India Quick Service Restaurant Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

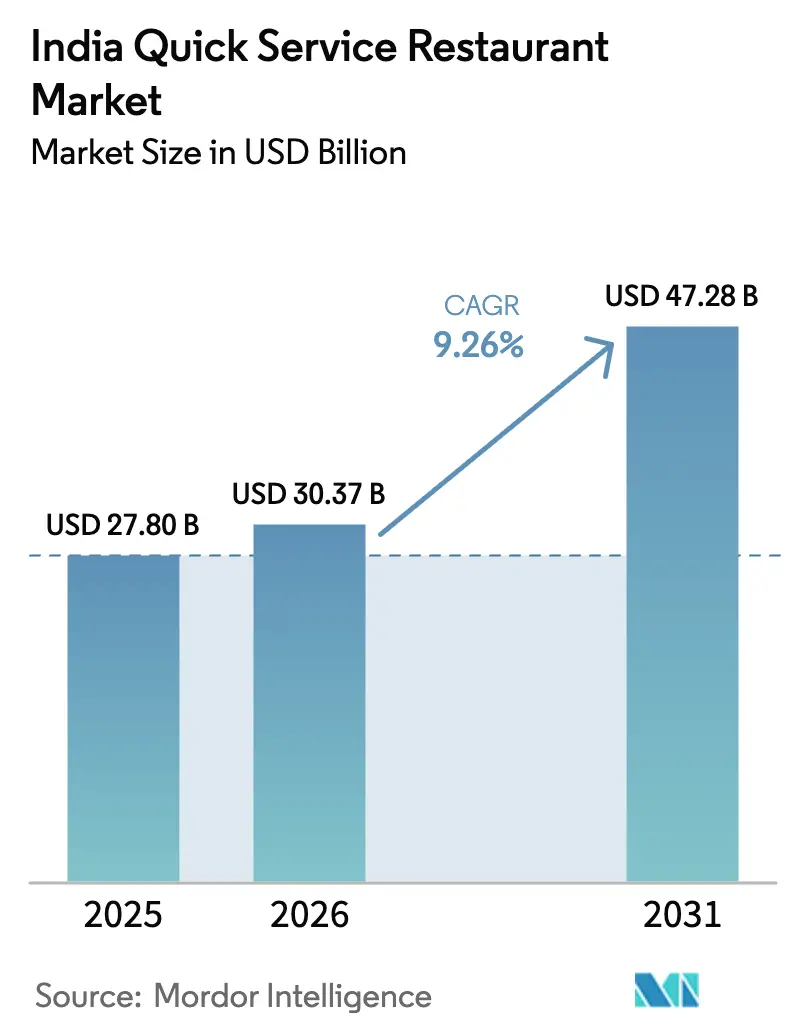

| Base Year Market Size (2025) | USD 27.80 Billion |

| Market Size (2026) | USD 30.37 Billion |

| Market Size (2031) | USD 47.28 Billion |

| Growth Rate (2026 - 2031) | 9.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Quick Service Restaurant Market Analysis by Mordor Intelligence

The India quick-service restaurant market size is expected to grow from USD 27.80 billion in 2025 to USD 30.37 billion in 2026, and is forecast to reach USD 47.28 billion by 2031, growing at a CAGR of 9.26% over 2026-2031. Structural shifts in urban eating patterns underpin this trajectory, with digital orders now driving 70% of transactions at leading pizza chains. In comparison, delivery aggregators such as Zomato recorded 30% annual order-volume growth through Q2 FY 2025. Three converging forces sustain momentum: platform economics that lower customer-acquisition costs for brands willing to share margin with aggregators, deep menu localization that lets international chains compete on taste rather than novelty, and a demographic dividend in which Generation Z, responsible for 40% of spending, equates social-media visibility with product quality. Those dynamics collectively propel same-store sales growth, justify rapid store rollouts, and expand white-space opportunities in tier-2 and tier-3 cities even as cost pressures mount.

Key Report Takeaways

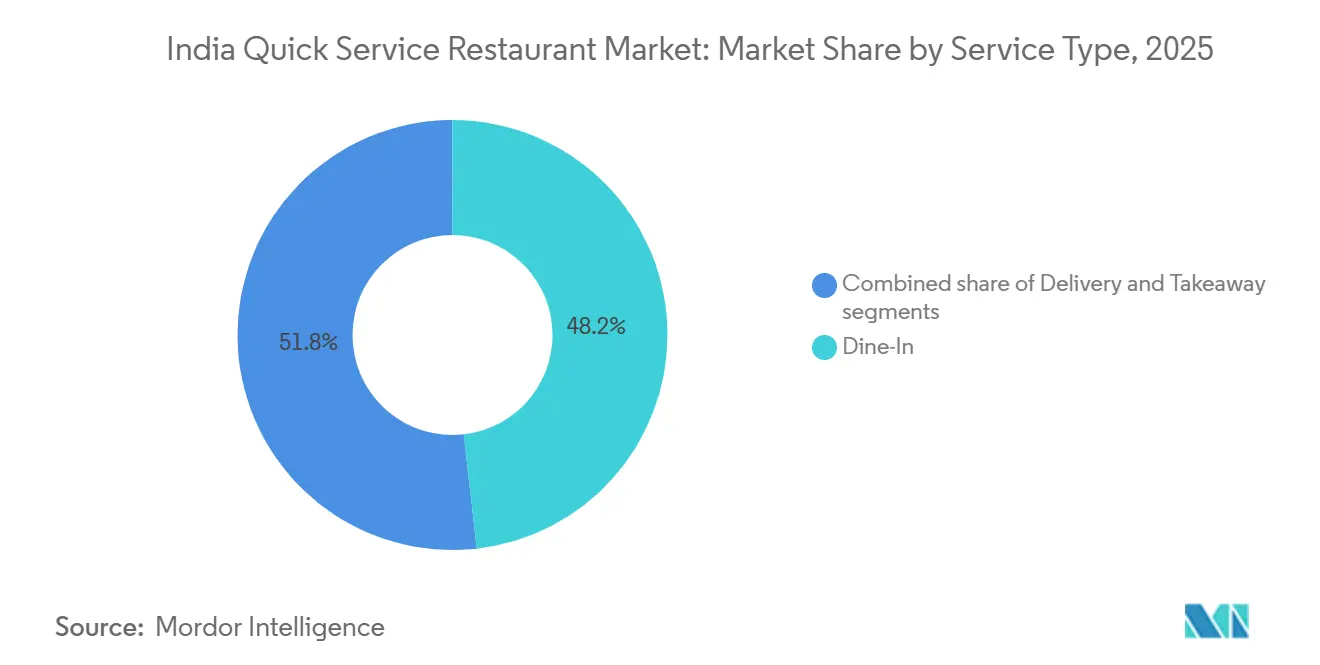

- By service type, dine-in commanded 48.21% of the Indian quick service restaurant market share in 2025, while delivery is advancing at a 10.58% CAGR through 2031.

- By cuisine, bakeries led with 25.38% revenue share in 2025, whereas pizza is projected to expand at a 11.21% CAGR to 2031.

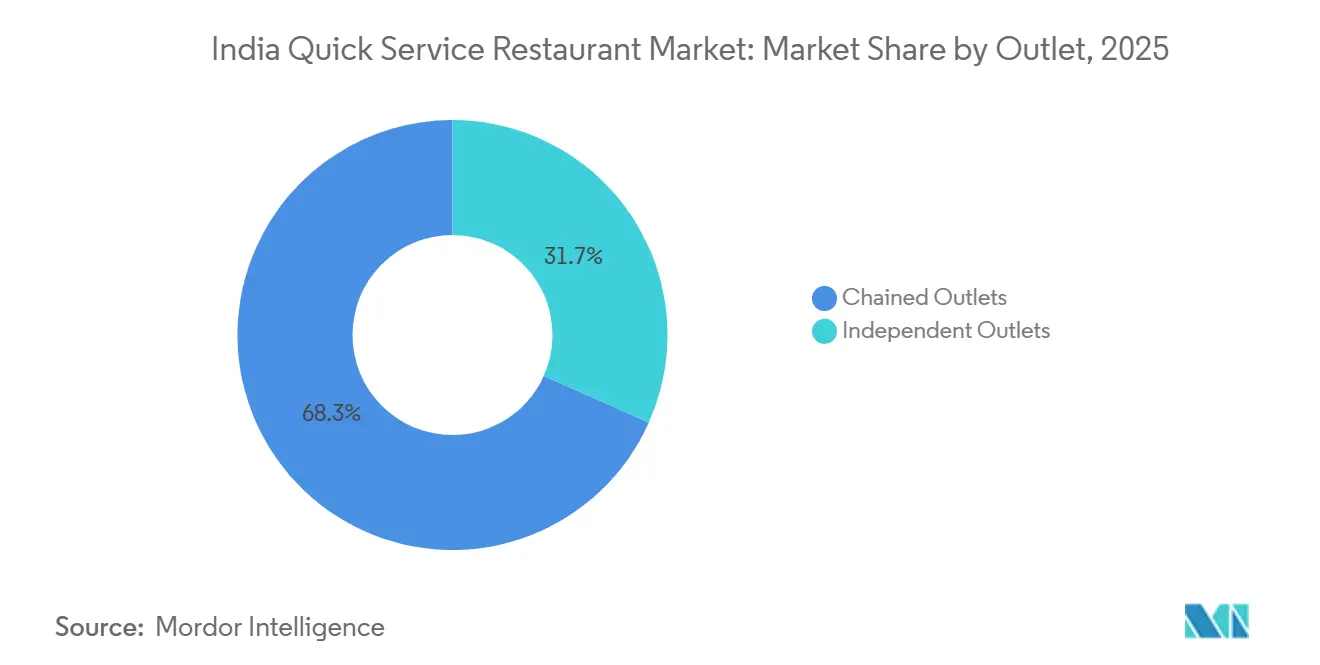

- By outlet, chained formats captured 68.32% share in 2025; independent outlets are recording the fastest growth at 10.85% CAGR.

- By location, standalone stores accounted for 72.38% of 2025 footfall, but travel hubs are forecast to rise at a 11.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Quick Service Restaurant Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Popularity of Online Food Delivery Apps and Digital Ordering Platforms | +2.1% | National, with concentration in metros and tier-1 cities | Medium term (2-4 years) |

| Evolving Consumer Preferences with Menu Localization by Brands | +1.5% | National, strongest in North and West India | Long term (≥ 4 years) |

| Rising Youth Population and Influence of Social Media | +1.8% | National, skewed toward urban centers | Long term (≥ 4 years) |

| Greater Exposure to Global Cuisines and Western Eating Habits | +1.3% | Metros and tier-1 cities, spillover to tier-2 | Medium term (2-4 years) |

| Strategic Alliances between QSRs and Delivery Aggregators | +1.2% | National, delivery-dense markets | Short term (≤ 2 years) |

| Expansion of Cafe Culture and Snacking Trends | +1.0% | Urban India, mall corridors, office districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Popularity of Online Food Delivery Apps and Digital Ordering Platforms

The increasing adoption of online food delivery apps and digital ordering platforms is driving the growth of the quick service restaurant (QSR) market in India. As of March 2024, the India Brand Equity Foundation reported that India had 954.40 million internet subscribers, significantly expanding the reach of platforms like Zomato and Swiggy[1]Source: India Brand Equity Foundation, "India's Internet Users to Exceed 900 Million in 2025, Driven By Indic Languages", ibef.org. These platforms process billions of orders annually, contributing to a delivery growth rate of approximately 30%. This trend highlights that QSR operators are renting demand rather than building it, which accelerates store-count expansion but links long-term profitability to commission agreements. Jubilant FoodWorks reported that 70% of Domino's orders in the second quarter of fiscal 2025 originated from digital channels. The company is also piloting AI-driven upsell prompts, which have increased average order values by 12%. Meanwhile, smaller chains face a challenge: aggregator visibility is crucial for discovery, but shrinking margins force them to streamline menus and cut labor costs, often at the expense of differentiation.

Evolving Consumer Preferences with Menu Localization by Brands

International QSR chains have transitioned from offering basic vegetarian options to developing products tailored to regional taste preferences. This strategic shift leverages latent demand in markets where flavor intensity and spice levels influence repeat purchases. In 2024, McDonald's India launched the McSpicy Paneer Burger and Masala McEgg. KFC introduced the Hyderabadi Biryani Bucket in southern states, while Domino's tested a Chettinad Paneer Pizza in Tamil Nadu. These localized offerings achieved an 8-10 percent increase in same-store sales within their pilot regions. Burger King has customized 60 percent of its menu for India, featuring items like the Tandoori Grill Veg and Chicken Makhani Burst. The chain reported that these localized SKUs deliver gross margins 40 percent higher than imported recipes. This is primarily due to replacing expensive cheese and beef with paneer and chicken, which are 30-40 percent cheaper. However, localization extends beyond menu adjustments. It involves supply chain reconfiguration, vendor certification for region-specific spices, and kitchen equipment modifications to handle the higher moisture content in Indian gravies.

Rising Youth Population and Influence of Social Media

A 2024 study by the Indian Institute of Management Bangalore found that 68 percent of Gen Z respondents discovered new QSR outlets through social-media posts, and 54 percent made purchase decisions within 24 hours of seeing a trending food video, compressing the consideration cycle from weeks to hours. This dynamic rewards brands that engineer "Instagrammable" products, oversized milkshakes, rainbow-colored desserts, and theatrical presentations, even when taste profiles remain conventional. According to the StatCounter Global Stats data from 2025, 40.17% of people in India used Instagram[2]. Starbucks India capitalized on this trend by launching limited-edition beverages tied to Bollywood releases, generating 2.5 million social-media impressions per campaign and driving a 15 percent uptick in store traffic during promotional windows. The strategic risk is that social-media-driven demand is fickle; brands must continuously refresh visual cues to maintain relevance, which inflates product-development costs and shortens SKU lifecycles. Regional chains such as Wow! Momo has embraced this model, releasing monthly limited-edition momos and leveraging micro-influencers in tier-2 cities to sustain buzz at a fraction of the cost incurred by multinational competitors

Greater Exposure to Global Cuisines and Western Eating Habits

Urban Indians are adopting global cuisines at an accelerating pace, with Korean food orders growing 17-fold, Vietnamese 6-fold, and Mexican 3.7-fold between 2020 and 2024, according to aggregator data compiled by Zomato. This diversification reflects rising disposable incomes; India's per-capita GDP crossed USD 2,700 in 2025, and increased international travel, which exposed 12 million Indians to foreign culinary traditions in 2024 alone. QSR chains are responding by hybridizing formats: Taco Bell introduced a Paneer Tikka Taco, and Subway launched a Tandoori Chicken Sub, each blending Western form factors with Indian flavor systems to reduce adoption friction. The strategic insight is that global cuisines succeed not by replicating authenticity but by offering novelty within a familiar taste envelope, allowing brands to charge a 20-30% premium over traditional offerings without alienating core customers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Rental and Real Estate Expenses | -1.4% | Metros and tier-1 cities, high-street locations | Short term (≤ 2 years) |

| Surging Raw Material and Commodity Inflation | -1.6% | National, acute in regions dependent on imports | Short term (≤ 2 years) |

| Rigorous Food Safety, Licensing, and Regulatory Standards | -0.8% | National, stricter enforcement in metros | Medium term (2-4 years) |

| Fierce Rivalry from Delivery-Only Cloud Kitchens | -1.2% | Urban India, delivery-dense markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Rental and Real Estate Expenses

From 2024 to 2025, commercial rental rates in prime urban corridors increased by 15-20 percent. High-street locations such as Mumbai's Bandra-Kurla Complex and Delhi's Connaught Place now demand monthly rents exceeding INR 500 per square foot (USD 6 per square foot), which is twice the rates in tier-2 cities. This rise in rents is primarily attributed to limited supply. India added only 12 million square feet of Grade A retail space in 2024, meeting just half of the demand growth, and landlords are favoring stable, long-term tenants. This trend creates challenges for QSR operators who typically require flexible lease terms. The financial impact is significant for chains targeting store-level EBITDA margins of 20-25%. For example, a 15 percent rent increase could reduce margins by 300 basis points unless mitigated by higher sales or price increases, both of which are constrained by demand elasticity. Westlife Foodworld reported that rental expenses accounted for 12% of its revenue in fiscal 2025, up from 10% in fiscal 2023. In response, the company shifted 40% of its new openings to food courts and non-traditional venues, such as airports, hospitals, and universities, where landlords prefer revenue-sharing models over fixed rents.

Surging Raw Material and Commodity Inflation

During 2024-2025, food input costs experienced significant volatility. In July-August 2024, unseasonal rains in Karnataka and Maharashtra drove tomato prices up by 400%. Wheat prices increased by 8% year-on-year due to export restrictions, while chicken prices fluctuated by 25% quarter-to-quarter as avian influenza outbreaks disrupted supply chains. Dairy prices saw a steady 6% annual inflation, and edible oil prices rose by 10%, primarily because India remained a net importer of palm and soybean oil, according to the Reserve Bank of India. These price fluctuations created challenges for Quick Service Restaurant (QSR) operators. While input costs reset monthly, brands typically adjust menu prices only twice a year to avoid losing customers. Jubilant FoodWorks reported an increase in raw-material expenses from 28% of revenue in fiscal 2023 to 31% in fiscal 2025, resulting in a 300 basis point decline in gross margins. Chains like McDonald's, which use centralized procurement and secure long-term contracts to lock in wheat and potato prices six months in advance, managed these price swings more effectively than regional players who rely on spot purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Delivery Gains Share Despite Dine-In Dominance

In 2025, dine-in services accounted for 48.21% of the market share, highlighting a steady consumer preference for experiential dining. This trend is particularly evident among families and social groups who value ambiance, attentive table service, and the tradition of dining out. Meanwhile, the delivery segment is experiencing significant growth, with a 10.58% CAGR, fueled by urban consumers seeking convenience amid time constraints. Takeaway services occupy a middle ground, appealing to office workers and students who prioritize speed and aim to avoid delivery fees. Delivery services are primarily thriving in metropolitan and tier-1 cities, where dual-income households and long commutes enhance the appeal of home delivery. Conversely, dine-in services maintain their strength in tier-2 and tier-3 cities, where QSR visits are social occasions, and delivery infrastructure remains underdeveloped. Jubilant FoodWorks reported that delivery constituted 70% of Domino's orders in the second quarter of fiscal 2025.

To counter competition from cloud kitchens, the company is piloting 15-minute delivery guarantees in select areas. However, takeaway services face challenges from both ends. Delivery aggregators offer discounts that erode the cost advantage of self-pickup, while dine-in formats improve their ambiance to justify the time investment. As a result, takeaway services primarily cater to price-sensitive customers and those placing orders while on the move. The strategic focus for QSR chains is clear: they must optimize omnichannel fulfillment by designing kitchens capable of handling dine-in, takeaway, and delivery orders simultaneously. While delivery is expected to drive incremental growth, QSR chains must also address the pressure it places on unit economics.

By Cuisine: Bakeries Lead, Pizza Accelerates on Value Innovation

In 2025, bakeries accounted for 25.38% of the market share, driven by the rise of café culture, increased snacking occasions, and the premiumization of baked goods. Pizza, on the other hand, was the fastest-growing cuisine, achieving an impressive 11.21% CAGR due to aggressive store expansions, value-meal bundling, and menu localization. Burger chains, supported by the strong brand equity of McDonald's and Burger King, ranked third, although their growth has slowed as the market matures. Ice cream parlors, benefiting from discretionary spending and seasonal demand, experienced steady but modest growth. Meat-based cuisines, particularly chicken-focused formats like KFC, gained traction in non-vegetarian-dominant states but faced challenges in vegetarian-majority regions. Other quick-service restaurant (QSR) cuisines, such as momos, dosas, and regional snacks, represent a fragmented yet rapidly growing segment as regional brands expand beyond their home markets.

Bakeries' market dominance stems from structural advantages: baked goods deliver gross margins of 40-50%, significantly higher than those of savory items. Additionally, baked goods cater to all-day consumption occasions, including breakfast, mid-morning snacks, afternoon tea, and evening desserts. Chains like Theobroma and Monginis expanded into tier-2 cities during 2024-2025, collectively opening 150 outlets. They introduced premium cakes priced between USD 9.60-14.40, targeting gifting occasions and celebrations. Pizza's growth has been fueled by strategic value engineering: Domino's launched "Everyday Value" meals priced at USD 1.19, bundling a personal pizza with a beverage. This initiative increased transaction frequency by 18% among price-sensitive customers while maintaining contribution margins through beverage upsells. Burger chains are encountering saturation in metropolitan areas. McDonald's and Burger King, with a combined 800 outlets in the top 10 cities, are now focusing on tier-2 markets, where brand novelty drives initial trials, though repeat visits remain below metro benchmarks.

By Outlet: Chains Scale, Independents Exploit Hyperlocal Niches

In 2025, chained outlets accounted for 68.32% of the market share, highlighting their franchise scalability, brand reliability, and access to capital. However, independent outlets are growing at a notable 10.85% CAGR. These regional players effectively cater to hyperlocal taste preferences, benefit from reduced overheads, and demonstrate flexibility in menu adjustments. Chains capitalize on centralized procurement, standardized operations, and nationwide marketing campaigns, advantages that independents cannot match. Meanwhile, independents differentiate themselves through authenticity, personalized service, and the ability to modify recipes and pricing in real time. The competitive landscape is diverging: chains dominate metros and tier-1 cities, where consumers prioritize consistency and hygiene, while independents maintain a stronghold in tier-2 and tier-3 cities, relying on local reputation and word-of-mouth over brand equity.

Chained outlets are driving market-share growth through franchise models that distribute capital risks and accelerate geographic expansion. For example, Jubilant FoodWorks operates 1,900 stores across brands like Domino's and Dunkin', with 80% of these stores franchised. In fiscal 2025, the company added 200 outlets, focusing on tier-2 cities where real estate costs are 40% lower than in metros. Similarly, Westlife Foodworld, which follows a company-owned model for McDonald's, opened 50 stores in fiscal 2025. The company also invested in technology, such as self-order kiosks, mobile ordering, and kitchen automation, which collectively reduce labor costs by 15% and enhance order accuracy. On the other hand, independent outlets face structural challenges, including limited access to institutional capital, fragmented supply chains, and exposure to regulatory audits. However, they mitigate these disadvantages through niche positioning: Goli Vada Pav targets the INR 30-50 (USD 0.36-0.60) price range with street-food-inspired offerings, Saravana Bhavan leads in South Indian vegetarian dining, and Bikanervala commands premium pricing for traditional sweets and snacks.

By Location: Standalone Sites Dominate, Travel Hubs Surge

In 2025, standalone locations accounted for a significant 72.38% share of the market, highlighting QSR operators' preference for high-visibility sites with dedicated parking and drive-through access. However, travel hubs, airports, and railway stations emerged as the fastest-growing segment, recording a strong 11.25% CAGR. These locations benefit from captive audiences, a willingness to pay premium prices, and extended operating hours. Retail locations, primarily mall-based outlets, attract foot traffic and offer co-marketing opportunities but face challenges such as high rental costs and restricted operating hours. Lodging venues, including hotel food courts and in-room delivery services, cater to business travelers and tourists. While they generate additional revenue, revenue-sharing agreements often reduce profit margins. Leisure venues, such as amusement parks and entertainment complexes, provide experiential benefits but are impacted by seasonal demand fluctuations.

The success of standalone sites is driven by their operational flexibility. Brands maintain control over site selection, lease terms, and store design, while capturing 100% of customer spending without revenue-sharing. Devyani International capitalized on this trend by focusing on standalone KFC and Pizza Hut outlets in tier-2 cities. In fiscal 2025, the company opened 80 stores, achieving same-store sales 20% higher than mall-based locations[2]Source: Devyani International Investor Presentation 2025, devyani.com. This performance is attributed to the drive-through facilities and extended hours offered by standalone sites. The rapid growth of travel hubs is fueled by significant infrastructure investments. Between 2020 and 2025, India inaugurated 25 new airports. Additionally, the Airports Authority of India required that 30% of concession space at these airports be allocated to food and beverage outlets, creating 500 new QSR opportunities[3]Source: Airports Authority of India "Airports Authority of India Mandates 30% Concession Space for food and beverages", aai.aero. Leading brands such as Starbucks, McDonald's, and Burger King secured multi-year concessions at major airports in Delhi, Mumbai, and Bangalore. In exchange for 12-15% revenue-sharing fees, these brands gained access to 200 million annual passengers, who spend 40% more on average than street-level customers. Railway stations are following a similar trend.

Geography Analysis

India's QSR market showcases distinct regional dynamics. While metros and tier 1 cities are projected to contribute 65 percent of the revenue in 2025, it is the tier 2 and tier 3 cities that are set to drive 75 percent of the incremental growth as chains look beyond their saturated urban hubs. The northern and western regions, including Delhi NCR, Mumbai, Pune, and Ahmedabad, dominate the market share, buoyed by higher disposable incomes, diverse food preferences, and robust delivery infrastructures. Meanwhile, southern states like Karnataka, Tamil Nadu, and Telangana are witnessing rapid expansion, fueled by a booming IT sector and a youthful demographic. Eastern and northeastern states, though underpenetrated due to lower per capita incomes and fragmented supply chains, are seeing brands like Kolkata's Wow! Momo capitalizes on regional insights to carve out significant market positions.

Tier 2 cities such as Coimbatore, Indore, Jaipur, Lucknow, and Visakhapatnam are emerging as the focal points for the next growth surge. Jubilant FoodWorks revealed that in fiscal 2025, 60 percent of new Domino's outlets were launched in tier 2 and tier 3 cities. Here, same-store sales growth hit 12 percent, outpacing the 6 percent growth in metros. To optimize capital, the company is experimenting with smaller format stores featuring limited seating and kitchens tailored for delivery. Westlife Foodworld mirrored this approach, inaugurating 30 out of 50 new McDonald's in tier 2 locales. They have also rolled out regional specialties like the Masala Grill Veg in Gujarat and Chicken Chettinad in Tamil Nadu, boasting 15 percent higher trial rates than their standard menu. Regional players are capitalizing on their foothold. Haldiram's boasts 200 outlets in North India, Bikanervala enjoys a premium status in Delhi and Jaipur, and Saravana Bhavan leads the South Indian vegetarian scene with 100 outlets in Tamil Nadu and Karnataka.

State-by-state regulatory landscapes differ, with Maharashtra and Karnataka imposing stringent FSSAI compliance, unlike Uttar Pradesh and Bihar, where enforcement is sporadic. This inconsistency complicates operations for national chains, necessitating adherence to diverse compliance protocols. Such fragmentation poses a challenge for smaller independents, who often lack the means to navigate these multi-state regulations. The takeaway? Expanding geographically demands not just capital and brand strength, but also a keen understanding of regulations and local alliances. This reality tends to benefit chains with robust government relations, overshadowing pure play startups.

Competitive Landscape

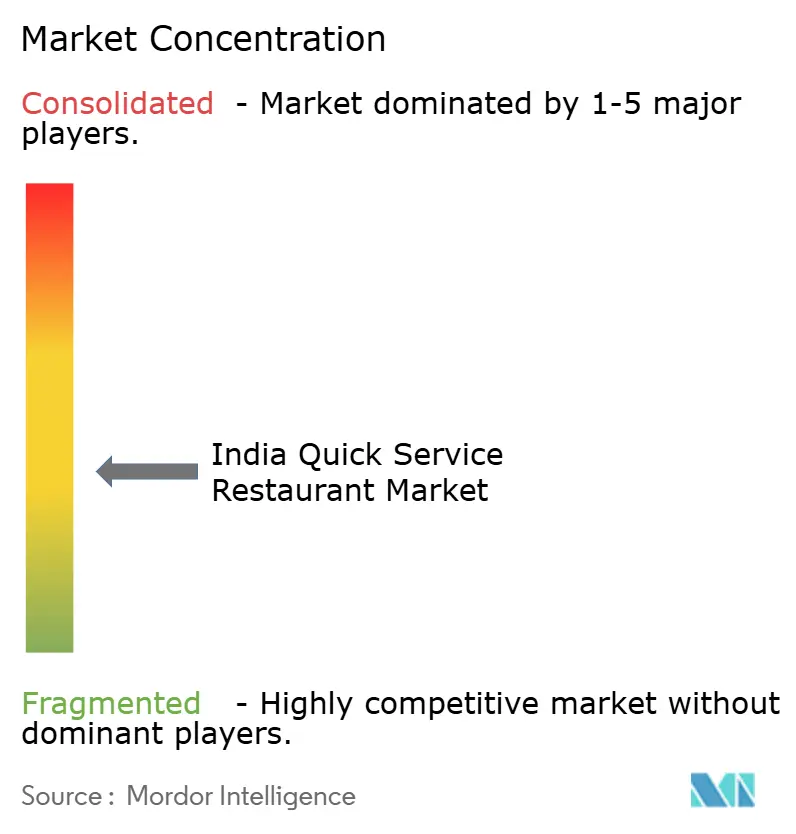

In India, the QSR market boasts a concentration score of 7 out of 10. This score highlights a core dominated by multinational franchisees, namely Jubilant FoodWorks, Westlife Foodworld, Devyani International, and Restaurant Brands Asia, while the periphery remains fragmented, featuring regional specialists and delivery-only disruptors. The top five players hold a combined market share of roughly 45%. In contrast, the remaining 55% is spread across over 5,000 independent outlets and emerging chains. This creates a competitive landscape where scale advantages meet hyperlocal differentiation. Strategic maneuvers in the market revolve around three main axes: accelerating franchises to spread capital risk and hasten store rollouts, adopting technology to cut labor costs and enhance order accuracy, and localizing menus to shift perceptions from foreign to a focus on taste.

There is a burgeoning opportunity in tier 2 and tier 3 cities, where brand penetration lingers below 30%. Additionally, nontraditional venues like travel hubs, corporate campuses, and coworking spaces present lucrative prospects, given their captive audiences and willingness to bear premium prices. Disruptors are emerging with asset-light models, taking on established players. For instance, Rebel Foods, with its 450 cloud kitchens spread across 75 cities, is on track to hit an annualized revenue of USD 200 million by mid 2025. Their unit economics enable them to offer menu prices 15 to 20 percent lower than conventional QSRs. In a notable move, the company secured 12 patents in 2024, focusing on kitchen automation, order routing, and predictive demand forecasting. This underscores their transition from mere operational execution to carving out a technology-led competitive edge. Meanwhile, regional chains are finding success through franchise collaborations. Take Wow! Momo, which inaugurated 100 stores in fiscal 2025, with a notable 70 percent being franchised. They are also testing the waters with a Wow! China brand, aiming to diversify and tap into the demand for Chinese cuisine.

Technology is becoming a cornerstone across the industry. Jubilant FoodWorks, for instance, poured INR 500 crore (USD 60 million) into digital infrastructure in fiscal 2025. Their AI-driven demand forecasting slashed food waste by 18%, while dynamic pricing algorithms boosted average order values by 12%. This shift underscores a pivotal change: competitive advantage is moving from traditional metrics like brand equity and real estate access to modern tools like data analytics, supply chain finesse, and rapid menu iterations. Operators recognizing QSR as a tech-driven business intertwined with food, stand to gain.

India Quick Service Restaurant Industry Leaders

-

Jubilant FoodWorks Ltd

-

McDonald’s Corp. (Westlife Foodworld)

-

Restaurant Brands Asia Ltd

-

Eversub India Pvt. Limited (Subway)

-

Yum! Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: EBG Group announced its ambitious plans to expand its flagship food and beverage brand, Natuf Cafe. The group aims to establish over 100 outlets across India by the end of 2026. This expansion strategy reflected EBG Group’s vision to position Natuf Cafe as one of the fastest-growing quick service restaurant (QSR) chains in the country, capitalizing on the increasing consumer demand for healthy, premium, and sustainable dining options.

- August 2025: The Burger Company introduced TBC PICO, a micro-QSR franchise model designed to lower the barriers to entry for aspiring food entrepreneurs. This innovative format requires an all-inclusive investment of INR 7.89 lakhs plus taxes and operates within a compact space of just 80-100 sq ft.

- July 2025: Burger Singh introduced an owner-partner franchise model aimed at empowering entrepreneurs to establish fully operational dine-in restaurants. This strategic initiative was designed to drive the brand's expansion into a diverse range of locations.

- March 2025: Swiggy entered into a partnership with Domino’s to enhance its quick service offerings, strengthening Swiggy’s position in the competitive food delivery market by providing customers with greater access to Domino’s extensive menu.

India Quick Service Restaurant Market Report Scope

Dine-In, Delivery, Takeaway are covered as segments by Service Type. Bakeries, Burger, Ice Cream, Meat-Based Cuisines, Pizza and Other QSR Cuisines are covered as segments by Cuisine. Chained Outlets and Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, and Travel are covered as segments by Location.

| Dine-In |

| Takeaway |

| Delivery |

| Bakeries |

| Burger |

| Ice Cream |

| Meat-Based Cuisines |

| Pizza |

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| By Service Type | Dine-In |

| Takeaway | |

| Delivery | |

| By Cuisine | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-Based Cuisines | |

| Pizza | |

| Other QSR Cuisines | |

| By Outlet | Chained Outlets |

| Independent Outlets | |

| By Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms