Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

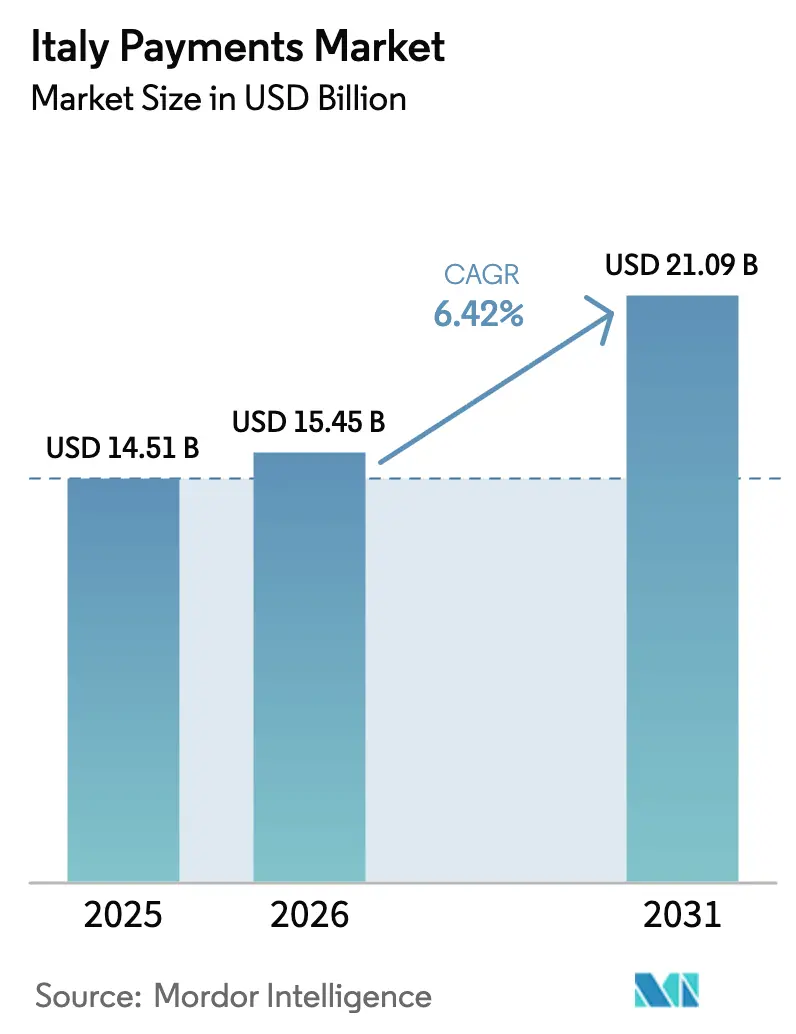

| Base Year Market Size (2025) | USD 14.51 Billion |

| Market Size (2026) | USD 15.45 Billion |

| Market Size (2031) | USD 21.09 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

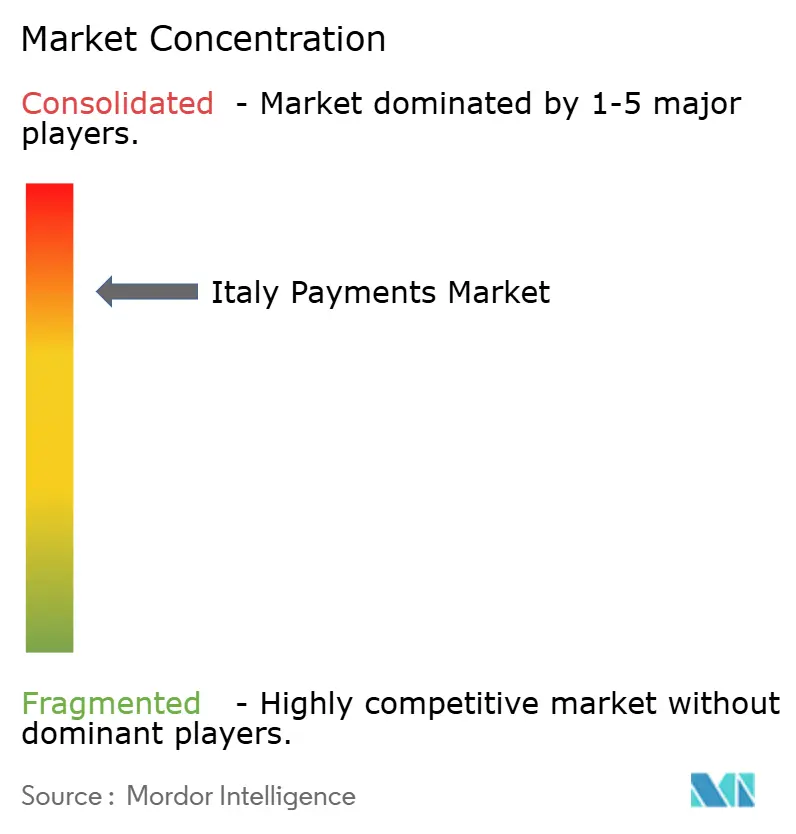

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Payments Market Analysis by Mordor Intelligence

The Italy payments market size stands at USD 15.45 billion in 2026 and is projected to reach USD 21.09 billion by 2031, reflecting a 6.42% CAGR over the forecast period. A decisive pivot away from cash toward digital rails underpins this growth, supported by instant-payment mandates, point-of-sale tax incentives, and record tourism receipts. Contactless adoption has crossed the 70% threshold at physical checkouts, while e-commerce gateways embed one-click authentication, reducing cart abandonment risk. Merchant acquirers consolidate for scale, fintech gateways court developers with open APIs, and real-time account-to-account rails begin to erode legacy settlement delays. Countervailing forces persist - regional cash affinity, elevated micro-merchant fees, and demographic drag - but none are strong enough to derail the structural migration to cashless transacting.

Key Report Takeaways

- By mode of payment, debit cards led with 38.52% of the Italy payments market share in 2025, and digital wallets for online sales are forecast to expand at a 7.33% CAGR between 2026 and 2031.

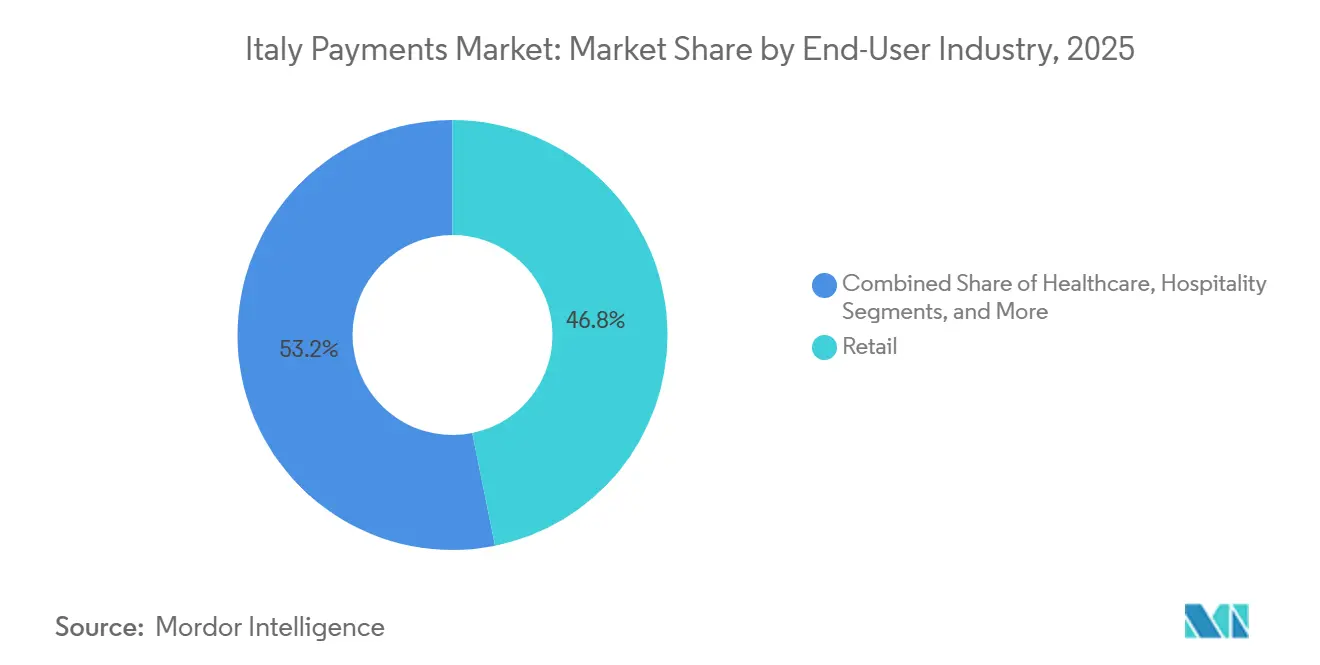

- By end-user industry, retail commanded 46.83% share of the Italy payments market size in 2025, and hospitality is projected to advance at a 7.66% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom fuels card and wallet usage | +1.2% | Northern urban centers, national spillover | Medium term (2-4 years) |

| Tourism rebound lifts cross-border spend volumes | +1.0% | Rome, Venice, Florence, Amalfi Coast | Short term (≤ 2 years) |

| Instant-payment rails RT1 and TIPS gain merchant adoption | +0.9% | National, early uptake by large retailers | Medium term (2-4 years) |

| Growing use of Buy-Now-Pay-Later for luxury and fashion | +0.8% | Milan and Rome fashion districts | Short term (≤ 2 years) |

| Digital tax incentives for SMEs to install POS terminals | +0.7% | Southern regions and rural areas | Long term (≥ 4 years) |

| PSD2-driven open-banking APIs accelerate A2A payments | +0.6% | National, fintech platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Fuels Card and Wallet Usage

Online retail volumes rose sharply after pandemic lockdowns and have held those gains, normalizing contactless and mobile checkout habits. Debit card transactions climbed to 6.7 billion in 2024 as issuers raised contactless limits and merchants implemented tokenization that mitigates fraud.[1]Bank of Italy, “Payment Systems Report 2025,” bancaditalia.it Digital wallets, including PostePay, Satispay, Apple Pay, and Google Pay, will gain share through instant checkout and loyalty integration that resonates with demographics under 40. Strong Customer Authentication briefly injected friction when it launched, yet low-value and trusted-merchant exemptions quickly restored conversion rates.[2]European Central Bank, “Payment Statistics,” ecb.europa.eu Gateways now route payments through least-cost algorithms, occasionally favoring account-to-account rails when interchange savings justify the switch. The cumulative effect is rising electronic penetration in segments once dominated by cash-on-delivery.

Tourism Rebound Lifts Cross-Border Spend Volumes

Italy welcomed 134 million visitors in 2024, generating EUR 58.6 billion (USD 62.8 billion) in revenue.[3]ENIT, “Tourism Statistics 2024,” enit.it Travelers prefer card payments that avoid foreign-exchange cash hassles, driving volumes in hospitality, retail, and cultural attractions. Visa and Mastercard benefit disproportionately, capturing interchange on both issuing and acquiring sides. Tourist familiarity with tap-and-go norms accelerated contactless upgrades at merchant terminals, shortening queues at high-traffic sites. Acquirers responded with dynamic currency conversion and multi-currency settlement features, improving transparency and guest satisfaction.

Instant-Payment Rails RT1 and TIPS Gain Merchant Adoption

SEPA Instant regulation obliges providers to receive real-time credit transfers from January 2025 and to send them by October 2025. Italy’s RT1 and the pan-European TIPS infrastructure now settle in under 10 seconds, freeing merchants from the working-capital drag of T+1 card funding. Early pilots among supermarkets and hotel chains deploy QR codes or NFC triggers that initiate direct bank transfers. Although instant payments represented less than 5% of credit transfers in 2024, cost savings over percentage-based card fees make the rail compelling for high-value tickets, laying the groundwork for long-term displacement of cards.

Growing Use of Buy-Now-Pay-Later for Luxury and Fashion

BNPL volumes reached EUR 6.8 billion (USD 7.3 billion) in 2024, up 46% year on year. Providers such as Scalapay and Klarna split purchases into equal installments, funding zero-interest plans through merchant fees that merchants accept as a conversion lever. Younger shoppers prefer transparent repayment schedules to revolving credit, while luxury brands maintain price integrity without discounting. Regulators proposed affordability checks and clearer disclosures in 2025, yet merchant demand for larger baskets is expected to keep the model expanding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently high cash affinity in Southern regions | -0.5% | Campania, Calabria, Sicily, Apulia | Long term (≥ 4 years) |

| Ageing population slows mobile-wallet penetration | -0.4% | National, 60+ demographic | Long term (≥ 4 years) |

| Elevated interchange and MDR fees for micro-merchants | -0.3% | National, small businesses | Medium term (2-4 years) |

| Tightened AML rules increase KYC onboarding friction | -0.2% | National, PSPs and fintechs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistently High Cash Affinity in Southern Regions

Cultural norms, an informal economy, and sparse terminal density sustain cash use in Campania, Calabria, Sicily, and Apulia. Even after a 30% tax credit for point-of-sale hardware, micro-merchants cite fixed fees as prohibitive, maintaining cash preference despite security and reconciliation drawbacks. The North-South digital gap therefore remains wide, with Lombardy exceeding 50% digital share while many Southern provinces remain below 35%. Bridging this divide requires a mix of fiscal incentives, fee reform, and consumer education.

Ageing Population Slows Mobile-Wallet Penetration

Italy’s median age of 48 skews toward older cohorts that are hesitant to adopt smartphone-based authentication. While contactless cards achieve near-universal acceptance, wallets such as Satispay, Apple Pay, and Google Pay penetrate unevenly outside major metros. Issuers run education campaigns and simplified onboarding flows, yet biometric login and app navigation still deter segments over 60. As this cohort controls significant discretionary spend, slow wallet uptake tempers total electronic growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Debit Cards Anchor POS, Wallets Surge Online

Debit card payments held 38.52% of the Italy payments market share in 2025 as contactless tapping normalized checkout behavior. Regulatory interchange caps and merchant familiarity sustain this dominance, while credit cards remain indispensable for cross-border travel and high-ticket purchases. Account-to-account methods captured under 5% of transfers in 2024 due to limited acceptance, although SEPA Instant mandates promise faster scaling through 2031.

Digital wallets for online purchases are projected to post a 7.33% CAGR through 2031, signaling the highest velocity among channels. One-click authentication, biometric login, and loyalty integration cut abandonment, while gateway-level routing shifts volume toward cheaper rails. Cash usage erodes each year yet stays relevant for micro-transactions and in rural markets where fixed terminal fees deter merchants. If instant transfers gain consumer trust, card schemes may face margin pressure on large-basket retail, but entrenched debit convenience suggests coexistence rather than immediate displacement.

By End-User Industry: Retail Dominates, Hospitality Accelerates

Retail commanded 46.83% of the Italy payments market size in 2025, encompassing grocery, fashion, electronics, and pharmacies. Rising contactless limits and self-checkout kiosks keep growth positive despite maturity. Buy-Now-Pay-Later installments drive higher order values in fashion, while grocery chains deploy tokenized card files for unattended checkout lanes.

Hospitality is forecast to pace the field with a 7.66% CAGR between 2026 and 2031, buoyed by surging inbound tourism and merchants’ urgency to accept international cards. Hotels, restaurants, and tour operators integrate dynamic currency conversion and instant settlement to improve liquidity. Entertainment venues adopt QR-ticketing with embedded payments, while healthcare digitizes slowly due to public-sector reimbursement cycles and older patient demographics. Transportation and utilities modernize in pockets, contactless transit in Milan, online tax portals in Rome, but progress remains uneven, leaving substantial headroom for electronic expansion.

Geography Analysis

Northern regions such as Lombardy, Emilia-Romagna, and Piedmont approach Scandinavian electronic penetration, exceeding 50% digital share in 2024. Dense banking networks and higher GDP per capita fuel terminal deployment and card issuance. The Italy payments market size for these provinces is forecast to compound above the national average through 2031 as open banking and instant rails find receptive early adopters.

Central tourism hubs such as Rome, Florence, and Venice benefit from record visitor inflows that favor card transactions, compelling merchants to accept near-field communication, dynamic currency conversion, and multi-currency settlement. SEPA Instant cuts settlement to seconds, improving cash-flow management for high-velocity hospitality outlets. Concurrently, smartphone-based dongles extend acceptance to seasonal vendors who once operated cash-only stands.

Southern provinces lag, with digital share below 35% despite the national tax credit targeting small businesses. Lower affluence, cultural cash preference, and a sizable informal economy slow adoption. Nevertheless, mobile wallets like Satispay gain traction by offering peer-to-peer convenience, and acquirers court micro-merchants with flat-fee packages that neutralize per-transaction costs. Convergence remains a decade away, yet incremental gains continue as utility billers and municipal services migrate to online portals.

Competitive Landscape

Domestic champion Nexi maintains the largest acquiring footprint through long-standing bank partnerships, processing a plurality of in-store volumes. Worldline and Adyen expand by serving multinational retailers that require unified European acceptance, while Stripe and PayPal dominate developer-led online onboarding. Together, these five players captured most of the merchant volume in the Italy payments market in 2025, signaling high concentration.

Strategic themes include vertical integration, acquirers buying gateways and software vendors to capture more value, and real-time settlement enablement that differentiates on liquidity speed. Tokenization and biometric authentication mitigate fraud while preserving conversion, and acquirers bundle analytics and loyalty modules to deepen merchant stickiness.

Open banking, enabled under PSD2, remains below 5% of transfers, yet fintechs see white-space in payroll, bill pay, and high-value retail. BNPL specialist Scalapay processed EUR 6.8 billion (USD 7.3 billion) in transactions in 2024 and eyes point-of-sale expansion. Compliance overhead under strengthened AML directives favors incumbents with mature KYC infrastructure, raising barriers for smaller entrants.

Italy Payments Industry Leaders

PayPal Holdings, Inc.

Bancomat S.p.A. (Bancomat Pay)

Mastercard Europe S.A.

Amazon Payments, Inc. (Amazon Pay)

Visa Europe Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SEPA Instant regulation took effect, requiring all Italian providers to receive real-time credit transfers and accelerating account-to-account settlement.

- October 2024: Nexi completed operational integration with Nets, creating a pan-European platform processing 40 billion transactions annually.

- September 2024: Italy extended its 30% tax credit for digital-payment infrastructure through 2025, focusing on small merchants in Southern regions.

- July 2024: Satispay surpassed 4 million active users and 300,000 merchant acceptance points, adding instant cashback features.

Italy Payments Market Report Scope

The Italy Payments Market Report is Segmented by Mode of Payment (Point of Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash, and More], Online Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash-on-Delivery, and More]), and End-User Industry (Retail, Entertainment, Hospitality, Healthcare, Other). Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Mode | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Mode |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Mode | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Mode | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Italy payments market in 2026?

The Italy payments market size is valued at USD 15.45 billion in 2026.

What is the expected CAGR for Italian payment transactions through 2031?

Aggregate transaction value is forecast to rise at a 6.42% CAGR between 2026 and 2031.

Which payment method is growing fastest online?

Digital wallets for online sales are projected to expand at a 7.33% CAGR over the forecast period.

Which end-user sector shows the strongest growth outlook?

Hospitality is expected to grow at a 7.66% CAGR from 2026 to 2031 due to record tourism inflows.

What infrastructure underpins real-time payments in Italy?

RT1 and TARGET Instant Payment Settlement process SEPA Instant transfers, settling funds in under 10 seconds.

Page last updated on: