Nigeria Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

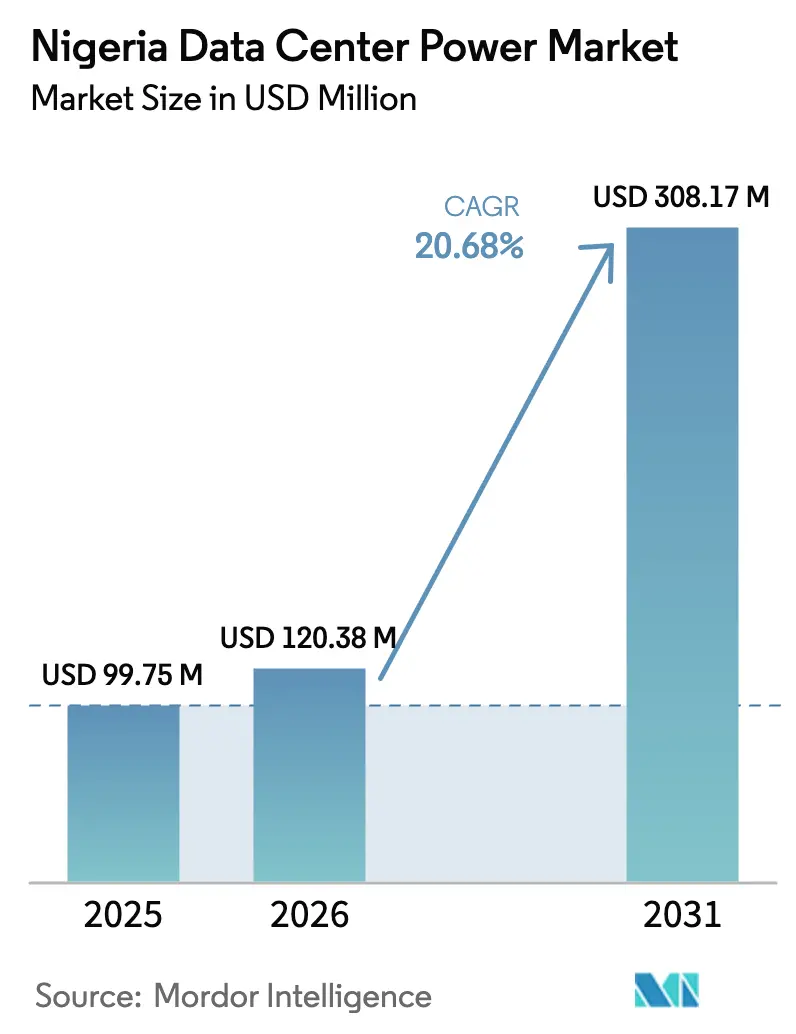

| Base Year Market Size (2025) | USD 99.75 Million |

| Market Size (2026) | USD 120.38 Million |

| Market Size (2031) | USD 308.17 Million |

| Growth Rate (2026 - 2031) | 20.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Data Center Power Market Analysis by Mordor Intelligence

The Nigeria data center power market size was valued at USD 99.75 million in 2025 and estimated to grow from USD 120.38 million in 2026 to reach USD 308.17 million by 2031, at a CAGR of 20.68% during the forecast period (2026-2031). Accelerated investment stems from the National Digital Economy Policy and Strategy 2020-2030, which elevates data centers to critical-infrastructure status. Operators confront an annual average of 4,600 minutes of grid outages, far above global benchmarks and forcing heavy reliance on backup systems. Growth concentrates on intelligent UPS platforms, gas-fired generators, and modular renewable micro-grids that offset diesel costs. Policy incentives, rising cloud adoption, and AI-driven rack densities exceeding 40 kW sustain long-term power-equipment demand across Lagos, Abuja, and emerging edge locations. Competitive advantage increasingly hinges on local partnerships, renewable-energy integration, and Tier-IV-ready modular deployments.

Key Report Takeaways

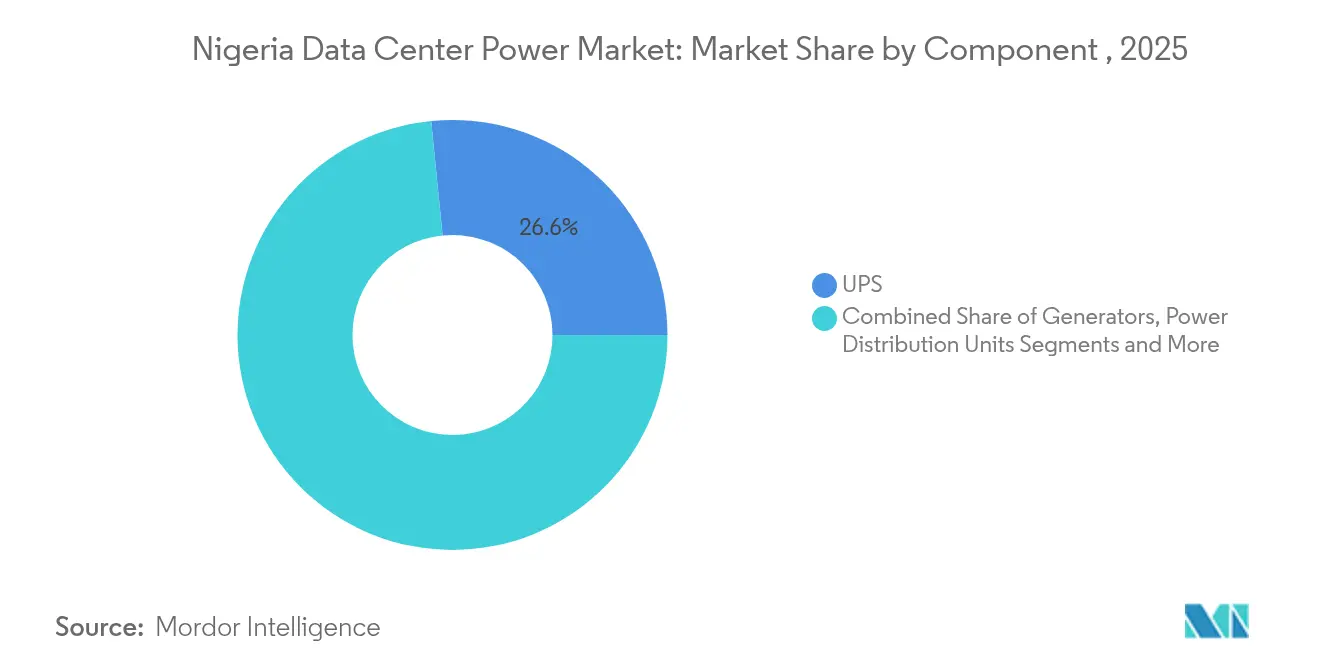

- By component, UPS systems led with 26.58% of Nigeria data center power market share in 2025, while power distribution units are forecast to expand at a 23.85% CAGR through 2031.

- By data-center type, colocation facilities held 51.12% of the Nigeria data center power market size in 2025; hyperscale/cloud service providers record the fastest projected CAGR at 24.55% to 2031.

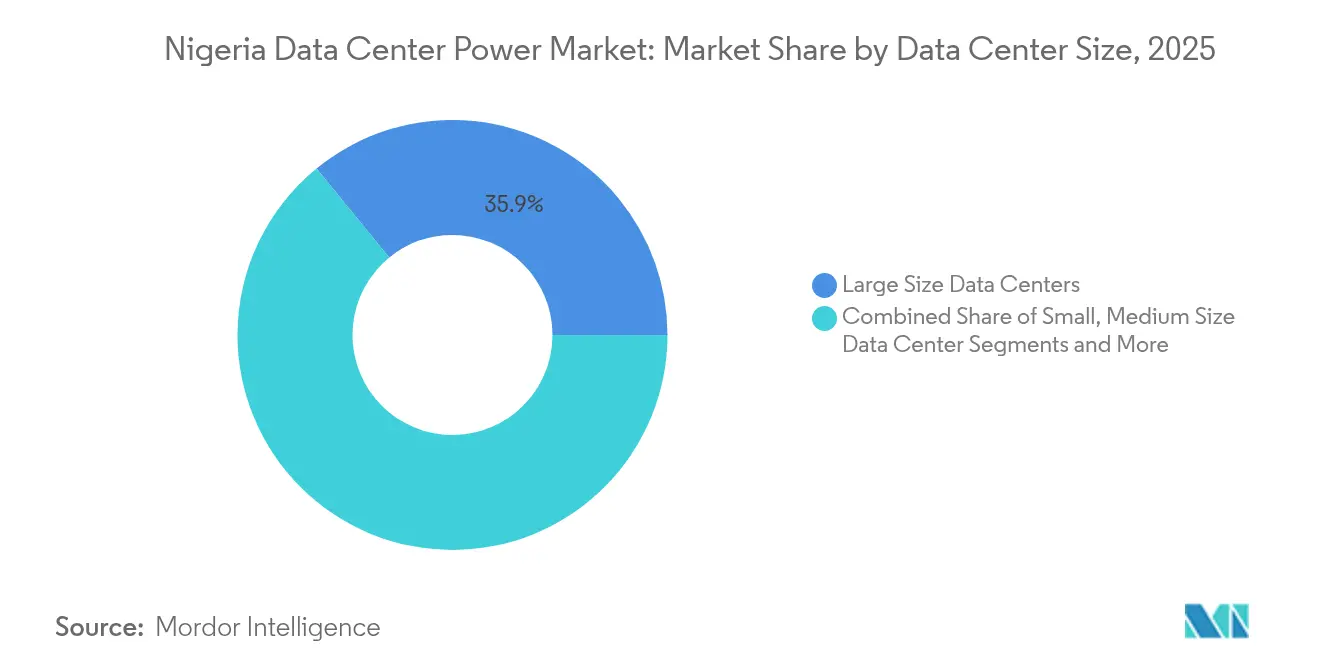

- By data-center size, large facilities accounted for 35.90% of the Nigeria data center power market size in 2025, whereas mega data centers are set to grow at a 27.9% CAGR.

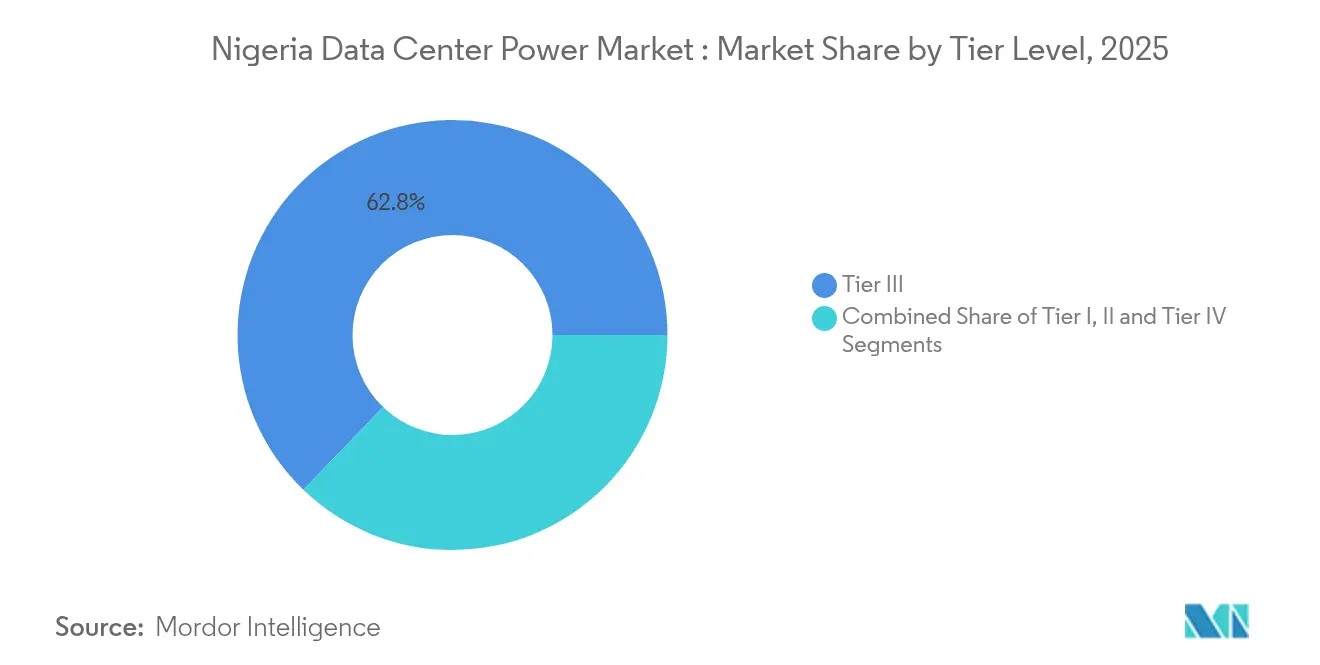

- By tier level, Tier III sites captured 62.80% of Nigeria's data center power market share in 2025, and Tier IV facilities are advancing at a 28.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mega data centres & cloud computing | +6.2% | National, concentrated in Lagos and Abuja | Medium term (2-4 years) |

| Increasing demand to reduce operational costs | +4.8% | National, with emphasis on industrial zones | Short term (≤ 2 years) |

| Government incentives for digital infrastructure & tax holidays | +3.5% | National, focused on special economic zones | Long term (≥ 4 years) |

| Surge in mobile-data traffic & 5G roll-out | +2.9% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Roll-out of renewable-energy micro-grids for data-centre campuses | +2.1% | National, prioritizing grid-constrained areas | Long term (≥ 4 years) |

| Emergence of edge facilities in oil- & gas-producing regions | +1.8% | Niger Delta, Port Harcourt, Warri corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Mega Data Centers & Cloud Computing

Hyperscalers are redefining the Nigeria data center power market by shifting from 5-10 MW halls to 100 MW campuses designed for AI workloads. Microsoft’s AI-optimised builds and MTN Nigeria’s 1,400-rack Tier IV project illustrate demand for power densities exceeding 40 kW per rack. The transition drives procurement of modular UPS blocks, busway-fed PDUs, and redundant 33 kV feeders that sustain 99.995% availability. As high-density racks proliferate, intelligent power-distribution software balances heterogeneous loads across battery, grid, and on-site gas micro-grids, ensuring fault-tolerant operations. Supply-chain partners that can pre-fabricate Tier-IV-ready power rooms now win the bulk of mega-facility contracts across Lagos and Abuja. The result is sustained double-digit expansion of the Nigeria data center power market throughout the forecast period.

Increasing Demand to Reduce Operational Costs

Diesel accounts for up to 70% of backup-power OPEX, prompting operators to diversify into gas, solar, and battery options that slash fuel spend. Aggreko’s 5 MW gas-generation project for MTN Nigeria cut energy costs by 40% compared with diesel sets. [1]Aggreko Plc, “Aggreko and MTN Nigeria Cut Fuel Costs with 5 MW Gas Solution,” aggreko.com Predictive maintenance tools further trim service visits and extend component life, while solar-plus-storage PPAs shield budgets from volatile fossil-fuel pricing. These economics are forcing a redesign of generator sizing, UPS autonomy, and battery chemistries across the Nigeria data center power market. Vendors that deliver hybrid-ready switchgear and cloud-based energy-management platforms gain clear cost-leadership advantages.

Government Incentives for Digital Infrastructure & Tax Holidays

The National Development Plan 2021-2025 and targeted special-economic-zone regimes grant duty-free imports, accelerated depreciation, and multi-year tax holidays to qualified data-center projects. [2]Federal Ministry of Finance“National Development Plan 2021-2025,” finance.gov.ngMandatory data localisation for banking and telecom workloads guarantees new capacity demand, driving sustained investment in UPS systems, medium-voltage switchgear, and lithium-ion battery strings. Incentive continuity over the plan horizon underpins long-cycle purchasing confidence for OEMs and EPCs active in the Nigeria data center power market. Companies aligning with localisation rules and renewable-energy quotas secure fast-track approvals and grid-connection easements.

Surge in Mobile-Data Traffic & 5G Roll-Out

5G sites consume 3-4 × more power than 4G and require sub-10 ms latency backhaul to edge nodes. Nigeria’s spectrum awards to MTN Nigeria and Mafab trigger thousands of small-cell builds, each demanding compact UPS units, DC-DC converters, and remote-monitoring PDUs. [3]American Tower, “ Backup Power Solutions,” americantower.comEdge data centers clustered near base stations rely on integrated battery-generator hybrids to keep unmanned sites online during grid sags. This distributed topology expands the Nigeria data center power market beyond tier-one cities into secondary urban hubs, lifting demand for ruggedised switchgear and solar-ready micro-inverters

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation & maintenance cost | -3.2% | National, acute in secondary cities | Short term (≤ 2 years) |

| Unreliable national grid & frequent outages | -2.8% | National, severe in non-urban areas | Medium term (2-4 years) |

| Diesel-price volatility driving OPEX uncertainty | -2.1% | National, concentrated in diesel-dependent facilities | Short term (≤ 2 years) |

| Constraints on domestic gas supply for on-site generation | -1.5% | National, focused on gas-dependent installations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation & Maintenance Cost

Comprehensive power infrastructure equals 30-40% of Nigerian build budgets. Imported UPS frames, explosion-proof gear, and lithium-ion batteries expose projects to forex swings and 6-12-month lead-times. Maintenance costs rise as certified technicians remain scarce, forcing expensive fly-in support agreements. These hurdles limit smaller entrants and slow roll-outs in secondary metros. Consequently, modular containerised power rooms that ship pre-tested are gaining traction across the Nigeria data center power market, reducing on-site labour by up to 50%.

Unreliable National Grid & Frequent Outages

Nigeria’s grid recorded 46 system collapses between 2017 and 2023, subjecting equipment to voltage sag and accelerated wear. Operators over-provision generators and UPS capacity, driving capital inefficiencies while inflating OPEX. Voltage-conditioning transformers, harmonic filters, and rapid-transfer switches become compulsory, raising BOM costs for every new facility. Until grid reforms advance, over-building for redundancy remains a structural drag on the Nigeria data center power market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead Despite PDU Acceleration

UPS platforms captured 26.58% of the Nigeria data center power market size in 2025, underscoring their role in voltage regulation and instant switchover during grid loss. Lithium-ion battery strings now dominate new UPS orders, doubling cycle life while cutting footprint versus VRLA alternatives. In parallel, intelligent PDUs are the fastest risers at a 23.85% CAGR, propelled by rack-level metering and branch-circuit analytics that align power draw with AI workload bursts. Generator demand remains solid, yet fuel diversification is reshaping the mix toward gas gensets that trim diesel exposure. Early pilot projects involving hydrogen fuel-cell backup, such as Vertiv’s collaboration with Ballard, hint at future shifts in the Nigeria data center power market.

The services ecosystem grows in lock-step: predictive-maintenance software, harmonic-analysis consulting, and turnkey EPC packages now account for a rising share of revenue. Vendors offering integrated design-install-maintain models command premium margins, especially when paired with remote-monitoring dashboards that reduce site visits in grid-constrained regions.

By Data Center Type: Colocation Dominance Challenged by Hyperscale Growth

Colocation operators held 51.12% of the Nigeria data center power market share in 2025, benefiting from carrier-neutral cross-connects and multi-tenant economics. Rack Centre’s uninterrupted service record illustrates the segment’s reliability premium. Hyperscale/cloud builds, however, are scaling faster at a 24.55% CAGR and push power-architecture complexity higher with 100 MW campus designs. AI training clusters demand hot-aisle temperatures and liquid-cooled racks, prompting custom busway designs and in-row UPS modules. Enterprise and edge facilities round out the mix, driven by oil-and-gas analytics nodes that need explosion-proof switchgear and local gas-fed generators.

Growth in all types reinforces the Nigeria data center power market as a multi-modal opportunity: OEMs must tailor gear for both mega-campuses and ruggedised edge pods. Regulatory localisation clauses further consolidate demand among domestic colocation players, while sovereign-cloud mandates draw hyperscalers into joint-venture builds with local ISPs.

By Data Center Size: Mega Facilities Drive Future Expansion

Large sites dominated installations with 35.90% of the Nigeria data center power market size in 2025, yet mega facilities will post a 27.9% CAGR as hyperscalers consolidate capacity. MTN Nigeria’s planned 20 MW campus and Open Access Data Centres’ 7,200 m² Lagos build exemplify mega-scale momentum Such footprints require 132 kV grid connections, dual utility feeders, and sectionalised switchyards to satisfy uptime SLAs. Power demand scales non-linearly, compelling investment in dynamic-bus UPS lineups and peak-shaving battery arrays.

Small and medium sites retain relevance for edge workloads and enterprise colocation, especially where real-estate constraints and latency demands coexist. Containerised power blocks allow operators to incrementally add 1-2 MW of capacity, maintaining capital efficiency while serving emerging secondary cities.

By Tier Level: Premium Standards Accelerate Despite Tier III Leadership

Tier III facilities represented 62.80% of installations in 2025, balancing cost and 99.982% uptime expectations. Nevertheless, Tier IV builds are expanding at a 28.96% CAGR, catalysed by financial services compliance and oil-and-gas reliability mandates. Galaxy Backbone’s dual Tier IV certification delivered via Huawei’s pre-fabricated modules validates the viability of rapid Tier IV deployment in Nigeria. Tier certification drives heightened demand for redundant UPS strings, concurrently operated generators, and closed-transition switches.

Uptime Institute audits enforce rigorous design scrutiny, spurring OEM innovation in self-diagnosing UPS firmware and smart breakers that report MTBF metrics in real time. As operators compete on SLA differentiation, Tier-IV features such as concurrently maintainable distribution paths and fault-tolerant control systems become mainstream across the Nigeria data center power market.

Geography Analysis

The Nigeria data center power market concentrates heavily in Lagos, where seaport logistics, fibre-landing stations, and financial-services clusters co-locate. High land costs and grid instability force Lagos operators into gas-gen hybrids and rooftop solar arrays to meet 100% uptime SLAs. Abuja follows as a policy-driven hub, hosting federal workloads that demand on-shore data residency. Proximity to regulators accelerates permitting, while government agencies increasingly impose Tier III minimum standards on hosting suppliers.

Secondary markets Port Harcourt, Kano, and Ibadan emerge as edge locations aligned with industrial corridors. Niger Delta sites leverage abundant associated gas for cost-effective on-site generation, whereas northern states opt for solar-heavy micro-grids due to high insolation. Benin City’s state-owned facility marks the first decentralised government deployment outside Lagos and Abuja, underscoring geographic diversification.

Competitive Landscape

Competition is moderately fragmented, with ABB, Schneider Electric, and Vertiv supplying high-end switchgear, UPS, and prefabricated power rooms alongside regional integrators that provide site services. Global players differentiate through intelligent PDUs and integrated renewable-energy micro-grids that address Nigeria’s diesel-cost burden. For example, Vertiv’s hydrogen-backup pilot signals a push into zero-carbon resiliency options.

Local system integrators focus on maintenance contracts, battery-refresh projects, and edge-site roll-outs where deep knowledge of logistics and regulatory regimes is vital. Partnerships between OEMs and telecom operators such as MTN Nigeria accelerate time-to-market for mega campuses, while joint ventures with oil-and-gas majors drive ruggedised edge deployments. Competitive priority now centres on delivering full-life-cycle services—from financing to remote monitoring—rather than stand-alone equipment sales.

Nigeria Data Center Power Industry Leaders

ABB Ltd

Schneider Electric SE

Vertiv Group Corp.

Eaton Corp. plc

Caterpillar Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Cassava Technologies unveiled plans for an Africa-wide AI factory, integrating Nvidia systems into Nigerian data centers to support high-density workloads.

- February 2025: Schneider Electric introduced TeSys Deca Advanced contactors that cut energy use and CO₂ by 22%, applicable to data-center power trains.

- February 2025: NITDA urged domestic data centers to scale capacity, reinforcing policy support for local infrastructure.

- January 2025: Wärtsilä agreed to supply equipment for a new Nigerian gas-fired plant aimed at stabilising power for data-center operators.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Nigeria data center power market as the value of electrical infrastructure, uninterruptible power supply units, diesel or gas generators, power distribution units, switchgear, cabling, and related monitoring services installed in new and existing carrier-neutral, enterprise, edge, hyperscale, and government data centers.

Scope exclusion: Cooling equipment, IT compute hardware, software-only DCIM tools, and civil works are outside this valuation.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews and follow-up surveys with facility operators, OEM specialists, electrical engineers, and energy regulators across Lagos, Abuja, Port Harcourt, and Kano helped us validate grid downtime figures, rack density trends, landed generator pricing, and typical service mark-ups. Insights from hyperscale architects and regional colocation managers enabled us to align utilization ramps and renewable mix scenarios with on-the-ground reality.

Desk Research

Mordor analysts gathered baseline inputs from open datasets issued by bodies such as the Nigerian Communications Commission, National Bureau of Statistics, Nigerian Electricity Regulatory Commission, and the Africa Data Centres Association, together with trade filings, investor decks, customs shipment logs, and peer-reviewed power engineering journals. We then enriched these with energy mix statistics from the International Energy Agency and grid reliability reports from the Transmission Company of Nigeria, before cross-checking company financials through D&B Hoovers, news flows on Dow Jones Factiva, and shipment counts on Volza. A final sweep of government gazettes, patent abstracts (Questel), and public procurement portals clarified pipeline capacity and import duties. This list is illustrative; many other secondary sources were reviewed to tighten assumptions and verify anomalies.

Market-Sizing & Forecasting

A top-down model converts national IT load build-outs and average capex per megawatt into spend, which is then sanity checked through selected bottom-up approximations such as sampled ASP by component multiplied by shipment volumes from import records. Key variables include annual MW capacity additions, grid availability minutes, diesel price index, average rack density, and share of lithium-ion UPS deployments. Forecasts blend multivariate regression with scenario analysis to capture fuel price and policy uncertainty; outliers are reconciled through iterative expert feedback. Gap areas in bottom-up inputs, especially for private builds, are bridged using regional benchmarks and disclosed vendor shipments.

Data Validation & Update Cycle

Model outputs pass a three-layer review: automated variance checks, senior analyst reconciliation, and a pre-publication refresh tied to new facility announcements or policy shifts. Reports are fully updated every twelve months, with interim patches when material events trigger our alert system.

Why Mordor's Nigeria Data Center Power Baseline Earns Trust

Published estimates often diverge because firms pick different component baskets, price points, and refresh speeds.

Key gap drivers here include whether standby generators are costed at purchase or full lifecycle value, the treatment of Tier I and II edge sites, currency translation timing, and how quickly analysts bake in hyperscale contracts still at memorandum stage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 99.75 M (2025) | Mordor Intelligence | - |

| USD 135 M (2024) | Regional Consultancy A | excludes Tier IV builds, applies lower rack density assumption and slower diesel inflation curve |

| USD 82.30 M (2024) | Industry Association B | counts only commissioned capacity, omits announced projects and uses historical exchange rates |

Taken together, the comparison shows that Mordor's balanced scope, live project tracking, and annual refresh cadence deliver a dependable midpoint that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Nigeria data center power market?

It stands at USD 120.38 million in 2026 and is projected to grow to USD 308.17 million by 2031

Which component captures the largest market share?

UPS systems lead with 26.58% of Nigeria data center power market share as of 2025.

How do government incentives influence investment?

Tax holidays, duty-free imports, and accelerated depreciation reduce project payback periods, stimulating new builds in special economic zones.

What role does renewable energy play in data-center power strategies?

Solar-plus-storage micro-grids and gas-fired generators lower OPEX and reduce reliance on volatile diesel supply

Page last updated on: