Japan Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

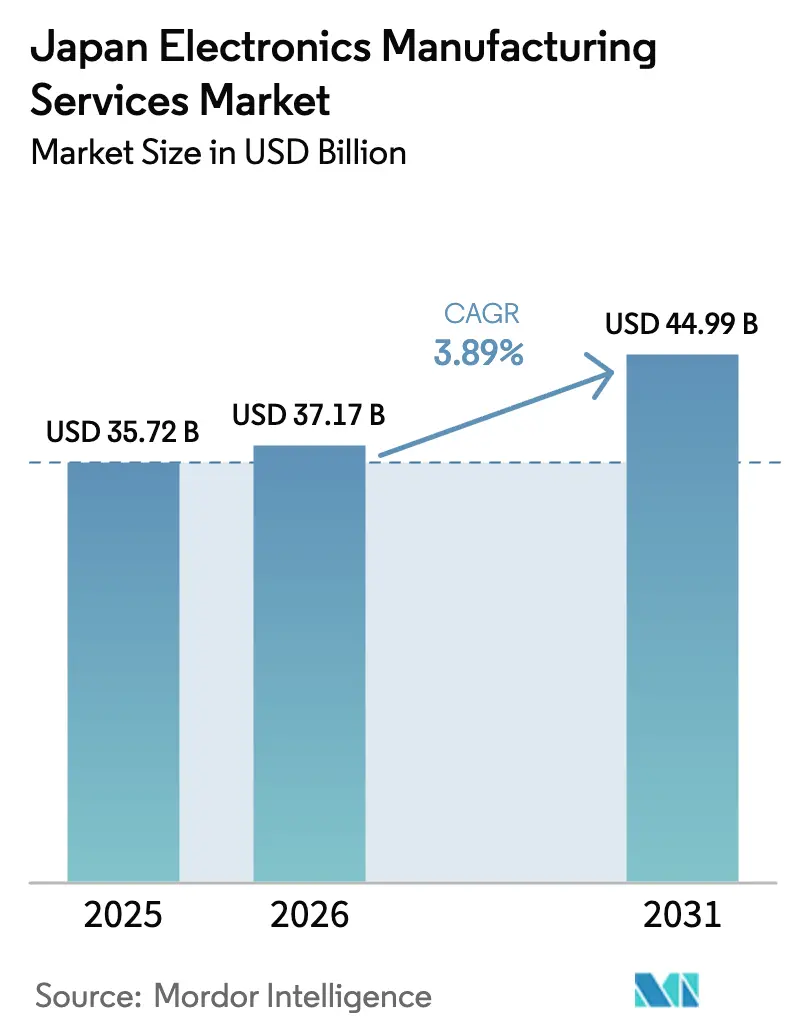

| Base Year Market Size (2025) | USD 35.72 Billion |

| Market Size (2026) | USD 37.17 Billion |

| Market Size (2031) | USD 44.99 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

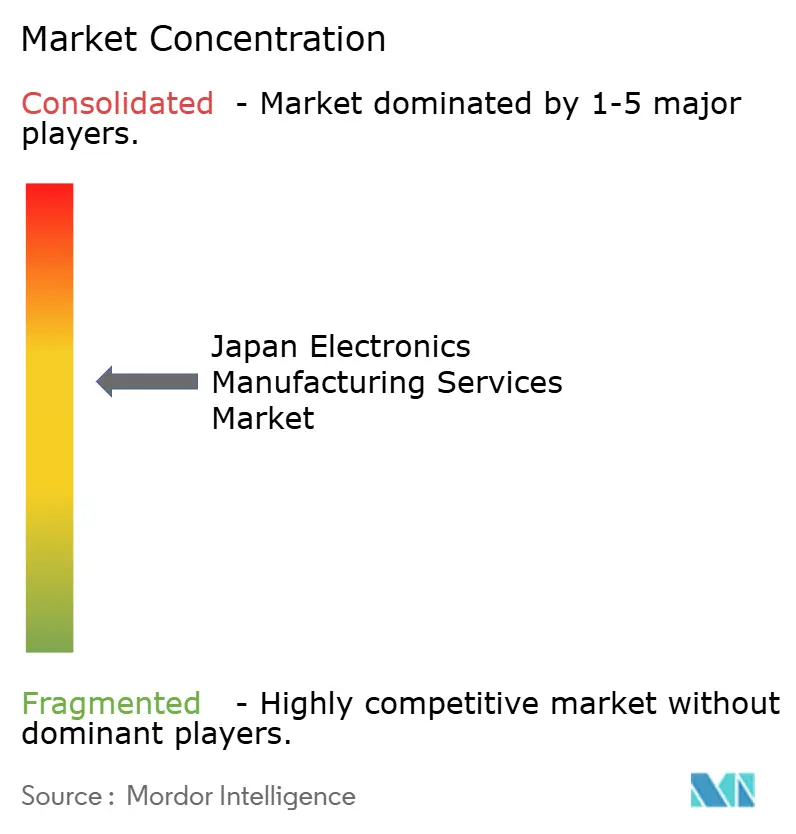

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Japan Electronics Manufacturing Services Market was valued at USD 35.72 billion in 2025 and expected to grow from USD 37.17 billion in 2026 to reach USD 44.99 billion by 2031, at a CAGR of 3.89% during the forecast period (2026-2031). Demand pivots from mass-market consumer devices toward automotive electrification, high-density medical equipment, and industrial IoT hardware are redefining production priorities. Government incentives worth JPY 2 trillion (USD 12.8 billion) are steering critical semiconductor and advanced packaging lines back onshore, even as 20 to 30% higher electricity tariffs compress margins. Tier 1 automotive suppliers are pouring capital into silicon carbide power modules that require turnkey box-build capabilities, while medical OEMs facing stringent ISO 13485 audits are turning to certified partners to accelerate approvals. Together, these shifts underpin a gradual relocation of complex assemblies to domestic EMS facilities and reinforce the medium-term growth outlook for the Japan electronics manufacturing services market.

Key Report Takeaways

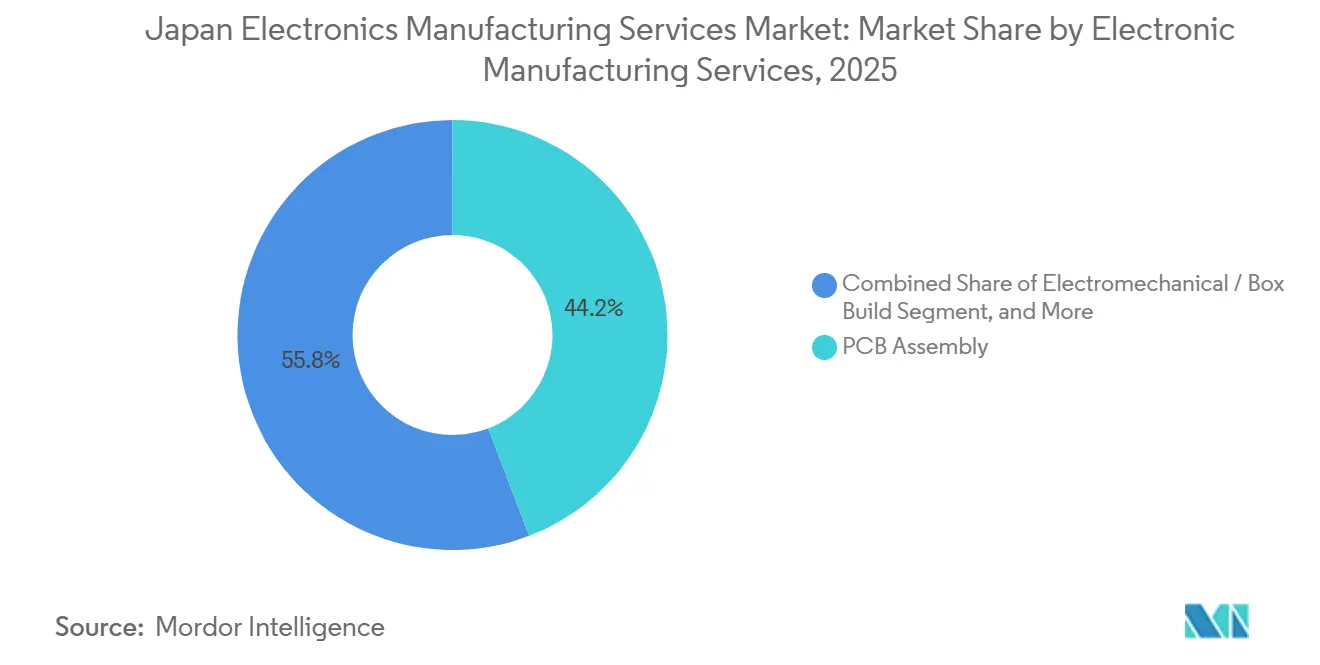

- By electronic manufacturing services, electromechanical assembly/box build services are forecast to expand at a 4.63% CAGR through 2031, outpacing the 44.19% share held by PCB assembly in 2025.

- By business model, contract manufacturing accounted for 62.46% of the Japan electronics manufacturing services market share in 2025, while hybrid / turnkey / other business models are set to climb at a 4.46% CAGR to 2031.

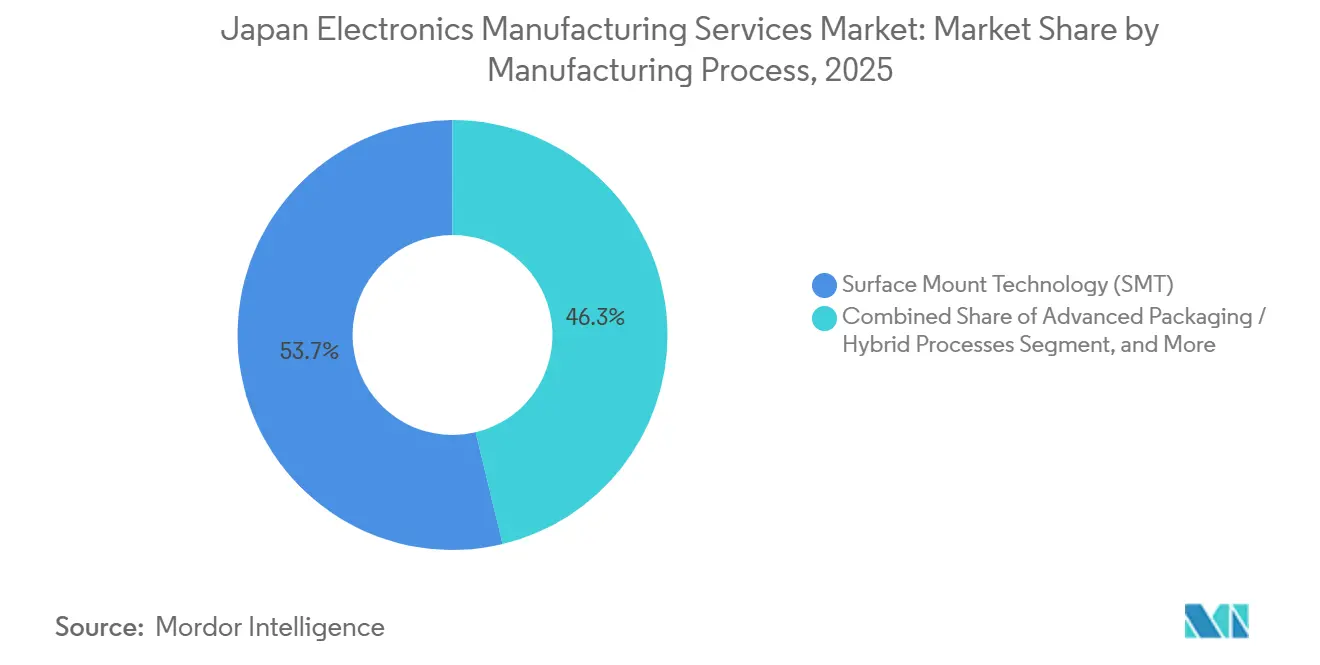

- By manufacturing process, advanced packaging/hybrid processes had the fastest trajectory, with a 4.87% CAGR through 2031, compared with the 53.74% share commanded by surface mount technology in 2025.

- By end-user, automotive is projected to grow at a 4.38% CAGR through 2031, while the consumer electronics segment accounted for 36.37% market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Figures recorded within Japan feed into a worldwide estimate while studying the global industry. Mordor Intelligence's electronics manufacturing services market size captures this aggregation.

Japan Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Automotive Electronics for EV/ADAS | +1.2% | Aichi, Kanagawa, Hiroshima | Medium term (2-4 years) |

| Increased Outsourcing by Japanese OEMs to Reduce Fixed Costs | +0.9% | National, spillover to ASEAN | Short term (≤ 2 years) |

| Demand for Miniaturized High-Density PCBs Outpacing In-House Capacity | +0.8% | Tokyo-Yokohama, Osaka corridors | Medium term (2-4 years) |

| Rising Turnkey Service Adoption to Shorten Time-to-Market | +0.7% | National | Short term (≤ 2 years) |

| Government Incentives for Domestic EMS Relocation | +0.5% | Kumamoto, Hokkaido, Tohoku | Long term (≥ 4 years) |

| Growth of Medical Device Contract Manufacturing for Elderly Care | +0.4% | Kanto, Kansai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Automotive Electronics for EV/ADAS

Electric vehicle battery management, ADAS sensor fusion, and software-defined architectures are generating unprecedented electronic content per vehicle. The Honda and Nissan merger earmarked USD 50 billion for joint electrification, channeling large-volume inverter and domain controller work to ISO/TS-certified EMS partners.[1]Honda Motor Co., Ltd., “Honda-Nissan Merger Announcement,” Honda.com DENSO’s USD 4.9 billion investment in silicon carbide devices underscores the need for power modules that integrate PCB, mechanical, and thermal components within sealed housings. The Ministry of Economy, Trade and Industry expects the value of electronics per car to triple to USD 1,800 by 2030, cementing automotive demand as the primary driver of the Japan electronics manufacturing services market.

Increased Outsourcing by Japanese OEMs to Reduce Fixed Costs

Rising electricity and labor expenses are dismantling the vertically integrated model that once characterized Japanese manufacturing. Sharp’s shuttering of its Sakai LCD plant and Kyocera’s sale of its handset business symbolize the retreat from capital-heavy, low-margin lines. A Japan Bank for International Cooperation survey found that 62% of manufacturers plan to increase outsourcing or offshore production within 3 years. [2]Japan Bank for International Cooperation, “Overseas Production Survey,” Jbic.go.jp This wave of restructuring is reallocating mid-volume, high-mix assemblies to qualified EMS vendors, sustaining growth for the Japan electronics manufacturing services market.

Demand for Miniaturized High-Density PCBs Outpacing In-House Capacity

Twenty-five-micron line widths and 124-layer stacks developed by OKI Printed Circuit underline technical thresholds that captive OEM shops struggle to meet. [3]OKI Printed Circuit, “124-Layer PCB Development,” Okiprintedcircuit.com Meiko Electronics’ HDI capacity expansion and Fujitsu’s breakthroughs in semi-additive processes demonstrate that only specialized EMS houses possess the capital and process control required for sub-20-micron geometries. [4]Meiko Electronics Co., Ltd., “HDI Production Expansion,” Meiko-elec.com As wearable, IoT, and mm-wave applications proliferate, this capability gap channels boards and module builds toward the Japan electronics manufacturing services market.

Rising Turnkey Service Adoption to Shorten Time-to-Market

Product life cycles have compressed to 12-18 months, forcing OEMs to bundle design, procurement, assembly, and logistics under one roof. SIIX’s addition of embedded software teams and Kaga Electronics’ purchase of a power-electronics design boutique exemplify EMS players capturing upstream value. The 2024 METI white paper ranked time-to-market just behind product quality as a global success factor, accelerating uptake of full-service contracting across the Japan electronics manufacturing services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Production Volumes of Legacy Consumer Electronics | -0.8% | Osaka, Shizuoka | Short term (≤ 2 years) |

| Rising Domestic Labor and Utility Costs | -0.6% | Metropolitan areas | Medium term (2-4 years) |

| Stringent JIS and ISO13485 Compliance Extending Qualification Lead-Times | -0.3% | National | Medium term (2-4 years) |

| Limited Availability of Skilled SMT Engineers in Rural Regions | -0.2% | Tohoku, Hokkaido, Shikoku | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Production Volumes of Legacy Consumer Electronics

A multi-year slide in domestic TV, camera, and audio lines culminated in Sharp’s LCD exit and Sony’s smartphone shift to Thailand, leaving idle capacity in long-standing EMS factories. JEITA recorded a 7.2% fall in output value for 2024, extending a decline that has persisted since 2020 and trimming baseline demand for the Japan electronics manufacturing services market. Panasonic’s 2024 withdrawal from the TV segment removed another anchor customer, prompting several mid-tier EMS providers to repurpose unused lines for automotive and medical builds. The swift pivot toward higher-reliability applications raises qualification costs, but it also preserves jobs in regions most exposed to legacy product contraction.

Rising Domestic Labor and Utility Costs

Industrial power rates climbed to JPY 18.5 per kilowatt-hour in 2024, while manufacturing wages jumped 4.3% year on year. The Daiwa Institute warns of a 350,000-worker shortfall by 2030, forcing EMS providers either to automate or relocate simpler assemblies offshore. Higher LNG import dependence after nuclear shutdowns magnifies electricity volatility, driving some factories to add rooftop solar and battery storage to buffer peak tariffs. These pressures shave competitiveness and slow expansion plans within the Japan electronics manufacturing services market, particularly for operators without the scale to invest in energy-efficient equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Electronic Manufacturing Services: Electromechanical Assemblies Accelerate with Vehicle Electrification

Electromechanical assembly is expected to capture a 4.63% CAGR through 2031 as OEMs demand sealed inverters, LiDAR, and battery modules incorporating boards, cooling plates, and housings. DENSO’s silicon carbide inverter stack typifies complex builds that require environmental stress screening and functional safety validation. PCB assembly still accounted for 44.19% of 2025 revenue, but price competition under turnkey contracts is narrowing margins. Cable and testing services are gaining traction in medical device builds that require 100% traceability to meet PMDA audit requirements.

The Japan electronics manufacturing services market relies on prototyping teams to iterate solid-state LiDAR and next-generation BMS designs, keeping innovation cycles short. Engineering consulting, once sold separately, now anchors turnkey bids that bundle design for manufacturability, failure analysis, and logistics support. Service diversification enables providers to capture more value per program and defend against pure-play board assembly price wars across the Japan electronics manufacturing services market.

By Business Model: Hybrid and Turnkey Contracts Capture Design Authority

Contract manufacturing retained 62.46% of 2025 revenue, yet hybrid/turnkey/other business Models deals are set to climb at 4.46% CAGR as OEMs trade hardware control for speed. Small and mid-cap medical and industrial firms with limited R&D staffs outsource embedded firmware, certification, and supply chain functions. Kaga Electronics’ acquisition of power-electronics IP and SIIX’s software practice illustrate how EMS companies step into roles once managed by OEMs.

Original design manufacturing remains niche in Japan due to perceived IP leakage risks, but it is gaining ground in commoditized IoT sensors where differentiation shifts to cloud analytics. The Japan electronics manufacturing services market thus evolves toward multi-tier engagement models, enabling providers to offer configurable packages ranging from simple build-to-print to full product realization.

By Manufacturing Process: Advanced Packaging Outpaces Conventional SMT

Surface mount technology accounted for 53.74% of 2025 revenue, yet advanced packaging / hybrid processes are growing at a 4.87% CAGR as chips disaggregate into chiplets. The Semiconductor Energy Laboratory advanced wafer-level packaging for HBM stacks while ASMPT logged strong tool sales for Japanese lines, underlining a national drive to reclaim packaging leadership.

Hybrid lines that marry SMT and through-hole remain indispensable in industrial drives and medical pumps, where legacy components persist. Investments exceeding USD 50 million per line restrict entry and consolidate high-end capacity among well-capitalized groups. This differentiation supports premium pricing within the Japan electronics manufacturing services market for advanced packaging builds.

By End-User: Automotive Leads Growth as Consumer Electronics Contract

Automotive is projected to grow at a 4.38% CAGR, driven by joint electrification spending from Honda and Nissan and by ADAS sensor proliferation. Module commonality will raise order volumes for EMS plants with IATF 16949 certification, propelling the Japan electronics manufacturing services market. Consumer electronics retained 36.37% of the 2025 value but face waning domestic demand and offshoring.

Medical devices show double-digit momentum as Terumo invests USD 100 million in ISO 13485 cleanrooms and Nihon Kohden secures PMDA approval for connected AEDs. Industrial automation, driven by aging workforce labor substitution, and communication infrastructure tie up the remaining mix, maintaining baseline demand diversity in the Japan electronics manufacturing services market.

Geography Analysis

The Kanto-Chubu corridor accounts for more than half of national EMS revenue, buoyed by automotive and industrial OEM clusters in Aichi and Kanagawa. Facilities here benefit from dense supplier networks, skilled labor pools, and proximity to port and airport logistics, sustaining the Japan EMS market. The Kansai region, including Osaka and Kyoto, still hosts legacy consumer electronics lines but is diversifying into medical and robotics assemblies to offset flat TV volumes. Recent municipal tax incentives encourage mid-tier EMS firms to repurpose idle cleanrooms for health-tech prototyping.

Tohoku and Hokkaido are emerging as relocation hubs under the JPY 2 trillion (USD 12.8 billion) subsidy program earmarked for semiconductor back-end and advanced packaging. Companies opening greenfield sites in Kumamoto leverage lower land costs and newly trained technicians graduating from government-funded mechatronics programs. However, limited surface-mount talent in rural prefectures requires a heavy reliance on automation to meet automotive zero-defect targets.

Western Honshu and Shikoku host a scattering of specialized plants focusing on power electronics and high-voltage connectors for electric drivelines. Nidec’s Shiga complex consolidates three older factories into a single smart-factory blueprint, slashing internal logistics time by 30%. Coastal sites maximize renewable energy capacity to mitigate high grid tariffs, support ESG requirements from global OEMs, and preserve competitiveness in the Japan electronics manufacturing services market.

Mordor Intelligence evaluates the electronics manufacturing services market across all key regional markets, including Europe, Asia, and North America, with deeper country-level insights covering China, Taiwan, United Kingdom, United States, Vietnam, and India.

Competitive Landscape

The Japan electronics manufacturing services market has a moderate concentration profile. Global giants such as Foxconn, Flex, and Jabil devote their Japanese fabs to multinational customers, while domestic champions SIIX, Kyocera, and Sumitronics leverage cultural affinity, language advantage, and fast engineering turnaround to anchor key automotive and industrial accounts. Mid-tier specialists like Kaga Electronics and SIIX target niches where ISO 13485 or IATF 16949 hurdles deter low-cost entrants.

Strategic moves revolve around vertical integration. Kyocera has patented a machine-learning solder-joint inspection system that detects micro-voids invisible to standard X-ray inspection, enhancing the credibility of power modules destined for EV inverters. Sumitronics installed inline X-ray and AOI systems to ensure 100% inspection of safety-critical boards, while Kaga invested in inverter control algorithm IP to secure design wins in traction drives. Such technology investments raise switching costs for OEMs and raise the market entry threshold for Japan's electronics manufacturing services market.

Competitive tension is rising as Taiwanese firms Pegatron and Wistron court Japanese automotive Tier 1s with aggressive bids, and BYD Electronics targets commodity lighting controls. Dual-source policies keep pricing pressure elevated, yet domestic providers offset this with quick engineering change order cycles and local component sourcing. The Ministry of Economy, Trade and Industry underscores process automation and defect elimination as policy imperatives, supporting advanced equipment grants that favor entrenched incumbents and uphold quality leadership in the Japan electronics manufacturing services market.

Japan Electronics Manufacturing Services Industry Leaders

Hon Hai Precision Industry Co., Ltd. (Foxconn)

SIIX Corporation

Kyocera Corporation

Flex Ltd.

Jabil Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alps Alpine Co., Ltd. announced a JPY 25 billion (USD 167 million) expansion of its Fukushima automotive sensor plant, adding 300,000 m² of cleanroom space for LiDAR, radar, and camera modules.

- December 2025: Murata Manufacturing Co., Ltd. completed a JPY 50 billion (USD 333 million) capacity increase for multilayer ceramic capacitors at its Shimane facility, lifting monthly output 30%.

- November 2025: Nidec Corporation committed JPY 100 billion (USD 667 million) to a new Shiga EV traction motor complex integrating assembly and power electronics under one roof.

- October 2025: Nihon Kohden Corporation received PMDA approval for a connected automated external defibrillator featuring real-time CPR coaching.

Japan Electronics Manufacturing Services Market Report Scope

The Electronics Manufacturing Services (EMS) Market is the industry that provides a range of services, including the design, assembly, production, and testing of electronic components and products for original equipment manufacturers (OEMs). These services enable OEMs to outsource manufacturing processes, allowing them to focus on core competencies such as research and development and marketing.

The Japan Electronics Manufacturing Services (EMS) Market Report is Segmented by Service Type (Electronic Manufacturing Services [PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, Other Electronic Manufacturing Services], Engineering Services, Test and Development Implementation, Logistics Services, and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging / Hybrid Processes), and End-User (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, and Other End-Users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-Users |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-User | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-Users |

Key Questions Answered in the Report

What is the projected value of the Japan electronics manufacturing services market in 2031?

It is forecast to reach USD 44.99 billion, growing at a 3.89% CAGR from 2026.

Which service type is expanding the fastest in Japan EMS?

Electromechanical assembly and box build services are expected to grow at a 4.63% CAGR through 2031.

Why are automotive programs vital for Japanese EMS providers?

Electrification and ADAS sensors are tripling electronic content per vehicle, steering high-complexity module builds toward domestic ISO-certified EMS partners.

How are rising utility costs affecting Japanese EMS competitiveness?

Power tariffs up to JPY 18.5 per kWh and tight labor markets are pushing OEMs to outsource or automate, reshaping plant economics.

What technology trend is redefining manufacturing processes in Japan EMS?

Advanced packaging, including fan-out and chiplet integration, is growing at 4.87% CAGR as heterogeneous integration gains traction.

Which regions are benefiting from government incentives for EMS relocation?

Kumamoto, Hokkaido, and Tohoku prefectures receive priority subsidies for semiconductor back-end and advanced packaging projects.

Page last updated on: