenous equipment in Japan | +0.4% | Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Mini-LED Backlighting Capacity in Mainland China

China shipped more than 8 million mini-LED televisions in 2025 and is on track to surpass 10 million units in 2026, roughly one-third of the domestic TV market and more than 70% of global mini-LED TV volumes.[1]“2025 年中国 Mini LED 电视超 800 万台,” Sina Finance, sina.com.cn Each 75-inch mini-LED panel integrates thousands of dies, lifting sapphire substrate demand and pulling furnace purchases forward. HKC’s Liuyang campus, financed at CNY 9 billion (USD 1.24 billion) and designed for more than 500 million mini-LED backlight modules per year, exemplifies the scale driving Kyropoulos and automation orde. Panel majors BOE and CSOT optimized Gen10.5 lines and absorbed LG Display’s Guangzhou Gen8.5 fab to secure over 50 million annual LCD TV panel shipments, reinforcing China’s upstream pull on equipment. RGB mini-LED architectures debuted at CES 2026 demand tighter die placement, which in turn requires higher substrate uniformity, spurring orders for closed-loop process-control options on new furnaces.

Ongoing Migration to 8-Inch Sapphire Wafers in Display LED Supply Chains

Display LED makers are transitioning from 6-inch to 8-inch (200 mm) sapphire to pare cost per die and boost fab throughput. RWTH Aachen and AIXTRON demonstrated nitrogen-polar III-nitride heterostructures on 200 mm sapphire using a 5 × 200 mm Planetary MOCVD reactor in 2025, proving large-wafer epitaxy viability.[2]Mike Cooke, “Nitrogen-polar III-N HFETs on 200 mm Sapphire Substrates,” Semiconductor Today, semiconductor-today.com Larger diameters demand crucibles over 400 mm and precise thermal-field control, driving upgrades that bundle high-resolution vision systems and motorized shield lifts Peking University showed reusable r-plane sapphire that survives three epitaxy-and-exfoliation cycles, hinting at future reductions in net wafer consumption and supporting furnace payback models. However, dislocation density and radial stress rise sharply beyond 300 mm, so fabs often adopt advanced automation to keep yields acceptable.

Government Subsidies for Domestic LED Equipment Vendors in China and Taiwan

Beijing’s Big Fund III earmarked an estimated USD 50 billion in 2025 to close domestic equipment gaps exposed by U.S. export controls. Although logic and memory are headline beneficiaries, sapphire toolmakers qualify through upstream-materials clauses. In Taiwan, the Ministry of Economic Affairs launched a NTD 93 billion (USD 2.9 billion) package in August 2025 that increases export-loan guarantees and offsets capital costs for indigenous tool adoption. Procurement conditions favor “big-lead-small” consortia, aligning local startups with established fabs. Japan’s Economic Security Promotion Act layers similar incentives but ties subsidies to a JPY 30 billion (USD 0.19 billion) investment threshold, nudging foreign vendors toward Japanese joint ventures.[3]Eva Chen, “Japan's Semiconductor Equipment Industry Policies and Guidelines,” Invest Taiwan, investtaiwan.nat.gov.tw

Increasing Adoption of Micro-LED in Wearables and AR Devices

Micro-LED technology is moving from prototypes into high-end wearables and augmented-reality glasses, lured by high luminance and long lifetime relative to OLED. HKC unveiled a 6.67-inch micro-LED prototype in December 2024 rated at 1,000 nits and now runs a dedicated factory in Mianyang that targets commercial ramp in 2026. AR glasses demand luminance above 10,000 nits, which elevates substrate quality requirements; defects that are tolerable in television LEDs create pixel kill in near-eye optics. Laser-assisted mass-transfer trials reached 99.5% die-transfer yields on 2-inch wafers with ±0.3 µm placement accuracy, underscoring the tight tolerances now expected from sapphire wafers. Patterned sapphire substrates have improved light extraction by more than 30%, anchoring process-tool demand for hybrid etch and growth workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity and long payback period for Kyropoulos furnaces | -0.8% | Global, acute in Southeast Asia | Short term (≤ 2 years) |

| Technical challenges in scaling above 300 mm sapphire boules | -0.6% | China, Taiwan, Japan | Medium term (2-4 years) |

| Volatility in LED chip pricing compressing equipment ROI | -0.5% | China, spillover to Taiwan and Korea | Short term (≤ 2 years) |

| Supply-chain disruptions for high-purity alumina crucibles | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity and Long Payback Period for Kyropoulos Furnaces

A modern Kyropoulos furnace capable of 800-1,000 kg boules typically costs more than USD 1 million installed, well above entry-level Czochralski tools. Financing challenges are most acute in Southeast Asia, where state-backed credit lines are limited and private lenders demand higher collateral. LED chip pricing swings worsen the equation; a 10% spot-price hike on back of copper and silver inflation in early 2026 failed to offset volume softness, stretching projected paybacks beyond 36 months. Thermal-stress modeling shows the highest von Mises stress during natural cooldown, which compels additional heater-zone controls that add cost.[4]S. Wang and H. Fang, “Dependence of Thermal Stress Evolution on Power Allocation during Kyropoulos Sapphire Cooling Process,” Applied Thermal Engineering, scipubonline.com Smaller capacity CZ or Edge-Defined systems remain fallback options for greenfield fabs despite lower optical quality.

Technical Challenges in Scaling Above 300 mm Sapphire Boules

Boules wider than 300 mm face higher dislocation density and radial thermal gradients that cut wafer yields unless seeding and cooldown are tightly controlled.[5]Jia Xu et al., “Optimization of the Quality Control Parameters in Sapphire Single Crystal Preparation,” CrystEngComm, rsc.org Taiyuan University used neural-network optimization to keep melt-gap variations within 0.5 mm, yet large-scale automation is not universally deployed. Korea Institute of Industrial Technology’s vision-based system reduces average seeding error to 1.87 mm but still needs operator oversight. Edge defects become prominent when smaller PSS tiles are etched into large wafers, raising scrap risk. Linton Crystal’s 600 mm CZ grower highlights mechanical feasibility, yet sapphire users remain cautious because stress and birefringence escalate with diameter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automation Fuels Incremental Growth

Crystal growth furnaces generated the majority of Asia-Pacific sapphire crystal growth equipment market for LED substrates industry revenue at 70.42% in 2025. Growth automation and process-control add-ons, while a smaller base, are projected to grow 6.17% annually through 2031, outpacing the overall Asia-Pacific sapphire crystal growth equipment market for LED substrates CAGR. Furnaces remain cornerstone assets because they determine boule diameter, optical quality, and throughput. However, operator-dependent seeding still introduces yield loss; fabs therefore allocate new-tool budgets toward software and vision upgrades that stabilize melt convection.

Automation vendors integrate high-resolution cameras, laser rangefinders, and predictive analytics that track melt-gap in real time and adjust shield-lift speed automatically. These upgrades cut cycle-to-cycle variability and help fabs meet micro-LED substrate specifications. Thermal-field and crucible sub-systems face margin squeeze because quartz-crucible prices eased in 2024, but they still anchor aftermarket revenue streams. Suppliers market longer-life insulation and consumables to lock in annuity sales, keeping the Asia-Pacific sapphire crystal growth equipment market for LED substrates industry ecosystem balanced.

By Growth Technology: Kyropoulos Quality Versus Czochralski Speed

The Kyropoulos method accounted for 58.96% of Asia-Pacific sapphire crystal growth equipment market for LED substrates industry revenue in 2025, thanks to low birefringence and uniform optical quality. Czochralski tools are forecast to deliver a 6.58% CAGR through 2031, driven by shorter pull times and tighter diameter control on 200 mm wafers. Edge-Defined Film-Fed Growth and Heat Exchanger Method occupy niche optics and sensor applications where geometry or homogeneity overrides defect density.

Kyropoulos cycles can exceed 18 days for 100 kg boules, elevating energy use and depreciation charges. Continuous improvements in heater-zoning and seed-lift algorithms mitigate but do not erase this drawback. Czochralski adopters leverage computational fluid-dynamics models to narrow the dislocation gap; recent pilot runs report near-Kyropoulos quality when seeds, rotation speed, and melt temperature are optimized. As panel makers shift to 8-inch and above, the Asia-Pacific sapphire crystal growth equipment market for LED substrates industry market size for Czochralski tools could scale quickly, provided suppliers resolve stress-induced cracking on cooldown.

By Sapphire Diameter Capability: Large-Wafer Economics Take Center Stage

Tools rated for 150-300 mm boules captured 50.28% of 2025 revenue, reflecting the installed base of 6-inch and 8-inch production lines. Equipment supporting above-300 mm boules is projected to log a 6.72% CAGR, the highest among diameter classes, as panel makers chase cost-per-die savings on mini-LED and future micro-LED backlights. Although above-300 mm Kyropoulos furnaces offer volume leverage, yields deteriorate without superior automation, so many fabs pilot large-diameter CZ lines first.

RWTH Aachen’s 200 mm nitrogen-polar demo validated large-wafer epitaxy on sapphire, catalyzing tool RFQs for 400 mm crucibles. ECM Greentech furnaces now quote optional high-pressure operation and robotic loading that lower operator exposure to high-temperature zones. Yet radial thermal gradients and dislocation density climb at 300 mm-plus sizes, so repeatable yields hinge on predictive software, another driver that blends this segment with the automation growth narrative.

Geography Analysis

China represented 58.37% of Asia-Pacific sapphire crystal growth equipment market for LED substrates revenue in 2025. Mini-LED television shipments above 8 million units, Big Fund III’s USD 50 billion war chest, and mandates on state-owned adopters anchor near-term tool demand. Domestic suppliers such as NAURA Technology Group and Zhejiang Jingsheng secure orders through preferential financing and localized service, insulating them from certain U.S. export restrictions. HKC’s Liuyang project and the television roadmaps of BOE and CSOT maintain furnace utilization above 85% and prioritize Kyropoulos orders.

Taiwan blends subsidy levers with international partnerships. The NTD 93 billion (USD 2.9 billion) program that began in 2025 boosts export-loan guarantees and reimburses domestic tool purchases, encouraging foundry-equipment startups to collaborate with established panel brands. Taichung’s full LED-streetlight conversion reduces municipal electricity usage by 80 million kWh yearly and illustrates downstream pull for efficient LED substrates. Japan counters with the Economic Security Promotion Act, tying subsidies to JPY 30 billion (USD 0.19 billion) investment thresholds and channeling JPY 1.23 trillion (USD 7.9 billion) toward cutting-edge semiconductor tooling for fiscal 2026.

Rest of Asia-Pacific, including Korea, Southeast Asia, and India, is forecast to post a 6.23% CAGR through 2031, outpacing the overall Asia-Pacific sapphire crystal growth equipment market for LED substrates. Korea leverages its strong semiconductor ecosystem and proximity to display panel makers to attract spillover equipment investment when China faces tightening export controls. Southeast Asian governments court diversified supply chains as a hedge against geopolitical shocks, offering tax holidays and land grants. India’s Production-Linked Incentive scheme for semiconductors may widen to include sapphire upstream if pilot micro-LED programs mature after 2027.

Mordor Intelligence provides coverage of the sapphire crystal growth equipment market for led substrates across other key regional markets. Detailed country-level analysis extends to China, Taiwan, and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The Asia-Pacific sapphire crystal growth equipment market for LED substrates is moderately fragmented. Western incumbents, AIXTRON, GT Advanced Technologies, and Linton Crystal Technologies, compete directly with Chinese suppliers such as NAURA Technology Group, Zhejiang Jingsheng, and Shenyang Crystec. AIXTRON accounted for 71% of global MOCVD revenue for compound semiconductors in 2023, yet its 2024 order intake fell 7%, suggesting slackening LED tool demand. NAURA rose to sixth globally among semiconductor-equipment vendors in March 2025, supported by thin-film and etch portfolios, and now targets crystal-growth automation to close remaining product gaps.

Zhejiang Jingsheng reported RMB 17.577 billion (USD 2.42 billion) revenue in 2024, reflecting vertical integration from furnace design to substrate supply that shields margins when sapphire ASPs fluctuate. Linton Crystal focuses on automation software, recently releasing a melt-gap management update that promises ±0.5 mm precision across full crucible travel. Alpha HPA’s AUD 225 million (USD 148 million) funding for a high-purity alumina plant diversifies crucible powder supply, a strategic move to lower contamination risk and reduce input costs.

Technology differentiation centers on thermal-field stability, energy efficiency, and turnkey automation. XKH Semitech markets an 800-1,000 kg Kyropoulos system with proprietary heat-exchange features that cut energy losses, while ECM Greentech offers high-pressure, robot-enabled furnaces for customers chasing micro-LED qualification. U.S. export controls that added NAURA to the Entity List in 2024 restrict its access to advanced metrology tools, spurring domestic R&D into homegrown process-control software but limiting overseas expansion for now.

Leaders of Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates

AIXTRON SE

NAURA Technology Group Co. Ltd.

Linton Crystal Technologies

GT Advanced Technologies Inc.

Crystal Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Alpha HPA completed a AUD 225 million (USD 148 million) funding round to build a high-purity alumina facility in Gladstone, Queensland.

- February 2026: TSMC announced USD 56 billion capex for 2026, including a USD 17 billion upgrade to its second Kumamoto fab targeting 3 nm production by late 2027.

- January 2026: Taichung City finalized the replacement of 268,000 streetlights with LEDs, saving 80 million kWh annually and generating verified carbon credits.

- December 2025: Japan’s METI nearly quadrupled fiscal-2026 chip and AI subsidies to JPY 1.23 trillion (USD 7.9 billion).

Scope of Report on Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates

The Asia-Pacific Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and Growth Automation and Process Control Systems), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and Czochralski Method), Sapphire Diameter Capability (Up to 150 mm, 150-300 mm, and Above 300 mm), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Crystal Growth Furnaces |

| Thermal Field and Crucible Systems |

| Growth Automation and Process Control Systems |

| Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) |

| Heat Exchanger Method |

| Czochralski Method |

| Upto 150 mm |

| 150-300 mm |

| Above 300 mm |

| China |

| Taiwan |

| Japan |

| Rest of the Asia-Pacific |

| By Equipment Type | Crystal Growth Furnaces |

| Thermal Field and Crucible Systems | |

| Growth Automation and Process Control Systems | |

| By Growth Technology | Kyropoulos Method |

| Edge-Defined Film-Fed Growth (EFG) | |

| Heat Exchanger Method | |

| Czochralski Method | |

| By Sapphire Diameter Capability | Upto 150 mm |

| 150-300 mm | |

| Above 300 mm | |

| By Geography | China |

| Taiwan | |

| Japan | |

| Rest of the Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 value forecast for Asia-Pacific sapphire crystal growth equipment?

The market is projected to reach USD 170.63 million in 2026, on its way to USD 227.06 million by 2031.

Which equipment segment is expanding the fastest?

Growth automation and process-control systems are expected to post a 6.17% CAGR through 2031, the fastest among all equipment types.

Why are 8-inch sapphire wafers important?

Moving to 8-inch substrates lowers cost per die and raises throughput, supporting the economics of mini-LED and future micro-LED displays.

How much market share did China hold in 2025?

China accounted for 58.37% of regional equipment revenue in 2025.

Which growth technology leads today?

The Kyropoulos method led with 58.96% revenue share in 2025 due to superior optical quality.

What hampers rapid furnace adoption in Southeast Asia?

High upfront costs for Kyropoulos tools and limited concessionary financing extend payback periods for new entrants.

Page last updated on: