Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

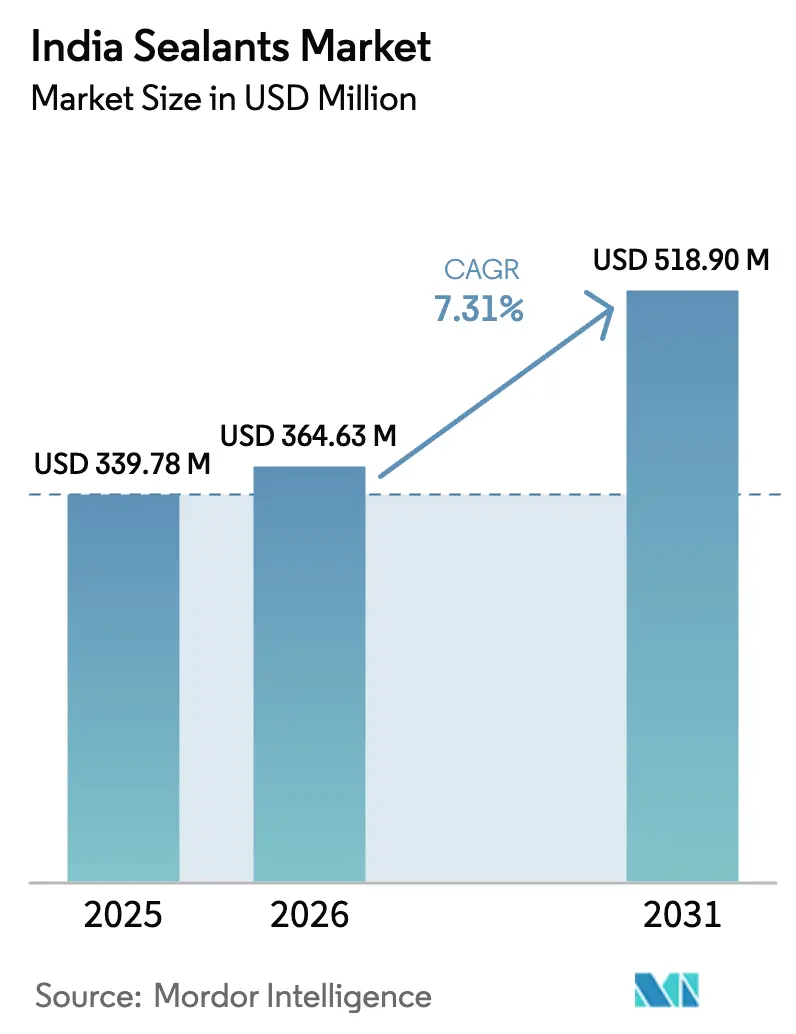

| Base Year Market Size (2025) | USD 339.78 Million |

| Market Size (2026) | USD 364.63 Million |

| Market Size (2031) | USD 518.9 Million |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

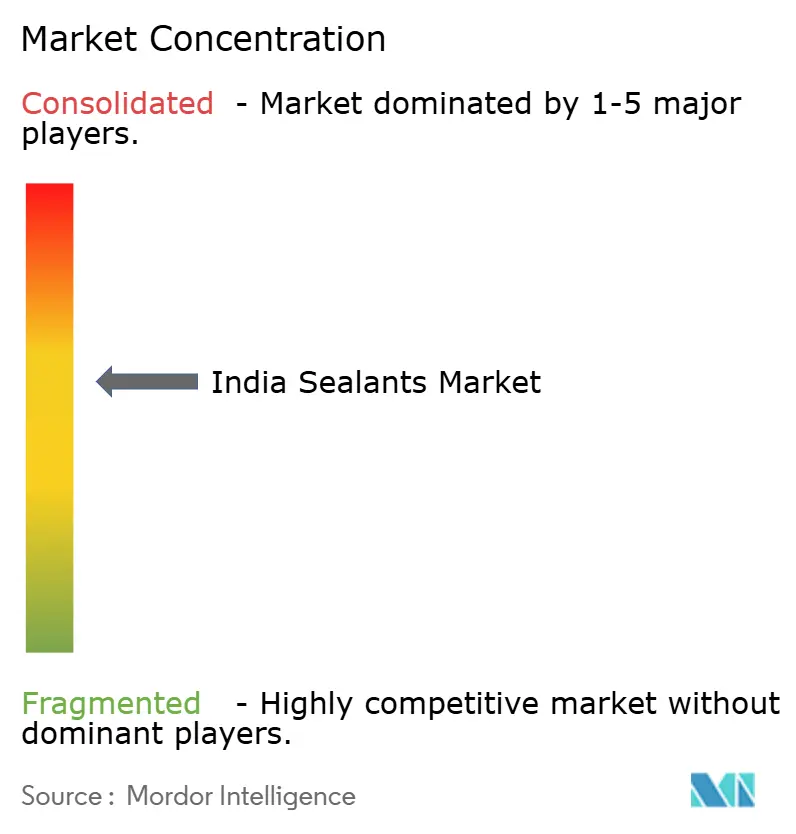

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Sealants Market Analysis by Mordor Intelligence

The India Sealants Market size was valued at USD 339.78 million in 2025 and estimated to grow from USD 364.63 million in 2026 to reach USD 518.9 million by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Robust public‐sector spending under PM Gati Shakti, tightening local-content rules for electric-vehicle (EV) battery packs, and steady healthcare facility upgrades combine to keep procurement pipelines active in metro and emerging cities. Rapid approvals through the National Master Plan reduce project lead times, pushing demand for expansion-joint, glazing, and waterproofing sealants that meet multi-modal durability standards. In parallel, the automotive industry’s pivot to localized battery-pack assembly raises specifications for thermal interface, potting, and gasket materials, advancing polyurethane and silicone uptake. Healthcare refurbishment, especially under Ayushman Bharat 2.0, is opening a premium niche for low-VOC, antimicrobial formulations able to withstand aggressive disinfectants. Feedstock price volatility and a flourishing grey market, however, continue to weigh on margins and brand positioning.

Key Report Takeaways

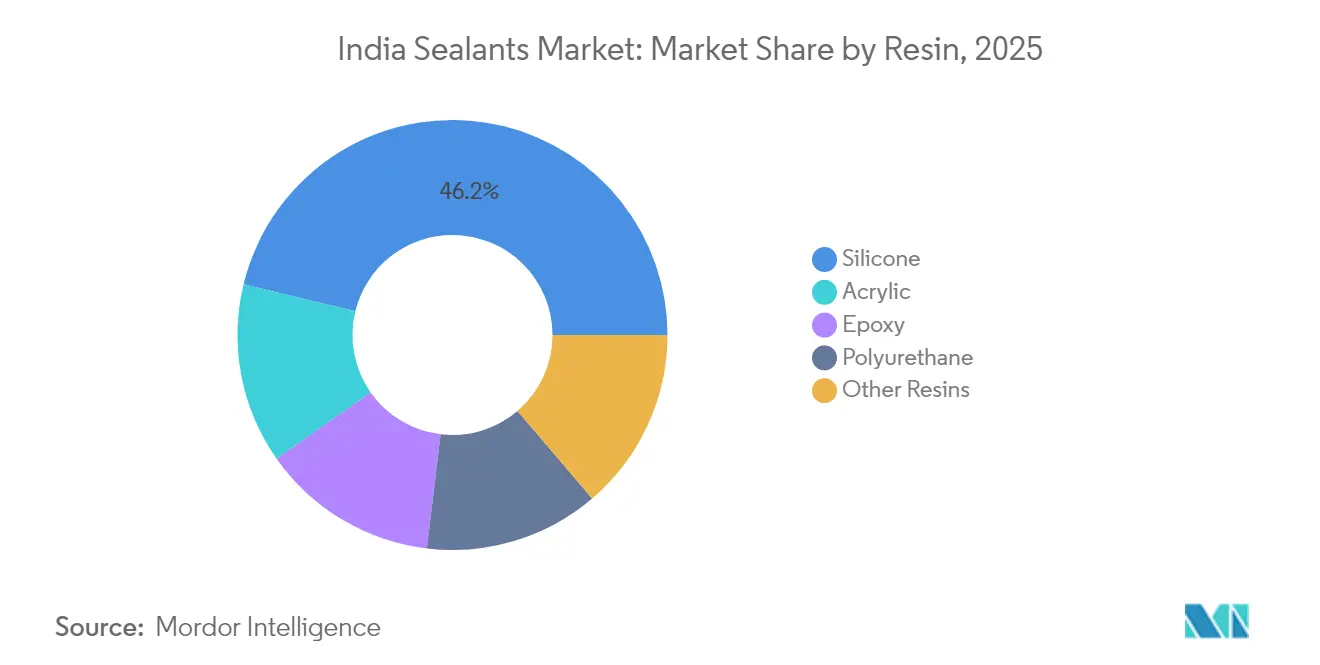

- Silicone held 46.20% of the India sealants market share in 2025 and is tracking the fastest 8.33% CAGR through 2031.

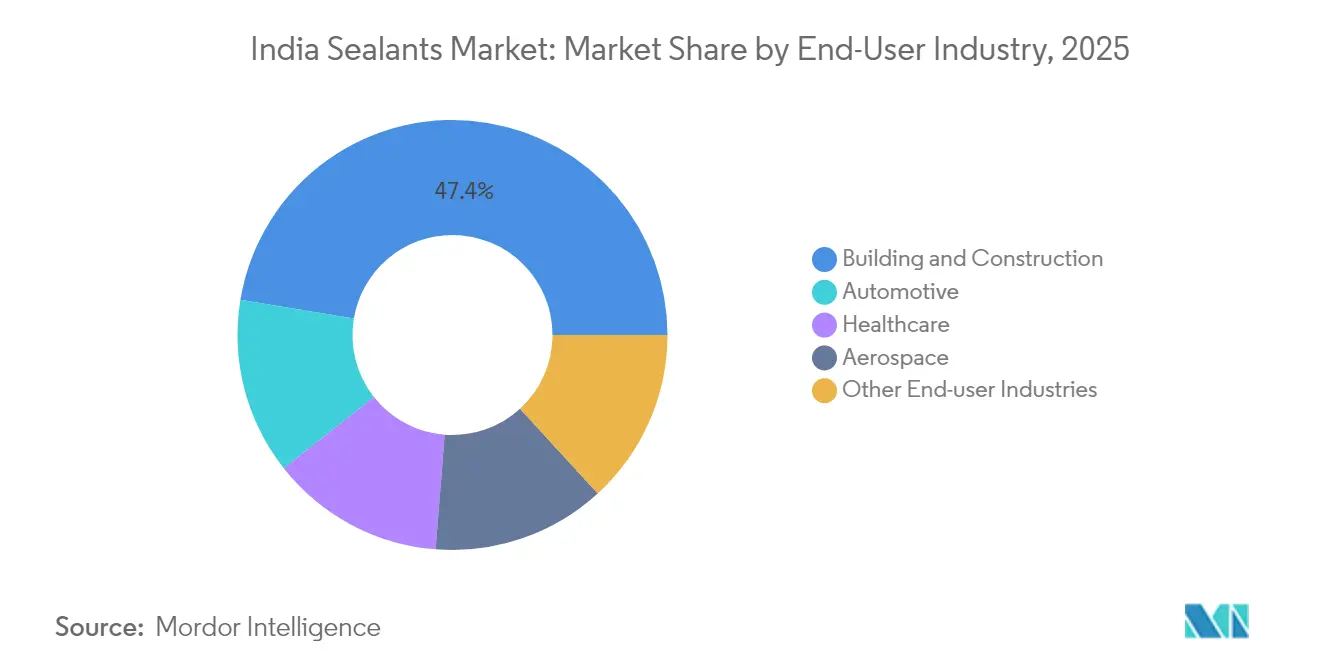

- Building and Construction accounted for a 47.38% share of the India sealants market size in 2025, while Other End-user Industries are projected to grow at a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure push via PM Gati Shakti | +2.1% | National industrial corridors, port zones | Long term (≥ 4 years) |

| Auto OEM localisation of EV battery packs | +1.8% | Maharashtra, Tamil Nadu, Gujarat automotive clusters | Medium term (2-4 years) |

| Rising healthcare facility refurbishment | +1.2% | Tier-2/3 cities nationwide | Medium term (2-4 years) |

| Tier-2/3 city mall boom | +0.9% | North and West Indian tier-2/3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PM Gati Shakti Infrastructure Acceleration Drives Multi-Modal Demand

The unified digital dashboard underpinning PM Gati Shakti now links 44 central ministries with 36 states, compressing approval cycles for rail, road, and port projects[1]IBEF, “PM Gati Shakti Yojana Boosting India’s Infrastructure Potential,” ibef.org . Sealant procurement scales alongside synchronized tender releases, covering expansion joints for expressways, structural glazing for multimodal logistics hubs, and marine-grade formulations for coastal terminals. The 2024-25 interim budget earmarked three economic railway corridors to intensify sealant demand for vibration-resistant joints and waterproofing across 96 new stations. Logistics-cost reduction targets further channel volume toward salt-spray-resilient silicone products in port modernizations. Suppliers that package application training with product supply gain an advantage because on-site quality control is now a key KPI for public procurement.

EV Battery Pack Localization Reshapes Automotive Sealant Specifications

The Ministry of Heavy Industries mandates local assembly of battery modules while allowing only cell imports, triggering a shift in specification sheets across OEMs. Gigafactory plans totaling 50 GWh under the PLI scheme require flame-retardant, low-volatile silicone potting materials capable of surviving 1,000 thermal cycles without delamination. Tier-1 suppliers already qualify dual-cure polyurethane systems that speed up line takt times by 20%. These upgrades raise average sealant value per EV by 15-20%, shifting revenue mix toward higher-margin chemistries.

Healthcare Infrastructure Expansion Creates Specialized Sealing Opportunities

Active construction of 196 hospital projects is widening the addressable base for ISO-11600-compliant, antimicrobial silicone products. Operating theaters and ICU zones demand ultra-low-VOC certifications and resistance to bleach-based cleaners, raising barriers to entry for generic acrylics. Private hospital chains are moving toward long-term maintenance contracts that bundle sealant supply with post-installation audits, opening cross-selling opportunities for premium flooring underlayments and moisture-barrier systems. Suppliers with proven compliance documentation are gaining faster vendor approvals.

Tier-2/3 City Commercial Development Expands Geographic Footprint

Malls and mixed-use complexes in cities such as Jaipur, Lucknow, and Indore have pushed curtain-wall projects outside the top-six metros, lifting near-term demand for weatherproofing silicones. Adoption rates hinge on installer capability, yet contractor shortages persist, with daily wages touching INR 1,000 in 2024. Manufacturers that invest in mobile technical teams and product sachet packs suited for smaller warehouses are capturing incremental volumes.

Restraints Impact Analysis*

| Restraints | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate and silicone feedstock prices | -1.5% | Global supply chains impacting national market | Short term (≤ 2 years) |

| GST-evaded grey market products | -0.8% | National, higher in unorganized construction segments | Medium term (2-4 years) |

| Skilled-applicator shortage in non-metro projects | -0.6% | Tier-2/3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility Pressures Margin Sustainability

Silicone spot prices have risen 5-10% in 2025 following Dow’s global hike, driven by chlor-alkali constraints and shipping bottlenecks. Indian formulators, dependent on imports for MMH and siloxane intermediates, face currency risk layered onto raw-material inflation. Some are testing epoxy-polysulfide hybrids as partial silicone substitutes, yet qualification cycles in infrastructure projects slow rapid switchovers. Anti-dumping probes on epoxies further tighten procurement windows, forcing higher inventory buffers that erode working capital.

Grey Market Competition Undermines Premium Positioning

Un-branded sealants dodging GST create a 10-15% price gap versus tax-compliant products, eroding brand equity in cost-sensitive segments. Quality lapses in these products have led to facade leaks that tarnish the entire category, compelling organized players to invest in awareness campaigns. Complex HSN classification, illustrated by the Sika block-joining mortar dispute, continues to spawn loopholes exploited by counterfeiters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Leadership Driven by Performance Requirements

Silicone accounted for 46.20% of India sealants market share in 2025, and its superior UV stability and wide service-temperature range underpin an 8.33% CAGR outlook through 2031. The segment benefits from rising structural glazing and EV-battery encapsulation projects, which command premium pricing and favor low-modulus, high-elongation products. Polyurethane remains the preferred choice for dynamic concrete joints but faces cost pressure from volatile isocyanate prices. Acrylic usage stays concentrated in interior repair and repaint cycles where price sensitivity overrides performance. Emerging bio-based and hybrid chemistries inside the “Other Resins” bucket are logging pilot-scale trials at public-sector research and development labs, targeting LEED-compliant projects.

The India sealants market size for silicone is positioned to widen its absolute lead, helped by Sika commissioning new mortar and sealant plants that shorten lead times for OEMs. Domestic research and development from Pidilite is adding water-borne grades that trim VOCs by 40%, meeting upcoming state-level indoor-air-quality norms. Such innovations also allow applicators to clean tools with water, lowering jobsite costs and attracting contractors in Tier-3 cities where solvent handling remains challenging.

By End-User Industry: Construction Dominance with Healthcare Emergence

Building and Construction generated 47.38% of India sealants market size in 2025, supported by a FY2024-25 public-capex outlay of USD 133 billion and cumulative PMAY-U housing sanctions of 1.18 crore units. The category draws volume from road overbridges, metro rails, and warehouse floors that specify joint widths exceeding 50 mm, favoring high-movement polyurethane systems. Long-term prospects remain buoyant as the National Logistics Policy targets 159 million sq ft of warehousing by 2047, demanding low-shrink, quick-tack sealants to speed slab pours.

Automotive is a significant consumer, but its growth curve steepens under FAME-III and PLI incentives that put localized battery packs and lightweight body structures on the roadmap. The India sealants market share for automotive applications will increase after 2026, when at least three gigafactories reach nameplate capacity. Other End-user Industries has emerged as the fastest-growing category, registering a 7.18% CAGR. Electronics assembly and data centers also contribute incremental demand for thermally conductive silicones and under-fill epoxies.

Geography Analysis

The western corridor, anchored by Maharashtra and Gujarat, leads India's sealants market consumption owing to its automotive clusters, petrochemical feedstock access, and ports that streamline raw-material imports. Tamil Nadu’s Chennai-Coimbatore belt follows, buoyed by EV assembly lines and textile processing units that require elastic sealants to handle humidity swings. Delhi-NCR remains a construction hot-spot as urban rail extensions and high-rise offices dominate tender schedules.

Eastern growth centers such as Kolkata are still nascent but could accelerate once the Galathea Bay trans-shipment port achieves financial closure, unlocking marine-grade sealant demand for quay walls and dredging equipment. Tier-2/3 cities represent the fastest-expanding footprint for the India sealants market, assisted by PM Gati Shakti connectivity that slashes travel time for logistics fleets. Yet labor shortages inflate project costs; 25,000-30,000 skilled applicators are estimated to be unavailable during peak months, pushing daily wages up and occasionally delaying joint-sealing schedules. Manufacturers deploying mobile training vans and e-learning modules improve adoption rates in these cities.

Competitive Landscape

Pidilite dominates with its Dr. Fixit, Fevicol, and M-Seal portfolio, backed by 68 Indian plants and a 160,000-dealer network that secures share reach. Sika, Henkel, Asian Paints, and 3M form the leading international bloc, each expanding capacity or localizing chemistries to tap advanced applications. Sika raised automotive sealant content per car in India during 2024 and activated new regional production lines. Henkel boosted its Adhesive Technologies vertical via the Seal for Life acquisition that augments corrosion-protection and pipe-coating offerings.

Asian Paints leverages its paint-putty dealer base to cross-sell tiling and waterproofing sealants, while new entrant Grasim’s Birla Opus has already recruited 50,000 dealers, instigating price resets in certain metro markets. 3M India’s 61.5% local manufacturing ratio enables quicker customization of structural acrylics for renewable-energy assembly work. Technology roadmaps across the top five players now focus on automation-ready cartridges, bio-based feedstocks, and digital twin support for facade engineers, differentiating offerings beyond mere price.

India Sealants Industry Leaders

Pidilite Industries Ltd

Sika AG

3M

Dow

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Saint-Gobain closed its USD 1.025 billion buyout of Fosroc, Inc., adding construction-chemical and sealant brands to its Indian portfolio.

- July 2024: Henkel completed Phase III of its Kurkumbh manufacturing facility near Pune, launching a new Loctite plant to support rising demand for sealants, adhesives, and surface treatment products in India.

India Sealants Market Report Scope

Aerospace, Automotive, Building and Construction, Healthcare are covered as segments by End User Industry. Acrylic, Epoxy, Polyurethane, Silicone are covered as segments by Resin.By Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Automotive |

| Aerospace |

| Healthcare |

| Other End-user Industries |

| By Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Automotive | |

| Aerospace | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms