Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

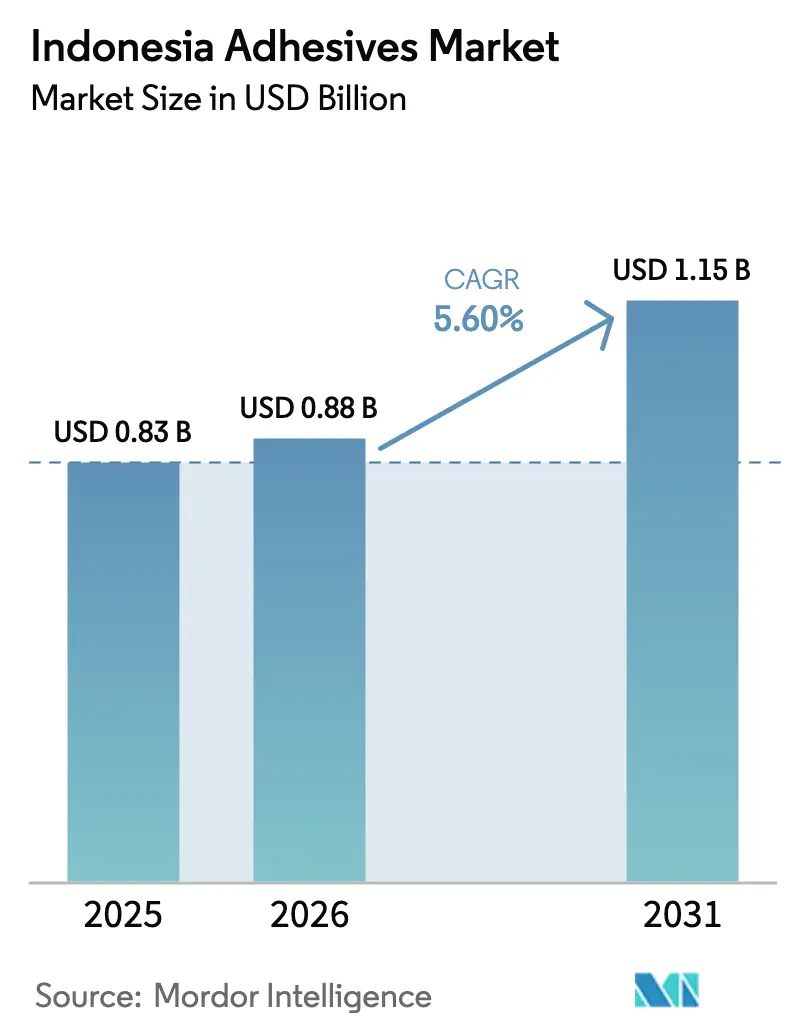

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Adhesives Market Analysis by Mordor Intelligence

The Indonesia Adhesives Market size is expected to grow from USD 0.83 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 1.15 billion by 2031 at 5.6% CAGR over 2026-2031. Demand gains stem from robust infrastructure spending, fast-growing packaging volumes, and steady automotive production, all of which anchor consumption in construction, corrugated cases, and vehicle assembly. Public funding of USD 410 billion for strategic projects through 2024, plus the multiyear build-out of Nusantara as the new capital, secures a long pipeline of bonding and sealing requirements. E-commerce fulfillment centers raise throughput of tamper-evident and moisture-resistant packs, while OEM (original equipment manufacturer) adoption of low-VOC chemistries spurs product upgrades in factories concentrated along Java’s industrial corridors. Competitive intensity remains moderate as multinationals leverage technical support and local firms exploit proximity advantages, yet fragmented shipment networks outside Java leave room for distributors that can cut last-mile costs.

Key Report Takeaways

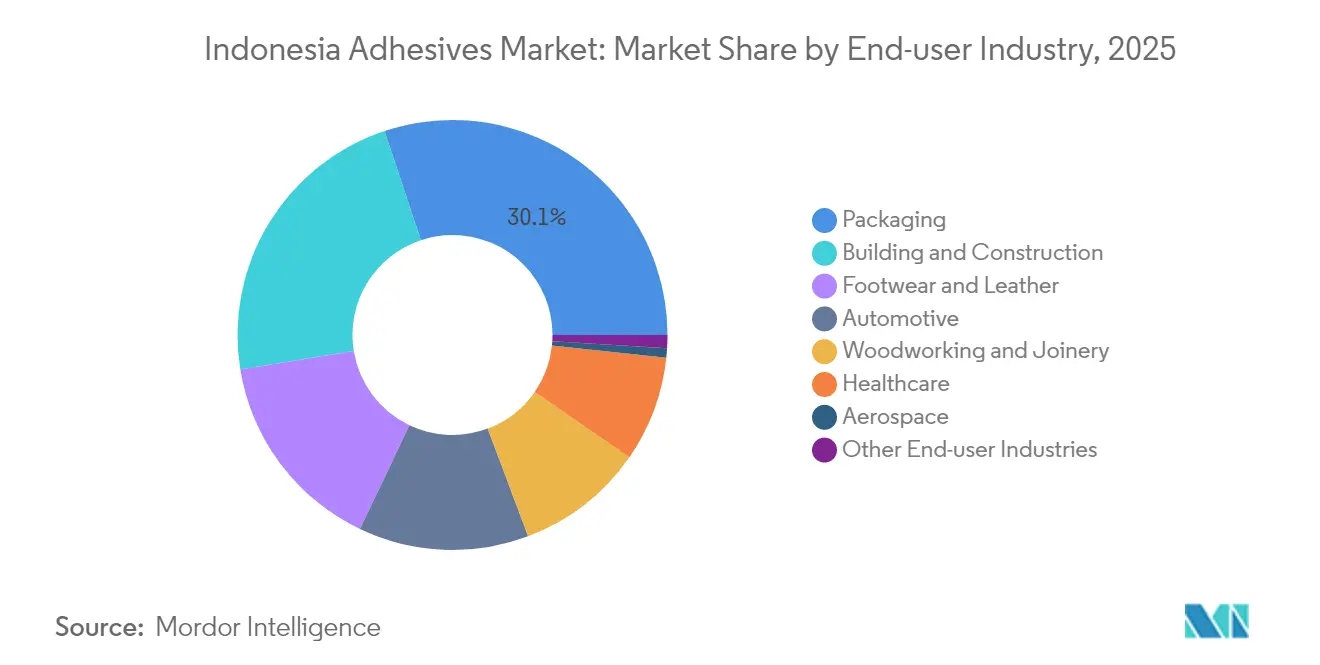

- By end-user industry, packaging led with 30.12% of the Indonesia adhesives market share in 2025; healthcare applications are advancing at a 6.35% CAGR to 2031.

- By technology, water-borne systems captured 45.88% of the Indonesia adhesives market size in 2025, while UV-cured lines are projected to expand at a 6.72% CAGR through 2031.

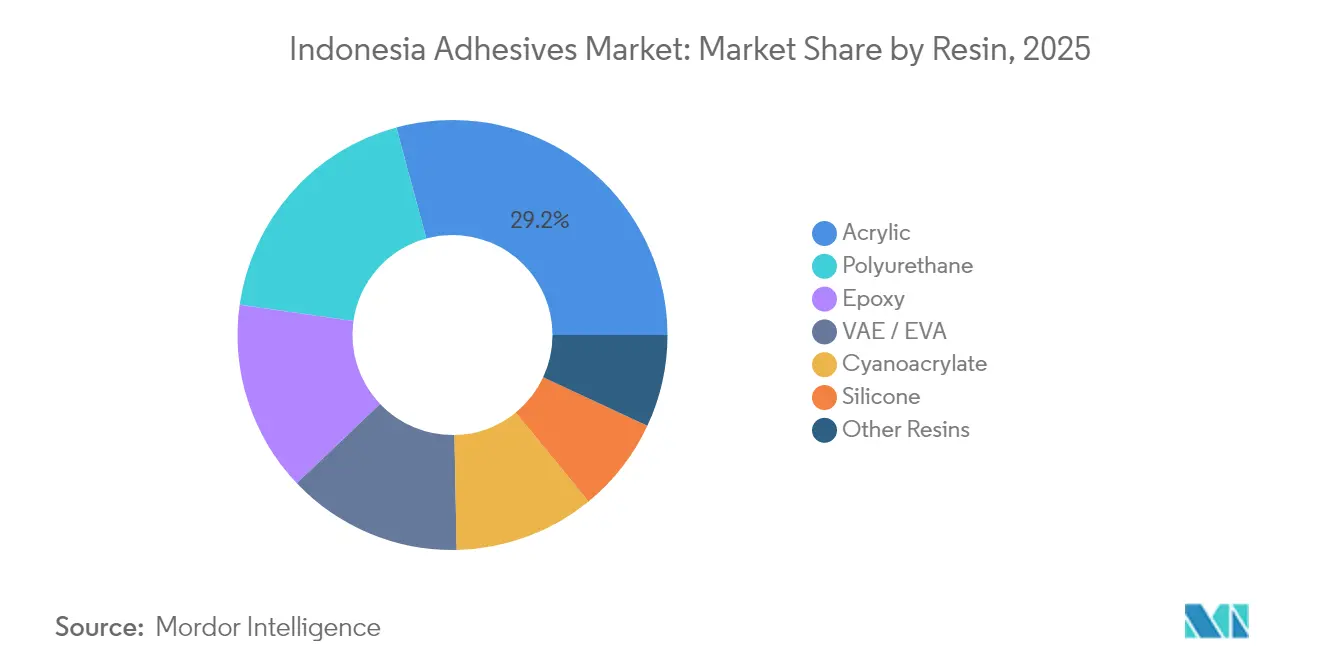

- By resin, acrylics commanded 29.21% of the Indonesia adhesives market size in 2025 and cyanoacrylate volumes are forecast to grow at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing domestic packaging industry | + 1.80% | National, concentrated in Java and Sumatra | Medium term (2-4 years) |

| Rapid e-commerce penetration | + 1.50% | National, urban centers leading | Short term (≤ 2 years) |

| Infrastructure and housing push | + 2.10% | National, emphasis on eastern regions | Long term (≥ 4 years) |

| OEM shift to water-borne technologies | + 0.90% | Java industrial corridors | Medium term (2-4 years) |

| Rise of halal-certified adhesives | + 0.70% | National, with emphasis on Muslim-majority regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Domestic Packaging Industry

Indonesia’s packaging chain continues to evolve from commodity export packing toward value-added protective formats for processed food, beverage, and personal-care shipments. Downstream nickel, palm, and wood processors now emphasize branded consumer packages that demand robust laminating, case-sealing, and label adhesives. Local carton plants running high-speed flexo lines prefer water-borne and hot-melt grades that meet food-contact and halal requirements. Several private label beverage fillers in West Java switched from solvent-borne to water-borne spine-gumming during 2025 to align with stricter VOC limits in factory permits. Ongoing capacity start-ups at integrated petrochemical sites in Merak and Cilegon improve feedstock access for vinyl acetate monomer, supporting the indigenous supply of pressure-sensitive grades. National standards agency BPOM is finalizing updated migration thresholds for flexible pouches, which should further lift demand for compliant acrylic dispersions in 2026[1]Badan Pengawas Obat dan Makanan, “Guidelines on Food-Contact Adhesives,” bpom.go.id.

Rapid E-commerce Penetration

Parcel volumes crossing fulfillment hubs in Greater Jakarta rose by 14% year-on-year during 2024 according to the Ministry of Communications, accelerating adoption of fast-curing UV-cured carton sealers that prevent line bottlenecks at sortation centers. Consumer-ready pack sizes translate into more linear meters of bonding per shipped kilogram than bulk industrial drums, magnifying adhesive intensity. Marketplace operators mandate tamper-evident tapes for electronics and beauty products to curb return fraud, a spec that favors instant-tack hot-melt lines. Recyclable mailers require easy-peel water-borne seal strips that survive Indonesia’s humid climate until arrival in remote islands. Electronic invoicing and customs pre-clearance streamline cross-border flows, which, combined with lower payment friction under the bilateral Rupiah-Yuan settlement scheme, adhesive demand for export packs resilient.

Infrastructure and Housing Push

Public works outlays continue to channel bond, seal, and grout products into toll roads, ports, hospitals, and social housing estates. The National Development Planning Agency targets 4.5 million new affordable homes by 2029, each consuming tile, flooring, and panel adhesives that simplify installation in high-humidity zones. Asphalt overlays on Trans-Sumatra and Trans-Papua motorways adopt polymer-modified strips that rely on polyurethane binders for crack resistance. Climate-resilient design codes published by the Ministry of Public Works now recommend flexible joint sealants rated at 50% elongation, raising volumes of silicone hybrids in bridge and seawall projects. As site contractors adopt prefabricated panels to reduce labor risks, factory-applied structural adhesives increasingly replace mechanical fasteners. These factors jointly underpin a long-dated demand curve for high-performance chemistries in the Indonesia adhesives market.

OEM Shift to Water-borne Technologies

Motorcycle and passenger-car plants in Bekasi, Karawang, and Surabaya accelerated trials of water-borne seam sealers during 2024 to cut solvent emissions and secure green-building credits for exported vehicles. Battery pack assemblers for locally produced hybrid models specify low-VOC acrylics that manage heat cycling and resist electrolyte leaks. Global Tier 1 suppliers have begun training local technicians in rheology adjustment and spray-booth humidity control to optimize film build. As electric-vehicle content grows from 10% to 20% of national auto output by 2028, substrates shift toward lightweight aluminum and composites, where water-borne hybrids offer superior multi-material adhesion. Government excise incentives for low-emission models raise production forecasts and underpin incremental gains for water-dilutable chemistries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile MDI and acrylic raw-material prices | -1.20% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Fragmented distribution network outside Java | -0.80% | Eastern regions, outer islands | Long term (≥ 4 years) |

| Limited cold-chain logistics for moisture-sensitive grades | -0.50% | Eastern regions, humid coastal areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile MDI and Acrylic Raw-Material Prices

Feedstocks make up roughly two-thirds of the total manufacturing cost in typical adhesive plants. Polyurethane lines feel the squeeze first when import parity prices for methylene diphenyl diisocyanate swing by double digits in a single quarter. Acrylic monomer economics also face pressure as regional crackers juggle naphtha margins. Spot shipments arriving at Tanjung Priok saw a 12% price spike during Q2 2025 after an unplanned outage in Taiwan curtailed supply. Smaller domestic formulators often lack long-term offtake contracts and must pass higher input costs, risking share loss to integrated multinationals. Price fluctuations complicate fixed-price tenders with construction contractors that run for multi-year project phases, making volume commitments harder to secure.

Fragmented Distribution Network Outside Java

Indonesia’s archipelagic geography imposes trans-shipment, inter-island barge, and feeder costs that raise delivered prices in the east by as much as 35% compared with Java. Terminal handling alone can represent nearly one-third of the Jakarta–Pontianak freight bill. Moisture-sensitive water-borne and cyanoacrylate grades require refrigerated containers that remain scarce on return legs, pushing inventory buffers higher. Dealers in Makassar and Manokwari frequently run out of specialty cartridges, forcing builders to substitute lower-spec products or delay work. Government e-logistics initiatives encourage shared warehousing, yet small fleet operators' digital platform uptake remains slow. Until door-to-door visibility improves, the Indonesia adhesives market will continue to concentrate around Java and North Sumatra.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Packaging Leads Multi-Sector Expansion

Packaging retained a 30.12% slice of the Indonesian adhesives market size in 2025, reflecting heavy reliance on corrugated shippers, flexible laminations, and folding cartons that protect processed goods traveling long, humid routes. Surging parcel traffic and supermarket private-label growth lift liner board throughput, and each square meter of board draws roughly 18 g of starch-reinforced water-borne glue. Healthcare consumption, though smaller in baseline, logs the quickest trajectory at 6.35% CAGR by 2031 as local device plants scale up disposable syringes and wound-closure strips that depend on medical-grade acrylic pressure-sensitives. Construction absorbs significant volume in tile, panel, and roofing applications, while automotive remains an innovation driver for anti-flutter and structural epoxy lines.

Indonesia's adhesives market demand in footwear remains in West Java’s sneaker hubs, where ethylene-vinyl acetate hot-melts bond midsoles to uppers at cycle times under 6 seconds. Woodworking steady gains trace to furniture export ambitions of USD 5 billion in 2024, albeit tempered by import competition. Aerospace still accounts for under 1% of tonnage, but opens a niche for high-temperature silicone and toughened epoxy systems as state-owned plane maker PT Dirgantara grows composite component output. Across all uses, brand owners now request halal compliance seals, raising certification costs yet bolstering consumer trust.

By Technology: Water-borne Dominance Amid UV Innovation

Water-borne chemistries delivered 45.88% of transaction value in 2025 and remain the anchor technology in the Indonesia adhesives market as governments tighten worker-exposure and plant-emission rules. Acrylic dispersions dominate corrugated case and label sticking, whereas polyurethane dispersions serve parquet flooring and flexible laminates needing higher heat resistance. UV-cured formulas, only 7% of the base year total, hold the swiftest outlook at 6.72% CAGR to 2031 because instant cures slash line space and energy bills, a key benefit in Indonesia’s cost-sensitive packaging plants.

Hot-melt stays relevant in shipping cases and hygiene disposables, prized for solvent-free chemistry and immediate bond strength. Reactive one-part polyurethane keeps traction in insulated panel and vehicle roof bonding, where high peel strength offsets premium price tags. Solvent-borne shares erode by roughly 20 basis points yearly, yet pockets such as leather finishing still rely on their deep penetration characteristics. Lotte Chemical’s incoming cracker assurance of domestic VAM and EVA feed boosts supply security for dispersions and hot-melts, potentially trimming price spreads versus imported solvent lines.

By Resin: Acrylic Leadership Challenged by Specialty Growth

Acrylic backbones made up 29.21% of sales in 2025 thanks to unmatched versatility, acceptable price points, and food-contact clearances that match Indonesia’s halal processing mandates. Usage extends from carton sealing tapes and pressure-sensitive labels to metal roofing panel laminations. Cyanoacrylate—notorious for instant cure on rubber, plastics, and skin—posts the fastest gains at 6.08% CAGR through 2031 as demand for electronics micro-bonding, disposable medical devices, and DIY (Do it yourself) repair kits scales.

Polyurethane chemistry rides construction growth where flexibility and water resistance matter, while epoxy systems cater to structural steel and marine craft that face prolonged salt spray. Silicones, albeit niche, are critical for joint sealant jobs exposed to monsoon cycles and thermal shocks. VAE/EVA blends enjoy uptake in parquet flooring and paper packaging, capitalizing on a favorable mix of adhesion and elasticity at competitive cost. Feedstock volatility remains a specter; integrated resin suppliers with backward linkages into isocyanate, styrene, or ethylene chains hold an edge on margin stability.

Geography Analysis

Java currently houses roughly 69.20% of national adhesive consumption, fueled by dense packaging, automotive, and consumer goods production clusters. Port access at Tanjung Priok and Tanjung Emas ensures a steady inflow of imported feedstocks, while proximity to customers slashes lead times to under two days. The island also hosts most formulation plants, including Bekasi sites operated by Sika and PT Pamolite, supporting agile product customization.

Sumatra contributes an estimated 15.40% share, powered by pulp, paper, and palm oil downstreamers in Riau and North Sumatra provinces. Corrugated board mills near Medan feed export mango and durian shipments to East Asia, pulling in water-borne MR-grade adhesives that resist tropical condensate. Planned grassroots PET and biaxially oriented polypropylene film lines in Lampung will expand flexible-pack laminating requirements. Aspirations for the Indonesian adhesives market in Sumatra remain tied to improving road links under the Trans-Sumatra tollway, which trims trucking times to Java ferries.

Kalimantan, Sulawesi, and Papua collectively represent less than one-fifth of tonnage today, but log the fastest growth as nickel processing, renewable energy projects, and new ports break ground. The move of national capital to East Kalimantan accelerates public-building demand for sealants compliant with high-humidity coastal settings. Logistics challenges endure, with freight surcharges adding up to USD 170 per 20-foot equivalent container versus Java routes. Government initiatives under the Sea Toll Program aim to shave the gap by widening roll-on/roll-off services and subsidizing back-haul cargo, improvements that will raise the Indonesia adhesives market addressable volume over the long term.

Competitive Landscape

The Indonesia Adhesives market is moderately consolidated. Sika’s 2024 investment in Bekasi more than doubled site capacity for tile and construction adhesives, underscoring faith in infrastructure-led pull. Henkel localizes carton-sealing grades in West Java to shorten supply cycles for e-commerce hubs, while 3M cross-licenses pressure-sensitive technology to an Indonesian coater to meet halal certification timelines. These moves reflect a strategic pivot from purely imported drums toward integrated regional operations that hedge currency risk and honor local-content quotas. Sustainability credentials—halal, ISO 14001, and EPD documentation—progressively influence tender scores in public works, nudging lagging firms to upgrade compliance infrastructure or risk procurement exclusion.

Indonesia Adhesives Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Pidilite Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Sika announced that it has more than doubled the production capacity at the Bekasi plant, its biggest manufacturing facility in Indonesia. The site specializes in producing mortars such as tile adhesives, grouts, and wall and facade systems.

- August 2024: Azelis, a key player in the specialty chemicals sector, signed a distribution deal with Allnex in Indonesia. Under this agreement, Azelis will distribute Allnex's additives, catering to the coatings, adhesives, sealants, and elastomers (CASE) segment. This move is poised to bolster Indonesia's adhesive market.

Indonesia Adhesives Market Report Scope

Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery are covered as segments by End User Industry. Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne are covered as segments by Technology. Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA are covered as segments by Resin.By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

By Technology

| Hot-Melt |

| Reactive |

| Solvent-borne |

| UV-Cured Adhesives |

| Water-borne |

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE / EVA |

| Other Resins |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| By Technology | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| UV-Cured Adhesives | |

| Water-borne | |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE / EVA | |

| Other Resins |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms