Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

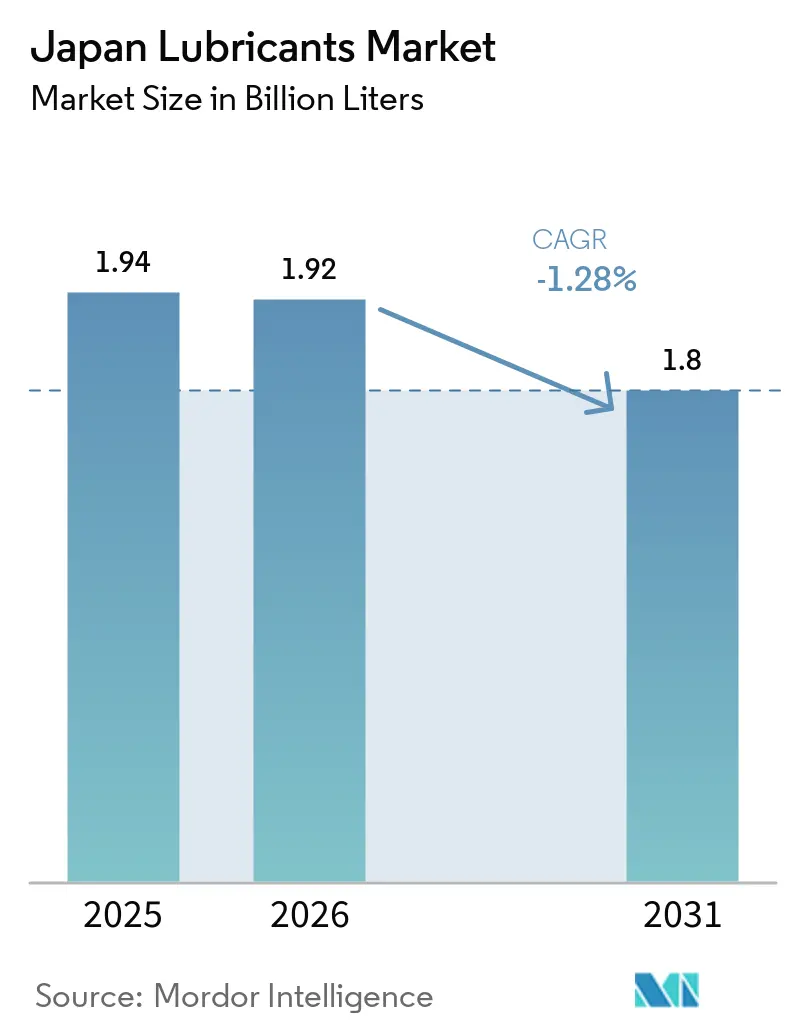

| Base Year Market Size (2025) | 1.94 Billion liters |

| Market Volume (2026) | 1.92 Billion liters |

| Market Volume (2031) | 1.8 Billion liters |

| Growth Rate (2026 - 2031) | -1.28% CAGR |

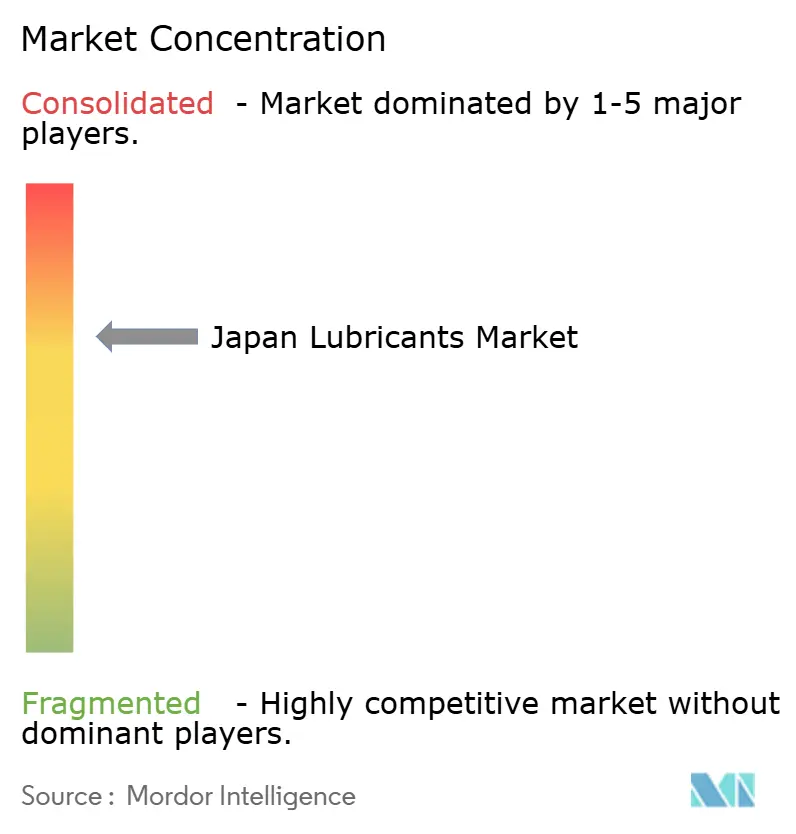

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Lubricants Market Analysis by Mordor Intelligence

The Japan Lubricants Market size was valued at 1.94 Billion liters in 2025 and estimated to decline from 1.92 Billion liters in 2026 to reach 1.8 Billion liters by 2031, at a CAGR of -1.28% during the forecast period (2026-2031). Hybrid electric vehicles (HEVs) currently represent 60% of new vehicle registrations. Their extended oil-change intervals reduce per-vehicle oil consumption, even as they dominate the national sales mix. Gasoline demand is expected to decline by approximately 2–2.5% annually through 2030, exerting structural pressure on automotive engine oil volumes. While mature industrial output limits overall market growth, opportunities exist in premium dielectric immersion-cooling fluids for hyperscale data centers and bio-based lubricants that align with corporate net-zero objectives. Increased merger and acquisition (M&A) activity, such as Idemitsu’s planned 2024 integration of Cosmo Oil Lubricants and ENEOS’s acquisitions in international additives and metalworking fluids, has intensified competition and driven portfolio shifts toward higher-margin specialty segments.

Key Report Takeaways

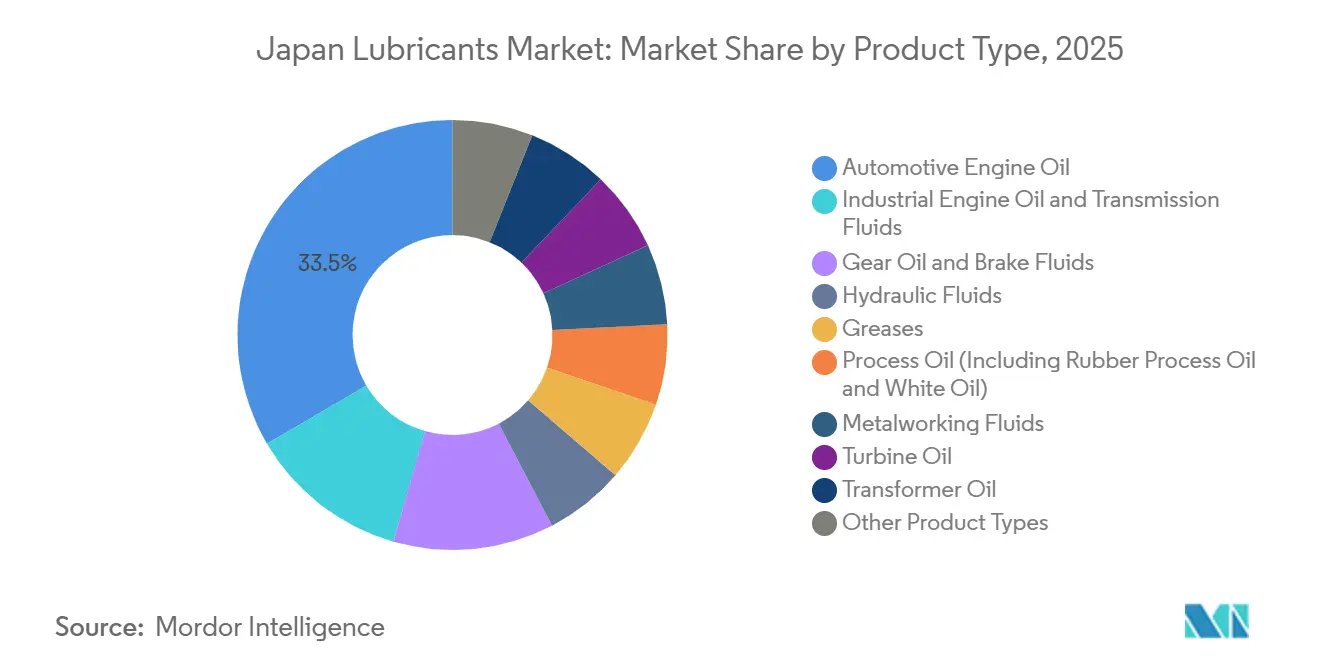

- By product type, automotive engine oil led with 33.45% of the Japan lubricants market share in 2025, while industrial engine oil is projected to post the fastest 0.04% CAGR through 2031.

- By base stock type, mineral oil-based lubricants commanded 64.12% of the Japan lubricants market share in 2025, whereas bio-based formulations are forecast to expand at a 0.05% CAGR over the period.

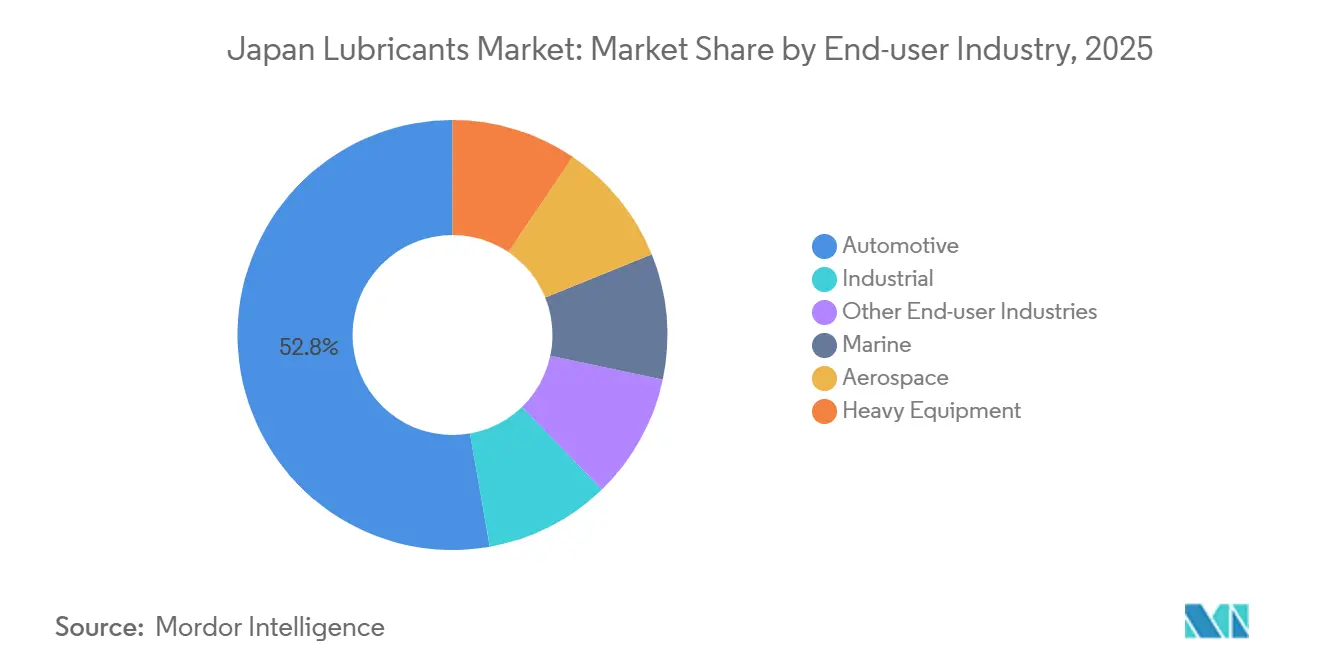

- By end-user industry, the automotive segment accounted for 52.78% of the Japan lubricants market share in 2025, yet the industrial segment is advancing at a 0.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Industrial Automation Boosting Hydraulic and Gear Lubes | +0.3% | National, with concentration in Aichi, Kanagawa, and Osaka manufacturing hubs | Medium term (2-4 years) |

| Corporate Net-Zero Targets Driving Bio-based Lubricants | +0.2% | National, led by Tokyo-headquartered refiners and automotive OEMs | Long term (≥ 4 years) |

| Data-center Immersion-Cooling Fluids Adoption | +0.1% | National, early adopters in Tokyo, Osaka, and Fukuoka data-center clusters | Short term (≤ 2 years) |

| Circular-Economy Policies Promoting Re-refined Oils | +0.1% | National, contingent on METI and Ministry of Environment subsidy continuation | Long term (≥ 4 years) |

| OEM Shift to Ultra-low Viscosity Oils for Fuel Economy | +0.2% | National, driven by Toyota, Nissan, Honda specifications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Industrial Automation Boosting Hydraulic and Gear Lubes

The demand for premium hydraulic fluids and gear oils remains steady in smart-factory hubs like Aichi and Osaka, where equipment upgrades require compliance with the 2024 JCMAS P041 and P042 revisions[1]Japan Construction Machinery Manufacturers Association, “Revised Hydraulic Fluid Standards JCMAS P041/P042,” jcma.or.jp. Enhanced viscosity stability and extreme-pressure thresholds are driving the preference for synthetic base stocks, increasing value even as volumes stabilize. Kyodo Yushi’s expansion of specialty grease exports in 2025 highlights the global demand for Japanese formulations. Yushiro Chemical’s JPY 52.34 billion (approx. USD 350.68 million) revenue in 2025 reflects the continued importance of metalworking oils in precision manufacturing. Stricter cleanliness (ISO 4406) and seal-compatibility standards now act as barriers to entry, favoring established players with technical service capabilities.

Corporate Net-Zero Targets Driving Bio-based Lubricants

Refiners are accelerating biomass initiatives to align with Japan’s 2050 carbon-neutral goals. ENEOS introduced a 100% plant-based engine oil, while Idemitsu’s GX series incorporates biomass-based stocks into mainstream passenger-car oils. The Eco Mark 2.7 criteria, introduced in April 2025, tightened biodegradation and toxicity standards, pushing R&D efforts toward high-performance esters. Green Science Alliance’s use of waste cooking oil highlights the growing interest in circular feedstocks. DIC’s algae-derived extreme-pressure additive reduces CO₂ emissions by 5% compared to crop-oil alternatives and significantly lowers land and water usage. However, premium pricing, which is 20-40% higher than mineral-based equivalents, limits adoption outside forestry and marine applications. Government procurement policies are increasingly rewarding low-carbon products.

Data-center Immersion-Cooling Fluids Adoption

Cosmo Energy launched its Cosmo Thermal Fluid in January 2026, targeting hyperscale data center operators aiming to reduce energy costs and optimize floor-space usage. ITOCHU’s December 2025 agreement with Castrol and its IT services division is expediting the commercialization of Castrol ON fluids. Although the market volume remains small, unit values are five to ten times higher than conventional hydraulic oils, making this niche an attractive counterbalance to declining engine oil revenues. Early trials in Tokyo and Osaka have demonstrated 20-30% improvements in power-usage effectiveness, while dielectric-strength requirements limit low-cost competition. Suppliers with expertise in thermal management can secure long-term service contracts tied to fluid maintenance and analytics.

Circular-Economy Policies Promoting Re-refined Oils

The Ministry of Environment supported Idemitsu’s 2024–2025 pilot project to demonstrate the feasibility of Group III re-refining. However, cost studies estimate production expenses at JPY 228-287 (approx. USD 1.53-USD 1.54) per liter, significantly higher than the JPY 150 (approx. USD 1) per liter price for virgin Group III, making the business model reliant on subsidies. A February 2026 METI program now offsets quality-assurance costs for small and medium-sized blenders transitioning to industrial grades. Industry organizations, such as the Petroleum Association of Japan, have formed carbon-neutral committees, indicating that circular feedstocks will be essential for Scope-3 compliance, even though near-term volumes are expected to remain modest.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature Industrial Output Limiting Volume Expansion | -0.4% | National, reflecting stagnant manufacturing capacity utilization | Long term (≥ 4 years) |

| OEM Long-drain Intervals Reduce Consumption per Vehicle | -0.5% | National, accelerated by HEV dominance and synthetic oil adoption | Medium term (2-4 years) |

| Low-cost Imports of Re-refined Oils | -0.2% | National, concentrated in commodity industrial grades | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mature Industrial Output Limiting Volume Expansion

Japan’s manufacturing capacity utilization has remained near historical averages since 2024, with major sectors such as steel and petrochemicals showing limited interest in greenfield capacity expansion. Auto-parts shipments totaled JPY 36.9 trillion (approx. USD 261 billion) in 2023, with no clear growth trajectory through 2030[2]Japan Automobile Parts Industries Association, “Auto Parts Shipment Statistics 2023,” japia.or.jp. Power-generation lubricant demand remains flat as thermal power units are retired in favor of renewable energy sources, which require smaller fluid volumes. Metalworking fluids face a maturing end market, even as quality requirements increase, creating a value-over-volume scenario for suppliers capable of differentiation through additives and services.

OEM Long-drain Intervals Reduce Consumption per Vehicle

The 2024 JASO GLV-2 specification supports 0W-16 and 0W-20 grades, which can last up to 15,000 km or 12 months, reducing per-vehicle engine oil consumption by approximately 10-15% over the vehicle’s lifetime. Hybrid electric vehicles (HEVs), now accounting for 60% of registrations, operate combustion engines intermittently, further extending drain intervals. Toyota, Nissan, and Honda already recommend GLV-1 0W-8 and 0W-12 oils for several hybrid models, reinforcing the downward trend in volume. Battery electric vehicles, which do not require engine oil, signal a deeper long-term contraction in demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Dominate Despite Structural Decline

Automotive engine oil accounted for 33.45% of the 2025 volume, remaining a cornerstone of the Japan lubricants market, even as HEVs and extended drain intervals reduce liters per vehicle. Industrial engine oil is the only sub-category expected to grow, with a projected 0.04% CAGR through 2031, supported by consistent demand from power plants and marine propulsion. Transmission and gear oils benefit from the increasing adoption of CVTs, which require specialized friction-modifier packages, while brake fluids remain stable due to Japan’s stringent safety inspection requirements. Hydraulic fluids now need to meet JCMAS P041/P042 standards for wider operating temperature ranges and enhanced EP performance, driving demand for synthetic blends with higher margins. Specialty products like metalworking and turbine oils maintain steady usage in precision-machining clusters, supported by suppliers such as Yushiro Chemical and ENEOS, which provide on-site fluid management services. Greases continue to serve robotics and industrial automation components, with Kyodo Yushi’s lithium-complex formulations gaining strong OEM acceptance. Overall, the shift toward higher-specification grades helps cushion the Japan lubricants market against outright volume loss.

By Base Stock Type: Mineral Oil-Based Lubricants Retain Majority Despite Bio-based Momentum

Mineral oil-based lubricants accounted for 64.12% of the 2025 volume, reflecting their cost advantage in the Japan lubricants market. Synthetic grades are preferred for ultra-low-viscosity engine oils and high-load hydraulic systems, where oxidation resistance and cold-flow properties justify their premium pricing. Semi-synthetic lubricants are catering to price-sensitive passenger car applications. Bio-based lubricants are the fastest-growing segment, with a 0.05% CAGR projected through 2031, driven by Eco Mark incentives and net-zero procurement policies. Suppliers are blending PAO or ester co-stocks with biomass-derived oils to address thermal stability challenges, while additive innovators like DIC are exploring algae feedstocks to avoid food-versus-fuel conflicts. Re-refined oils remain a niche due to their higher cost base of JPY 228-287 (approx. USD 1.53-USD 1.54) per liter compared to approximately JPY 150 (approx. USD 1) per liter for virgin Group III oils, highlighting the scale economy challenges faced by domestic recyclers.

By End-user Industry: Automotive Dominance Erodes as Industrial Stabilizes

The automotive industry accounted for 52.78% of the 2025 demand, continuing to anchor the Japan lubricants market. However, its share is declining due to HEV penetration and kei-car downsizing, which reduces sump volumes. Commercial vehicle demand remains relatively stable, supported by higher annual mileage and diesel prevalence, though electrification in last-mile delivery fleets may impact this segment post-2030. Two-wheeler lubricant consumption has leveled off, aligning with urban commuting trends. The industrial segment is projected to grow modestly at a 0.03% CAGR through 2031, driven by consistent demand for metalworking fluids in precision manufacturing and baseline turbine and transformer oil usage in power generation. Marine and aerospace sub-segments remain niche but strategic, with coastal shipping and fisheries sustaining demand for trunk-piston and cylinder oils, while aviation turbine oils adhere to stringent MIL-PRF-23699 specifications, favoring synthetic formulations. Heavy-equipment hydraulics follow the construction cycle, with IoT-enabled oil-condition monitoring solutions from Komatsu and Hitachi extending drain intervals and supporting demand for premium, sensor-compatible fluids.

Geography Analysis

Japan lacks formal sub-national market statistics, but regional industrial clusters significantly influence lubricant usage patterns. The Kanto corridor, encompassing Tokyo, Kanagawa, Saitama, and Chiba, represents the largest demand center, driven by assembly plants, data centers, and logistics hubs. This region favors ultra-low-viscosity passenger car oils, immersion-cooling fluids, and warehouse-equipment hydraulics. Cosmo Thermal Fluid trials in Tokyo and Osaka highlight early adoption among hyperscale data-center operators seeking higher rack densities and improved power-usage effectiveness.

The Chubu region, anchored by Toyota City and Nagoya, is a hub for engine oil, transmission fluid, and metalworking fluid consumption due to its concentration of automotive assembly, machining, and export logistics. Yushiro Chemical’s export activities through Nagoya emphasize the region’s dual role as a production and distribution hub. Kansai, including Osaka and Hyogo prefectures, supports demand for marine and industrial engine oils, while Kyoto’s precision-tool sector drives metalworking fluid usage.

Coastal prefectures such as Hokkaido, Niigata, and Okinawa contribute steady volumes of marine lubricants for fishing and coastal transport fleets. Japan’s 19 coastal refineries, with a combined crude throughput of 3.11 million barrels per day, ensure efficient base-oil supply for domestic blending plants. Nationally, 27,009 service stations in 2025 form a consolidating retail channel for automotive lubricants, with many transitioning to self-service formats and diversifying convenience offerings, subtly reshaping product-mix dynamics.

Competitive Landscape

ENEOS, Idemitsu, Shell plc, Exxon Mobil, and Cosmo Energy collectively accounted for an estimated 77% of the 2025 domestic volume, indicating a moderately concentrated market structure. Idemitsu’s 2023-2024 consolidation eliminated a competitor, enhancing scale efficiencies in procurement and logistics. ENEOS has pursued an international M&A strategy, acquiring Lawson Oil, Lubricant Consult, Fuchs Lubricants Canada, Zeeland Chemicals, and Quaker Houghton’s European metalworking division between 2024 and 2025, strengthening its specialty-fluid expertise and global OEM relationships.

International players such as Shell, BP (Castrol), ExxonMobil, and TotalEnergies focus on premium synthetics and niche segments like immersion-cooling fluids. BP’s Castrol brand gained traction through a 2025 MoU with ITOCHU Techno-Solutions, providing enterprise channel access for data-center applications. Domestic specialists, including Kyodo Yushi (greases), Yushiro Chemical (metalworking fluids), and Japan Sun Oil (hydraulic oils), defend their niches through OEM approvals and robust field-service programs. Innovations such as Green Science Alliance’s waste-oil-to-bio-lube technology and nanotech-additive startups targeting friction reduction represent an emerging pipeline monitored by larger incumbents.

Regulatory compliance is becoming more demanding. JALOS guidance aligned with 2023-2024 Industrial Safety and Health Law amendments now requires expanded chemical-substance disclosures, increasing operational overheads that favor companies with dedicated regulatory teams. IoT-based condition-monitoring solutions, such as Komatsu’s KOMTRAX and Hitachi’s ConSite OIL, generate recurring revenue streams while extending fluid life, prompting suppliers to adopt service-driven business models to counter declining volume sales.

Japan Lubricants Industry Leaders

ENEOS Corporation

Shell plc

COSMO ENERGY HOLDINGS Co., Ltd.

Idemitsu Kosan Co., Ltd.

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: COSMO ENERGY HOLDINGS Co., Ltd., through its subsidiary Cosmo Oil Lubricants, launched Cosmo Thermal Fluid. This high-performance, single-phase dielectric immersion cooling medium was designed to manage the significant heat produced by high-performance servers in hyperscale data centers, especially those handling intensive generative AI workloads.

- January 2026: PETRONAS Lubricants International (PLI) launched its first JASO-certified engine oils in Japan at the Tokyo Auto Salon. The range, including the PETRONAS Urania 5000 JASO DL-1 0W-30, is designed for high-efficiency engines and featured StrongTech technology to enhance durability and improve fuel economy by up to 19%.

Japan Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The Japan lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the volume of the Japan lubricants market?

The Japan lubricants market stands at 1.92 billion liters in 2026 and is on track to decline to 1.80 billion liters by 2031.

Why is lubricant demand shrinking in Japan?

HEV dominance, longer drain intervals, fuel-economy regulations, and flat industrial output are steadily reducing annual lubricant volumes.

Which product type offers growth potential through 2031?

Industrial engine oil shows marginal growth with a 0.04% CAGR through 2031, thanks to stable demand in power generation and marine propulsion.

How fast are bio-based lubricants expanding through 2031?

Bio-based lubricants are projected to advance at a 0.05% CAGR through 2031 as refiners pivot to plant-derived base stocks and Eco Mark incentives.

Page last updated on: