Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

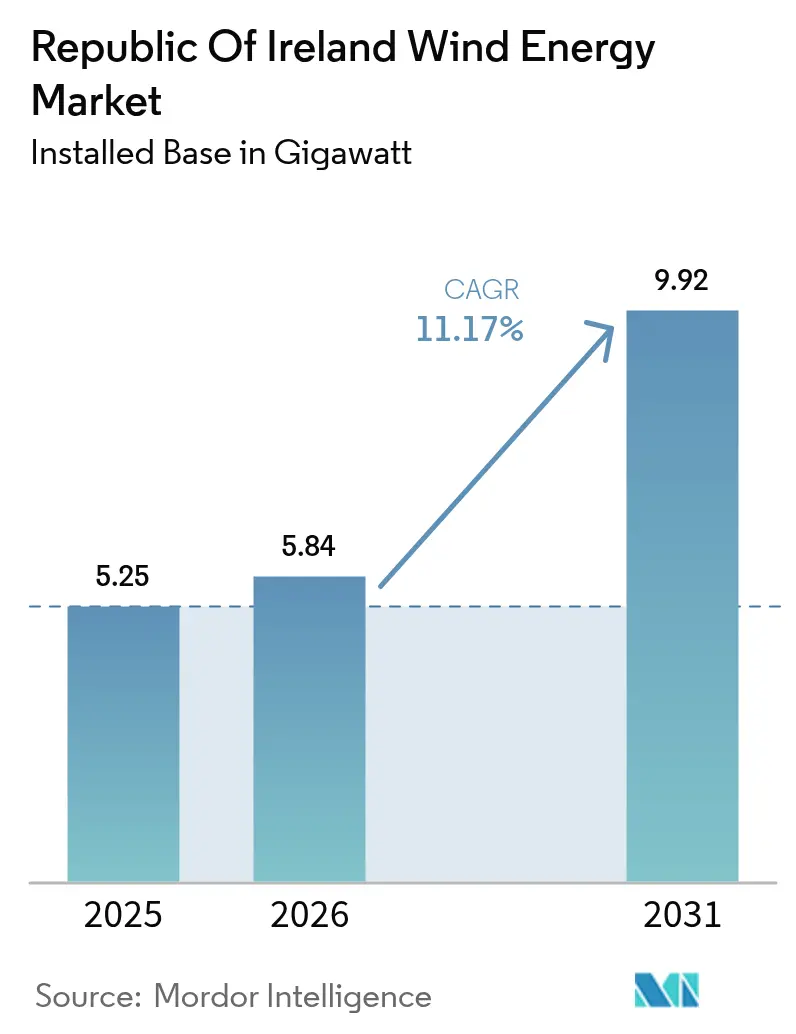

| Base Year Market Size (2025) | 5.25 gigawatt |

| Market Volume (2026) | 5.84 gigawatt |

| Market Volume (2031) | 9.92 gigawatt |

| Growth Rate (2026 - 2031) | 11.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Republic Of Ireland Wind Energy Market Analysis by Mordor Intelligence

Republic Of Ireland Wind Energy Market size in 2026 is estimated at 5.84 gigawatt, growing from 2025 value of 5.25 gigawatt with 2031 projections showing 9.92 gigawatt, growing at 11.17% CAGR over 2026-2031.

This growth is based on a statutory target that requires 80% renewable electricity by 2030, a €100 billion post-2030 offshore investment framework, and EirGrid’s €1 billion offshore grid procurement plan. Onshore projects still dominate deployments in 2025, yet the pipeline of fixed-bottom and floating offshore projects signals a decisive structural shift toward multi-gigawatt marine capacity. Larger turbines above 6 MW, synthetic inertia services, and AI-based siting analytics are improving capacity factors and lowering delivered costs, making wind the preferred substitute for imported gas. Corporate power-purchase agreements, green-hydrogen ventures, and community-ownership schemes widen demand and access to capital, positioning the Irish wind energy market for export capability within a rapidly expanding European grid.

Key Report Takeaways

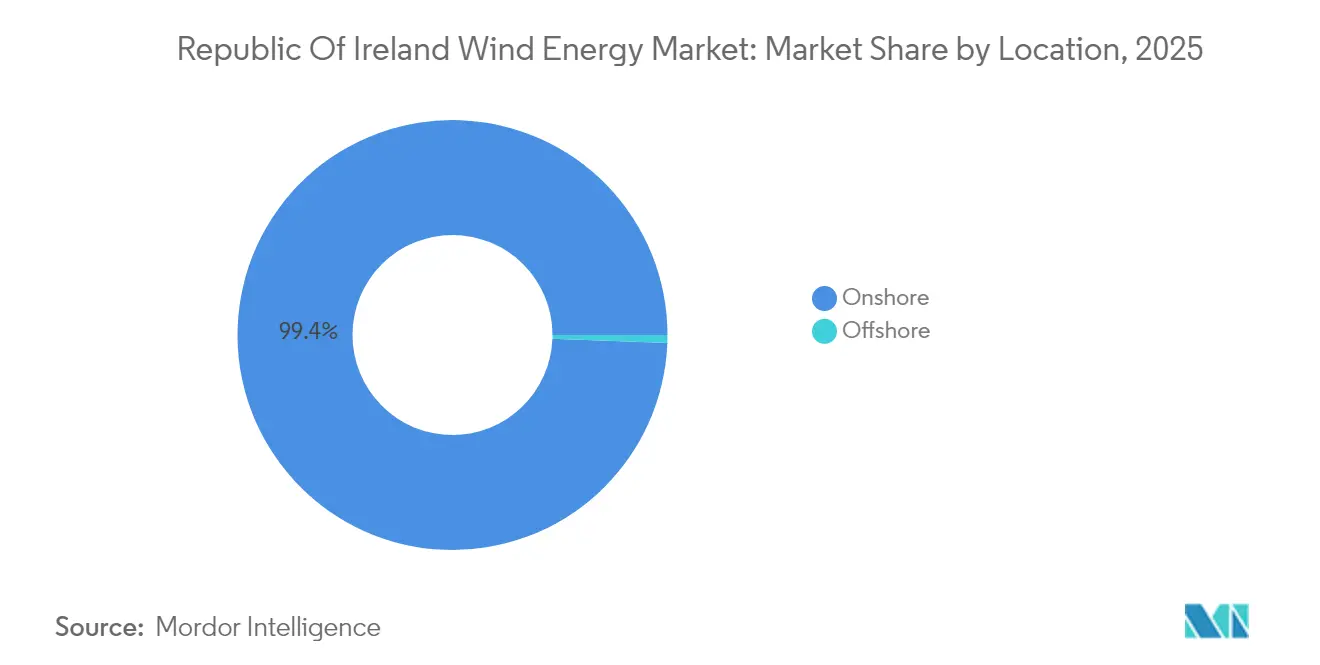

- By location, onshore installations accounted for 99.40% of the Irish wind energy market share in 2025, while offshore capacity is projected to expand at a 103.8% CAGR through 2031.

- By turbine capacity, systems exceeding 6 MW accounted for 62.05% of the Irish wind energy market size in 2025 and are projected to advance at a 12.27% CAGR over the outlook period.

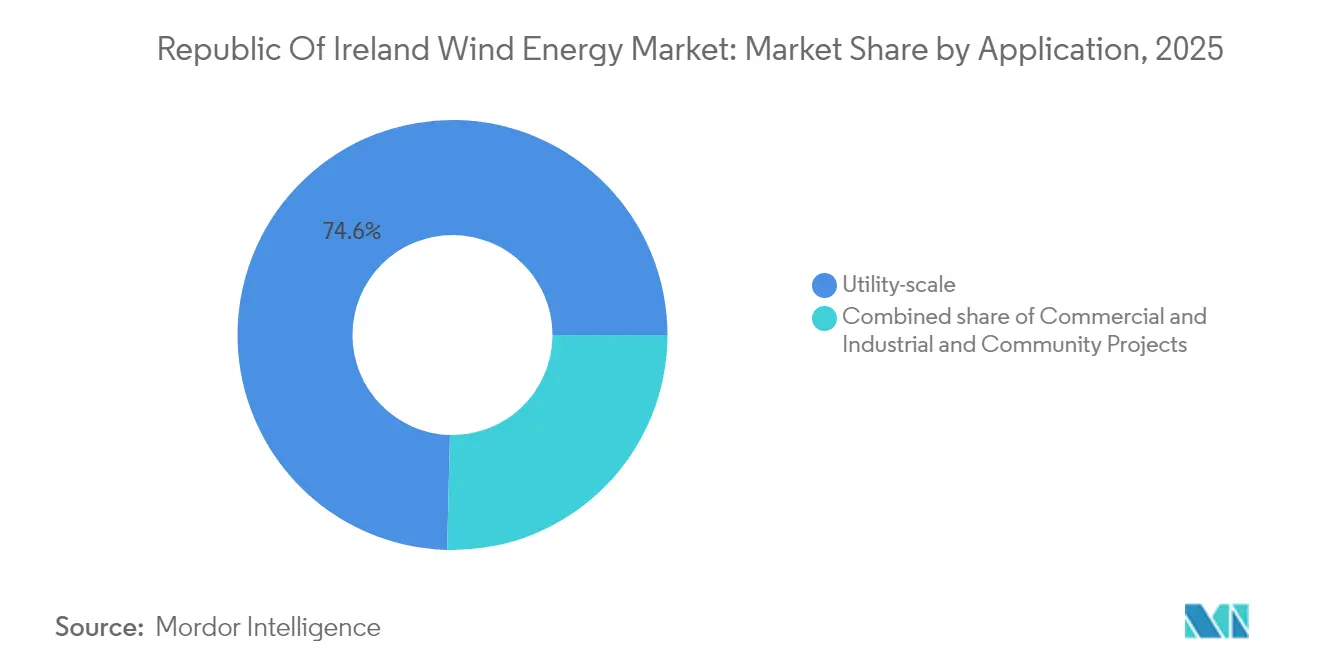

- By application, utility-scale assets held 74.60% of the installed megawatts in 2025, whereas community projects are the fastest-growing, with a 12.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Republic Of Ireland Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost reductions in onshore turbine technology | +2.1% | National, with higher impact in western coastal regions | Medium term (2-4 years) |

| Ireland's 80%-by-2030 renewable-electricity mandate | +3.4% | National | Short term (≤ 2 years) |

| Growing corporate PPAs & green-hydrogen demand | +1.8% | National, concentrated in industrial corridors | Long term (≥ 4 years) |

| Rare-earth magnet supply localisation (Irish-EU JV plans) | +0.9% | National, with EU supply chain benefits | Long term (≥ 4 years) |

| Grid-service revenues from synthetic inertia provision | +1.2% | National grid integration points | Medium term (2-4 years) |

| AI-optimised site-selection increasing capacity factors | +1.6% | National, particularly in complex terrain areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Reductions in Onshore Turbine Technology

Competitive pricing now places onshore wind at EUR 50-60 per MWh, below fossil fuel benchmarks, thanks to average turbine ratings of 5,500 kW and rotor diameters exceeding 180 m.[1]Global Wind Energy Council, “Wind Turbine Suppliers Deliver New Record Volume,” gwec.net Taller hub heights and extended planning terms of up to 30 years could halve delivered costs, particularly in western counties where wind speeds exceed 7 m/s. These economics strengthen the Ireland wind energy market as the country’s baseload substitute for gas-fired generation.

Ireland’s 80%-by-2030 Renewable-Electricity Mandate

The Climate Action Plan aims to achieve 5 GW of offshore and 9 GW of onshore wind by 2030, driving auction volume under the Renewable Electricity Support Scheme and reducing the minimum fossil fuel dispatch from five to four units on the grid.[2]EirGrid, “Number of Large Fossil Generators Reduced,” eirgrid.ie Binding policy certainty accelerates investment decisions and reduces the weighted average cost of capital across the Ireland wind energy market.

Growing Corporate PPAs & Green-Hydrogen Demand

Data centers that use more than 21% of Irish electricity now execute long-term PPAs to secure a renewable supply. ESB and dCarbonX aim to secure 11 TWh of offshore hydrogen storage, offering new monetization paths for surplus output and stabilizing revenue for wind developers. This multi-offtake model broadens the Ireland wind energy market customer base.

AI-Optimised Site Selection Increasing Capacity Factors

Machine-learning tools combine mesoscale weather data with high-resolution terrain inputs to refine turbine placement, raising annual energy production and lowering O&M costs by 13.41% in pilot projects.[3]arXiv, “Reinforcement Learning Approach to Battery Management,” arxiv.org Enhanced forecasting accuracy also lifts non-synchronous penetration limits, enabling greater instantaneous wind shares on the national grid.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Planning-permission bottlenecks & judicial reviews | -1.9% | National, with higher impact in densely populated counties | Short term (≤ 2 years) |

| Rising grid-connection charges under PR5 tariff regime | -1.3% | National transmission network connection points | Medium term (2-4 years) |

| Offshore supply-chain port infrastructure gaps | -1.1% | Coastal regions, particularly Cork and Dublin ports | Medium term (2-4 years) |

| Limited domestic blade-recycling capacity | -0.7% | National, with concentration in western wind farm regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Planning-Permission Bottlenecks and Judicial Reviews

Only one wind farm gained approval in Q3 2024, while 31 cases were awaiting adjudication, resulting in a backlog equivalent to 18% of the required capacity for 2030. Legal appeals, anti-wind zoning, and resource constraints at An Bord Pleanála extend timelines despite a 2024 Act that introduces statutory deadlines.

Rising Grid-Connection Charges Under the PR5 Tariff Regime

EirGrid recovers a record grid investment through higher Transmission Use-of-System fees, which lift upfront costs for new generators and squeeze project returns, especially for smaller developers. Elevated charges risk consolidating the Ireland wind energy market around large utilities capable of absorbing tariff shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore momentum builds while onshore remains dominant

Onshore projects supplied 99.40% of the installed capacity in 2025 and continue to underpin near-term additions, as they rely on mature supply chains and lower capital expenditures. Western and south-western counties record average wind speeds above 8 m/s, sustaining capacity factors that keep the Ireland wind energy market size robust at land-based sites. Yet land availability constraints and growing community resistance moderate future onshore growth. Offshore wind now defines the steepest trajectory, expanding at a 103.8% CAGR through 2031 as 66 projects totaling 70.28 GW advance in the planning queue. Fixed-bottom arrays, such as Codling Wind Park and Arklow Bank Phase 2, target capacity factors above 50%, and floating technology promises to unlock deeper Atlantic resources. Grid-ready ports and bespoke vessel access will determine the pace at which offshore wind energy can reshape the Irish wind energy market share during the forecast horizon.

By Turbine Capacity: Above 6 MW platforms take center stage

Systems above 6 MW accounted for 62.05% of installations in 2025 and grew at a 12.27% CAGR as developers favor higher hub heights and longer blades that deliver superior yield per foundation. Supply-chain economies accelerate cost-out, which tightens the levelised cost of energy and lifts the Ireland wind energy market size for this segment. Mid-range 3-6 MW machines retain their roles where grid constraints or landscape factors restrict the use of larger equipment, but their share declines steadily. Sub-3 MW units increasingly serve distributed and community projects that require smaller footprints or simplified logistics. Planning guidelines last updated in 2006 require revision to accommodate the height and swept-area profile of modern turbines.

By Application: Community growth challenges utility hegemony

Utility-scale fleets maintained 74.60% of operating megawatts in 2025, with integrated developers such as ESB, SSE Renewables, and Energia Group playing a key role. These players leverage balance-sheet heft and auction expertise to secure long-term contracts that underpin the Ireland wind energy market. Community projects, now growing at 12.9% CAGR, receive preferential RESS quotas and local investment incentives, turning citizens into co-owners while diffusing siting opposition. Commercial and industrial buyers occupy a middle tranche where on-site or near-site arrays satisfy sustainability mandates under corporate PPAs.

Geography Analysis

Most current installations cluster along the Atlantic rim in Galway, Mayo, and Kerry, where wind speeds exceeding 8 m/s support high capacity factors, and lower population density facilitates permitting. Cork emerges as the national offshore staging hub following a EUR 88.5 million port retrofit, which will service turbine assembly and heavy-lift operations. The Southern waters form the South Coast Designated Maritime Area, which is home to four zones slated to start production by 2030. East-coast development leverages proximity to large demand centers around Dublin but faces tighter zoning and visual-impact scrutiny. The Codling and Arklow projects benefit from existing grid nodes, yet they must navigate busy shipping lanes and sensitive ecological areas. Midlands and northern counties hold latent onshore potential that becomes viable as grid reinforcements extend capacity corridors. A long-term strategy looks toward the Celtic Sea, where floating turbines could double the developable resource areas and transform the Irish wind energy market into a net exporter by the early 2030s.

Regulatory Landscape

Ireland’s wind build-out is shaped by binding decarbonization policy and a planning and grid regime that continues to align with EU approaches. The Climate Action Plan 2025 sets out the pathway to 80% renewable electricity by 2030 and related wind targets, while the Offshore Renewable Energy Future Framework (May 2024) lays out a plan-led route for offshore development through designated maritime areas and auction-backed support. Planning and consenting have also been updated around RED III implementation, including Office of the Planning Regulator Circular CEPP 1/2026 (January 2026) and the European Union (Planning and Development) (Renewable Energy) Regulations 2025 (S.I. No. 274 of 2025), which aim to standardize and speed up renewable planning decisions.

Grid connection and offshore transmission oversight sit with the Commission for Regulation of Utilities (CRU) and EirGrid, with the next investment cycle framed by PR6. In May 2026, the CRU described PR6 as enabling up to EUR 18.9 billion of network investment for 2026-2030, keeping the focus on both onshore reinforcement and offshore grid readiness. Offshore transmission requirements are also being tightened for Phase 1 projects through CRU instruments, including updated cost reporting and post-construction review guidance (March 2026) and a June 2026 consultation on a Guarantee of Availability policy that addresses how outage-related risk is allocated for offshore wind.

Competitive Landscape

Market concentration sits at a moderate level. SSE Renewables leads the offshore sector with investments of up to EUR 6 billion and an 800 MW Arklow Bank Phase 2 project in late-stage planning. ESB partners with Equinor for 1.5 GW of floating capacity, leveraging its grid ownership and retail arm to integrate generation, transmission, and supply.[5]Renews, “ESB and Equinor Eye 1.5 GW Floater,” renews.biz Ørsted commands the largest onshore portfolio exceeding 500 MW and has recently made a financial investment decision on the 43.2 MW Farranrory site. International entrants, such as Statkraft, Brookfield Renewable, and Parkwind, intensify bidding and stimulate supply-chain localization. Turbine OEM competition centers on reliability, lifecycle service packages, and grid-forming capabilities that unlock revenue from synthetic inertia. Rising PR5 connection costs and lengthy permitting cycles could spur consolidation, advantaging capital-rich developers who are able to navigate the complex regulatory terrain across the Irish wind energy market.

Republic Of Ireland Wind Energy Industry Leaders

Nordex SE

Parkwind NV

General Electric Company

ELECTRICITE DE/ADR (EDF Group)

Statkraft AS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Offshore scale-up remains the main near- to mid-term whitespace, with opportunities tied to the state’s plan-led development model and the associated grid programs. The Offshore Renewable Energy Future Framework outlines actions for designated maritime areas, and ORESS auctions turn that structure into bankable revenue support for projects that obtain Maritime Area Consents and clear EirGrid grid assessments. EirGrid’s offshore transmission build program, including the Powering Up Offshore workstream and offshore grid procurements referenced in the report context, expands the addressable work across export cables, landfall works, substations, and grid-forming services. It also supports demand for specialized marine surveys and construction logistics connected to the South Coast Designated Maritime Area process.

Onshore capacity additions create additional use cases in hybridization and offtake structures that improve system value at higher wind penetration levels. Corporate PPAs continue to appear in new projects and can support financing beyond auction routes, while co-located storage is moving from concept to commissioned assets, which helps manage curtailment and grid support needs at wind-heavy nodes. Community participation remains another delivery channel through RESS quotas and local investment mechanisms, broadening the developer base beyond large utilities and helping address siting acceptance constraints in more contested counties.

Recent Industry Developments

- April 2026: Bord na Móna officially opened the 126 MW Derrinlough Wind Farm in County Offaly, built with 21 V150-6.0 MW turbines and backed by an investment reported at over EUR 150 million. The project includes a corporate power purchase agreement with Amazon, reinforcing the role of CPPAs in underwriting new Irish onshore wind capacity and strengthening bankability outside pure auction exposure.

- February 2026: Statkraft officially opened the Cushaling Battery Energy Storage System in County Offaly, positioned as Ireland’s first 4-hour duration grid-scale battery and co-located with the 55.8 MW Cushaling Wind Farm. The commissioning highlights the operational shift toward pairing wind with longer-duration storage to manage curtailment risk and provide grid-support services as non-synchronous generation increases.

- June 2025: DP Energy and ESB launched the Lyra onshore project, indicating continued utility-developer co-development activity in Ireland’s dominant onshore segment. This structure supports faster progress from development to delivery by combining project origination capability with balance-sheet strength and route-to-market experience.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Ireland wind energy market is defined as grid connected wind power capacity operating in the Republic of Ireland, counted as installed capacity and tracked across onshore and offshore deployment.

Scope exclusions: This sizing does not include Northern Ireland, behind-the-meter micro wind, or broader renewable technologies such as solar, hydro, and bioenergy.

Segmentation Overview

- By Location

- Onshore

- Offshore

- By Turbine Capacity

- Up to 3 MW

- 3 to 6 MW

- Above 6 MW

- By Application

- Utility-scale

- Commercial and Industrial

- Community Projects

- By Component (Qualitative Analysis)

- Nacelle/Turbine

- Blade

- Tower

- Generator and Gearbox

- Balance-of-System

Data Sources, Market Sizing, and Validation

Desk Research

To build the first layer of the dataset, we focused on public energy and statistics sources that report Ireland-level capacity, generation, and policy signals. Examples include national grid and system operator publications, government and regulator energy statistics, the IEA and IRENA data portals, and EU datasets such as Eurostat, which help cross-check year-to-year changes.

We also reviewed planning and auction-related disclosures, developer and utility annual reports, and reputable press coverage to track project timelines, commissioning slippage, and repowering activity. Where needed, company financials and a patent database were used to check ownership changes and technology direction, but not to replace public capacity baselines. This list is illustrative only, and other sources were also used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary discussions were used to confirm what is operational versus under construction, and to test assumptions on offshore timing, repowering schedules, and expected utilization under Irish wind conditions. We spoke with developers, EPC and O&M participants, utilities, and large power buyers. Feedback was taken from onshore- and offshore-focused respondents so the final model reflects commissioning behavior rather than stated targets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | APAC: 50% |

| Mid tier: 53% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 15% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

Market size is modeled mainly through a top-down build that reconstructs installed capacity by year from official capacity baselines and verified additions and retirements, and then it is split between onshore and offshore using project-level commissioning status. To keep totals realistic, selective bottom-up approximations are run in parallel, including summing known operational wind farms and applying sampled turbine nameplate capacity, followed by checks against reported national wind output.

Key inputs that shape the yearly totals include announced and consented pipeline by status, commissioning dates and grid connection milestones, repowering and life extension timing, typical capacity factors by site type, and curtailment or grid constraint signals where they materially affect observed generation. For forecasting, scenario analysis is used so policy support, auction schedules, and delivery risks translate into clear build rates, which are reviewed and adjusted using expert consensus from field discussions. When a project detail is missing, gaps are handled through conservative assumptions based on similar Irish projects, and the impact is tested so a single missing data point does not distort the full curve.

Data Validation & Update Cycle

Outputs are checked against independent indicators, including total installed wind capacity reported by official sources, annual wind generation, and known commissioning events, and then variances are investigated before sign off. If a spike or dip cannot be explained by a pipeline change, an additional review is triggered and respondents may be re-contacted to confirm the reason.

Reports refresh annually, and interim updates are made when a material event occurs, such as a major auction result, a large project delay, or a policy change that impacts commissioning timelines. Before delivery, an analyst runs a fresh pass across the dataset so clients receive the most current view available at that time.

Mordor Intelligence's Ireland Wind Energy Market Size Compared With Other Published Estimates

It is normal to see different market sizes for Ireland wind energy because some sources measure value while others report installed capacity, and the boundaries around geography and technology are not always consistent. Currency timing, price-per-MW logic, and the point at which late project changes are reflected can also shift the final number.

A refresh led gap shows up when capacity additions are updated quickly, but price assumptions are left on an older exchange rate or an older turbine cost curve, which then moves USD values up or down even if the same wind farms are being counted. In our capacity-first view, the 2025 to 2031 path is tied to commissioning verification and an annual refresh cycle, and then the latest currency timing and ASP checks are applied before publishing under Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.25 B (2025) | |

| Trade Journal A | USD 2.67 B (2025) | This figure is value based and can understate scale if it counts only annual spending or a narrow revenue pool, and it may not fully align with installed capacity additions in the same year. |

| Global Consultancy B | USD 3.90 B (2023) | The scope is broader renewable energy rather than wind only, and the year and currency timing differ, which makes direct comparison to a wind capacity driven model uneven. |

The comparison shows that the biggest drivers are the unit of measure (capacity versus value), scope boundaries (wind only versus wider renewables), and timing effects when USD conversion and price per MW assumptions are refreshed. By keeping the capacity base anchored to verified commissioning and then layering assumptions transparently, the final estimate remains traceable to clear steps that can be repeated year after year.

Key Questions Answered in the Report

How large is the Ireland wind energy market in 2026?

The Ireland wind energy market totals 5.84 GW of installed capacity in 2026.

What growth rate is expected for Irish wind capacity through 2031?

Capacity is projected to expand at an 11.17% CAGR, reaching 9.92 GW by 2031.

Which segment will add the most new capacity in Ireland?

Offshore wind shows the steepest climb, growing at a 103.8% CAGR from 2025 to 2031.

What policy supports Ireland’s wind build-out?

A legally binding 80% renewable-electricity mandate for 2030 underpins auction volume and grid upgrades.

Why are grid-connection charges a concern for developers?

PR5 tariffs raise upfront costs, squeezing project returns, especially for smaller entrants.

Can Ireland become an exporter of renewable power?

Planned multi-gigawatt offshore projects and hydrogen storage strategies position Ireland to export surplus clean energy later this decade.

Page last updated on: