Italy Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

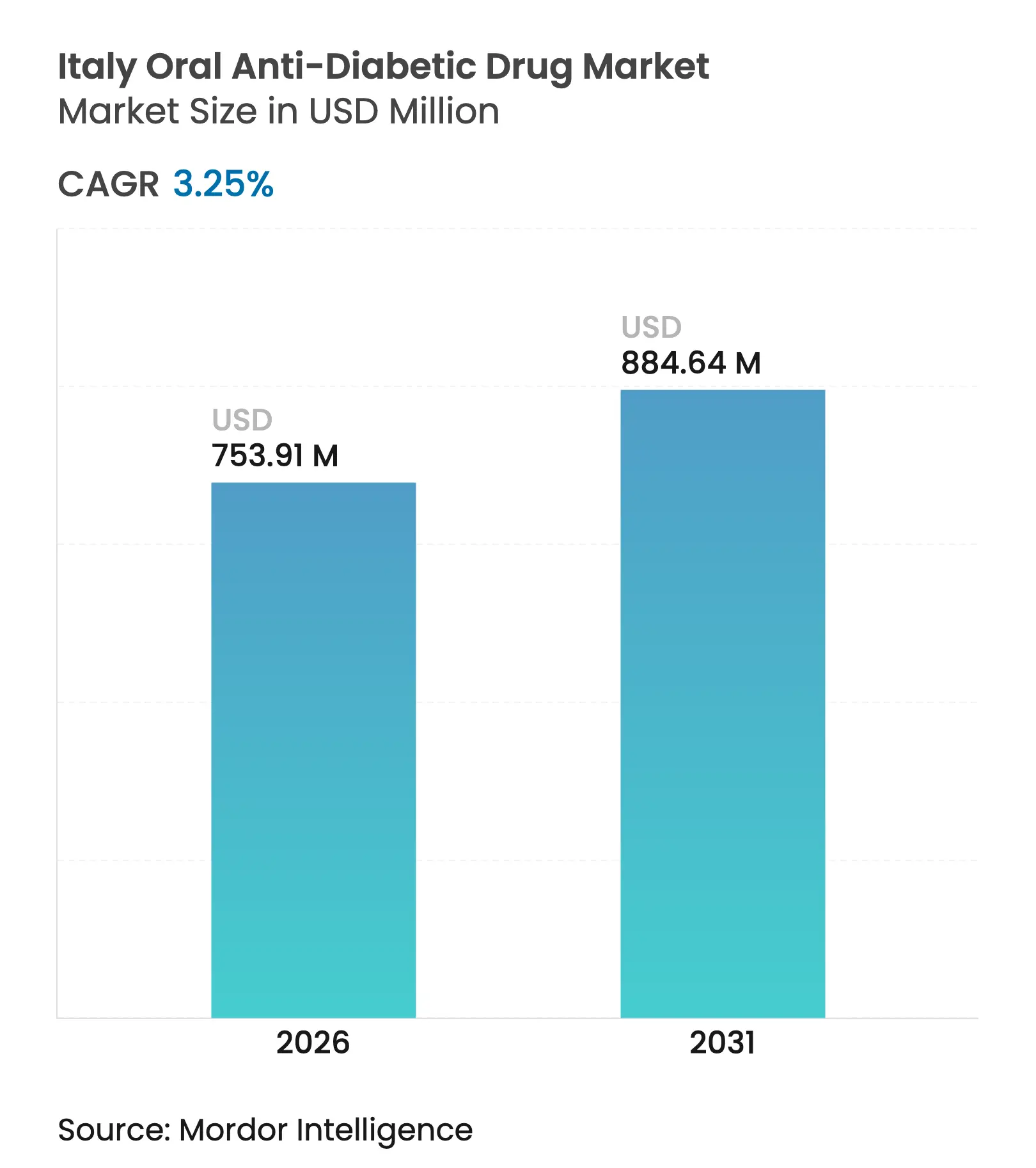

| Market Size (2026) | USD 753.91 Million |

| Market Size (2031) | USD 884.64 Million |

| Growth Rate (2026 - 2031) | 3.25 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

Italy oral anti-diabetic drug market size in 2026 is estimated at USD 753.91 million, growing from 2025 value of USD 730.17 million with 2031 projections showing USD 884.64 million, growing at 3.25% CAGR over 2026-2031. Current expansion is modest compared with wider European growth because AIFA still enforces some of the continent’s most restrictive price ceilings [1]Agenzia Italiana del Farmaco, “Rapporto Nazionale OsMed 2024,” aifa.gov.it , reference pricing rules and regional budget caps. Adoption of outcome-focused classes—especially SGLT-2 inhibitors and GLP-1 receptor agonists—continues, yet uptake is tempered by periodic supply shortages and by reimbursement negotiations that squeeze manufacturer margins. Market penetration of premium agents nevertheless accelerates in specialist diabetes centers as prescribers pivot toward cardio-renal benefits, and digital health tools start to close persistent adherence gaps. These factors collectively shape a competitive landscape in which long-established metformin dominance co-exists with rapid gains for newer classes, while looming patent expiries open space for generics to claim share.

Key Report Takeaways

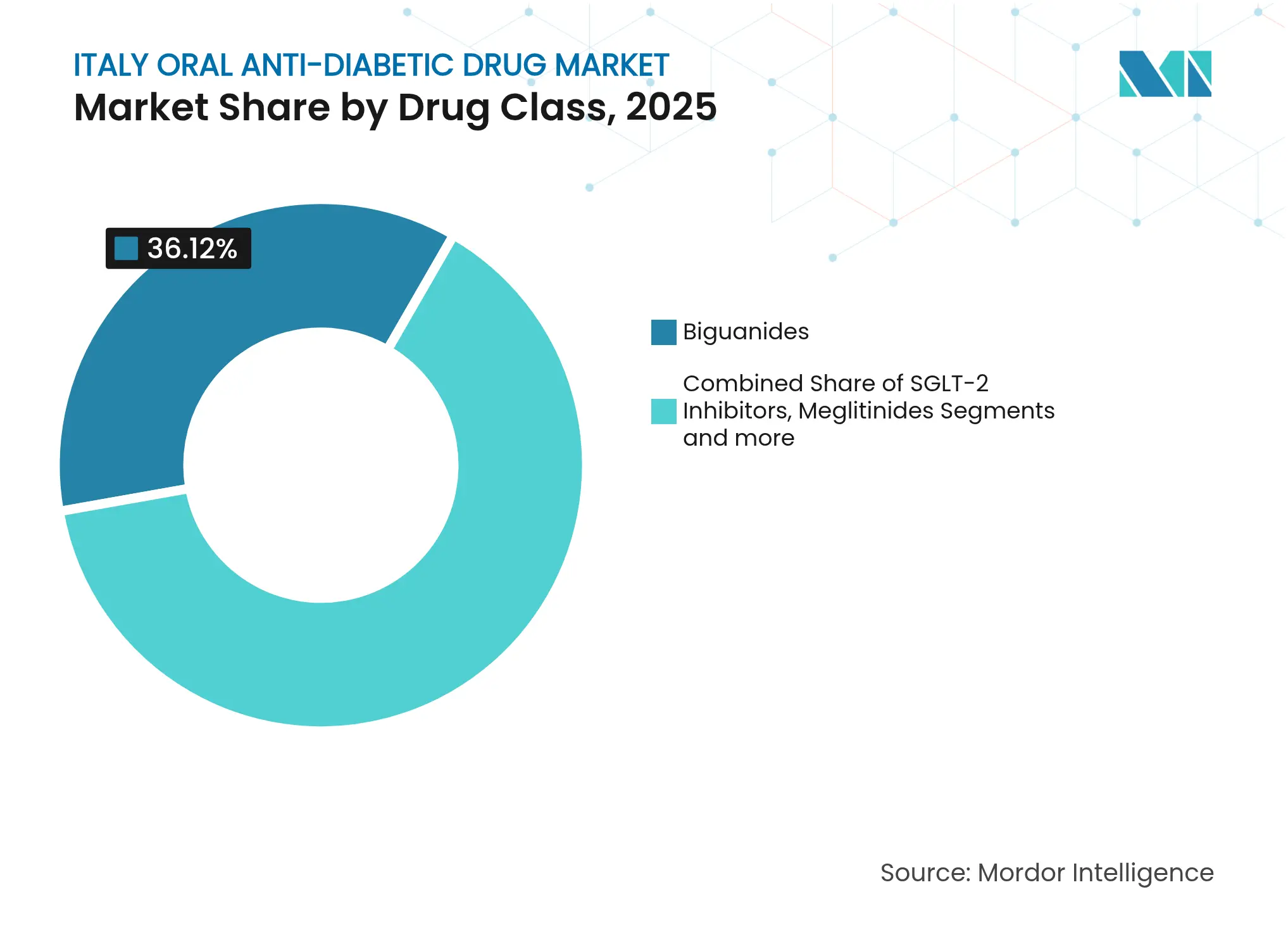

- By drug class, biguanides led with 36.12% of the Italy oral anti-diabetic drug market share in 2025, whereas SGLT-2 inhibitors are projected to post the highest 3.85% CAGR through 2031.

- By age group, adults held 66.20% of the Italy oral anti-diabetic drug market size in 2025; the geriatric segment shows the strongest 3.88% CAGR to 2031.

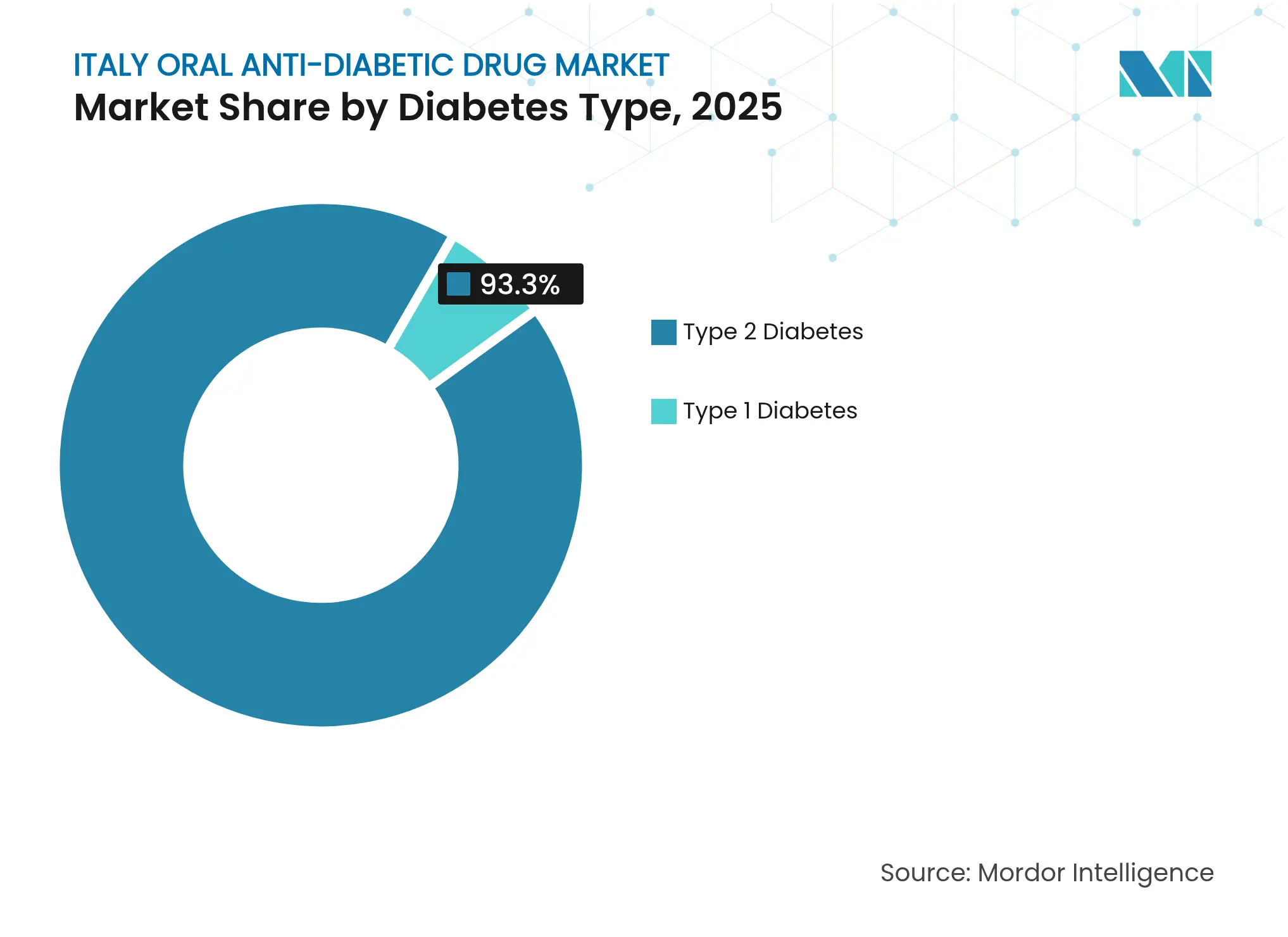

- By diabetes type, Type 2 diabetes accounted for 93.30% of the Italy oral anti-diabetic drug market size in 2025 and is set to expand at a 4.05% CAGR.

- By distribution channel, hospital pharmacies captured 66.90% revenue share in 2025, while online pharmacies are advancing at a 4.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of T2DM & pre-diabetes

Rising prevalence of T2DM & pre-diabetes

| +0.8% | National, concentrated in southern regions | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

National, concentrated in southern regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

Widening reimbursement for SGLT-2 / DPP-4 classes

Widening reimbursement for SGLT-2 / DPP-4 classes

| +0.6% | National, with regional implementation variations | Medium term (2-4 years) | |||

Shift to cardio-renal outcome-driven prescribing

Shift to cardio-renal outcome-driven prescribing

| +0.5% | National, led by specialized diabetes centers | Medium term (2-4 years) | |||

Fixed-dose combo generics post-2026 patent cliff

Fixed-dose combo generics post-2026 patent cliff

| +0.4% | National, stronger impact in price-sensitive regions | Long term (≥ 4 years) | |||

Tele-prescription platforms boosting adherence

Tele-prescription platforms boosting adherence

| +0.3% | National, accelerated in northern regions | Short term (≤ 2 years) | |||

Pharma–retail data-sharing for micro-targeting

Pharma–retail data-sharing for micro-targeting

| +0.2% | National, concentrated in urban areas | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of T2DM & Pre-Diabetes

Type 2 diabetes affects more than 3.5 million Italians, or 6.4% of the population, and annual healthcare costs stand at EUR 20.3 billion. An aging demographic intensifies demand, with people aged ≥ 65 driving over 60% of pharmaceutical spend despite representing a smaller share of the population. Southern regions such as Puglia record notably higher incidence and mortality, signalling sizeable unmet therapeutic need that keeps the Italy oral anti-diabetic drug market on a steady growth path. Persistent epidemiological pressure underpins long-term drug volume expansion, largely independent of near-term pricing restraints.

Widening Reimbursement for SGLT-2 / DPP-4 Classes

AIFA’s 2025 innovative-drug list added tirzepatide, underscoring a willingness to reimburse novel dual agonists once cost–benefit thresholds are met [2]Agenzia Italiana del Farmaco, "Innovative medicines list: AIFA publishes March 2025 update," aifa.gov.it . Broader cardiovascular and renal indications now underpin the reimbursement of established SGLT-2 agents such as empagliflozin, with economic modelling showing hospital-event offsets that achieve budget neutrality. As reimbursement couplings shift from simple glycaemic benefit to total-outcome value, prescribers gain confidence to switch suitable patients, which accelerates premium-class uptake across the Italy oral anti-diabetic drug market.

Shift to Cardio-Renal Outcome-Driven Prescribing

Italian guidelines published in 2024 put SGLT-2 inhibitors and GLP-1 receptor agonists ahead of sulfonylureas for second-line therapy due to proven cardiovascular benefit. Evidence from major CVOT trials continues to show empagliflozin, semaglutide and tirzepatide cutting MACE in high-risk cohorts, which has re-framed specialist decision-making [3]Oliver Schnell, "CVOT summit report 2024: new cardiovascular, kidney, and metabolic outcomes," Cardiovascular Diabetology, cardiab.biomedcentral.com. Regional diabetes networks, notably in Marche and Veneto, employ integrated electronic records to track clinical outcomes in real time, reinforcing the pivot toward therapies that deliver organ protection alongside glycaemic control. This shift boosts the Italy oral anti-diabetic drug market by favouring classes with higher per-script value.

Fixed-Dose Combo Generics Post-2026 Patent Cliff

Patents shielding key combinations such as Janumet start to expire from 2026 onward, providing space for generics in a market where generic share of diabetes expenditure is only 19%. AIFA’s reference-price model means generic entry typically halves branded prices within a year, so payers in southern regions are expected to adopt low-cost alternatives quickly. Multinationals like Teva and Viatris, together with Indian firms, have filed dossiers to launch combination generics that simplify dosing and improve adherence. As these launches proceed, price elasticity is likely to reshape segment hierarchies across the Italy oral anti-diabetic drug market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price controls & regional spending caps (AIFA)

Price controls & regional spending caps (AIFA)

| –0.7% | National, stronger impact in budget-constrained regions | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

–0.7%

|

Geographic Relevance

:

National, stronger impact in budget-constrained regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

Supply shortages of GLP-1 / dual incretin stocks

Supply shortages of GLP-1 / dual incretin stocks

| –0.4% | National, affecting all distribution channels | Short term (≤ 2 years) | |||

Persisting preference for legacy sulfonylureas

Persisting preference for legacy sulfonylureas

| –0.3% | National, concentrated in primary care settings | Medium term (2-4 years) | |||

Low generic penetration vs EU average

Low generic penetration vs EU average

| –0.2% | National, particularly in northern regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Price Controls & Regional Spending Caps (AIFA)

Italy’s transparency list locks reference prices across regions, while mandatory pharmacy and manufacturer discounts cut realised unit revenue below list levels. Local health enterprises set fixed departmental budgets that compel physicians to meet diabetic-drug targets within capped allocations. These mechanisms restrict headroom for premium innovation and dampen the Italy oral anti-diabetic drug market’s value growth despite rising volume.

Supply Shortages of GLP-1 / Dual Incretin Stocks

Recurrent shortages of semaglutide and liraglutide have prompted AIFA to limit new initiations and instruct physicians to prioritise existing users. Substitution toward SGLT-2 or DPP-4 classes meets short-run needs but risks locking in alternative regimens. If production delays persist into 2026, GLP-1 volume recovery could lag, muting the premium segment’s contribution to the Italy oral anti-diabetic drug market over the next two years.

Segment Analysis

By Drug Class: SGLT-2 Inhibitors Lead Innovation Despite Biguanide Dominance

The Italy oral anti-diabetic drug market size for biguanides stood at USD 263.74 million in 2025, equal to 36.12% of total value. Metformin’s entrenched first-line status, low cost and extensive post-marketing evidence keep it central to treatment algorithms. However, SGLT-2 inhibitors posted the fastest 3.85% CAGR and reached USD 123.08 million in 2025 as cardiologists and nephrologists now recommend their use regardless of baseline HbA1c. Sulfonylurea prescriptions have dropped steadily, falling to 12.9% of oral diabetes scripts in 2024, as hypoglycaemia and weight-gain risks drive switching toward safer alternatives.

Balancing cost pressures and efficacy needs, Italian prescribers now sequence agents according to comorbidity profile rather than strict glucose thresholds. DPP-4 inhibitors retain a stable niche for elderly patients intolerant to SGLT-2–related diuresis, while α-glucosidase inhibitors remain limited to post-prandial spikes. Dual and triple agonists such as tirzepatide already feature in tertiary-care protocols and could redefine the premium end of the Italy oral anti-diabetic drug market once supply stabilises.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Segment Drives Growth Amid Adult Dominance

Adults represented USD 483.37 million or 66.20% of the Italy oral anti-diabetic drug market size in 2025, reflecting high prevalence among working-age cohorts. Yet spending on patients aged ≥ 65 increased fastest at a 3.88% CAGR, taking the segment to USD 195.26 million. Elderly Italians incur more comorbidities and complex regimens, lifting per-patient drug costs almost twofold versus younger adults. Digital-health pilots in Lombardy show that remote glucose monitoring raises adherence to 78% in geriatric users compared with 66% on standard care, highlighting technology’s role in closing outcome gaps.

Long-acting oral molecules and once-weekly injectables fit geriatric adherence patterns, and AIFA’s rapid approval of weekly insulin icodec underscores regulatory support for simplified regimens. Because older patients contribute disproportionately to hospitalisations, regional payers increasingly view higher upfront drug costs as acceptable if they avert expensive complications, further enlarging the geriatric slice of the Italy oral anti-diabetic drug market.

By Diabetes Type: Type 2 Dominance Reflects Epidemiological Reality

Type 2 diabetes accounted for 93.30% of Italy oral anti-diabetic drug market share in 2025, equivalent to USD 680.25 million, and is forecast to rise at a 4.05% CAGR through 2031. Worsening obesity rates in Sicily, Campania and Calabria accelerate incident cases, while earlier onset among younger adults expands lifetime drug exposure. Advanced kidney disease and neuropathy prevalence make cardio-renal protective classes essential, boosting demand for SGLT-2 inhibitors within this dominant segment.

Type 1 diabetes remains a small share but exhibits therapeutic innovation. Pilot studies in Emilia-Romagna are evaluating adjunct GLP-1 therapy alongside insulin to flatten glycaemic variability. Success here could modestly enlarge the total addressable portion of the Italy oral anti-diabetic drug market, although the bulk of value will still trace to Type 2 patients for the foreseeable future.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Emerge Despite Hospital Dominance

Hospital pharmacies dispensed USD 488.48 million in 2025, equal to 66.90% of the Italy oral anti-diabetic drug market. Specialist prescribing and mandatory hospital follow-up for advanced cases concentrate volumes in hospital formularies. However, online channels recorded a 4.06% CAGR, accelerating after the pandemic normalised e-prescribing. Portals such as Farmaè routinely bundle antidiabetics with testing supplies and deliver to remote regions within 24 hours, broadening access where brick-and-mortar density is low.

Retail community pharmacies still anchor chronic-care medicine supply, yet their share is declining as tele-medicine and e-refill tools integrate directly with digital pharmacies. The National Recovery and Resilience Plan funds ePrescription modules that will allow seamless physician-to-patient transmission, potentially lifting the online share of the Italy oral anti-diabetic drug market to double digits before decade end.

Geography Analysis

Regional differences in prevalence, economic capacity and care integration drive mixed performance across the Italy oral anti-diabetic drug market. Northern regions enjoy higher GDP per capita and invest more in multidisciplinary diabetes pathways. Veneto’s PDTA scheme links primary care with 47 specialist centres; early data show a 13% fall in diabetes-related hospital stays since 2023. Lombardy’s digital-health pilots use shared records to flag cardio-renal risk and have lifted SGLT-2 uptake to 28% of new scripts, versus a national average of 19%.

Central Italy exhibits intermediate metrics. Tuscany combines robust hospital networks with primary-care engagement, yet variation persists across local health enterprises. Lazio reports higher generic adoption than the south but still lags industrialised north-east provinces. The central belt therefore offers scope for both premium-class expansion and value-brand penetration, depending on local budget leeway.

Southern Italy shoulders the heaviest epidemiological burden while allocating fewer euros per diabetic patient. Puglia cites 73 diabetes-related deaths daily and forecasts prevalence doubling by 2050. Resource constraints keep metformin and sulfonylureas common, yet AIFA’s uniform pricing means innovative classes remain accessible once clinicians demonstrate cost-offsets. Supply chains favour northern production hubs, but the Novo Nordisk fill-finish facility in Anagni (Lazio) due online in 2026 will add redundancy that benefits southern distribution, potentially easing shortages and lifting segment value across all geographies of the Italy oral anti-diabetic drug market.

Competitive Landscape

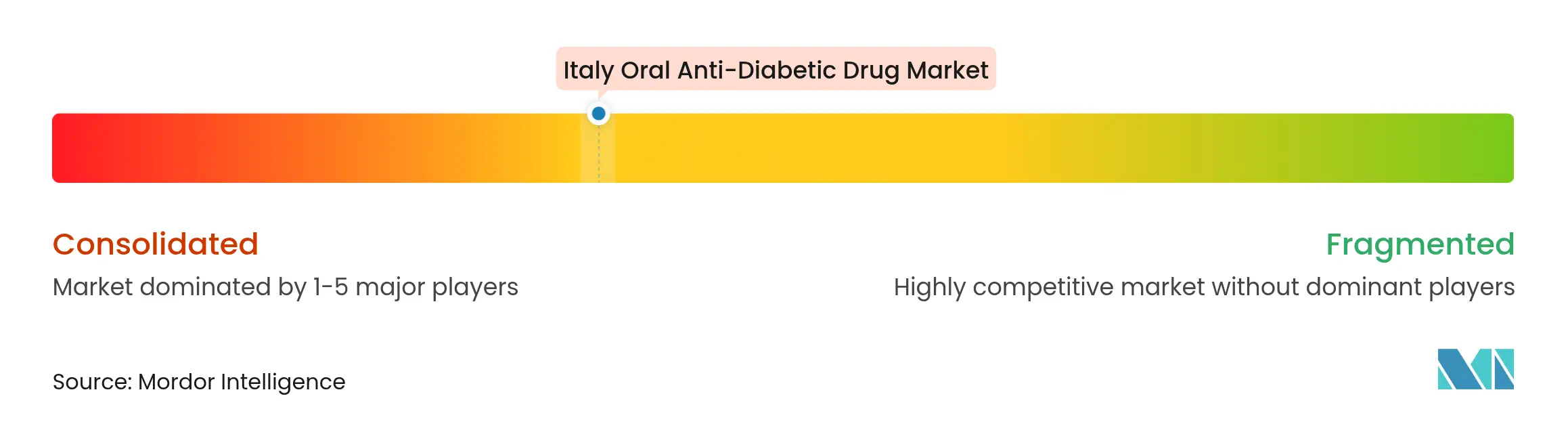

Market Concentration

Italy’s oral segment is moderately consolidated. Novo Nordisk leads globally and locally, commanding 55.1% of GLP-1 revenue through Ozempic and Rybelsus. Its portfolio breadth—from human insulin to oral semaglutide—creates strong physician loyalty. Eli Lilly challenges with tirzepatide; early Italian launch sales rose 52.3% year-on-year in 2025 as endocrinologists embraced superior HbA1c and weight-loss data.

AstraZeneca positions dapagliflozin at the heart of its cardio-renal strategy and advances an oral GLP-1 candidate, AZD5004, that delivered 5.8% weight reduction after four weeks in Phase I. Merck bolstered its presence by acquiring Molteni Pharma, securing local manufacturing and distribution leverage for its DPP-4 franchise. Generics players prepare for post-2026 opportunities: Teva and Viatris have submitted bioequivalence packages covering sitagliptin-metformin combinations, while Italian generics consortium Alfasigma expands capacity in Emilia-Romagna.

Digital-therapeutic partnerships add a new competitive layer. Novo Nordisk co-develops an AI-based adherence app with Milan-based PatchAi, while Lilly funds telemonitoring pilots in Bologna. Companies integrating drug and data services are better placed to satisfy AIFA’s real-world outcome tracking requirements, a trend that could re-order rankings in the Italy oral anti-diabetic drug market over the next five years.

Italy Oral Anti-Diabetic Drug Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AIFA added tirzepatide to its innovative-drug list, broadening access to dual GIP/GLP-1 therapy for inadequately controlled Type 2 diabetes.

- July 2024: Trilantic Europe and Alto Partners merged Doppel Farmaceutici and Mipharm to create Domixtar Pharmaceuticals, boosting local CDMO capacity for antidiabetic generics.

- February 2024: Novo Nordisk purchased a fill-finish site in Anagni as part of an USD 11 billion capacity expansion for diabetes and obesity drugs, with production slated for 2026.

Table of Contents for Italy Oral Anti-Diabetic Drug Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence of T2DM & Pre-Diabetes

- 4.2.2Widening Reimbursement For SGLT-2 / DPP-4 Classes

- 4.2.3Shift To Cardio-Renal Outcome-Driven Prescribing

- 4.2.4Fixed-Dose Combo Generics Post-2026 Patent Cliff

- 4.2.5Tele-Prescription Platforms Boosting Adherence

- 4.2.6Pharma-Retail Data-Sharing for Micro-Targeting

- 4.3Market Restraints

- 4.3.1Price Controls & Regional Spending Caps (AIFA)

- 4.3.2Supply Shortages Of GLP-1/Dual Incretin Stocks

- 4.3.3Persisting Preference for Legacy Sulfonylureas

- 4.3.4Low Generic Penetration Vs EU Average

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Consumers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitute Products & Services

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Drug Class

- 5.1.1Biguanides

- 5.1.2Sulfonylureas

- 5.1.3Meglitinides

- 5.1.4Thiazolidinediones

- 5.1.5Alpha-Glucosidase Inhibitors

- 5.1.6DPP-4 Inhibitors

- 5.1.7SGLT-2 Inhibitors

- 5.1.8Others

- 5.2By Age Group

- 5.2.1Adults

- 5.2.2Pediatric

- 5.2.3Geriatric

- 5.3By Diabetes Type

- 5.3.1Type 1 Diabetes

- 5.3.2Type 2 Diabetes

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Novo Nordisk

- 6.3.2Merck & Co.

- 6.3.3AstraZeneca

- 6.3.4Boehringer Ingelheim

- 6.3.5Johnson and Johnson

- 6.3.6Eli Lilly

- 6.3.7Takeda

- 6.3.8Sanofi

- 6.3.9Astellas

- 6.3.10Bristol Myers Squibb

- 6.3.11Novartis

- 6.3.12Pfizer

- 6.3.13Berlin-Chemie / Menarini

- 6.3.14Recordati

- 6.3.15Teva Pharmaceuticals

- 6.3.16Mylan (Viatris)

- 6.3.17Sun Pharma

- 6.3.18Lupin

- 6.3.19Servier

- 6.3.20Zentiva

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Italy Oral Anti-Diabetic Drug Market Report Scope

Orally administered antihyperglycemic drugs reduce blood glucose levels. The medications function by boosting the release of insulin from the pancreas, improving the body's response to insulin, or delaying the absorption of glucose in the intestines after meals. The Italy Oral Anti-Diabetic Drug Market is segmented into drugs. The report offers the value (in USD) and volume (in Units) for the above segments.