Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Adhesives Market Analysis by Mordor Intelligence

The Italy Adhesives Market size is projected to expand from USD 1.56 billion in 2025 and USD 1.64 billion in 2026 to USD 2.14 billion by 2031, registering a CAGR of 5.47% between 2026 and 2031. Packing-grade water-borne and hot-melt formulations surged on the back of e-commerce logistics that lifted corrugated-case output at new sites such as Progroup’s 200,000-tonne Cessalto mill. Construction-related volumes pivoted from subsidized home renovation to National Recovery and Resilience Plan infrastructure, redirecting demand toward polyurethane foams and silicone sealants. Automotive downturn weighed on total tonnage after Stellantis output fell 20% in 2025, yet electric-vehicle adoption preserved structural-epoxy and polyurethane uptake in battery assemblies. Meanwhile, volatile ethylene and propylene prices compressed margins for acrylic and VAE lines, steering formulators toward hedged feedstock contracts.

Key Report Takeaways

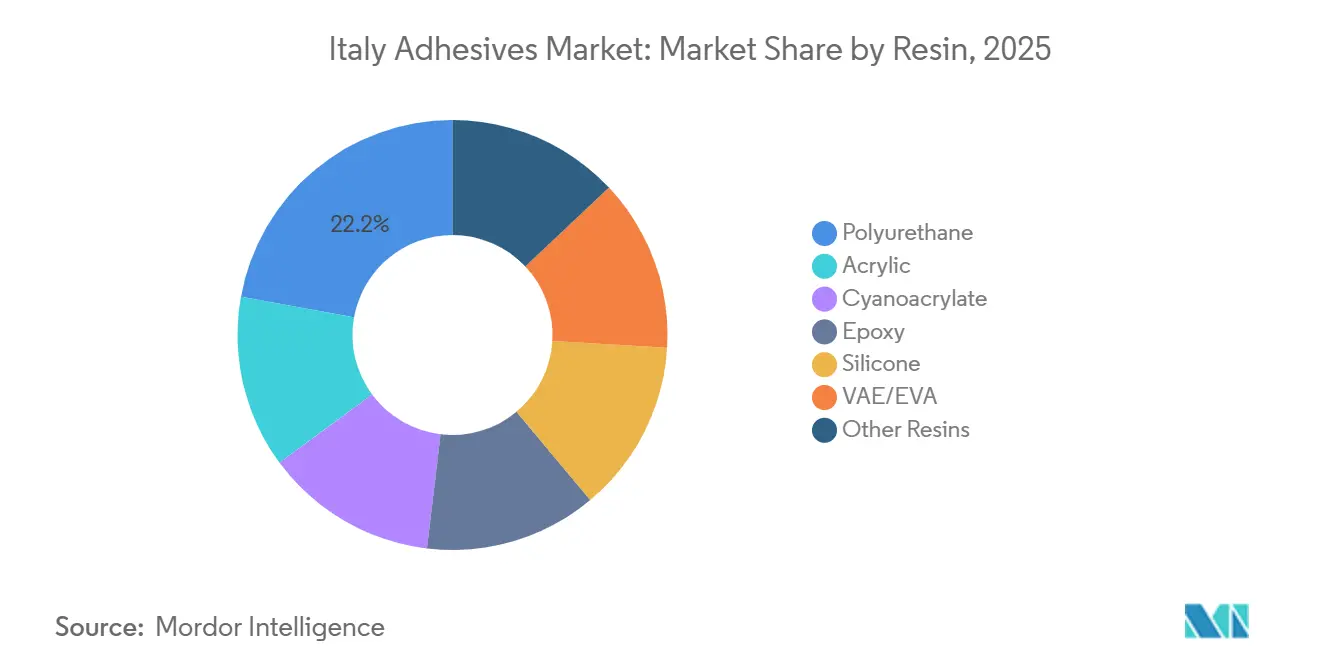

- By resin, polyurethane led with a 22.15% Italy Adhesives market share in 2025. VAE/EVA is forecast to expand at a brisk 6.47% CAGR through 2031, marking the fastest-growing resin family in the Italy Adhesives market.

- Water-borne technology held 54.18% of the Italy Adhesives market size in 2025. Hot-melt technology is expected to grow at a CAGR of 6.21% during the forecast period (2026-2031).

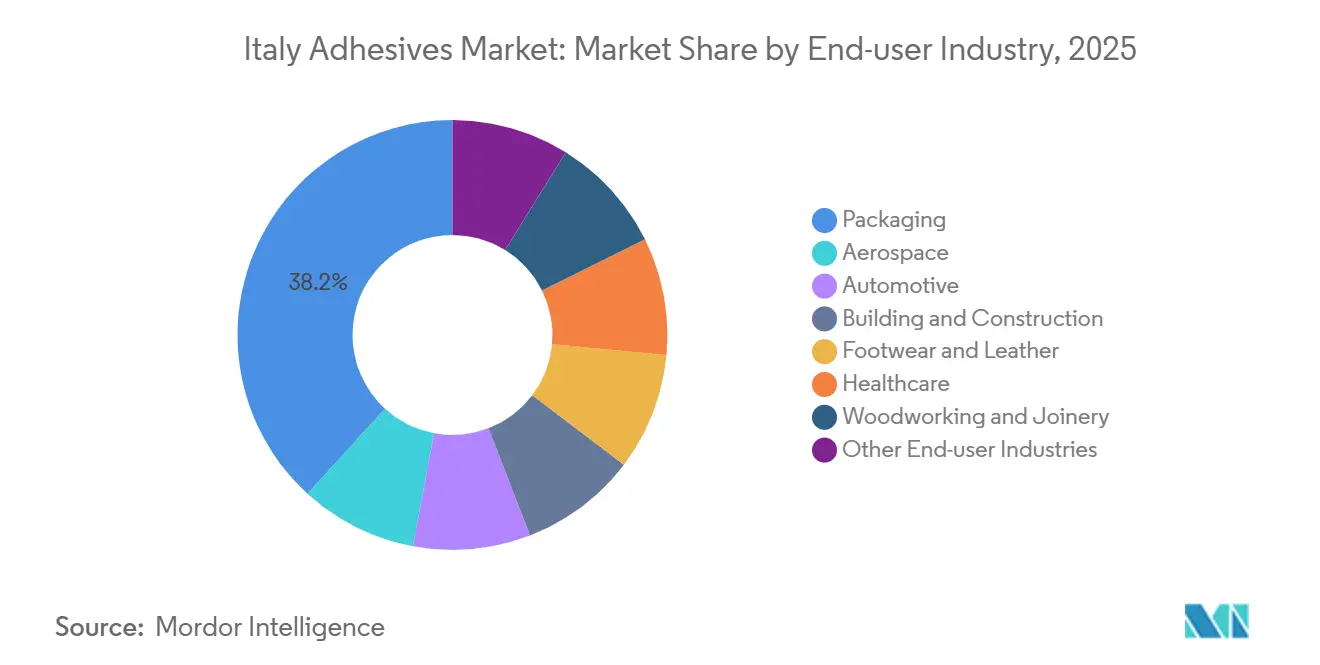

- Packaging end-users captured 38.22% of volume in 2025 and are projected to grow at 6.82% CAGR, the highest among all application segments in the Italy Adhesives market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce packaging boom | +1.2% | National, concentrated in Lombardy, Veneto logistics hubs | Short term (≤ 2 years) |

| EU Renovation Wave incentives | +0.9% | National, with emphasis on Southern Italy infrastructure | Medium term (2-4 years) |

| Automotive lightweighting and EV batteries | +0.7% | National, Piedmont and Emilia-Romagna automotive clusters | Medium term (2-4 years) |

| Low-VOC regulatory push (REACH/VOC) | +0.6% | EU-wide, Italy compliance-driven adoption | Long term (≥ 4 years) |

| Luxury-furniture export clusters | +0.5% | Brianza, Marche, Veneto furniture districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Packaging Boom

Italy’s fulfillment centers multiplied across Lombardy and Veneto during 2025, pulling corrugated output to record highs and lifting demand for water-borne starch blends and VAE emulsions that cure fast without contaminating food contact surfaces. Adoption of cold-seal hot-melts in confectionery wraps cuts energy use by 30% per linear meter, while mono-material paper laminates require specialized adhesives that resist delamination during pulping. Players owning pilot coaters and rheology labs gained share as brand owners enforced recyclability targets. Automated case-sealing lines further reinforced hot-melt traction, underpinning the upward trajectory of the Italy Adhesives market. Market leaders invested in bio-based tackifiers to future-proof supply chains against petrochemical volatility.

EU Renovation Wave Incentives

More than EUR 8.6 billion flowed into efficiency retrofits between 2021 and 2025, sustaining polyurethane foam and silicone sealant pull-through 2025[1]European Commission, “National Recovery and Resilience Plan Italy,” ec.europa.eu. When the Superbonus 110% incentive ended in January 2026, residential momentum faltered, but rail electrification, school seismic upgrades, and bridge rehabilitation stepped in under NRRP budgets. Epoxy structural adhesives and acrylic tapes now appear routinely in public-works specifications that stipulate 50-year durability. Domestic suppliers such as MAPEI expanded waterproofing lines to align with local-sourcing clauses, reinforcing regional competitiveness in the Italy Adhesives market.

Automotive Lightweighting and EV Batteries

Although Stellantis built only 379,706 units in 2025, Italian registrations of plug-in hybrids jumped 86.6% and battery-electrics 44%[2]ANFIA, “Automotive Production Statistics 2025,” anfia.it. EV architectures demand thermally conductive epoxies for pack potting and low-free-isocyanate polyurethanes like Sika Purform for glazing tasks, thereby buffering overall tonnage. Tier-1 suppliers deploy UV-cured acrylics for trim bonding to shorten takt times, while Huntsman and Dow compete on cure speed and coefficient-of-expansion alignment to aluminum housings. The pivot toward electrification, therefore, sustains higher-margin, high-performance chemistries inside the Italy Adhesives market.

Low-VOC Regulatory Push (REACH/VOC)

Since August 2023, every worker handling polyurethane with less than 0.1% free isocyanate must complete certified training, costing EUR 500-1,500 per employee. This burden steers small furniture shops toward water-borne polyurethane dispersions that avoid the mandate. EMICODE EC1 PLUS and EU Paints Directive limits jointly shape formulator roadmaps, accelerating stripping of residual monomers and migration toward silane-terminated polyethers that give similar strength without isocyanates. Compliance has become a marketing differentiator inside the Italy Adhesives market, helping multinationals lock in customers through bundled training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical raw-material volatility | -0.8% | Global, acute impact on Italian importers | Short term (≤ 2 years) |

| REACH diisocyanate training costs | -0.4% | EU-wide, concentrated in SME-heavy regions | Medium term (2-4 years) |

| Skilled-labour gap for robotic dispensing | -0.3% | National, Piedmont and Lombardy industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Raw-Material Volatility

Ethylene moved between USD 610 and USD 740 per tonne and propylene between USD 690 and USD 810 in early 2026, eroding margins for acrylic and VAE producers lacking hedges. Middle-East shipping disruptions lifted freight and insurance premiums, while the forthcoming BASF MDI expansion in Louisiana may not relieve Europe due to North-American off-take commitments. Smaller Italian formulators absorb shocks via delayed price passes, draining working capital and threatening just-in-time supply to packaging converters that underpin the Italy Adhesives market.

REACH Diisocyanate Training Costs

Compliance outlays run EUR 10,000 for a 10-person shop, swallowing sizeable chunks of the 7-12% operating margin typical in artisanal woodworking. Transition toward water-borne polyurethane dispersions and silane-terminated polyethers accelerates, while larger suppliers leverage in-house training centers, Henkel’s Bonding Process Center being a prime example, to convert regulation into customer lock-in.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Anchors Share, VAE/EVA Leads Growth

Polyurethane captured 22.15% of the Italy Adhesives market share in 2025 as its gap-filling and moisture-cure profile dominated windshield and insulation-panel lines. Sika Purform keeps free isocyanate under 0.1%, letting OEMs bypass REACH training. VAE/EVA is forecast to post a 6.47% CAGR through 2031, riding corrugated packaging gains and woodworking reversibility targets. The Italy Adhesives market size for these copolymers is projected to climb steadily as e-commerce volumes expand. Acrylic, epoxy, cyanoacrylate, and silicone niches persist, with REACH formaldehyde caps shrinking phenolic and urea-formaldehyde demand.

A second wave of innovation is reshaping product hierarchies. UV-cured acrylics bring sub-five-second curing to pressure-sensitive tapes, expanding their presence in automotive trim. Silane-terminated polyethers displace tin-catalyzed silicones in façade glazing by offering comparable weatherability minus organotin liabilities. Water-borne polyurethane dispersions such as Polynt Urotuf now achieve less than 30 g/L VOC, easily satisfying EMICODE EC1 PLUS and safeguarding share inside the Italy Adhesives market.

By Technology: Water-Borne Dominance Meets Hot-Melt Acceleration

Water-borne chemistries held 54.18% of the 2025 market share as European Union (EU) Paints Directive ceilings pressed converters to cut solvent. Hot-melts are catching up at 6.21% CAGR through 2031, owing to metallocene polyolefins that wet low-surface-energy films and cold-seal grades that protect heat-sensitive confectionery.

Reactive adhesives remain indispensable for structural joints and electronics potting. Solvent-borne lines retreat to footwear and leather, although water-borne dual-component products from Frabo Adesivi now challenge them in upholstery. UV-cure platforms support high-speed automotive assembly, while hybrid STP formulations free of isocyanate and solvent open new specification doors in public construction, further broadening the Italy Adhesives market.

By End-user Industry: Packaging Leads, Automotive Pivots to EVs

Packaging represented 38.22% of 2025 volume and is projected to grow fastest at 6.82% CAGR during the forecast period (2026-2031), propelled by corrugated-case proliferation around Cessalto and expanding fulfillment networks. Building and construction requirements realign toward NRRP civil projects, cushioning the post-Superbonus dip in residential renovation.

Automotive uptake fell with Stellantis output, yet EV growth sustained demand for thermal-management epoxies and low-isocyanate polyurethanes. Furniture districts continue to specify EVA and polyurethane hot-melts for edge-banding, maintaining a vital domestic consumption pillar. Footwear clusters in Marche still rely on solvent-borne chloroprene, though migration to water-borne dispersions is visible as luxury brands raise sustainability thresholds.

Geography Analysis

Northern Italy accounts for the bulk of adhesive shipments, with Lombardy and Veneto alone responsible for nearly half of the packaging-related pull. Corrugated capacity expansions, including Progroup’s new plant, intensify local sourcing of water-borne starch blends, anchoring regional robustness in the Italy Adhesives market. Piedmont and Emilia-Romagna house automotive and Tier-1 suppliers where reactive polyurethane and epoxy grades dominate windshield, battery and structural bonding lines.

Central districts, notably Marche and Tuscany, sustain solvent-borne and water-borne polyurethane demand through footwear, leather goods, and high-end upholstery workshops. Brianza’s furniture cluster in Lombardy records the highest per-capita consumption of EVA hot-melts for edge-banding, whereas Veneto’s bathroom-furniture exporters increasingly prefer laser-activated grades to access US premium-kitchen channels.

Southern regions remain smaller but gain traction through NRRP-funded infrastructure. Rail electrification in Puglia and seismic retrofits in Sicily import significant volumes of epoxy anchoring systems and acrylic vapor-barrier tapes. While absolute tonnage is lower than the North, higher growth rates could widen geographic balance within the italy adhesives market during the forecast horizon.

Competitive Landscape

The Italy Adhesives market is moderately fragmented. Technology stratification persists. Automotive Tier-1s deploy robotic dispensing and UV-cured lines that favor large suppliers offering training and service contracts. Artisanal furniture shops stay with solvent-borne legacy grades due to capital constraints. The resultant two-speed market allows scale players to consolidate share while niche specialists defend territories through customization and quick turnaround, reinforcing a moderately concentrated Italy Adhesives market.

Italy Adhesives Industry Leaders

H.B. Fuller Company

Henkel AG & Co. KGaA

MAPEI S.p.A.

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GE Aerospace announced plans to invest EUR 77 million in Italy to enhance advanced manufacturing and testing capabilities across multiple commercial and defence engine programmes. This can help in boosting the overall demand for adhesives in the country.

- January 2026: Stellantis announced plans to increase production shifts at several plants across Italy and introduce new models to meet a goal to hike local output from 2026. This can help in boosting the overall demand for adhesives in the country.

Italy Adhesives Market Report Scope

Adhesives, including glue and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The Italy Adhesives Market is segmented by resin, technology, and end-user industry. By Resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By Technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By End-user Industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD).

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Hot-melt |

| Reactive |

| Solvent-borne |

| UV-cured |

| Water-borne |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Hot-melt |

| Reactive | |

| Solvent-borne | |

| UV-cured | |

| Water-borne | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms