Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

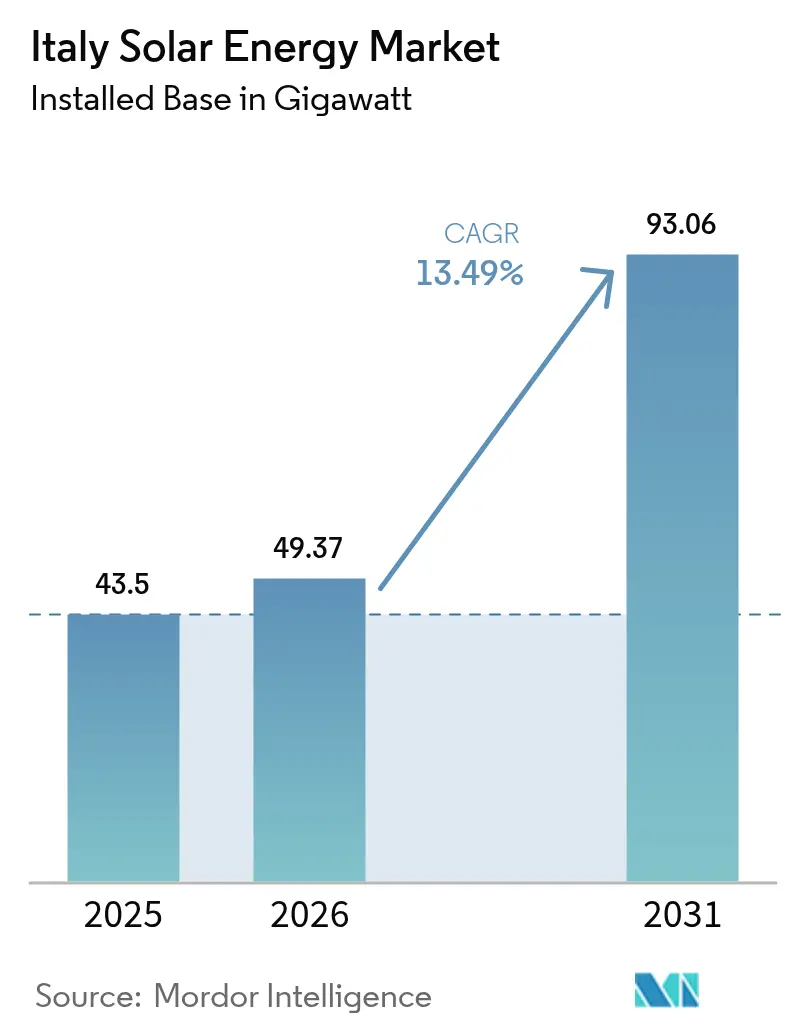

| Base Year Market Size (2025) | 43.5 gigawatt |

| Market Volume (2026) | 49.37 gigawatt |

| Market Volume (2031) | 93.06 gigawatt |

| Growth Rate (2026 - 2031) | 13.49% CAGR |

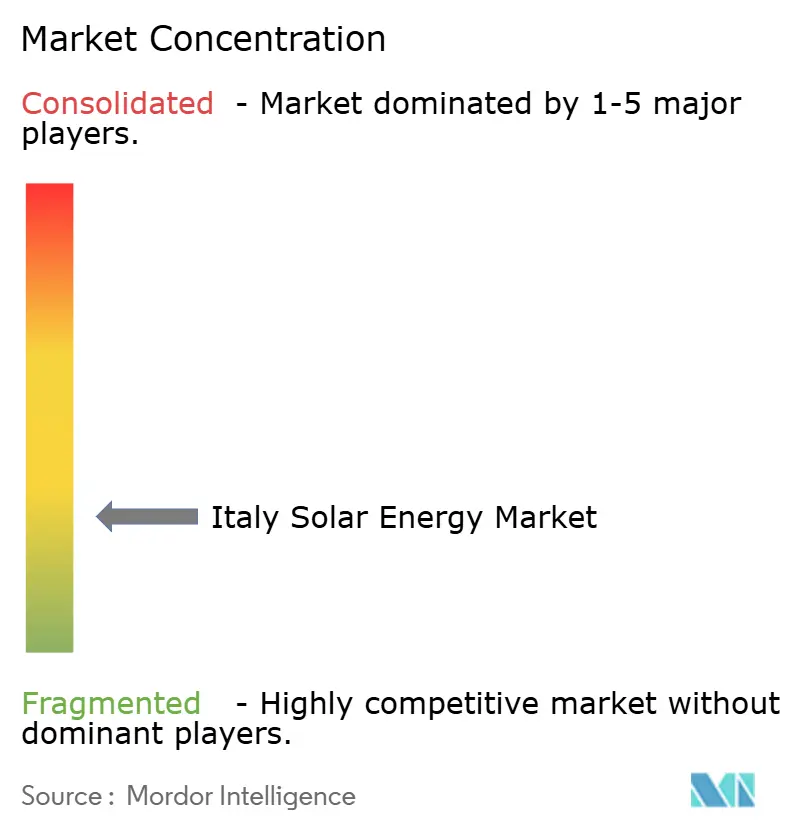

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Solar Energy Market Analysis by Mordor Intelligence

The Italy Solar Energy Market size in terms of installed base was valued at 43.5 gigawatt in 2025 and estimated to grow from 49.37 gigawatt in 2026 to reach 93.06 gigawatt by 2031, at a CAGR of 13.49% during the forecast period (2026-2031).

Lowered levelized cost of electricity, the European Union’s REPowerEU mandate, and Italy’s PNIEC 2030 target combine to provide developers with long-range visibility, while abundant capital inflows sustain momentum even as subsidies taper. Utility-scale projects now achieve an average LCOE of below EUR 0.040/kWh in sunny southern provinces, outperforming gas-fired generation at every hour of the day.(1)International Renewable Energy Agency, “Renewable Power Generation Costs 2023,” irena.org Corporate power-purchase agreements (PPAs) worth EUR 2.8 billion were signed in 2024 alone, indicating that large manufacturers view fixed-price solar contracts as a hedge against commodity volatility. At the household level, the Superbonus incentive is spurring residential demand, although its upcoming phase-down creates urgency that may prompt front-loading of installations into 2025.

Key Report Takeaways

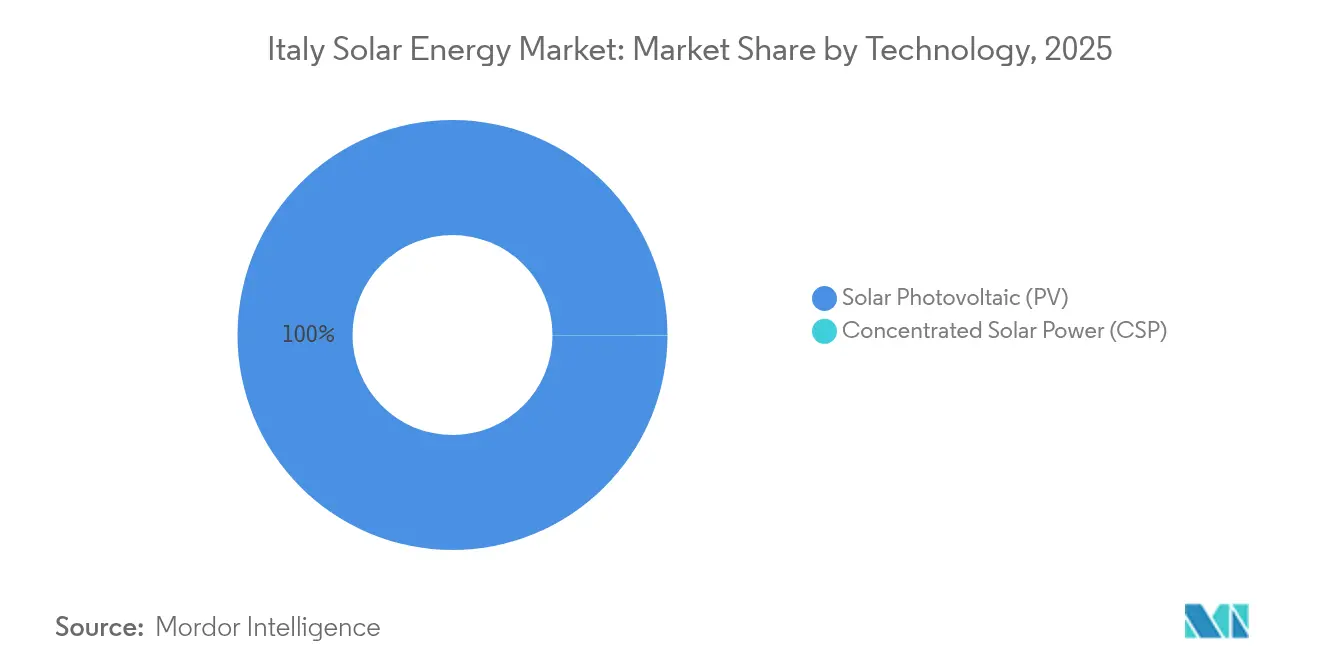

- By technology, photovoltaic systems held 99.97% of Italy's solar energy market share in 2025; concentrated solar power is forecast to expand at a 104.7% CAGR through 2031.

- By grid type, on-grid installations accounted for a 97.55% share of the Italian solar energy market size in 2025, while the off-grid segment is projected to advance at a 26.9% CAGR through 2031.

- By end-user, utility-scale plants accounted for 53.65% of the Italy solar energy market size in 2025 and are set to grow at a 14.21% CAGR over the forecast period.

- Enel Green Power, EF Solare Italia, and Sonnedix collectively controlled approximately 34.60% of the Italian solar energy market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE of PV electricity | +3.2% | National, highest in the South | Medium term (2-4 years) |

| EU REPowerEU & PNIEC 2030 targets | +2.8% | National, accelerated in Mezzogiorno | Long term (≥ 4 years) |

| Corporate-PPA boom among industrials | +2.1% | Northern industrial corridors | Short term (≤ 2 years) |

| Residential “Superbonus” tax credits | +1.9% | Urban centers nationwide | Short term (≤ 2 years) |

| Agrivoltaics enhancing land value | +1.4% | Puglia, Sicily, Emilia-Romagna | Medium term (2-4 years) |

| Behind-the-meter storage cost parity | +1.1% | High-tariff regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining LCOE of PV Electricity

Italy’s average solar LCOE fell to EUR 0.045/kWh in 2024, marking the first instance of subsidy-free parity with conventional generation.(2)International Renewable Energy Agency, “Renewable Power Generation Costs 2023,” irena.org Module efficiencies reached 22.5% for mainstream crystalline panels, and standardized racking further trimmed balance-of-system expenses. Southern utility projects now deliver LCOE as low as EUR 0.040/kWh, pushing gas peakers into residual duty. Domestic inverter maker Fimer introduced 99.2% efficiency string models that reduce conversion losses, locking in cost reductions that are likely to deepen through 2027.

EU REPowerEU & PNIEC 2030 Targets

Brussels raised Italy’s 2030 solar obligation to 85 GW, nearly doubling the earlier PNIEC figure and incorporating quarterly compliance reviews that maintain political focus.(3)European Commission, “REPowerEU: Joint European Action for More Affordable, Secure and Sustainable Energy,” ec.europa.eu Rome earmarked EUR 6.9 billion in PNRR funds, with 60% dedicated to southern solar build-out. Regional “green corridors” have reduced permit cycles for sites exceeding 50 MW from 24 months to approximately 8 months, while new commercial buildings over 1,000 m² are required to install rooftop systems, creating an assured demand pipeline.

Corporate-PPA Boom Among Italian Industrials

Industrial buyers locked in 2.3 GW of new solar PPAs during 2024, a 340% jump year-on-year. Steelmaker Arvedi signed for 180 MW under a 15-year fixed-price deal, and magnetics producer Bekaert lined up 95 MW to curb input-cost swings. Banks now treat PPAs as quasi-hedging instruments, offering debt at spreads below those of traditional project finance, because corporate credit stands behind the cash flows.

Residential “Superbonus” & Tax-Credit Schemes

The 110% Superbonus drove 4.2 GW of residential rooftop capacity through 2024, democratizing access across income brackets. The incentive begins stepping down to 90% in 2025, prompting a rush that has installer waiting lists stretching to 12 months in Lombardy. While complexity adds EUR 2,000-4,000 to average system cost, energy communities enjoy an extra 20% credit, accelerating neighborhood-scale deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid saturation & lengthy permitting | -2.3% | Northern regions, spreading central | Short term (≤ 2 years) |

| Phase-down of Superbonus incentives | -1.8% | Residential nationwide | Short term (≤ 2 years) |

| Restrictions on farmland ground-mount | -1.2% | Protected rural landscapes | Medium term (2-4 years) |

| Local opposition & landscape rules | -0.9% | Heritage and coastal areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Saturation & Lengthy Permitting

Northern grids face 23 GW of queued projects, which delays connections by up to two years and increases interconnection fees to EUR 80,000/MW in hotspots. Terna’s EUR 18 billion expansion plan is still ramping. Developers must navigate 14 approvals; environmental impact assessments alone can take up to 12 months. Fast-track rules for sub-10 MW plants ease pressure but do little for the large farms that dominate new capacity.

Phase-down of Superbonus Incentives

Cutting the Superbonus to 90% in 2025 reduces paybacks and clouds installer pipelines, with many forecasting revenue drops of 40-60% post-2025. Material shortages already add 15-20% to component costs during current demand peaks, and banks are tightening lending amid an uncertain future for savings. Regional programs attempt to fill gaps but often add administrative layers that can confuse consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Masks CSP Renaissance

PV installations accounted for 99.97% of total additions in 2025, driven by mature supply chains and the ease of rooftop siting. Concentrated solar power, though scarcely 0.02 GW today, is accelerating at a 104.7% CAGR and could supply evening peaks with six-hour molten-salt storage. Sicily's high direct normal irradiance, exceeding 2,000 kWh/m²/year, enables CSP to dispatch at fixed tariffs that rival those of gas units, and the EU taxonomy favors its grid-firming traits. Enel Green Power's hybrid CSP-PV blueprint pairs up-front PV yields with stored thermal output after dusk, a template that could reshape baseload renewables.

The Italy solar energy market size for CSP remains modest, yet favorable debt terms under green bonds lower capital cost. Independent power producers secure 25-year feed-in contracts that cover both electricity and "capacity-like" availability payments, improving risk-adjusted returns. A policy requiring ≥50 MW projects to demonstrate grid-support services implicitly rewards thermal storage, nudging developers toward CSPs' dispatchable profile. Medium-term growth thus hinges less on technology risk than on how quickly component suppliers can scale specialized receivers and salts.

By Grid Type: Off-Grid Acceleration Challenges On-Grid Hegemony

On-grid systems enjoy 97.55% market share thanks to net-metering simplicity and a streamlined process for <20 kW connections. Yet the off-grid segment is pacing at a 26.9% CAGR, catalyzed by island microgrid programs where diesel costs exceed EUR 0.35/kWh. Sicily's minor islands plan to replace aging gensets entirely by 2028, and mainland factories hurt by 2022 energy shocks are installing solar-storage microgrids that cut outage risk.

Italy's solar energy market size for off-grid remains small, but battery innovation makes it feasible for mines, data centers, and food processors to sever grid dependence. Projects bypass long interconnection queues, trimming development time to under a year. Vanadium flow batteries are suited to 10-hour profiles common in isolated resorts, while lithium-iron-phosphate units dominate shorter-cycle industrial applications. Regulators now permit off-grid plants to export surpluses into local distribution networks up to 5 GWh per year, a hybrid model that further blurs the boundaries of the grid.

By End-User: Utility-Scale Momentum Reshapes Market Dynamics

Utility-scale plants captured 53.65% market share in 2025, advancing at a 14.21% CAGR on the back of cheap capital and appetite for corporate PPAs. Land-bank schemes in Puglia and Basilicata pre-permit brownfields, removing a key barrier and letting projects reach notice-to-proceed in under nine months. Terna’s new grid code compensates large sites for providing reactive power support, adding a small but dependable revenue stream.

The Italian solar energy market size tied to commercial and industrial rooftops continues to expand, albeit at a slower pace than utility farms, as many SMEs still rent their premises. Residential uptake depends on evolving incentives, although energy-community bonuses maintain a baseline level of interest. Utility-scale investors now routinely integrate agrivoltaics or sheep grazing to mitigate land-use conflicts, and combined PV-plus-storage arrays achieve an average capacity factor of 30% when dispatch optimization is included.

Geography Analysis

Southern Italy maintains the strongest solar economics, with capacity factors of 22-25% compared with 15-17% in the north. Puglia leads with 3.8 GW of installed capacity, boosted by dedicated agrivoltaic fast lanes in regional permitting. Sicily and Sardinia add a laboratory use-case, piloting floating solar and CSP hybrids that inform mainland rollouts. Central provinces, such as Abruzzo, balance solid irradiation and proximity to Rome’s load centers, making them favored by PPA-backed developers.

Northern regions suffer grid congestion but host Italy’s largest industrial off-takers; Lombardy alone registered 7 TWh of signed solar PPAs in 2024. Developers willing to fund 150 kV upgrade taps unlock lucrative dispatch zones. Terna budgets EUR 3.2 billion through 2028 for North-South transmission reinforcement to shift surplus midday solar energy from south to north. New HVDC corridors mitigate curtailment risk, reducing merchant price volatility, particularly in Emilia-Romagna.

Internal trade in guarantees of origin (GO) is emerging: southern generators monetize excess certificates to northern corporates that lack local rooftop potential. Previously overlooked Molise and Basilicata capitalize on flat terrain and friendly town councils, offering over 1,000 hectares of pre-zoned land for sites exceeding 50 MW. Coastal heritage rules steer tourist districts toward rooftop formats; hence, Liguria prioritizes BIPV tiles, avoiding visual intrusion. The disparate regulatory tempo across provinces incentivizes developers to diversify pipelines geographically, spreading approval risk.

Competitive Landscape

The top five operators hold roughly 40% combined share, indicating moderate concentration that still leaves space for niche entrants. Enel Green Power leverages its grid affiliate expertise to secure priority interconnection and has earmarked EUR 1.2 billion for 2.1 GW of new southern sites by 2027.(5)Enel, “Annual Report 2024,” enel.com EF Solare Italia focuses on operational excellence, reporting 99.5% fleet availability through predictive maintenance. Sonne, as leading firms now own EPC arms, tracker manufacturers, and O&M software suites, thereby expanding by acquiring 450 MW of pipeline assets, underscoring that scale can be bought as well as built.

Vertical integration is the dominant strategy: leading firms now own EPC arms, tracker manufacturers, and O&M software suites, capturing more value and de-risking schedules. Fimer’s high-efficiency inverters gain share due to compliance with the latest grid-support mandates, while Canadian Solar’s planned 2 GW panel plant aims to shorten European supply chains and hedge tariff risk. Digital newcomers, such as Otovo, curate turnkey packages for homeowners via online portals, thereby squeezing soft costs and boosting close rates.

Specialty arenas, agrivoltaics, floating arrays, and BIPV offer white-space where smaller innovators with agronomic or marine expertise can compete. Institutional investors pour pension money into mid-size portfolios (10-50 MW) for steady inflation-linked returns, spawning a secondary market for de-risked assets. Meanwhile, battery aggregators court homeowners with upfront rebates in return for multi-year cycling rights, forging new alliances between utilities and retail installers.

Italy Solar Energy Industry Leaders

Enel Green Power S.p.A.

EF Solare Italia S.p.A.

Sonnedix Power Holdings Ltd

Renantis S.p.A.

A2A S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Enel Green Power announced a EUR 1.2 billion plan to deliver 2.1 GW of utility-scale solar, much of it agrivoltaic, by 2027.

- September 2025: Sonnedix acquired a 450 MW development pipeline from Gruppo STG for EUR 180 million, thereby expanding its footprint in the Mezzogiorno region.

- August 2025: A2A linked 15,000 home batteries into a 75 MW virtual power plant that will participate in Terna’s ancillary market.

- July 2025: Rome enacted fast-track permits for solar energy on brownfields, cutting the approval time to eight months.

- June 2025: Canadian Solar revealed plans for a 2 GW module factory in southern Italy, investing EUR 800 million and adding 1,200 jobs.

- May 2025: Edison signed a 380 MW, 15-year PPA with Stellantis worth EUR 2.1 billion.

Italy Solar Energy Market Report Scope

Solar energy is radiant light and heat from the sun that is harnessed using a range of technologies, such as solar PV or concentrated solar power (CSP), to generate electricity, solar thermal energy, and solar architecture.

The Italian solar energy market is segmented by type, end-user, and deployment. By type, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into residential, industrial & commercial, and utility-scale.

For each segment, the market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What is the projected installed capacity for solar power in Italy by 2031?

The country is expected to reach 93.06 GW of cumulative solar capacity by 2031.

How fast is utility-scale solar growing compared with other segments in Italy?

Utility-scale projects are advancing at a 14.21% CAGR, outpacing residential and C&I installations.

Will the Superbonus still support rooftop solar after 2026?

Yes, but the reimbursement rate falls from 110% to 90% in 2025 and to 70% in 2026, so paybacks lengthen.

Why are corporate PPAs important for new Italian solar farms?

Industrial PPAs lock in long-term revenue, enabling projects to raise debt at attractive terms and avoid wholesale price risk.

How does agrivoltaics benefit Italian farmers?

Dual-use systems can triple per-hectare revenue by combining crop output with electricity sales while reducing water stress.

Page last updated on: