Integrated Marine Automation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

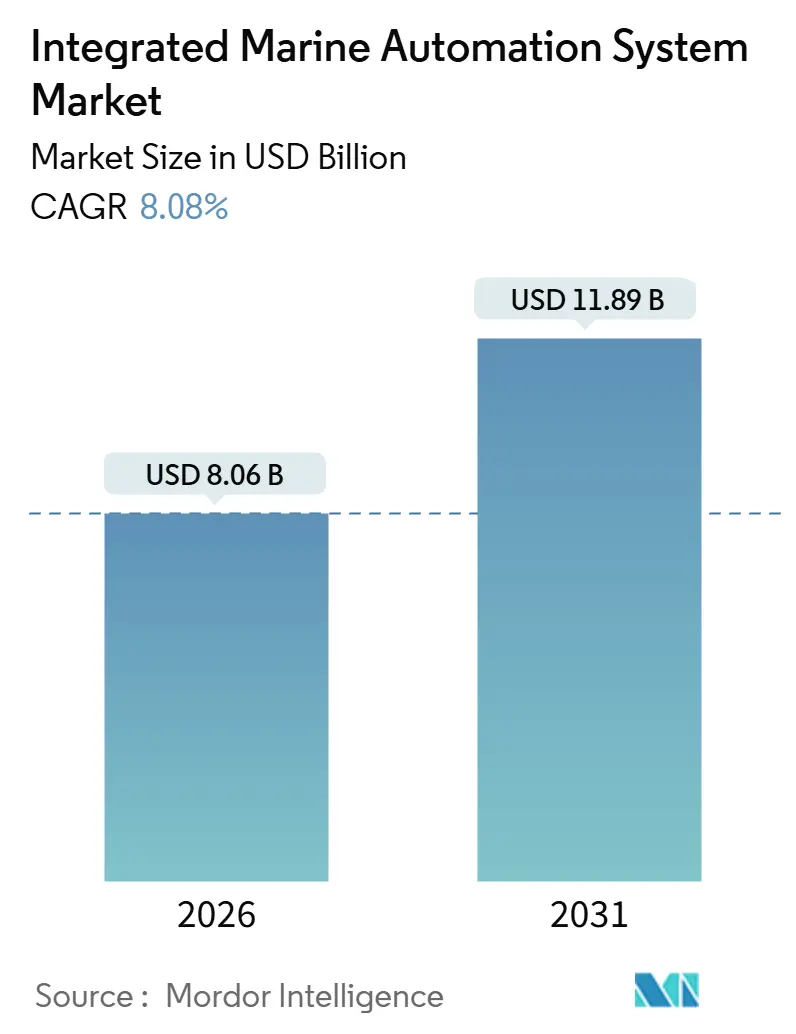

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 11.89 Billion |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Integrated Marine Automation System Market Analysis by Mordor Intelligence

The integrated marine automation system market size stands at USD 8.06 billion in 2026 and is projected to reach USD 11.89 billion by 2031, advancing at an 8.08% CAGR through the period. Intensifying emissions regulations, rising crew costs, and accelerating digitalization keep owners focused on real-time monitoring, predictive analytics, and automated power management. The European Union Emissions Trading System begins covering maritime transport in 2024, while FuelEU Maritime introduces well-to-wake greenhouse-gas limits in 2025, together spurring demand for sensor-to-cloud stacks and verification software. Crew shortages raise day-rate pressure, so operators value automation that reduces manning without compromising safety. Asia Pacific dominates newbuild installations, while retrofit activity accelerates in Europe and North America as owners adapt existing fleets to Energy Efficiency Existing Ship Index and Carbon Intensity Indicator thresholds. Competition remains moderate, with legacy hardware suppliers defending share against software-centric entrants leveraging edge analytics and cloud platforms.

Key Report Takeaways

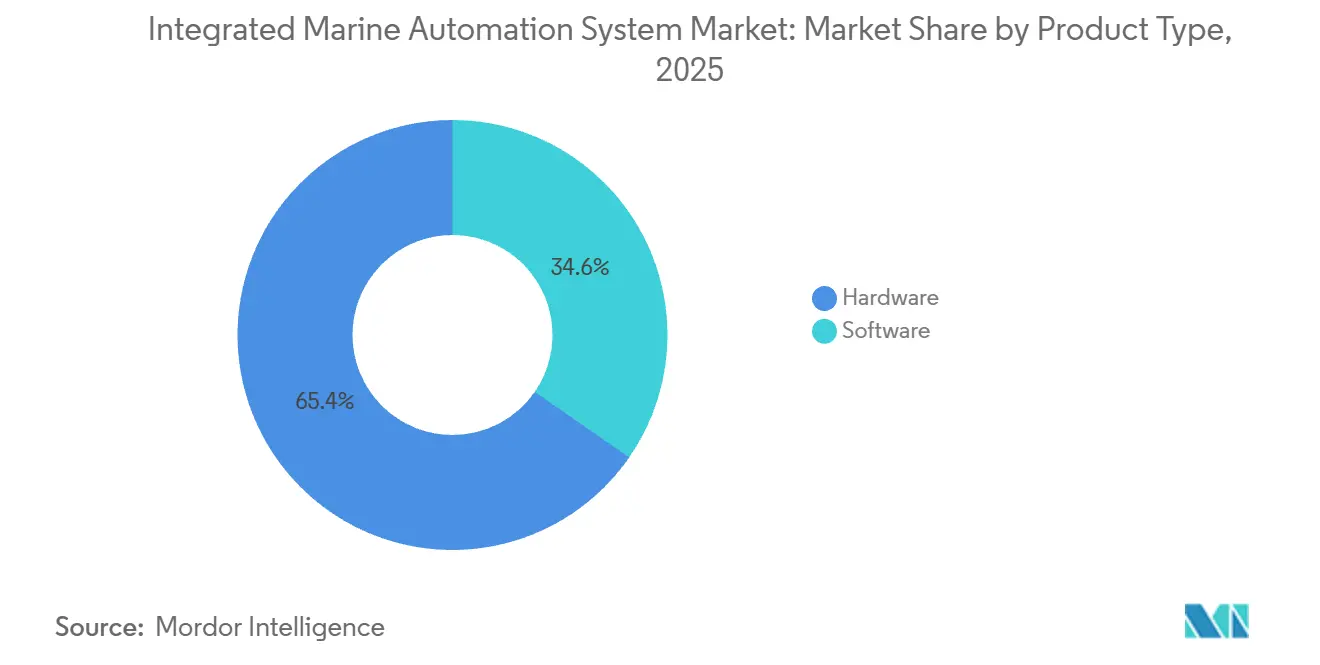

- By product type, hardware held 65.36% of the integrated marine automation system market share in 2025, while software is forecast to grow at a 9.87% CAGR to 2031.

- By solution, vessel-management systems commanded 45.12% of 2025 revenue, whereas analytics and predictive-maintenance software is projected to expand at an 11.27% CAGR through 2031.

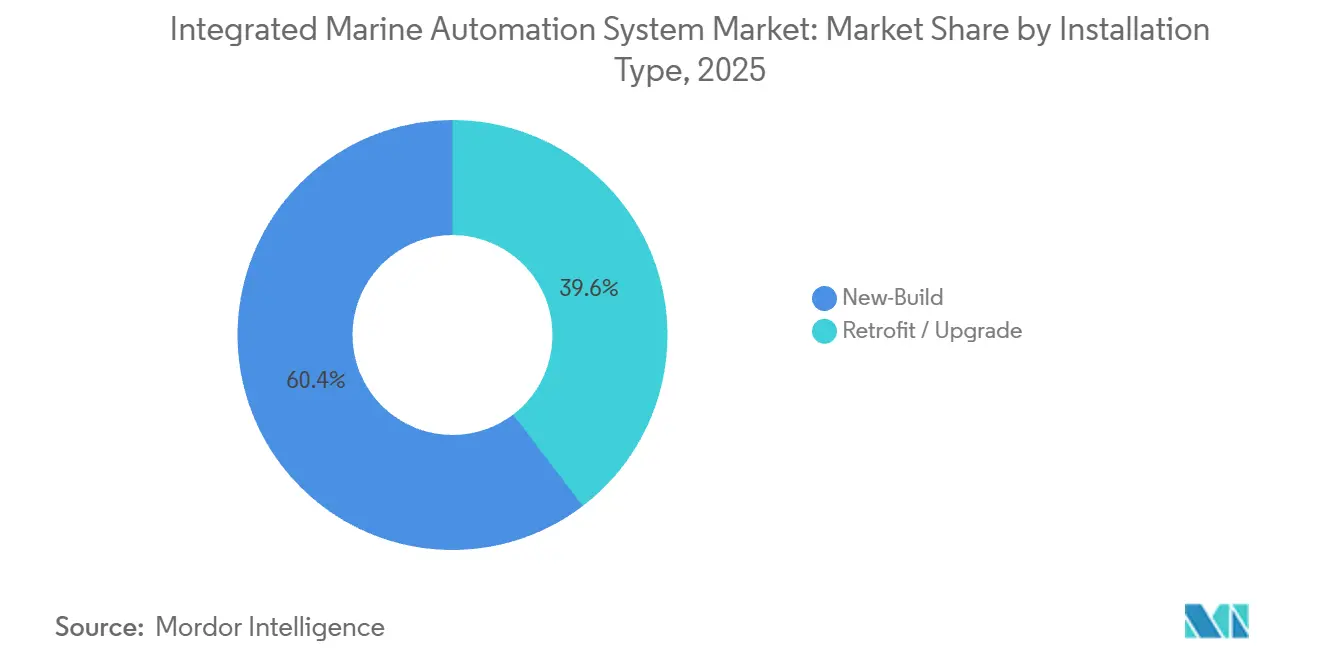

- By installation type, new-build projects led with 60.37% share in 2025, and retrofit and upgrade work is expected to post a 12.19% CAGR over the outlook period.

- By end user, commercial operators accounted for 75.42% of 2025 demand, yet defense applications are set to rise at a 10.19% CAGR to 2031.

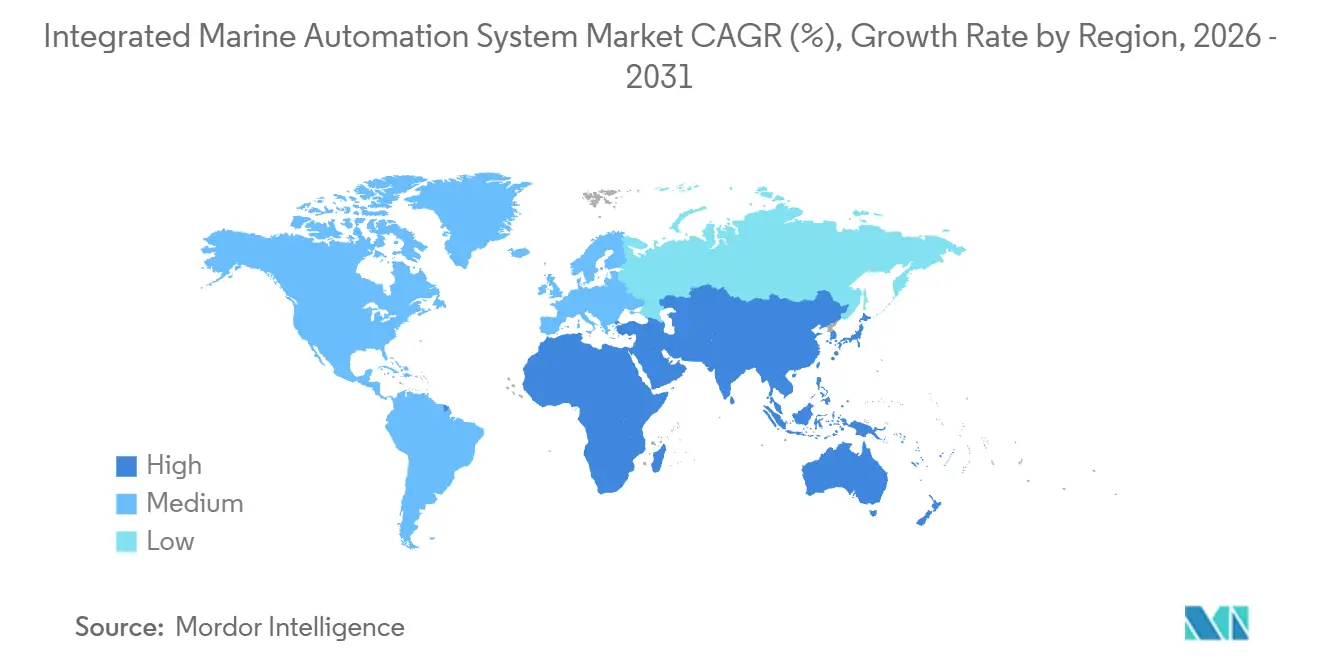

- By geography, Asia Pacific captured 35.13% revenue in 2025, while the Middle East is on track for the fastest 12.89% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Integrated Marine Automation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Growth in Maritime Tourism Industry | +0.9% | Global, with concentration in Mediterranean, Caribbean, Asia Pacific cruise routes | Medium term (2-4 years) |

| Volumetric Growth in Seaborne Trade | +1.2% | Global, particularly Asia Pacific export corridors and transatlantic routes | Medium term (2-4 years) |

| IMO Energy-Efficiency Regulations Driving Digital Automation | +1.8% | Global, with early adoption in EU and North America due to regional carbon pricing | Short term (≤ 2 years) |

| Crew Cost Optimisation Amid Seafarer Shortage | +1.3% | Global, acute in Europe and North America where crew wages are highest | Short term (≤ 2 years) |

| Remote-Operated and Autonomous Vessels for Offshore-Wind Maintenance | +1.0% | Europe, Asia Pacific (China, Taiwan, Japan offshore wind zones), emerging in Middle East | Medium term (2-4 years) |

| Growing Demand for Edge-Based Cyber-Resilient Automation Modules | +0.7% | Global, prioritized in defense and critical infrastructure segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IMO Energy-Efficiency Regulations Driving Digital Automation

Mandatory carbon-intensity targets force owners to install automated emissions monitoring, fuel-flow sensors, and class-approved reporting software, creating an immediate procurement wave for integrated hardware and analytics. Fleet-level pooling under FuelEU Maritime multiplies demand for optimization tools that calculate voyage-by-voyage balances and distribute credits across owners. Early adopters in Europe connect shore-power interfaces to ship-to-shore power-management software, lifting auxiliary-engine savings and reducing port emissions.

Crew Cost Optimization Amid Seafarer Shortage

A widening officer shortfall drives automation that cuts routine watchkeeping and diagnostic tasks.[1]International Chamber of Shipping, “Seafarer Workforce,” ics-shipping.org Platforms such as Kongsberg Vessel Insight stream standardised data to shore, letting technical managers monitor fleets remotely and redeploy specialists only when sensors flag anomalies. Predictive algorithms prevent unplanned downtime, enabling leaner manning scales without sacrificing reliability.

Remote-Operated and Autonomous Vessels for Offshore-Wind Maintenance

Rapid offshore-wind build-out fuels demand for service craft equipped with autonomous navigation, automated dynamic positioning, and collision-avoidance sensors. Uncrewed surface vessels handle inspection and light maintenance up to 150 nautical miles from base, trimming charter costs for crewed ships. Demonstrations such as Kawasaki Kisen’s Seawing kite, targeting double-digit fuel savings, illustrate commercial appetite for automation-enabled efficiency.

Growing Demand for Edge-Based Cyber-Resilient Automation Modules

High-profile cyber incidents expose the need for onboard processing that sustains control even when connectivity drops. Edge devices filter and analyze data locally, sending compressed insights to shore, lowering bandwidth bills and meeting updated BIMCO guidelines for segmented maritime networks. Defense buyers specify ruggedized, cyber-hardened architectures able to operate in contested electromagnetic environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vulnerability to Cyber-Attacks Through Digitalisation | -1.1% | Global, with heightened concern in defense and critical infrastructure segments | Short term (≤ 2 years) |

| High Upfront Cost and Integration Complexity | -1.4% | Global, particularly acute in retrofit projects and for small to mid-sized operators | Medium term (2-4 years) |

| Interoperability Gaps Among Proprietary Systems | -0.8% | Global, fragmented vendor ecosystems in Asia Pacific and Europe | Medium term (2-4 years) |

| Limited Satellite Bandwidth on Remote Routes | -0.6% | Remote ocean routes, polar regions, and areas with sparse satellite coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vulnerability to Cyber-Attacks Through Digitalisation

Maritime operational-technology networks combine legacy control systems with new IP-based devices, creating attack vectors that can disable propulsion and navigation. The IMO now mandates cyber-risk management in safety systems, yet smaller operators lag on patching and incident response.[2]International Maritime Organization, “Energy Efficiency Regulations,” IMO, imo.org Type-approved security retrofits often exceed USD 500,000 per vessel, deterring budget-constrained owners.

High Upfront Cost and Integration Complexity

Complete automation packages can cost USD 2-10 million for a mid-size ship, with retrofit projects lasting up to 20 months from feasibility study to completion. Limited drydock slots and the need to interface new sensors with legacy control logic inflate timelines and elevate financing hurdles, especially for smaller fleets that lack in-house engineering teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hardware Dominates as Software Accelerates

Hardware retained 65.36% of 2025 revenue thanks to the installed base of sensors, control modules, and bridge electronics. The integrated marine automation system market size for hardware benefits from mandated emissions and fuel-flow monitoring but posts modest growth as many newbuilds arrive sensor-ready. Conversely, software revenue is projected to climb at 9.87% CAGR, driven by analytics, digital twins, and predictive-maintenance apps that monetize the expanding data stream. The hardware-to-software transition lets vendors capture recurring fees, locking in clients for lifecycle support.

Software’s rapid rise hinges on physics-informed AI that predicts component wear. For example, Synthetica’s platform flagged abnormal lubricator behavior on four bulkers in 2025, averting USD 80,000 repairs per hull. As owners pivot to condition-based maintenance, the integrated marine automation system market capitalizes on cloud infrastructures that scale analytics across fleets.

By Solution: Vessel-Management Systems Lead, Predictive Analytics Surge

Integrated bridge and engine-room platforms captured 45.12% 2025 share, underscoring demand for single-pane-of-glass control. These systems embed navigation, propulsion, cargo handling, and auxiliary functions, reducing crew workload and enabling remote operations. Power-management modules balance generators, batteries, and shore-power interfaces, essential for hybrid vessels and port-side zero-emission mandates.

Analytics and predictive-maintenance software is the fastest-growing solution, forecast at an 11.27% CAGR. Danelec Performance, installed on 14,000 vessels, streams voyage-data-recorder feeds to cloud AI that pinpoints hull fouling, engine inefficiencies, and propeller wear, unlocking 3-8% fuel savings. The integrated marine automation system market share for analytics increases as class societies endorse data-driven maintenance contracts.

By Installation Type: Retrofit Wave Builds Momentum

Newbuilds still account for 60.37% of 2025 installations because shipyards can wire automation while modules are accessible. Yet a 12.19% CAGR for retrofits through 2031 signals intensifying compliance deadlines and aging fleets. Over half of merchant tonnage sailed past the 15-year mark by 2023, and many hulls need new sensors, data-acquisition racks, and software gateways to satisfy EEXI and CII audits. Modular packages using common protocols such as OPC UA and Modbus simplify plug-and-play integration.

Shipyards expand capacity to absorb retrofit demand. South Korean yards improved throughput 8% in 2025 by adding berths and digitizing workflows. Such efficiency gains support a larger retrofit orderbook, bolstering the integrated marine automation system market.

By End User: Commercial Fleets Dominate, Defense Spend Quickens

Commercial operators provided 75.42% of 2025 revenue, targeting lower fuel burn, reduced crewing, and regulatory compliance. Container lines and LNG carriers use integrated bridge systems and predictive maintenance suites to trim voyage operating costs.

Defense demand, while smaller, is forecast to grow 10.19% annually as navies field unmanned surface vessels and retrofit legacy combatants with automation, readying them for network-centric warfare. The Royal Saudi Naval Forces and United Arab Emirates Navy release tenders bundling predictive maintenance and autonomous capabilities, widening the addressable market for secure, military-grade systems.[3]Gulf International Forum, "Securing the Seas: Examining Changing Saudi & Emirati Naval Capabilities," gulfif.org

Geography Analysis

Asia Pacific captured 35.13% revenue in 2025 on the back of South Korean and Japanese shipyard strength and government-led autonomy roadmaps. Seoul waived a feasibility study in 2025 to accelerate Level 4 autonomous-ship R&D, while Tokyo funds AI robotics in shipbuilding to counter skilled-labor gaps. Chinese yards scale low-carbon vessel production, embedding integrated automation as standard. Regional policies target manufacturing productivity gains above 40% by 2030, further anchoring the integrated marine automation system market.

The Middle East is projected to record the fastest 12.89% CAGR through 2031, fueled by naval modernization and offshore-energy activity. A 2025 United Arab Emirates contract worth AED 1.3 billion (USD 350 million) covering new patrol vessels includes predictive-maintenance and inventory-management packages, demonstrating preference for turnkey automation. Saudi Arabia’s King Salman complex accelerates regional shipbuilding, while SAMI Sea pursues unmanned platforms requiring cyber-resilient control systems.

North America and Europe prioritize retrofits to meet emissions policy milestones. Cross-border partnerships, such as HD Hyundai’s 2025 deal with Siemens to apply digital twins in United States yards, address domestic capacity gaps and spread advanced automation know-how. EU ports enforce shore-power mandates, boosting ship-to-shore automation, and ETS compliance software gains traction across Atlantic trader fleets.

Regulatory Landscape

Global regulatory drivers for integrated marine automation systems focus on decarbonization compliance, cyber-risk management, and interoperability expectations. The EU Emissions Trading System began covering maritime transport in 2024, and FuelEU Maritime introduced well-to-wake greenhouse-gas limits in 2025. Together, they are pushing demand for class-accepted emissions monitoring, automated reporting, and voyage and power optimization software integrated with onboard control systems.

On safety and digital resilience, the IMO updated Guidelines on Maritime Cyber Risk Management (MSC-FAL.1/Circ.3/Rev.3) through MSC 108 (May 2024) and FAL 49 (March 2025). The IMO Facilitation Committee also placed work on mandatory cybersecurity measures for maritime single windows onto its 2026-2027 agenda. For technical harmonization, the IEC 61162 digital interface standard family for navigation and radiocommunication equipment was updated in 2024 (including Parts 1, 2, and 450), supporting data exchange across integrated bridge, engine, and monitoring subsystems. In parallel, IACS Unified Requirement E26 applies to newbuilds contracted on or after 1 July 2024, reinforcing cyber-resilience expectations for shipboard systems that increasingly rely on networked automation.

Value Chain Analysis

The value chain includes sensor and field-device suppliers, control and safety system OEMs, bridge and navigation electronics providers, and maritime software developers supplying platform management, emissions and performance analytics, and cyber-security layers. System integration and commissioning are handled by OEMs and specialist integrators, working with shipyards for newbuilds and with yards and drydock networks for retrofit and upgrade projects. In retrofit programs, interfacing new gateways and data acquisition to legacy control logic is a frequent cost and schedule driver.

Recent contracting patterns underline the importance of shipyard-aligned delivery and single-supplier integration packages. Valmet secured an order to deliver Valmet DNA Integrated Automation Systems for Finnlines new RoPax vessels (April 2026), while Kongsberg Maritime won multiple newbuild package selections spanning dynamic positioning, integrated control, and energy management for vessels being built at yards such as Tersan Shipyard in Turkiye (February 2026) and for a polar expedition vessel program (March 2026). Overall, this points to unified architectures that reduce multi-vendor commissioning risk and to lifecycle digital services, such as monitoring and optimization, layered onto the installed automation base.

Competitive Landscape

The integrated marine automation system market features moderate fragmentation: top suppliers Kongsberg, ABB, Wärtsilä, and Siemens leverage global service networks and class approvals, yet face nimble software firms exploiting platform openness. Kongsberg Vessel Insight couples edge devices with cloud dashboards under DNV and ABS certification, securing subscription revenue beyond hardware sales. Samsung Heavy Industries pushes vertical integration with its S-EDP design-automation suite, aiming to double ship-design automation by 2030 and license the platform to partner yards.

Shipbuilders themselves become technology vendors. HD Hyundai’s alliance with Siemens integrates digital twins into American construction sites, signaling a shift where yards market smart-production IP alongside hull tonnage. Smaller companies such as Praxis Automation and Logimatic carve niches in retrofit integration and regional after-sales support, while defense integrators with security clearances maintain moats in classified programs.

White-space remains in edge-based cyber-resilient modules, onboard carbon-capture process control, and pooling software for FuelEU Maritime. Vendors that align modular products with open standards win flexibility-minded owners wary of vendor lock-in, shaping the competitive trajectory of the integrated marine automation system industry.

Integrated Marine Automation System Industry Leaders

-

Kongsberg Gruppen

-

ABB Group

-

Wartsila

-

Siemens AG

-

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automation demand is expanding beyond traditional machinery and bridge integration, moving toward compliance-grade digital reporting, cyber-resilient operations, and higher-autonomy workflows that reduce crew workload. A key whitespace is compliance automation that connects continuous emissions monitoring, voyage optimization, and auditable reporting into vessel-management systems, aligning with EU ETS coverage from 2024 and FuelEU Maritime well-to-wake limits from 2025. Kongsberg Maritime also added a Continuous Emissions Monitoring System integrated with its K-Chief vessel automation system (June 2025), illustrating how emissions compliance is being productized within core automation platforms.

Autonomy and shore-based operations further raise the bar for integrated stacks that connect onboard control, communications, and land-based fleet operations. In Japan, Mitsui O.S.K. Lines reported that four demonstration vessels under MEGURI2040 Stage 2 received MLIT certification as autonomous ships with Level 4-equivalent autonomous navigation in commercial service (March 2026), which increases expectations for integrated sensing, control, and remote monitoring. At the international level, the IMO published a non-mandatory MASS Code (July 2026) and started a two-year experience-building phase, while it also advanced a global maritime digitalization strategy emphasizing interoperability and data governance (March 2026, for submission to the IMO Assembly for adoption in 2027). These steps support near-term procurement focus on interoperable data architectures (aligned with IEC 61162 updates) and cyber-resilient automation modules that keep critical control functional during connectivity disruptions.

Recent Industry Developments

- April 2026: Valmet received an order to supply Valmet DNA Integrated Automation Systems for three new Finnlines RoPax vessels. The award highlights continued owner and shipyard preference for tightly integrated automation suites in newbuild programs, where unified control and monitoring are used to reduce commissioning complexity and improve operational performance.

- July 2025: ABB signed an agreement with Samsung Heavy Industries to equip nine shuttle tankers with the Onboard DC Grid power system, including DNV Closed Bus-Tie notation for dynamic positioning configurations. The deal extends integrated power management as a core marine automation capability, particularly for vessel types where redundancy, efficiency, and automated electrical control affect uptime and fuel use.

- June 2024: Kongsberg Maritime received Approval in Principle from DNV for a concept that moves the Chief Engineer role to a shore-based control center. The milestone supports broader remote-operations architectures that link onboard automation with fleet operations centers, consistent with crew optimization goals and higher-autonomy readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the integrated marine automation systems market is defined as revenue from integrated, shipboard automation where hardware, sensors, controllers, and marine-grade software work together to monitor, control, and protect vessel functions across navigation, propulsion, power, and safety, for both newbuilds and retrofits.

Scope exclusions: port-side automation equipment, standalone marine sensors sold without integration, and purely shore-based fleet software are excluded from this market sizing.

Segmentation Overview

-

By Product Type

-

Hardware

- Sensors and Field Devices

- Control Modules

- Navigation and Communication Systems

- Other Hardware

-

Software

- Integrated Platform-Management Software

- Safety and Security Software

- Analytics and Predictive-Maintenance Software

- Other Software

-

Hardware

-

By Solution

- Vessel-Management Systems

- Power-Management Systems

- Safety and Security Systems

- Other Solutions

-

By Installation Type

- New-Build

- Retrofit / Upgrade

-

By End User

- Commercial

- Defense

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and to keep assumptions anchored to observable maritime activity. We reviewed public sources such as IMO publications, UNCTAD shipping statistics, World Bank and OECD macro series, and customs or port authority disclosures where available. We also used ship registry and classification society publications as practical references for fleet mix, vessel age profiles, and retrofit timing patterns that influence automation uptake.

On the supply side, we checked annual reports, investor presentations, and press releases to understand product scope language and typical delivery models, for example equipment combined with commissioning. Where needed, paid subscriptions for company financials and news were used to confirm timelines and cross-check revenue commentary. A patent database was also reviewed to identify where automation capabilities were being developed. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate what is counted as an integrated system on a vessel, and to close gaps around retrofit cycles, typical bundling of modules, and how pricing changes with vessel class. Respondent input also helped clarify whether a deal is typically delivered as a single integrated package versus a mix of standalone subsystems. We spoke with a mix of system integrators, component suppliers, shipyards, vessel operators, and maritime consultants across APAC, EMEA, and the Americas, so regional build activity and regulation-driven upgrades could be compared in a consistent way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 43% |

| Mid tier: 61% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 14% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing was built using top-down logic where fleet activity and shipbuilding signals are used to reconstruct the addressable demand pool, and then the share that typically receives integrated automation is applied by vessel category and region. To keep totals realistic, we corroborated the top-down results with selective bottom-up checks, including sampled system pricing ranges multiplied by estimated installation volumes, and channel checks on retrofit intensity in key ship types.

Key inputs in the model included newbuild deliveries and orderbook direction, the operational fleet age profile that drives retrofit needs, adoption of automation modules linked to bridge and engine room modernization, regulatory and class compliance requirements that trigger upgrades, and the typical scope of commissioning services per installation. When granular installation counts were not available, gaps were handled using proxy indicators such as yard throughput, retrofit seasonality, and procurement patterns confirmed through interviews, and then the assumptions were stress-tested before finalizing.

For forecasting, scenario analysis was used so the model could reflect different build-cycle and retrofit-cycle outcomes without forcing a single path. Growth variables were adjusted year by year using consensus ranges from primary experts, especially around shipyard capacity, capex intent from operators, and the pace of digital integration on commercial versus defense fleets.

Data Validation & Update Cycle

Validation was done by triangulating modeled totals against independent signals such as ship deliveries, retrofit activity levels, and the implied spend per vessel for integrated automation content. Outliers were reviewed by checking currency timing, one-off project effects, and whether a data point reflected integrated delivery or a standalone subsystem sale, and then adjustments were made with clear notes.

Before sign-off, the work is reviewed in multiple steps, including cross-checks by another analyst and a final sanity review against market drivers and constraints. Reports are refreshed annually, with interim updates when material events change build rates, retrofit incentives, or procurement momentum. Right before delivery, a fresh pass is completed so clients receive the latest updated view based on recently available public information, with re-contact triggers for sources when needed.

Mordor Intelligence's Integrated Marine Automation Systems Market Size Compared Against Other Published Estimates

Published market values for integrated marine automation systems can look far apart because each publisher draws the scope line in a different place and then applies different build and retrofit assumptions. Timing also matters since shipbuilding cycles move in waves, and a single strong year of orders can shift the near-term picture.

The key gap drivers usually come from what is treated as an integrated delivery versus a mix of standalone subsystems, how commissioning and software are counted, and whether the estimate leans more on newbuilds or on retrofit demand. Differences also show up when one model pushes faster ASP growth through aggressive digital upgrade assumptions, or when currency conversion and update cadence do not align with the same reference year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.06 B (2026) | |

| Global Consultancy A | USD 6.53 B (2024) | Uses an earlier reference year and a shorter forecast window, and it can also reflect a broader shipboard automation view that does not consistently separate fully integrated system deliveries from adjacent subsystem revenues. |

| Industry Publisher B | USD 5.11 B (2026) | Often relies on a narrower component and solution mix and may treat services and commissioning differently, which can compress the value captured per installation for integrated programs. |

The table shows a clear spread that mostly comes from where the integration boundary is placed and which revenue items are counted consistently across regions and vessel classes. In Mordor Intelligence's model, the scope is limited to integrated shipboard automation that combines hardware, software, and commissioning, while leaving out port automation, standalone sensors, and shore-only fleet software. Once those choices are aligned, the remaining difference is usually explained by the reference year used, the assumed balance of newbuild versus retrofit demand, and how pricing progression is applied across vessel categories.

Key Questions Answered in the Report

What is the current value of the integrated marine automation system market?

The integrated marine automation system market size is USD 8.06 billion in 2026.

How fast is demand for retrofit automation solutions growing?

Retrofit and upgrade projects are forecast to expand at a 12.19% CAGR from 2026 to 2031.

Which region is expected to post the highest growth rate through 2031?

The Middle East is projected to record the fastest 12.89% CAGR over the forecast period.

Which solution segment is expanding the quickest?

Analytics and predictive-maintenance software is set to grow at an 11.27% CAGR.

Why are defense buyers accelerating automation spending?

Naval modernization programs and the need for unmanned and cyber-resilient platforms push defense automation demand at a 10.19% CAGR.

What competitive advantage do edge-based systems offer?

Edge architectures ensure critical control functions continue during connectivity loss while lowering satellite bandwidth costs.

Page last updated on: