India Self-Monitoring Blood Glucose Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

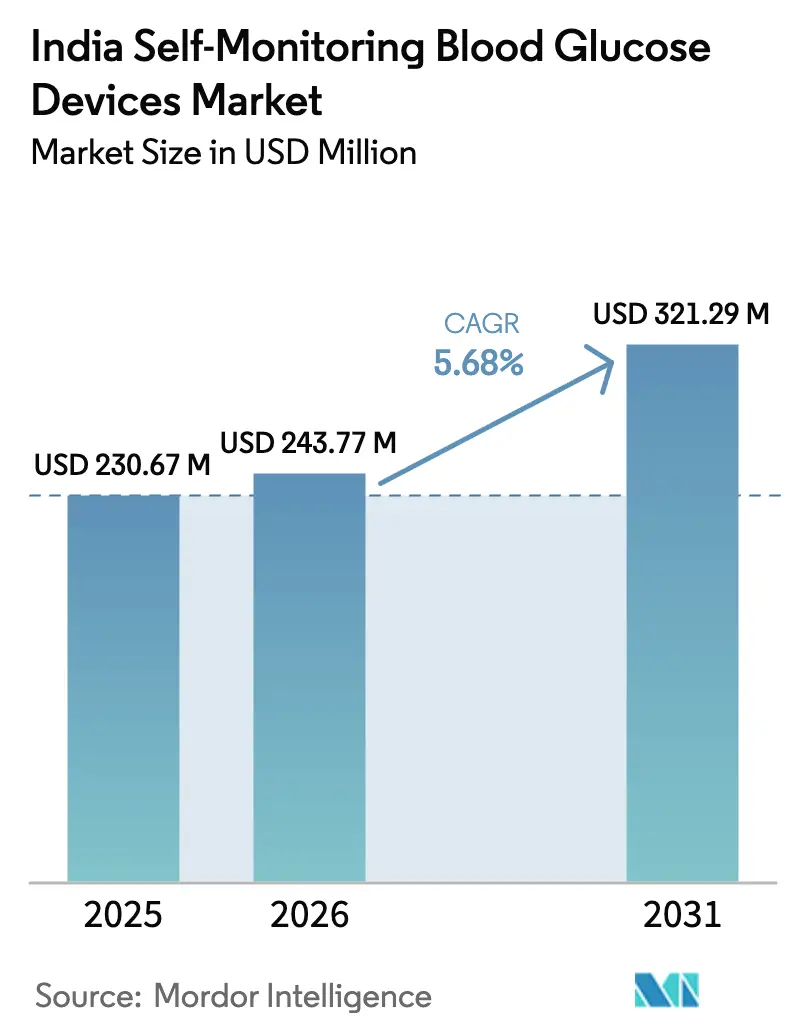

| Base Year Market Size (2025) | USD 230.67 Million |

| Market Size (2026) | USD 243.77 Million |

| Market Size (2031) | USD 321.29 Million |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

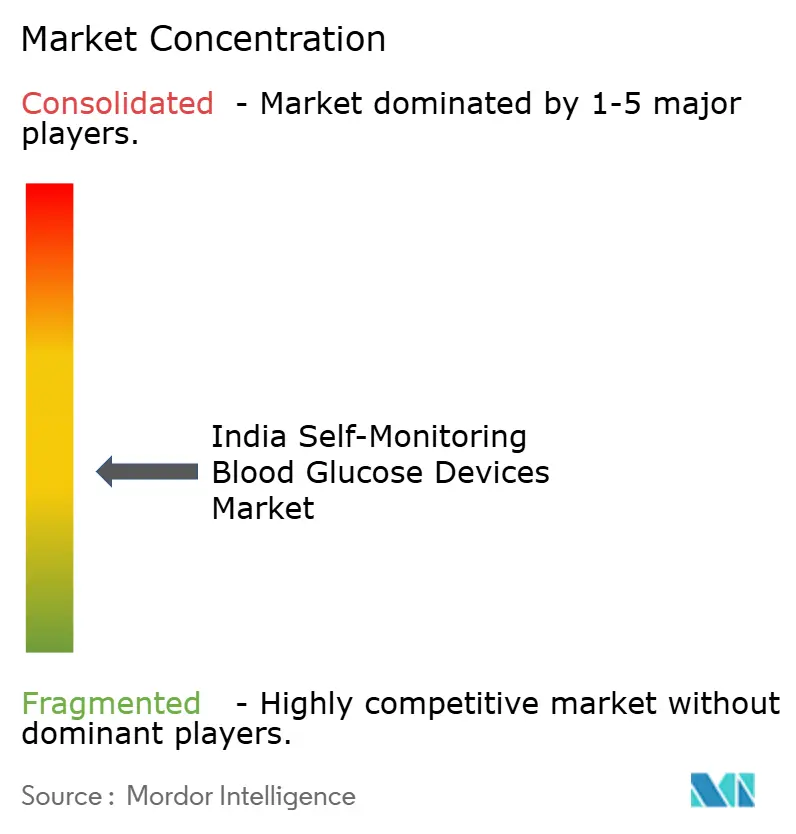

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Self-Monitoring Blood Glucose Devices Market Analysis by Mordor Intelligence

The India Self-Monitoring Blood Glucose Devices market size was valued at USD 230.67 million in 2025 and estimated to grow from USD 243.77 million in 2026 to reach USD 321.29 million by 2031, at a CAGR of 5.68% during the forecast period (2026-2031). Rising diabetes prevalence, earlier disease onset among working-age adults, and smartphone-enabled glucometers are propelling the India Self-Monitoring Blood Glucose Devices market. Government screening under the National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke has boosted detection volumes, while tightening quality regulations are sidelining refurbished imports and counterfeit strips. Domestic production incentives lower consumable costs, e-pharmacy subscriptions improve rural access, and AI-enabled coaching drives adherence, all reinforcing the expansion of the India Self-Monitoring Blood Glucose Devices market.

Key Report Takeaways

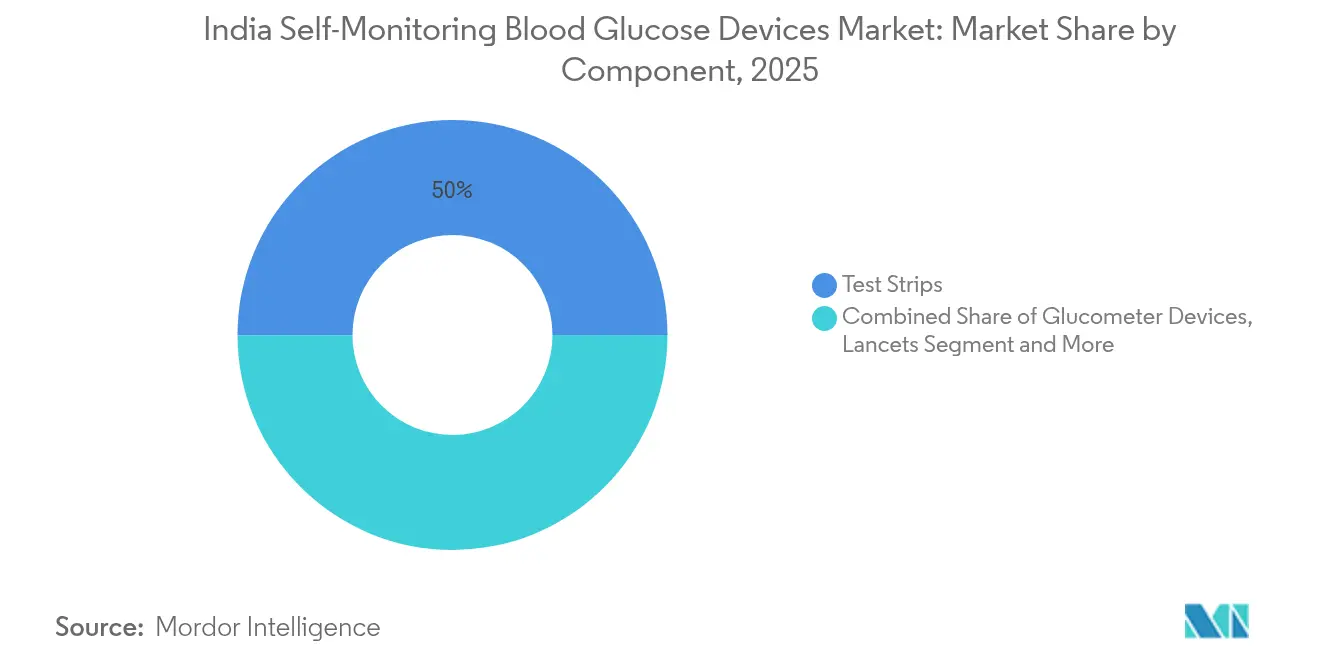

- By component, test strips led with 50.02% of the India Self-Monitoring Blood Glucose Devices market share in 2025; glucometer devices are expanding at an 10.74% CAGR through 2031.

- By technology, electrochemical biosensors commanded 76.10% revenue share in 2025, while smartphone-integrated dongles are projected to grow at a 15.28% CAGR to 2031.

- By end user, home-care patients accounted for 62.05% share of the India Self-Monitoring Blood Glucose Devices market size in 2025, with clinics & diagnostic labs advancing at a 12.35% CAGR through 2031.

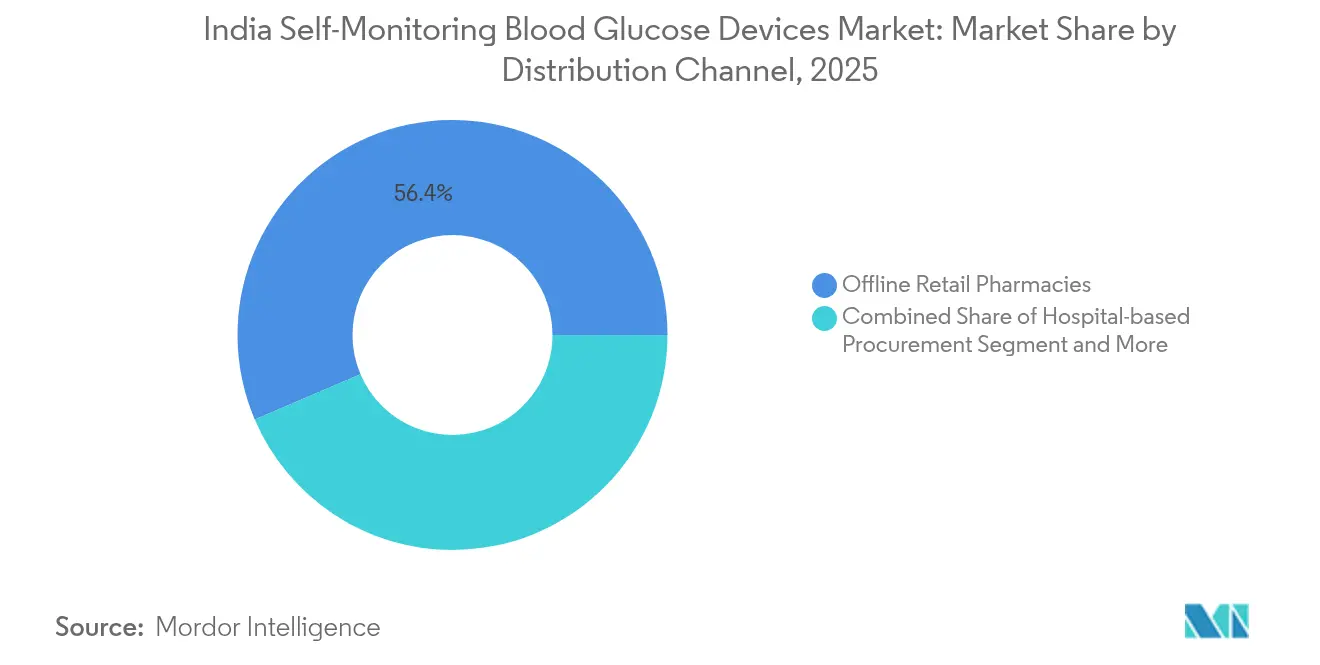

- By distribution channel, offline retail pharmacies held 56.42% revenue share in 2025; e-pharmacies & direct-to-consumer channels are forecast to register a 16.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Self-Monitoring Blood Glucose Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence & earlier onset | +1.2% | Urban metros and expanding peri-urban zones | Long term (≥ 4 years) |

| Government screening & subsidy programmes | +0.8% | National, early gains in rural and semi-urban districts | Medium term (2-4 years) |

| Higher disposable income & lifestyle awareness | +0.9% | Tier-1 and tier-2 cities, spreading to tier-3 | Medium term (2-4 years) |

| Digital-health integration with glucometers | +1.1% | Urban first, gradually permeating smaller markets | Short term (≤ 2 years) |

| E-pharmacy subscription penetration (tier-2/3) | +0.7% | Tier-2 and tier-3 cities with limited pharmacy density | Short term (≤ 2 years) |

| Localised strip manufacturing under PLI scheme | +0.6% | National production hubs, price relief country-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Earlier Onset

India’s 77 million adult Type 2 patient base, alongside 25 million prediabetic individuals, has intensified demand for self-testing devices. Earlier onset among professionals aged 25-40 pushes lifetime monitoring volumes higher and favors connected meters that fit digital lifestyles. The India Self-Monitoring Blood Glucose Devices market consequently records rising repeat purchases of strips and an uptick in premium device upgrades.

Government Screening & Subsidy Programmes

Nationwide screening now spans more than 700 districts, embedding glucose checks in public primary care. Tamil Nadu alone screened 2.5 million residents in 2024, stimulating downstream retail sales of meters and consumables[1]Government of Tamil Nadu, “Diabetes Screening Programme,” TN.GOV.IN. Partial reimbursements under CGHS and ESIC cover meters but exclude strips, sustaining recurring revenue potential for suppliers while constraining adoption among low-income groups.

Digital-Health Integration with Glucometers

BeatO’s Curv model, launched in November 2024, links USB-C dongles to an AI coach, demonstrating how connected analytics heighten adherence by turning readings into actionable insights. Remote monitoring eases pressure on India’s strained 1:1,456 doctor-patient ratio. Academic innovation, such as SRM Institute’s mini-NIR non-invasive prototype unveiled in January 2025, signals future disruption, though commercial timelines remain uncertain.

E-Pharmacy Subscription Penetration (Tier-2/3)

Digital pharmacies fill chronic-care supply gaps outside major metros. Bundled strip-and-lancet plans lower per-test costs and guarantee monthly refills, anchoring the India Self-Monitoring Blood Glucose Devices market in towns formerly underserved by brick-and-mortar chemists. Government support for telemedicine and electronic prescriptions bolsters regulatory clarity for these channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High recurring cost of consumables | −0.9% | Nationwide, acute in rural and low-income clusters | Long term (≥ 4 years) |

| Limited insurance / reimbursement coverage | −0.7% | Country-wide, especially middle- and lower-income | Medium term (2-4 years) |

| Counterfeit & grey-market strips | −0.5% | E-commerce-heavy urban pockets | Short term (≤ 2 years) |

| Data-privacy risks in app-linked devices | −0.3% | Initially tech-savvy urban users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Recurring Cost of Consumables

Monthly strip expenses often exceed the one-time meter outlay, leading to reduced testing frequency among price-sensitive users. Limited private-insurance coverage and minimal public reimbursements exacerbate the affordability gap[2]Insurance Regulatory and Development Authority, “Health Insurance Guidelines,” IRDAI.GOV.IN.

Limited Insurance / Reimbursement Coverage

Most private policies classify monitoring as preventive and exclude consumables; Ayushman Bharat covers hospitalization, not outpatient supplies[3]National Health Authority, “Ayushman Bharat Coverage,” NHA.GOV.IN. Out-of-pocket spending slows scaling of the India Self-Monitoring Blood Glucose Devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Consumables Drive Revenue Despite Device Innovation

Test strips retained 50.02% ownership of India Self-Monitoring Blood Glucose Devices market share in 2025, highlighting the consumable-centric revenue architecture. Glucometer devices, buoyed by replacement cycles and digital add-ons, are pacing at an 10.74% CAGR. Lancets and lancing devices, though smaller, follow a predictable volume trajectory. BeatO’s USB-C Curv launch exemplifies design upgrades aimed at younger, tech-friendly diabetics. SRM Institute’s non-invasive prototype, if commercialized, could compress strip demand and reshape the India Self-Monitoring Blood Glucose Devices market.

Electrochemical strips account for the bulk of manufacturing under India’s PLI scheme, trimming landed costs by 10-15% and enabling local brands to widen distribution beyond tier-1 cities.

By Technology: Electrochemical Dominance Faces Digital Disruption

Electrochemical biosensors claimed 76.10% of 2025 revenues, supported by mature supply chains and validated accuracy. Photometric platforms occupy niche institutional demand. Smartphone-integrated dongles, rising at 15.28% CAGR, capitalize on India’s 750 million internet-connected handsets. Continuous strip-free cassettes cater to users seeking lower lifetime spend but require higher upfront cash outlay. CDSCO approval processes promote safety yet elongate time-to-market for novel platforms, dictating the pace at which the India Self-Monitoring Blood Glucose Devices market absorbs next-gen formats.

By End User: Home-Care Dominance Reflects Healthcare Infrastructure Gaps

Home-care patients held 62.05% ownership of India Self-Monitoring Blood Glucose Devices market size in 2025. The preference mirrors cultural norms of family oversight and the shortage of endocrinologists in smaller cities. Government detection drives, however, are funneling newly diagnosed patients into clinical networks, giving clinics & diagnostic labs the fastest projected growth at 12.35% CAGR. Hospitals continue routine ward-based testing, but their share remains relatively stable as ambulatory monitoring shifts to homes.

By Distribution Channel: Digital Transformation Accelerates E-Pharmacy Growth

Offline pharmacies preserved 56.42% revenue share in 2025, offering immediate fulfillment and face-to-face counsel valued by seniors. Yet e-pharmacies and direct-to-consumer storefronts are rising at 16.95% CAGR, bundling monthly strip shipments with AI coaching and loyalty discounts. As logistics networks deepen, the India Self-Monitoring Blood Glucose Devices market relies increasingly on last-mile delivery to bridge rural gaps.

Geography Analysis

Variations across India hinge on income, urbanization, and state health initiatives. The north-western corridor, anchored by Delhi, Mumbai, and Pune, sets the adoption bar for connected meters thanks to higher per-capita income and stronger specialty-clinic density. Southern states trail closely: Tamil Nadu’s screening of 2.5 million citizens in 2024 spurred sharp retail demand, while Karnataka’s tech workforce favors app-paired meters. Eastern regions, led by West Bengal and Odisha, represent springboard opportunities as government schemes and e-pharmacy logistics mitigate historical supply shortages.

Tier-2 and tier-3 city penetration remains the principal upside lever. National Programme screening uncovers undiagnosed diabetics, and digital pharmacies deliver strip subscriptions to towns lacking chronic-care chemists. Nevertheless, uneven state-level enforcement of CDSCO norms creates compliance costs and rollout friction; multinationals often partner with verified local distributors to ensure regulatory conformity and customer trust.

Competitive Landscape

The India Self-Monitoring Blood Glucose Devices market features moderate fragmentation. Global entities such as Roche, Abbott, and others contend with domestic challengers including BeatO and Agatsa. Lawsuits over counterfeit strips in 2024 reinforced the premium placed on authenticity and pushed legitimate players to adopt holographic labels and app-based verification. BeatO differentiates on AI coaching, while Agatsa advances prick-less meters to attract needle-averse segments. CDSCO’s January 2025 embargo on refurbished imports sidelines gray-market products, widening lanes for Original-Design Manufacturers leveraging Production-Linked Incentives to localize strip fabrication at scale. Non-invasive prototypes from academic labs hint at future disruption, but commercialization hurdles safeguard incumbent revenues in the near term.

India Self-Monitoring Blood Glucose Devices Industry Leaders

Roche Diabetes Care

Abbott Diabetes Care

Ascensia Diabetes Care

LifeScan

Dr. Morepen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Agatsa’s EasyTouch+, India’s first smart, prickless glucose meter, cleared by CDSCO.

- November 2024: Beurer India introduced the GL 22 Blood Glucose Monitor under its ‘Make in India’ manufacturing drive.

India Self-Monitoring Blood Glucose Devices Market Report Scope

Self-monitoring of blood glucose is an approach used by diabetic patients to measure their blood sugar level themselves using a glucometer, test strips, and lancets. Based on the readings, patients can adjust or check the effect of their treatment. The India self-monitoring blood glucose device market is segmented by components. The report offers the value (in USD) and volume (in units) for the above segments.

| Glucometer Devices |

| Test Strips |

| Lancets & Lancing Devices |

| Electrochemical Biosensors |

| Photometric (Optical) |

| Continuous Strip-Free (e.g., cassette) |

| Smartphone-integrated Dongles |

| Home-care Patients |

| Hospitals |

| Clinics & Diagnostic Labs |

| Pharmacies & Wellness Stores |

| Offline Retail Pharmacies |

| Hospital-based Procurement |

| e-Pharmacies & Direct-to-Consumer |

| By Component | Glucometer Devices |

| Test Strips | |

| Lancets & Lancing Devices | |

| By Technology | Electrochemical Biosensors |

| Photometric (Optical) | |

| Continuous Strip-Free (e.g., cassette) | |

| Smartphone-integrated Dongles | |

| By End User | Home-care Patients |

| Hospitals | |

| Clinics & Diagnostic Labs | |

| Pharmacies & Wellness Stores | |

| By Distribution Channel | Offline Retail Pharmacies |

| Hospital-based Procurement | |

| e-Pharmacies & Direct-to-Consumer |

Key Questions Answered in the Report

What is the 2026 value of India self-monitoring blood glucose devices?

The market stands at USD 243.77 million in 2026, progressing toward USD 321.29 million by 2031.

How fast is demand for smartphone-integrated glucometers growing?

Devices that plug directly into phones are projected to log a 15.28% CAGR through 2031.

Which component generates the most revenue?

Test strips deliver 50.02% of 2025 revenues, reflecting the consumable-driven model.

Why are e-pharmacies important for diabetes care outside metros?

Subscription models guarantee monthly strip supply and extend reach to tier-2 and tier-3 cities lacking chronic-care pharmacies.

What regulatory move impacted refurbished device imports?

CDSCO halted refurbished medical device imports in January 2025, tightening quality controls and favoring original manufacturers.

Page last updated on: