India Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

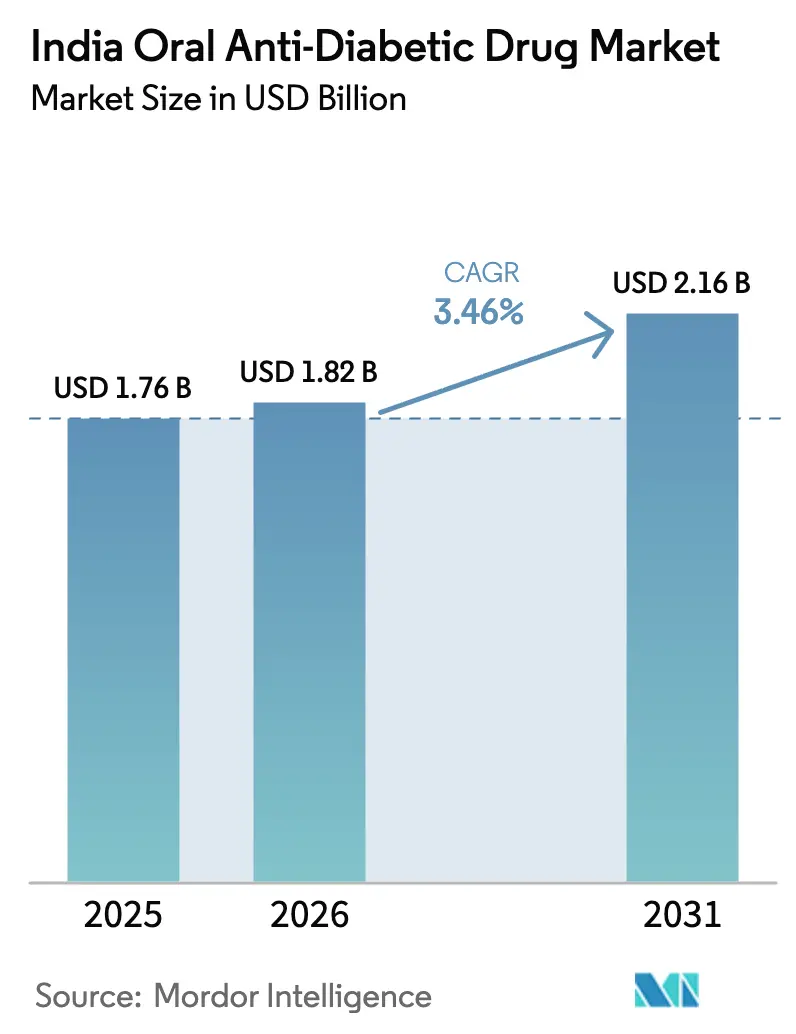

| Base Year Market Size (2025) | USD 1.76 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

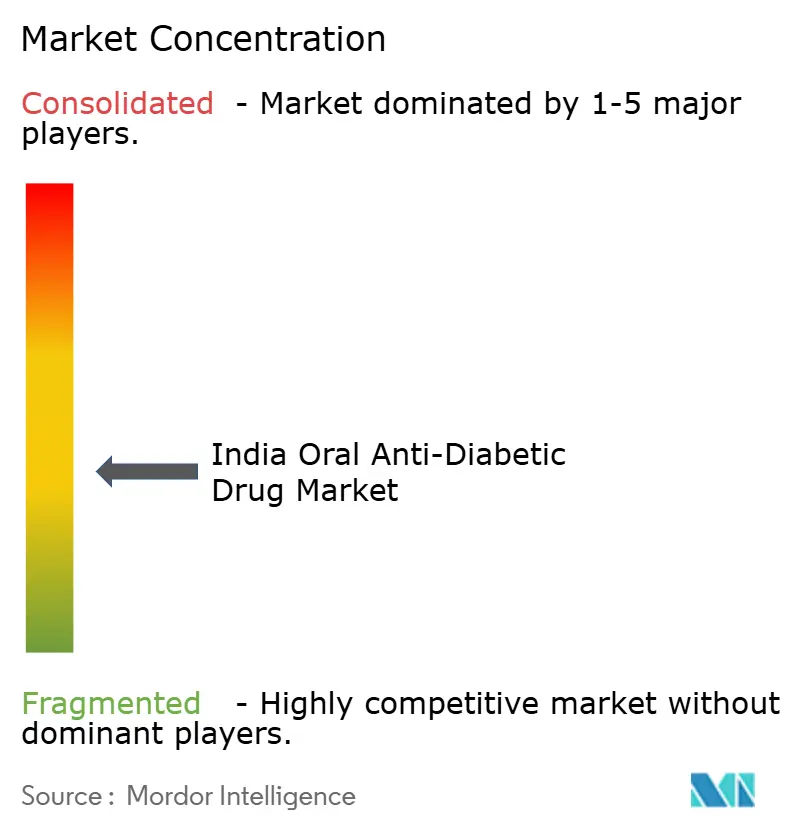

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The India oral anti-diabetic drug market size was valued at USD 1.76 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 2.16 billion by 2031, at a CAGR of 3.46% during the forecast period (2026-2031). The sales trajectory is shaped by a mix of patent expiries, intensified generic competition, government price controls and a domestic manufacturing push that is lowering average treatment costs while broadening patient access. Rapid urbanisation, the growing burden of type 2 diabetes mellitus (T2DM), and rising acceptance of digital pharmacies are sustaining prescription volume growth even as unit prices fall. Multinational innovator brands are responding with differentiated fixed-dose combinations (FDCs) and once-daily novel classes aimed at adherence improvement, yet price-sensitive buyers increasingly opt for trade generics and Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) outlets. Meanwhile, the Production-Linked Incentive (PLI) scheme is adding local capacity for critical active pharmaceutical ingredients (APIs), reducing import dependence and reinforcing supply-chain resilience.

Key Report Takeaways

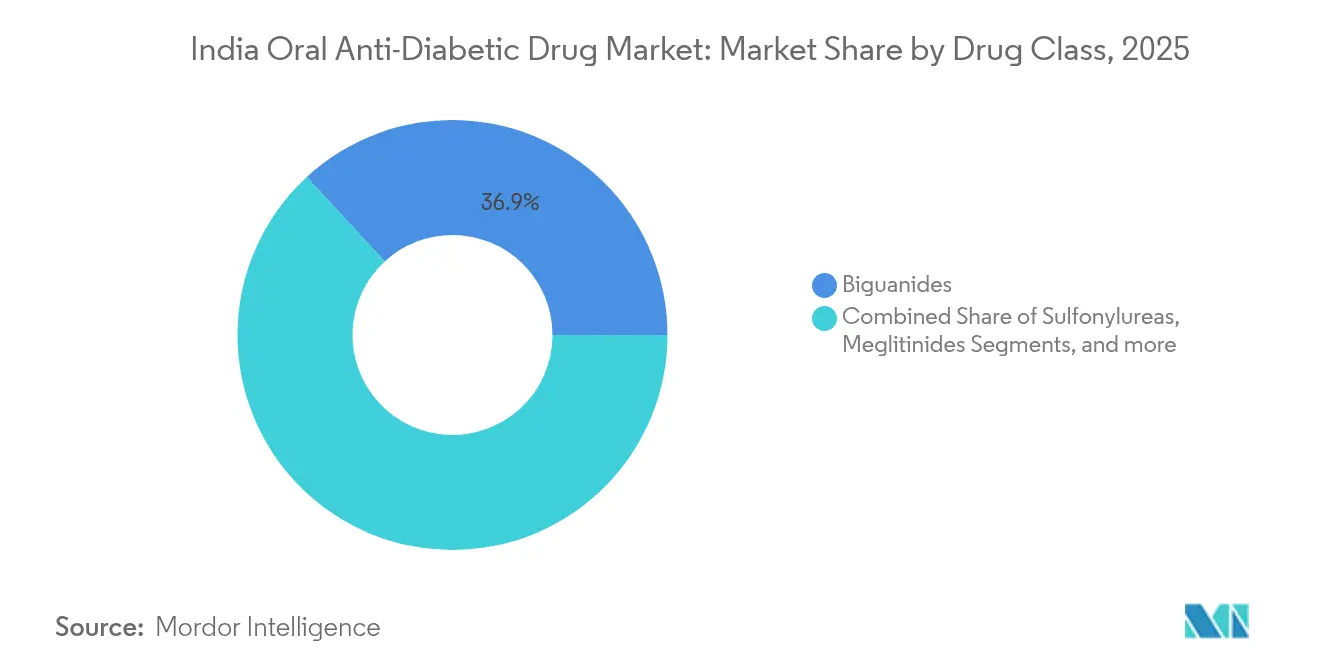

- By drug class, Biguanides led with 36.85% of India oral anti-diabetic drug market share in 2025; SGLT-2 inhibitors are projected to expand at a 3.79% CAGR through 2031.

- By age group, adults held 67.05% share of the India oral anti-diabetic drug market size in 2025, whereas the geriatric cohort is poised for the fastest 3.94% CAGR to 2031.

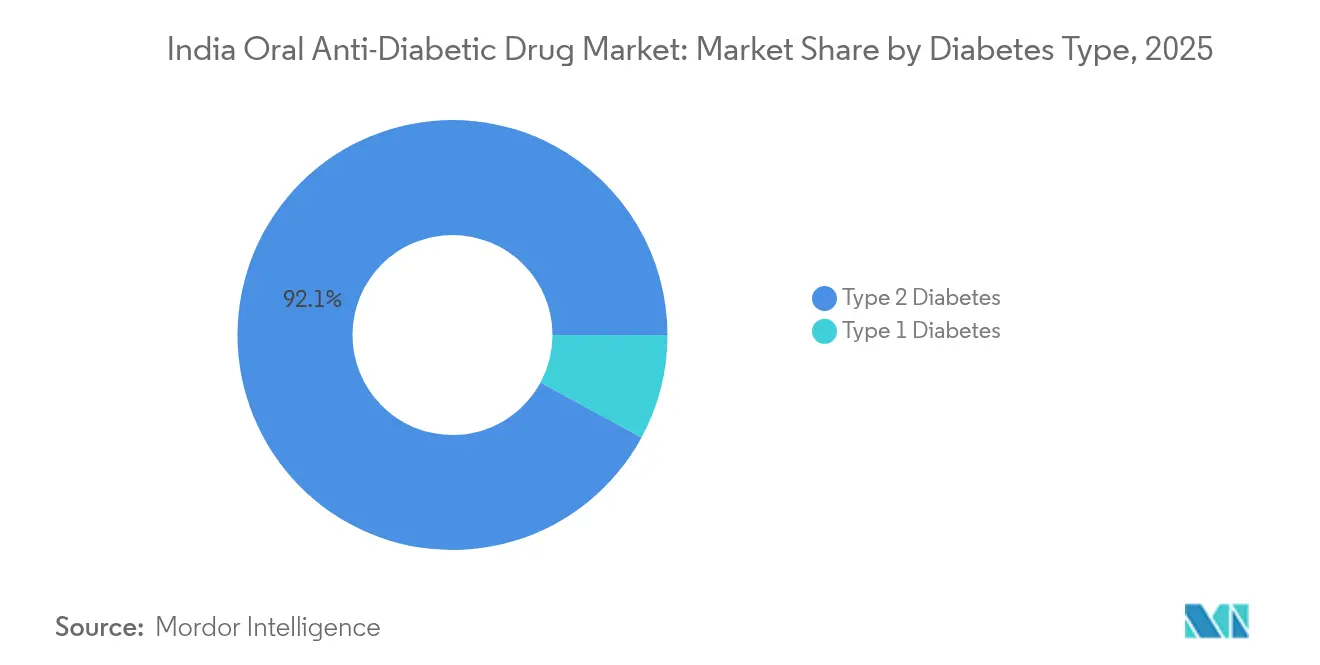

- By diabetes type, type 2 diabetes accounted for 92.10% of the India oral anti-diabetic drug market in 2025 and is forecast to maintain a 3.62% CAGR through 2031.

- By distribution channel, hospital pharmacies commanded 66.05% of 2025 revenues, while online pharmacies are advancing at a 4.29% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with India being one of the contributors. Our global oral anti-diabetic drugs market size represents that cumulative total.

India Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of T2DM & pre-diabetes | +1.2% | National, higher in urban centres | Long term (≥ 4 years) |

| Patent expiries driving rapid generic penetration | +0.8% | National, immediate impact in metro cities | Short term (≤ 2 years) |

| PLI scheme for diabetes APIs/formulations | +0.6% | National, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Surge in FDCs & once-daily novel classes (SGLT-2, DPP-4) | +0.4% | Urban and semi-urban markets | Medium term (2-4 years) |

| Digital-first pharmacy expansion in Tier-2-4 cities | +0.3% | Tier-2, Tier-3 and rural markets | Medium term (2-4 years) |

| Pharmacogenomic-guided dosing pilots in tertiary centres | +0.2% | Metro cities and medical college hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of T2DM & Pre-Diabetes

India hosts 77 million individuals with diabetes and projections indicate 134 million cases by 2045. Urban blood-glucose screening campaigns reveal that 49.43% of tested adults show abnormal values and 27.18% already meet diabetic thresholds. Lucknow prevalence data record 15.8% urban versus 11.7% rural incidence, underscoring market opportunities beyond metros. Annual diabetes-linked healthcare costs exceed USD 5 billion, and poorer households devote up to 23.7% of income to disease management. These epidemiological realities drive consistent therapy demand, though the India oral anti-diabetic drug market grows at a measured pace given rising generic penetration and price caps.

Patent Expiries Accelerating Generic Launches

Empagliflozin’s March 2025 patent cliff spurred an influx of 147 generic brands, doubling market participants within a month. Generic tablets retail at INR 5.49 compared with the innovator’s INR 59, unleashing 80-90% price erosion. Upcoming expiries—Semaglutide (Jan 2026) and Sitagliptin/Metformin FDCs (Jul 2029)—promise sustained openings for domestic formulators. Multinationals respond by bundling cardiovascular-renal claims and co-packaged devices to justify premium positioning. Rapid genericisation democratises access while rewiring competitive dynamics across the India oral anti-diabetic drug market.

PLI Scheme Boosting Diabetes API Output

PLI incentives have mobilised INR 1.61 lakh crore in pharma investment, generating production of INR 14 lakh crore across 764 approved projects [1]Ministry of Commerce and Industry, "PLI scheme incentivizes domestic manufacturing, increases production, creates new jobs and boosts exports," pib.gov.in. Thirty-two diabetes-relevant API ventures worth INR 4,024 crore are operational, targeting 41 bulk drugs, including Metformin and Dapagliflozin intermediates. The policy reduces import reliance, which had hovered near 70%, and lays groundwork for exporting next-generation formulations post-2026 expiries. Greenfield bulk-drug parks, power-reliable manufacturing clusters and single-window clearances accelerate capacity commissioning, enhancing supply security throughout the India oral anti-diabetic drug market.

Surge in FDCs & Once-Daily Novel Classes

Physician adoption of DPP-4 inhibitors rose from 48.9% to 61.2% within two years as hypoglycaemia risk and weight neutrality influence prescribing. The SGLT-2 inhibitor segment, worth INR 3,235 crore, posts 25% annual growth owing to demonstrated cardio-renal benefits. Consensus guidelines from 94 cardiologists now favour early Dapagliflozin-Sitagliptin FDC initiation in high-risk patients [2]Ray, Soumitra, "Expert Opinion on Fixed Dose Combination of Dapagliflozin Plus Sitagliptin for Unmet Cardiovascular Benefits in Type 2 Diabetes Mellitus," Journal of Diabetology, journals.lww.com. Once-daily regimens improve adherence among semi-urban diabetics, 78% of whom skip self-monitoring because of cost or low awareness. Differentiated FDC portfolios thus provide competitive moats against immediate post-expiry price compression in the India oral anti-diabetic drug market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price of novel GLP-1 oral agents | -0.7% | Urban markets primarily, limited rural penetration | Medium term (2-4 years) |

| National price-control & trade-generic proliferation squeezing margins | -0.5% | National, affecting all market segments | Short term (≤ 2 years) |

| Patient drift to long-acting injectables/implants | -0.4% | Metro cities and Tier-1 urban centres | Medium term (2-4 years) |

| Extreme inter-brand price dispersion eroding prescriber confidence | -0.3% | National, particularly affecting rural and semi-urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price of Novel GLP-1 Oral Agents

Monthly therapy with oral Semaglutide costs INR 10,000, deterring widespread uptake in a market where generic Metformin costs under INR 100. Out-of-pocket spending dominates, as 80% of patients lack comprehensive insurance coverage. Clinical trials show 1.56% HbA1c reductions and 5 kg weight loss, yet cost-effectiveness remains negative for most households. Sales therefore remain confined to affluent urban cohorts until patent expiry-led generics emerge post-2026. The India oral anti-diabetic drug market thus balances clinical efficacy gains against affordability ceilings.

National Price-Control & Trade-Generic Squeeze

The National Pharmaceutical Pricing Authority fixed ceiling prices for 84 Empagliflozin SKUs and mandated 50% cuts for off-patent components in FDCs. Trade-generic launches surged once protective patents lapsed, intensifying discount wars that favour patients but slash manufacturer margins. Para 32 exemptions, enabling Indian Patent Office experts to shape pricing verdicts, inject regulatory uncertainty for innovators. Volume-led strategies dominate as brand equity erodes, prompting firms to re-engineer cost structures while preserving therapeutic quality across the India oral anti-diabetic drug market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biguanides Dominance Faces Novel-Class Disruption

Biguanides anchored by Metformin held 36.85% of India oral anti-diabetic drug market share in 2025. Empagliflozin’s patent expiry and rapid price erosion, however, redirected prescribers toward SGLT-2 inhibitors, the fastest-growing class with a 3.79% CAGR to 2031. Sulfonylureas are declining due to hypoglycaemia fears, while DPP-4 inhibitors widened adoption on safety merits. Alpha-glucosidase inhibitors and Meglitinides remain niche. Pharmacogenomic studies show higher prevalence of alleles linked to poor Metformin response among Indian patients, opening avenues for personalised dosing . The India oral anti-diabetic drug market size for SGLT-2 inhibitors is projected to reach USD 611.8 million by 2031, reflecting emerging therapeutic preferences. Novel dual SGLT-1/2 compounds and GLP-1 combinations in the development pipeline may further recalibrate shares as price-sensitive FDCs mature.

A confluence of cardiovascular-renal data and initial price drops is strengthening SGLT-2 molecule positioning. Domestic players with vertically integrated API capacity leverage PLI incentives to undercut imports while ensuring quality compliance. Innovator firms seek differentiation through outcome-based real-world studies, but generics already capture volume prescribing. Net-net, competitive intensity within drug classes is redefining value capture along the India oral anti-diabetic drug market.

By Age Group: Adult Stability Versus Geriatric Momentum

Adults generated 67.05% of 2025 prescriptions, yet their CAGR trails at 2.98% because of therapeutic maturity and slowing incidence growth in mid-life cohorts. The geriatric cohort shows a 3.94% CAGR driven by longevity gains and higher multi-morbidities requiring safer agents. India oral anti-diabetic drug market size for geriatrics is estimated at USD 427.6 million in 2025, growing as elderly pensioners turn to affordable Jan Aushadhi generics that cut monthly spend by 70%. Rural elderly patients face access gaps, but teleconsultation pilots in states such as Tamil Nadu are bridging follow-up care.

Polypharmacy challenges accelerate demand for weight-neutral, low-hypoglycaemia formulations. Digital adherence tools customised for large-font interfaces record 18% higher engagement among older users, underpinning incremental sales gains. Meanwhile, paediatric prescriptions remain low volume, yet research into Metformin add-on therapy to mitigate insulin resistance in type 1 adolescents highlights future niche expansion. Overall, demographic evolution ensures a steady patient pipeline within the India oral anti-diabetic drug market.

By Diabetes Type: Type 2 Dominance Shapes Therapeutic Evolution

Type 2 diabetes maintained 92.10% share of India oral anti-diabetic drug market in 2025 and advances at a 3.62% CAGR to 2031. Only 20.8% of T2DM patients currently achieve HbA1c < 7%, signalling substantial room for treatment intensification. Early combination therapy using DPP-4 or SGLT-2 inhibitors with Metformin is gaining traction. Regional discrepancies persist, with southern states exhibiting higher prevalence yet better control due to stronger primary care infrastructure. Digital therapeutics pilots report 1.2% incremental HbA1c reduction when paired with oral agents.

Type 1 diabetes accounts for a small share but commands higher per-patient spend owing to complex regimens. Research into immune-modulating oral agents suggests future convergence of therapy pathways. Overall, type 2 disease patterns continue to dictate formulary decisions, supply-chain planning, and public-health budgeting in the India oral anti-diabetic drug market.

By Distribution Channel: Hospital Pharmacies Lead as Online Channels Accelerate

Hospital pharmacies retained 66.05% revenue share in 2025 because prescribers favour in-house dispensing for long-term disease management. Yet online pharmacies log the fastest 4.29% CAGR on the back of smartphone penetration and e-commerce trust gains. India oral anti-diabetic drug market size within online channels is forecast to top USD 229.7 million by 2031, aided by e-pharmacy regulation that mandates CDSCO registration and secure cold-chain logistics. Retail chemists still serve Tier-2 and Tier-3 towns, where physical access matters and credit purchases dominate.

PMBJP’s 15,000 outlets expand generic reach at 50-80% lower prices and shift walk-in traffic from private retailers. Start-ups offering doorstep HbA1c tests bundle medication subscriptions, incentivising monthly auto-refills. Hospital chains counter by integrating tele-consults with pharmacy home-delivery, maintaining influence across the India oral anti-diabetic drug market.

Geography Analysis

Southern India registers the country’s highest diabetes prevalence, but its superior endocrinology infrastructure underpins higher drug uptake and adherence rates. Western metros such as Mumbai and Ahmedabad show swift adoption of SGLT-2 inhibitors after patent expiry, buoyed by cardiologist endorsement and early cardiovascular outcome trials. Northern Tier-2 cities, including Jaipur and Lucknow, reveal rising incidence yet remain predominantly Metformin-centric, owing to cost constraints.

Rural markets, still only 18% of national pharma sales as of 2025, lag in therapy intensity because of limited diagnostics, but government sub-centres and mobile medical vans are narrowing gaps. Telehealth platforms now reach remote Himalayan districts, overcoming geographical barriers and promoting continuity of oral therapy. The Ayushman Bharat programme has enabled 7.79 crore hospitalisations since launch and cuts out-of-pocket expenses by 21%, indirectly freeing disposable income for medicines.

Eastern and northeastern states battle logistics hurdles related to poor road connectivity and intermittent electricity that complicates pharmacy refrigeration. Producers are piloting solar-powered micro-warehouses paired with digital stock-tracking to reduce stockouts. Overall, evolving infrastructure, policy incentives and technology diffusion continue to widen geographic reach, enlarging patient pools for the India oral anti-diabetic drug market.

Coverage of the oral anti-diabetic drugs market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia, Latin America, and North America, alongside detailed country-level intelligence for Malaysia, South Korea, Brazil, Mexico, France, and Vietnam, each shaped by local operating conditions.

Competitive Landscape

Domestic manufacturers capture a decent share of national pharmaceutical volumes and rapidly erode premium price bands through early generic launches. Within weeks of Empagliflozin’s expiry, 37 local firms introduced products priced up to 90% cheaper than the innovator. Novo Nordisk and Eli Lilly still dominate premium GLP-1 segments, but Glenmark’s Lirafit biosimilar launch in March 2025 cut treatment cost by 70% and signalled intensifying biosimilar rivalry.

Strategically, local players leverage PLI-funded backward integration, API self-sufficiency and aggressive trade-generic branding to retain physician mindshare. Cipla’s USD 857 million war chest targets acquisitions in chronic therapeutics to widen its cardiometabolic portfolio. Innovators pursue differentiation via outcome-based contracts, patient-support apps and co-formulated once-weekly oral candidates. Meanwhile, AI-assisted drug discovery and pharmacogenomic screening partnerships emerge as future moats, shifting competition beyond simple cost vantage points.

Value migration is evident: gross margins compress but unit volumes spike, forcing firms to optimise supply chains, scale packaging automation and co-source distribution. Over 50 alliances between digital-health start-ups and pharma marketers formed in 2024-2025, pairing continuous glucose monitoring apps with medication discount coupons, thereby deepening customer retention. Competitive pressures are expected to intensify through 2030 as additional patent cliffs approach and rural channel expansion accelerates across the India oral anti-diabetic drug market.

India Oral Anti-Diabetic Drug Industry Leaders

-

Sanofi

-

Eli Lilly

-

Astellas

-

Astrazeneca

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eli Lilly reported Phase 3 data showing once-daily oral orforglipron matches injectable GLP-1 efficacy in T2DM patients.

- March 2025: Mankind Pharma introduced its low-cost Empagliflozin generic after patent expiry.

- March 2025: USV launched Xenia (Empagliflozin and combinations) to strengthen its INR 1,100 crore SGLT-2 inhibitor franchise.

- March 2025: Glenmark expanded its cardiometabolic line with Empagliflozin FDC brands Glempa, Glempa-L and Glempa-M.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India oral anti-diabetic drugs market as prescription and trade-generic small-molecule therapies administered by mouth for glycemic control in Type 1 and Type 2 diabetes patients. Covered classes include biguanides, sulfonylureas, meglitinides, thiazolidinediones, alpha-glucosidase inhibitors, DPP-4 inhibitors, and SGLT-2 inhibitors. Sales are tracked at manufacturer selling price and include branded and unbranded generics circulating through hospital, retail, and online pharmacies.

Scope exclusion: injectables such as insulin, GLP-1 analogs, devices, and nutraceuticals lie outside this market.

Segmentation Overview

-

By Drug Class

- Biguanides

- Sulfonylureas

- Meglitinides

- Thiazolidinediones

- Alpha-Glucosidase Inhibitors

- DPP-4 Inhibitors

- SGLT-2 Inhibitors

- Others

-

By Age Group

- Adults

- Pediatric

- Geriatric

-

By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Interviews with endocrinologists, hospital pharmacists, bulk-drug makers, and nationwide distributors helped us test prevalence estimates, generic uptake rates, and average selling prices. Respondents across Tier 1 cities and semi-urban clusters clarified channel mix shifts and impending patent-cliff impacts, enabling us to refine assumptions before locking the model.

Desk Research

Mordor analysts first compiled baseline inputs from authoritative, public datasets such as the Indian Council of Medical Research-INDIAB survey, International Diabetes Federation Atlas, NPPA ceiling-price notifications, CDSCO approval lists, and Ministry of Commerce trade statistics. These were cross-checked with peer-reviewed journals, Diabetes Foundation of India bulletins, and annual reports of leading pharma manufacturers. For financial sanity checks, we tapped paid repositories like D&B Hoovers for company revenue splits and Volza for shipment volumes. Additional context flowed from investor presentations, parliamentary questions on drug pricing, and reputable business dailies. The sources cited here are indicative; numerous other publications informed data validation.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that multiplies diagnosed patient pools by therapy penetration and weighted annual therapy cost, which are then reconciled with selective bottom-up checks from sampled manufacturer sales and pharmacy audit data. Key variables include diagnosed diabetes prevalence, generic share post-Empagliflozin patent expiry, NPPA price revisions, uptake of SGLT-2/DPP-4 classes, and the growing online pharmacy slice. A multivariate regression model projects each variable to 2030, referencing macro drivers such as urbanization rate and per-capita health spend. Gaps in supplier roll-ups are bridged through respondent-verified adjustment factors before final triangulation.

Data Validation & Update Cycle

Outputs pass variance screening against historical series, global price corridors, and quarterly corporate disclosures. Senior analysts perform anomaly reviews and, when deviations exceed preset thresholds, we recontact domain experts. The dataset is refreshed yearly, with interim updates triggered by material events like major patent lapses or policy price caps.

Why Our India Oral Anti-Diabetic Drug Market Baseline Commands Reliability

Published market values often differ; definitions, patient pools, and price assumptions rarely align.

We acknowledge this spread upfront and show below how Mordor's disciplined scope and refresh cadence deliver a balanced reference point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.76 B (2025) | Mordor Intelligence | - |

| USD 1.80 B (2024) | Global Consultancy A | Treats 2024 generics surge as structural, inflating forecast before validated price erosion |

| USD 1.70 B (2025) | Industry Tracker B | Excludes online-pharmacy turnover, understating total demand |

| USD 2.27 B (2023) | Regional Consultancy C | Bundles insulin-tablet combos and oral adjuncts, widening scope beyond pure oral drugs |

2023 figure covers the entire diabetes-drug basket, hence the higher value. The comparison shows that divergence stems mainly from scope creep, channel omissions, or premature extrapolation. By grounding estimates in verified prevalence, price-controlled ASPs, and patent-driven generic dynamics, Mordor Intelligence offers decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current value of the India oral anti-diabetic drug market?

The India oral anti-diabetic drug market stands at USD 1.82 billion in 2026 and is forecast to rise to USD 2.16 billion by 2031 at a 3.46% CAGR.

Which drug class is expanding fastest in India?

SGLT-2 inhibitors represent the fastest-growing class, posting a 3.79% CAGR through 2031 due to cardio-renal benefits and post-patent price reductions.

How are patent expiries influencing competition?

The March 2025 Empagliflozin patent cliff attracted 37 generic entrants within weeks and slashed retail prices by up to 90%, fundamentally reshaping competitive dynamics.

Why are online pharmacies gaining share in diabetes medicines?

Improved last-mile logistics, CDSCO e-pharmacy rules and smartphone adoption enable convenient home delivery, driving a 4.29% CAGR for online channels through 2031.

What government policies support domestic diabetes drug manufacturing?

The PLI scheme earmarks incentives for critical APIs, while bulk-drug parks and single-window approvals strengthen domestic capacity, lowering import dependence.

Are novel GLP-1 oral agents affordable for most Indian patients?

No. Current monthly therapy costs of roughly INR 10,000 limit uptake to affluent urban patients; generics post-2026 should reduce prices and widen access.

Page last updated on: