Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

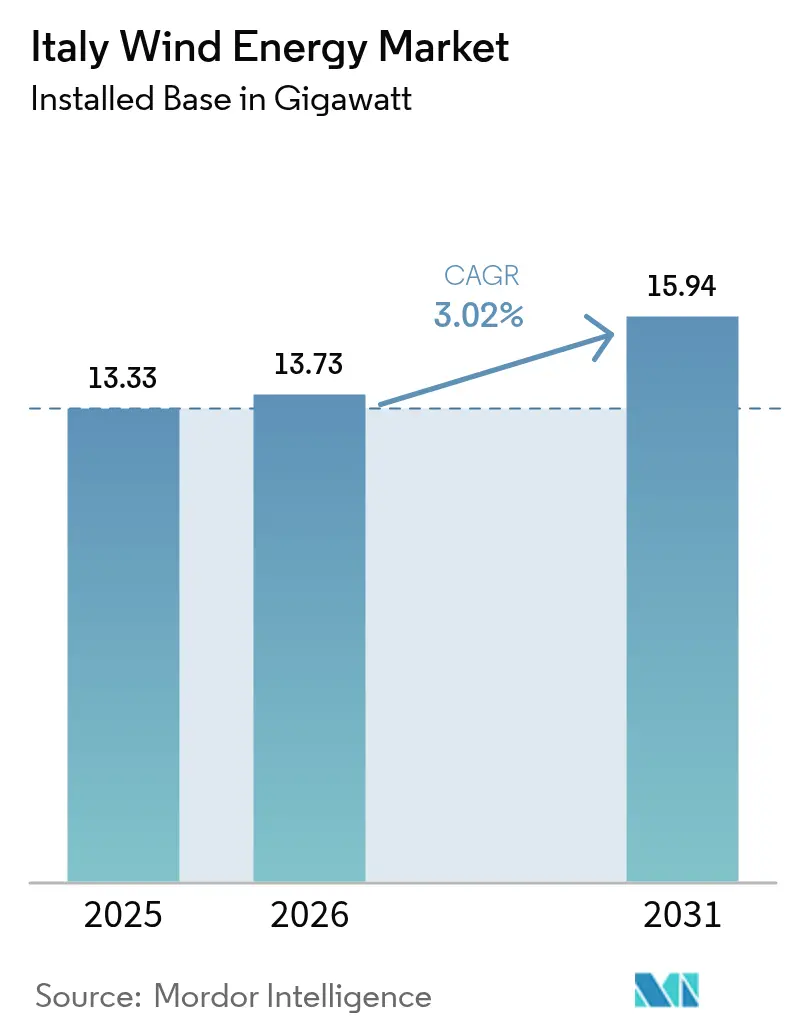

| Base Year Market Size (2025) | 13.33 gigawatt |

| Market Volume (2026) | 13.73 gigawatt |

| Market Volume (2031) | 15.94 gigawatt |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Wind Energy Market Analysis by Mordor Intelligence

The Italy Wind Energy Market size in terms of installed base is expected to grow from 13.33 gigawatt in 2025 to 13.73 gigawatt in 2026 and is forecast to reach 15.94 gigawatt by 2031 at 3.02% CAGR over 2026-2031.

The expansion is shaped by floating offshore technologies that unlock the country’s deep-water Mediterranean resource, a dense pipeline of more than 100 GW of grid connection requests, and supportive auction frameworks that lower revenue risk through two-way contracts for difference. Grid-digitalization investments by Terna and the European Commission’s multi-billion-euro recovery funds further improve integration prospects and financing visibility. At the same time, local permitting reforms shorten approval cycles, while corporate power-purchase agreements (PPAs) from steel, chemicals, and automotive players add predictable offtake demand. Rising commodity prices and supply-chain inflation create cost headwinds that temper near-term capacity additions, yet these challenges are partly offset by repowering programs that replace aging turbines with higher-capacity units.

Key Report Takeaways

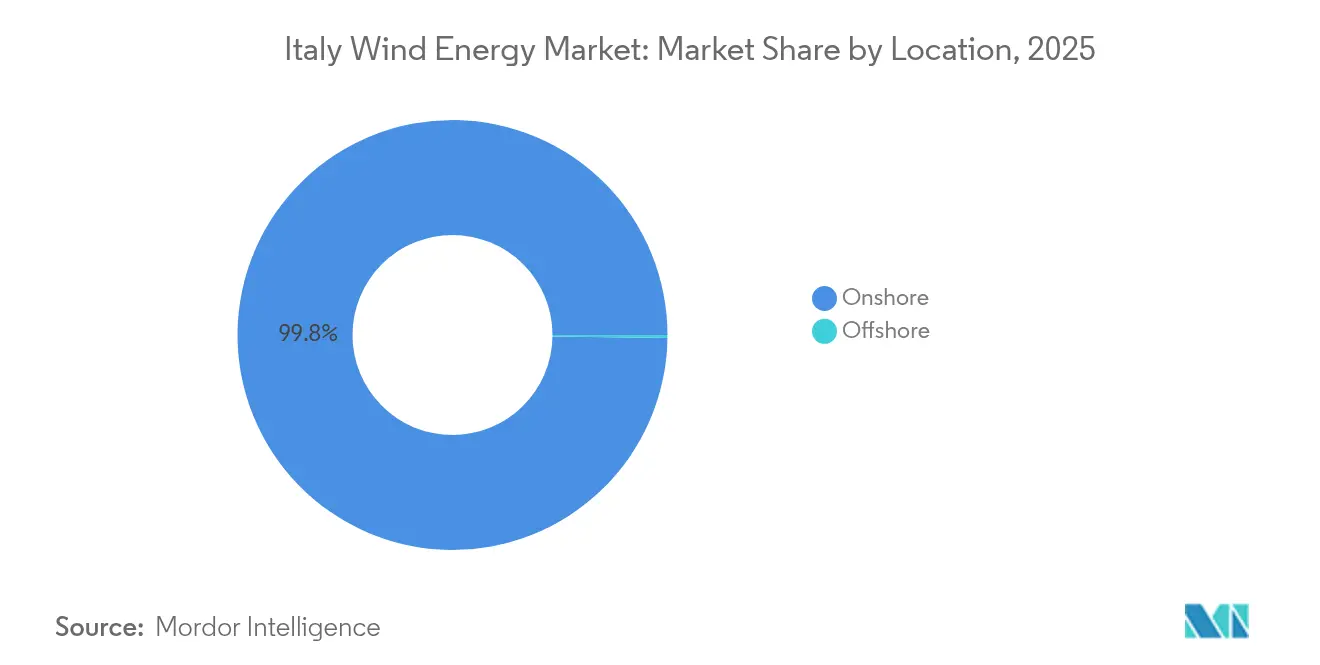

- By location, onshore installations accounted for 99.78% of Italy's wind energy market share in 2025; offshore capacity is projected to advance at a 71.6% CAGR through 2031.

- By turbine capacity, platforms with a capacity above 6 MW captured 18.60% of the growth in Italy's wind energy market size between 2025 and 2031, making them the fastest-expanding class.

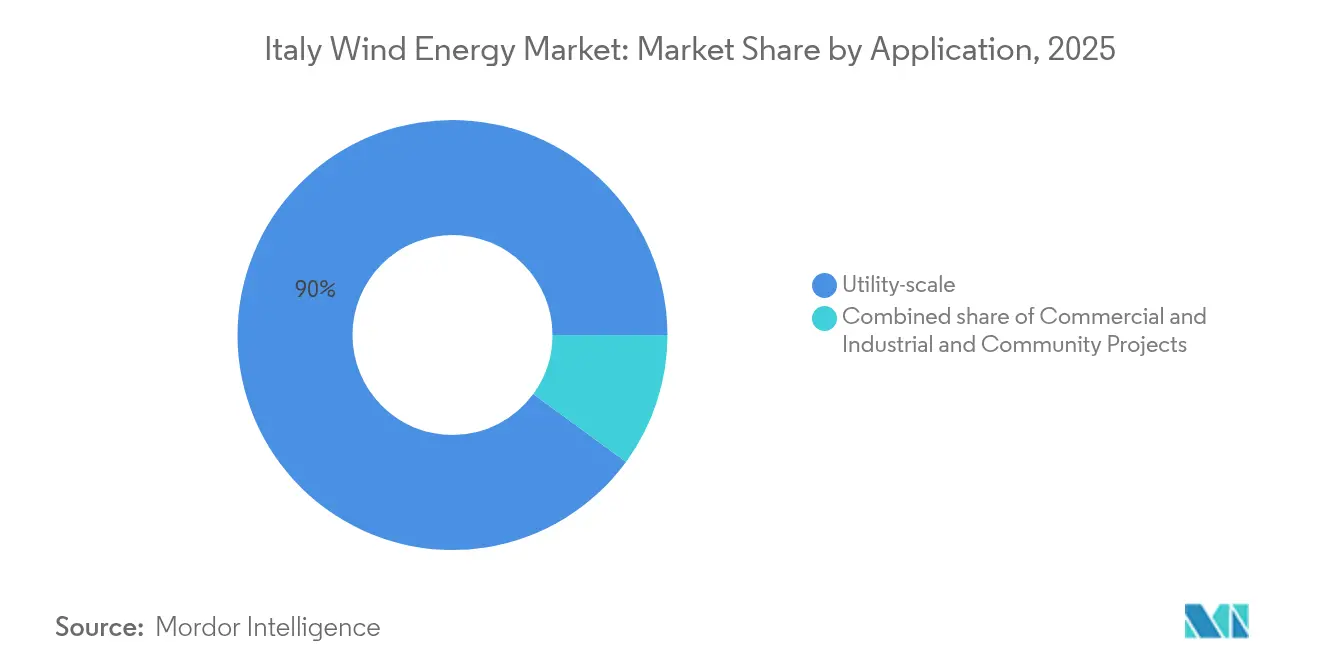

- By application, utility-scale projects commanded 89.95% of Italy's wind energy market share in 2025, while commercial and industrial systems are forecast to expand at a 12.2% CAGR to 2031.

- By company, Enel Green Power, ERG, and Edison collectively accounted for nearly 44.6% of 2025 installed capacity within the Italy wind energy market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy auction pipeline expansion | +0.8% | National, concentrated in Southern Italy and Sicily | Medium term (2-4 years) |

| NECP-aligned permitting reform momentum | +0.6% | National, with early gains in Emilia-Romagna, Puglia | Short term (≤ 2 years) |

| Corporate-PPA pull from hard-to-abate industries | +0.4% | Northern Italy industrial corridors, Lombardy, Veneto | Medium term (2-4 years) |

| Floating-offshore wind resource unlock | +0.9% | Mediterranean coastal regions, Sardinia, Sicily, Puglia | Long term (≥ 4 years) |

| Grid-digitalization & storage synergy | +0.5% | National | Medium term (2-4 years) |

| EU regulatory support and funding mechanisms | +0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renewable‐energy auction pipeline expansion

Italy’s FER2 decree establishes two-way CfDs with a EUR 185/MWh (USD 199.8/MWh) strike price for offshore wind, eliminating merchant revenue uncertainty and facilitating project debt financing. The European Commission approved a EUR 35.5 billion (USD 38.3 billion) scheme spanning 2028 that encompasses 4.59 GW of new renewable capacity, including gigawatt-scale floating projects in the Adriatic and Ionian Seas.[1]Enerdata, “Italian Renewable Contract-for-Difference Scheme,” enerdata.net Environmental approvals for Agnes-1-2 (700 MW) and Energia Wind 2020 (330 MW) show the funnel converting from intent to shovel-ready status, with late-2024 auctions moving projects toward 2025-2026 construction starts

NECP-aligned permitting reform momentum

Legislative Decree 190/2024 and the Testo Unico Rinnovabili introduce a single-window system and standardized environmental assessments, trimming the average approval cycle from fourteen to under five years.[2]Terna S.p.A., “Piano di Sviluppo 2024,” terna.it The Energy Release 2.0 measure accelerates grid-connection procedures, while a presumption of overriding public interest limits legal challenges. Adoption of maritime spatial plans in October 2024 finally brings certainty to offshore zone delimitation.

Corporate-PPA pull from hard-to-abate industries

Italian steelmakers, chemical refineries, and automotive suppliers increasingly lock into 10- to 15-year renewable PPAs to hedge wholesale price volatility and meet Scope 2 targets. Recent deals include Iberdrola–Acciaierie Venete and Eni Plenitude–Autostrade per l’Italia, which support bankability for mid-sized onshore projects in Basilicata and Veneto. ETS carbon-price escalation and CSRD reporting rules widen the value gap between grid-average and zero-carbon power, accelerating industrial renewable procurement.

Floating-offshore wind resource unlock

Italy hosts 207.3 GW of technical floating potential, the third-largest globally, with Sardinia and Sicily offering the strongest resource.[3]European Commission, “Recovery and Resilience Facility—Italy,” ec.europa.eu Flagship projects such as Renexia’s 2.8 GW Med Wind and the 1.11 GW Barium Bay array plan to deploy 15- to 18-MW turbines on semi-submersible foundations, bringing annual generation of up to 9 TWh per site. LCOEs near EUR 200/MWh (USD 216/MWh) remain above onshore levels but are expected to fall as blade lengths exceed 115 meters and supply-chain localization advances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy local-permitting & NIMBY pushback | -0.7% | Regional variations, strongest in Sardinia with renewable moratorium | Short term (≤ 2 years) |

| Solar-PV cost-competitiveness pressure | -0.3% | National, particularly Southern Italy high-irradiance zones | Medium term (2-4 years) |

| Euro-wind-turbine supply-chain inflation | -0.4% | National | Short term (≤ 2 years) |

| Grid integration and curtailment challenges | -0.6% | Southern mainland & islands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy local-permitting & NIMBY pushback

Despite national streamlining efforts, several regions slow or halt projects due to concerns over landscape and tourism. Sardinia’s temporary moratorium leaves 2.5 GW of authorized but unbuilt capacity, extending carrying costs for developers and widening the gap between tender awards and actual commissioning.

Solar-PV cost-competitiveness pressure

Utility PV LCOE fell 85% over 2010-2022, undercutting onshore wind in sunny Apulia and Sicily. Solar’s shorter construction lead times lure bidders in pay-as-bid auctions, compelling wind proponents to offer hybrid configurations or accept lower bid volumes in mixed-technology tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Emergence Transforms Market Dynamics

Onshore assets dominated the Italian wind energy market, accounting for 13.3 GW in 2025, which is equivalent to 99.78% of the installed capacity. Yet offshore additions are forecast to lift the location’s share to about 4.9% by 2031 on a 71.6% CAGR, making it the sector’s prime growth engine. The Italy wind energy market is tracking a clear pivot as floating foundations overcome the peninsula’s steep continental shelf, bringing multi-megawatt turbines to waters 60-200 meters deep.

Early offshore projects, such as Med Wind, Krimisa, and Messapia, leverage 15- to 18-MW machines that reduce foundation counts, lower balance-of-plant costs, and shorten construction timelines. Regulatory certainty from maritime spatial plans and FER2 auction pricing aligns with EU recovery funds to unlock debt financing. Onshore growth continues through repowering in Puglia and Calabria; yet, incremental sites are scarcer, underscoring the rising importance of offshore wind for the Italian wind energy market.

By Turbine Capacity: Technology Shift Toward Higher-Efficiency Platforms

Turbines under 3 MW still account for 71.95% of 2025 installations, a legacy of first-generation onshore wind builds. This cohort drives a repowering wave that replaces aging hardware with 4- to 6-MW units, doubling output on fewer towers and trimming O&M costs. Above 6 MW equipment records an 18.44% CAGR, the fastest within the Italy wind energy market, and is projected to command nearly one-fifth of cumulative capacity by 2031.

Higher-rated turbines increase annual energy production and reduce project footprints, which is critical in a market where permitting agencies favor smaller visual impacts. Vestas’ Ferrandina order for 5 × V162-6.4 MW platforms illustrates the onshore shift toward large rotors. Offshore arrays will rely almost exclusively on >15 MW machines by the decade’s end, accelerating supply-chain localization for blades, nacelles, and floating substructures.

By Application: Utility-Scale Dominance with C&I Acceleration

Utility projects accounted for 89.95% of the Italian wind energy market share in 2025, driven by auction design and grid interconnect standards that favor 50- to 500-MW clusters. Their aggregated bidding power yields lower financing spreads and easier access to EU grants. Italy's wind energy market size for utility-scale is projected to reach 14.37 GW by 2031, even as total market growth moderates.

Commercial and industrial (C&I) demand grows at a 12.2% CAGR, catalyzed by triple-digit ETS prices and mandatory corporate disclosures. Many C&I buyers sign synthetic PPAs or acquire equity stakes in dedicated renewable energy projects, ensuring the traceability of renewable attributes. Community schemes remain small but stable, aided by cooperative financing mechanisms that channel local savings into micro-wind clusters.

Geography Analysis

Southern regions host about 89.60% of existing wind assets, with Puglia leading due to flat terrain, robust Adriatic-Ionian winds, and proximity to Taranto’s heavy-industry load. Sicily follows, though grid-export limits delay some projects. Sardinia offers world-class resources but faces a political moratorium that pauses fresh approvals until 2026.

The Italy wind energy market is gradually diversifying northward. Emilia-Romagna and Veneto secure fixed-bottom offshore sites in shallower hubs for clean power in the Mediterranean Adriatic waters, evidenced by the Agnes-1-2 and Rimini projects. Improved north-south transmission links cut balancing costs, allowing surplus southern output to reach Lombardy’s industrial belts.

Island interconnectors, such as the Tyrrhenian Link and the Sicily–Calabria upgrade, unlock stranded capacity and reduce curtailment. Together with HVDC expansion toward the Balkans, these projects integrate variable wind flows, enabling Italy to function as a Mediterranean hub for clean power.

Competitive Landscape

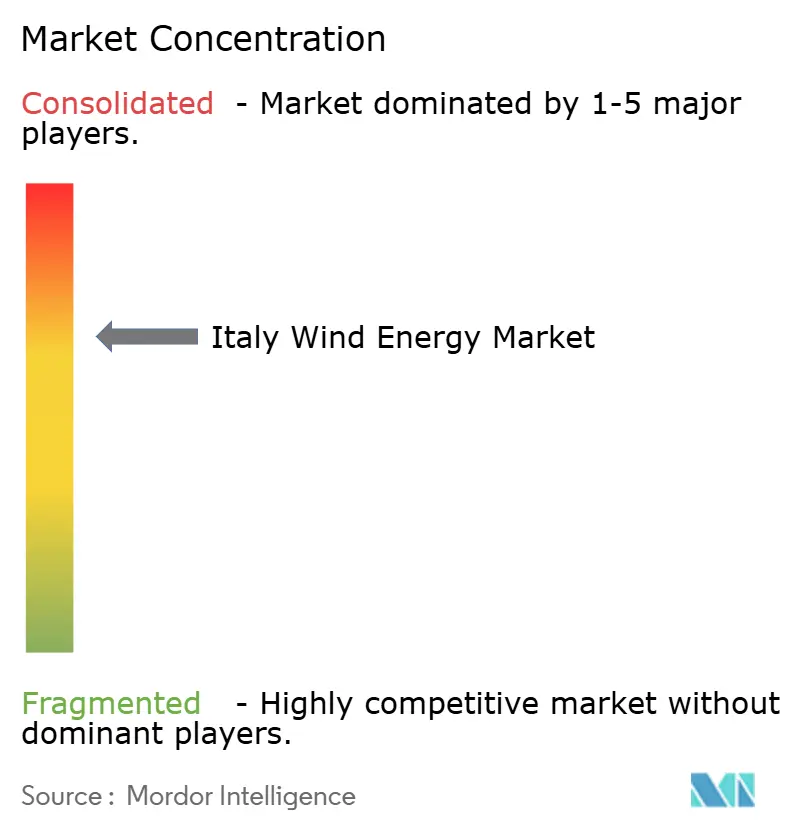

Market concentration is moderate, as the five largest developers, Enel Green Power, ERG, Edison, Renexia, and RWE, control approximately 60% of the installed onshore capacity. Enel leverages a 2.2 GW domestic fleet and a 4 GW project pipeline, including the repowering of early-2000s farms. ERG pivots toward offshore joint ventures, while Edison earmarks USD 1.5 billion for wind through 2026.[5]Edison S.p.A., “Strategic Plan 2025-2026,” edison.it

New entrants such as BlueFloat Energy and Spanish utility Iberdrola partner with floating-foundation specialists to capture FER2 offshore volumes. Chinese OEM MingYang teams with Renexia on the 2.8 GW Med Wind, introducing lower-cost 18 MW turbines that challenge European incumbents Vestas and Siemens Gamesa.

Supply-chain localization gains traction: Vestas doubled headcount at its Taranto blade plant to deliver 115-meter blades for the V236-15 MW platform, while Prysmian prepares submarine cables for HVDC links financed by EU resilience funds. Yet, turbine price inflation, raw material volatility, and ongoing consolidation test the profitability of developers and suppliers.

Italy Wind Energy Industry Leaders

ERG S.p.A

Enel Green Power

Edison SpA

EDP Renováveis

Alerion Clean Power SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vestas wins 94 MW in Italian onshore orders, Vis Roboris and Castelfranco, for Q2 2026 delivery.

- April 2025: Eni Plenitude inks 10-year PPA with Autostrade per l’Italia for a 16 MW Basilicata plant supplying 390 GWh over contract life.

- February 2025: Saipem books provisions for French offshore cost overruns, signaling execution risk spillovers into Italian floating contracts.

- November 2024: Vestas expands Taranto offshore blade production, targeting 2,000 jobs and 115-meter blade output for V236-15 MW machines.

- July 2024: Ministry of Environment clears EIA for Agnes-1-2 (700 MW) and Rimini (330 MW) offshore projects, enabling auction entry.

Italy Wind Energy Market Report Scope

Wind energy is the process where the wind generates mechanical power or electricity. Wind turbines then convert the kinetic energy in the wind into mechanical power.

The Italy wind energy market report provides insight into the market size, growth, trends, analysis, government policies and regulations, competitive landscape, market dynamics, and opportunities. The market sizing and forecasts have been done for each segment based on installed capacity.

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How large is the installed wind capacity in Italy in 2026?

The Italy wind energy market size stands at 13.33 GW for 2025 and is expected to surpass 13.73 GW during 2026 based on the 3.02% CAGR trajectory.

What CAGR is forecast for Italian wind additions between 2026 and 2031?

Capacity is projected to expand at a 3.02% CAGR, lifting total installations to 15.94 GW by 2031.

Which location segment is growing fastest?

Offshore installations lead with a 71.6% CAGR through 2031 as floating foundations unlock deep-water Mediterranean resources.

Why are corporate PPAs important for Italian wind?

They provide long-term revenue certainty, lower financing costs, and help industries meet decarbonization targets amid rising ETS prices.

What are the main restraints on future wind growth?

Local permitting delays, grid congestion causing curtailment, turbine cost inflation, and intense price competition from low-cost solar PV.

Which companies dominate Italy’s wind sector?

Enel Green Power, ERG, Edison, Renexia, and RWE account for about 59.30% of installed capacity, while BlueFloat Energy and MingYang target emerging offshore opportunities.

Page last updated on: