Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

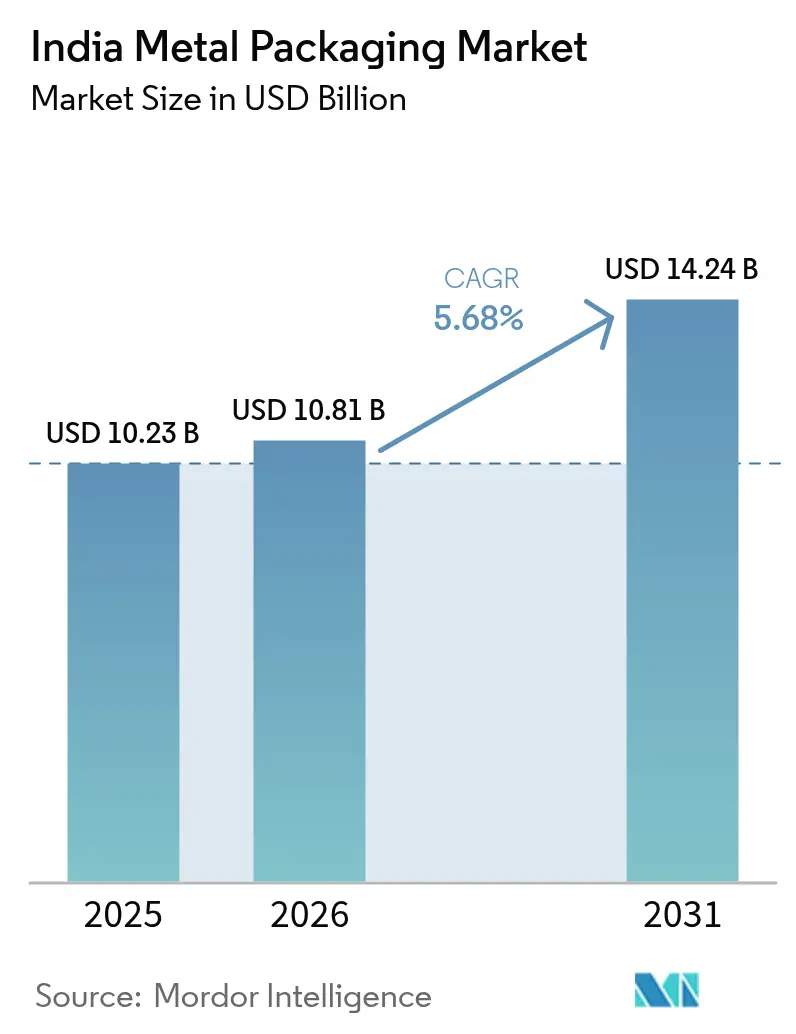

| Base Year Market Size (2025) | USD 10.23 Billion |

| Market Size (2026) | USD 10.81 Billion |

| Market Size (2031) | USD 14.24 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Metal Packaging Market Analysis by Mordor Intelligence

The India metal packaging market size is expected to grow from USD 10.23 billion in 2025 to USD 10.81 billion in 2026 and is forecast to reach USD 14.24 billion by 2031 at 5.68% CAGR over 2026-2031. Expanding cold-chain logistics, higher beverage consumption, and stricter Extended Producer Responsibility (EPR) rules are steering demand toward infinitely recyclable metal containers. Aluminium’s light weight and recycling efficiency give the material a cost-of-ownership edge while new BIS quality control orders raise the technical bar for tinplate and steel inputs. Brand owners are switching from single-use plastics to metal to avoid EPR penalties, and two-piece aluminium can technology is spreading across soda, craft beer, and energy-drink lines. Meanwhile, investments in downstream aluminium processing are easing supply constraints and lowering lead times for converters. Raw-material price volatility remains a margin risk, but hedging programs and long-term contracts are helping large converters stabilize input costs.

Key Report Takeaways

- By material type, aluminium led with a 62.24% revenue share in 2025, and steel is projected to grow at a 7.32% CAGR through 2031.

- By product type, cans accounted for 41.02% share in 2025, while bulk containers are forecast to expand at an 7.65% CAGR to 2031.

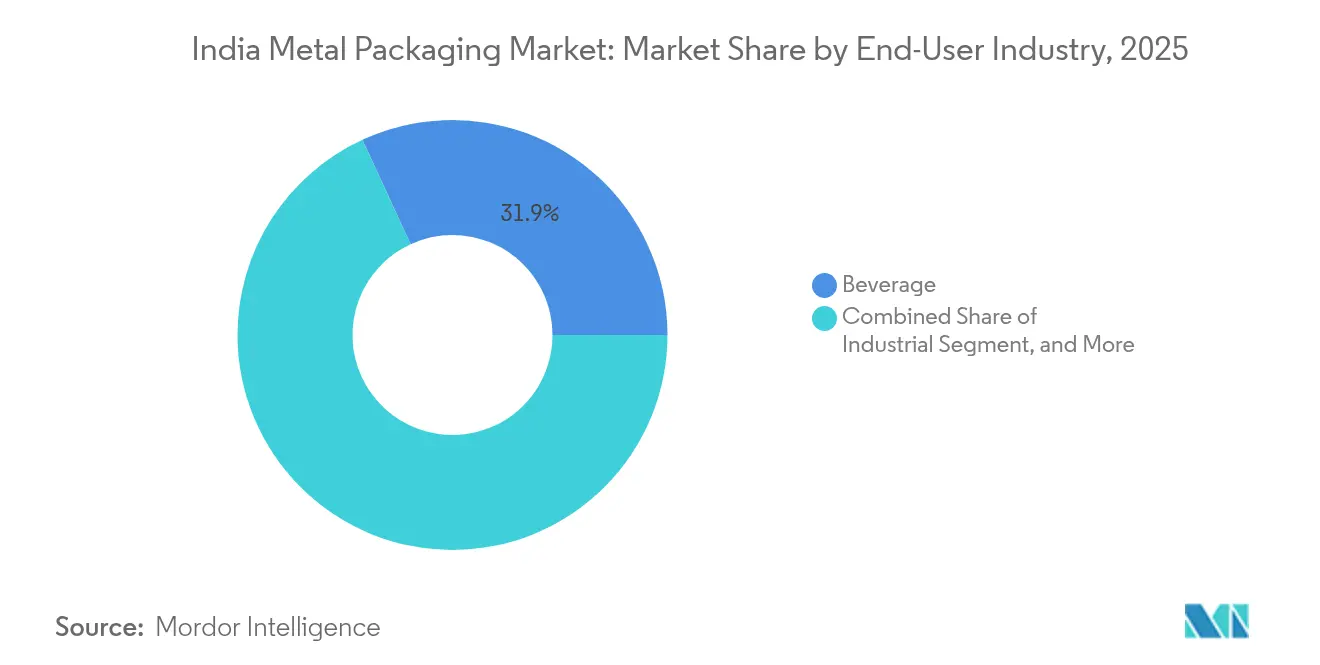

- By end-user industry, beverages held 31.88% of the India metal packaging market share in 2025, whereas industrial applications are set to climb at a 7.45% CAGR through 2031.

- By coating type, epoxy phenolic dominated with 38.12% share in 2025, and BPA-free alternatives are predicted to increase at a 6.93% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High recyclability rates of metal packaging | +1.2% | National, higher impact in urban centers | Long term (≥ 4 years) |

| Rising demand from ready-to-drink beverage brands | +1.8% | National, concentrated in metro cities | Medium term (2-4 years) |

| Government push for Extended Producer Responsibility | +1.5% | National implementation with state variations | Short term (≤ 2 years) |

| Rapid growth of India’s craft beer and energy-drink segments | +0.9% | Urban and Tier-2 cities | Medium term (2-4 years) |

| Expansion of cold-chain logistics for processed foods | +1.1% | National, focused on agricultural states | Long term (≥ 4 years) |

| Investments in lightweight two-piece aluminium can lines | +0.8% | Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Recyclability Rates of Metal Packaging

Metal’s infinite recycling loop aligns with EPR policy targets that are tightening collection and traceability rules. Aluminium can recycling saves 95% of the energy used in primary smelting, and steel’s magnetic properties allow efficient recovery in municipal facilities[1]Aluminium Association of India, “Sustainability Report on Metal Packaging Recyclability,” AAI.IN. BIS specification IS 15410:2024 now mandates minimum recycled content, creating a stable end-market for secondary metal, while the National Action Plan on Climate Change seeks a 40% cut in emission intensity by 2030. Consumer education campaigns led by the Central Pollution Control Board emphasize metal’s lower life-cycle footprint, prompting large beverage brands to shift SKU mixes toward recyclable cans. Together, these factors add long-run momentum to the India metal packaging market.

Rising Demand from Ready-to-Drink Beverage Brands

Legalization of alcoholic RTDs in multiple states during 2024 and a 23% surge in energy-drink sales have expanded use of two-piece aluminium cans that protect flavor and carbonation across India’s hot climate zones. Coca-Cola’s new lightweight can line in Sanand and Red Bull’s distribution push illustrate the premiumization trend that favors metal over glass or plastic. The Food Safety and Standards Authority of India has tightened barrier-performance requirements for carbonated drinks, indirectly steering packaging decisions toward metal. For converters, the RTD boom supplies volume certainty that underwrites capital spending on high-speed can lines, reinforcing growth in the India metal packaging market.

Government Push for Extended Producer Responsibility

The 2024 amendment to the Plastic Waste Management Rules widened EPR coverage to include metal, obliging producers to demonstrate end-of-life management via a centralized CPCB portal linked to GST data. Maharashtra and Tamil Nadu impose penalties of INR 50,000 (USD 567.7 million ) million for non-compliance, prompting FMCG and beverage companies to redesign packs around materials with established recycling streams. Because scrap dealers and re-rollers already collect aluminium and steel at scale, metal formats let brand owners hit EPR targets at lower administrative cost than multilayer plastics. This compliance premium is accelerating demand across beverages, processed foods, and industrial lubricants and is adding 1.5 percentage points to the market’s CAGR.

Rapid Growth of India’s Craft Beer and Energy-Drink Segments

Fifteen states permitted craft beer taprooms in 2024, driving demand for smaller 250-330 ml cans with decorative finishes.IN. Independent brewers prefer aluminium for its light-blocking and logistical advantages, while energy-drink brands opt for slim cans that signal performance and fit vending channels. BIS standard IS 17025:2024 raised mechanical-integrity benchmarks, nudging craft operators to outsource to canners equipped with automated seam-inspection systems. The upmarket positioning of both beverage types raises unit margins for converters and further consolidates aluminium’s 62.64% grip on the India metal packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of alternate flexible and rigid plastic solutions | -1.4% | National, cost-sensitive segments | Medium term (2-4 years) |

| Volatility in aluminium and steel prices | -1.1% | Nationwide manufacturing regions | Short term (≤ 2 years) |

| Health concerns around BPA-based can liners | -0.7% | Urban markets with higher awareness | Long term (≥ 4 years) |

| Logistics bottlenecks in regional supply of tinplate | -0.6% | Eastern and Central India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of Alternate Flexible and Rigid Plastic Solutions

Stand-up pouches and rigid PET jars undercut metal on material cost by 30-40% in value-focused food categories . Modern multilayer films now match oxygen and moisture barrier levels once exclusive to metal, eroding the latter’s technical edge in commodity segments. Retailers favor pouches for shelf-space efficiency, and brand owners benefit from a 15-20% freight-cost reduction relative to cans or tins. The Plastic Waste Management Rules permit recyclable mono-material laminates, letting plastics occupy the sustainability narrative. As a result, flexible packaging is siphoning volumes from entry-price foods and home-care SKUs, restraining top-line expansion of the India metal packaging market.

Volatility in Aluminium and Steel Prices

Aluminium traded between USD 1,800-2,400 per tonne in 2024, while steel followed a similar rollercoaster due to energy prices and geopolitical supply shocks.[2]London Metal Exchange, “Aluminium and Steel Price Data 2024,” LME.COM Such swings compress converter margins because contract prices often reset quarterly, whereas metal costs fluctuate almost daily. Smaller can makers lack the balance-sheet strength to hedge via LME futures, and RBI guidelines cap the extent of over-the-counter hedging accessible to micro-enterprises. Tinplate import restrictions under BIS quality-control orders have tightened domestic supply, sending spot premiums upward. This volatility injects procurement risk and slows capex cycles in the India metal packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminium Dominance Drives Innovation

Aluminium held 62.24% of the India metal packaging market share in 2025 and is forecast to sustain leadership as downstream processing investments remove supply bottlenecks. Hindalco’s USD 10 billion program will add coil-coating and can-body stock lines, enabling converters to capture rising beverage volumes without imports. Steel is accelerating at a 7.32% CAGR through 2031 as industrial paints and lubricants demand stronger bulk containers. The India metal packaging market size for steel-based formats is therefore poised to climb at the fastest pace among materials. Tin remains niche but lucrative in premium confectionery and gourmet foods, where consumers associate tin-plate graphics with giftable quality.

Growing numbers of contract canners are adopting lightweight two-piece body designs that trim gauge thickness by up to 12% while preserving stacking strength. For aluminium this translates to freight savings and lower EPR fees per liter of product, supporting overall cost leadership. Steel’s resurgence hinges on paint manufacturers upgrading to UN-rated pails that meet global hazardous-goods rules, which favor high-strength alloys over plastics. Aluminium’s infinite recycling potential complements brand sustainability pledges, and smelter-level decarbonization efforts could further cement its advantage in the India metal packaging market.

By Product Type: Bulk Containers Accelerate Industrial Growth

Cans controlled 41.02% of 2025 revenue, underpinned by soft drinks, beer, and processed foods. The India metal packaging market size for cans will keep expanding, yet bulk containers such as barrels and drums are projected to climb at an 7.65% CAGR to 2031, fueled by industrial output growth. Chemical formulators and paint makers favor metal drums for UN certification and puncture resistance, and the shift to one-way export barrels widens volume potential. Caps and closures piggyback on fill-line upgrades in beverage and pharmaceutical plants, while decorative cans occupy a premium gift segment.

Higher capital allocations in petrochemicals and specialty chemicals under the government’s PLI scheme are triggering fresh demand for 200-liter steel drums. In contrast, aerosol cans add consumer-oriented upside as personal-care brands roll out deodorants and disinfectant sprays. New can lines integrate camera-based seam inspection that cuts rejection rates below 0.5%, a capability essential for the India metal packaging market where QC norms are tightening. Bulk container manufacturers are adopting robotic welding to boost throughput, spreading automation benefits across the product-type mix.

By End-User Industry: Industrial Applications Drive Future Growth

Beverages delivered 31.88% of overall 2025 revenue, but industrial uses are set to record the fastest 7.45% CAGR through 2031. The India metal packaging market size for paints, coatings, and process chemicals is widening as domestic construction and auto sectors rebound. Food remains a resilient customer vertical, particularly canned seafood and ready meals that target urban consumers seeking convenience. Pharmaceuticals demand sterile, tamper-evident packs and commands higher per-unit margins, though volume is modest.

Make-in-India incentives for specialty chemicals motivate global players to localize production, boosting metal barrel and pail consumption. In beverages, returnable steel kegs are gaining among craft breweries, yet one-way aluminium cans dominate retail channels for portability. Industrial customers value steel’s top-load strength during palletization, and epoxied interiors prevent corrosion for solvent-based products. As a result, the India metal packaging market continues to diversify beyond its beverage core, creating a balanced revenue portfolio for converters.

By Coating Type: BPA-Free Alternatives Gain Momentum

Epoxy phenolic coatings accounted for 38.12% revenue in 2025 owing to broad chemical-resistance and affordability. The India metal packaging market size for BPA-free coatings is expected to grow fastest at a 6.93% CAGR as consumer concern over endocrine disruptors gains media traction. Acrylic and polyester chemistries fill niche performance windows, while bio-based resins are in pilot scale. Global suppliers like PPG and AkzoNobel are licensing proprietary formulas to Indian coaters, reducing time-to-market for safer liner.

Regulators have not imposed a national BPA ban, yet FSSAI has lowered migration limits for food-contact materials, nudging brands toward alternatives. Line trials show that BPA-substitute coatings run at similar cure temperatures, avoiding major oven-retrofit costs. Converters that master these chemistries may charge a 4-6% price premium, improving margins against volatile metal prices. Therefore, coating-type innovation remains a strategic lever for differentiation in the India metal packaging market.

Geography Analysis

Production is clustered in Gujarat, Maharashtra, and Tamil Nadu, which together host roughly 65% of national capacity due to port access, smelter proximity, and large FMCG bases. Gujarat leads with integrated smelter-to-can sheet supply chains, cutting logistics drag and shortening lead times. Maharashtra benefits from automotive and consumer-electronics ecosystems that require robust industrial and consumer packs. Tamil Nadu’s food-processing corridor relies on metal cans for shelf-stable products distributed nationwide.

Northern and eastern states rely on inbound supply from western plants, raising freight costs and amplifying the appeal of flexible packaging substitutes. The Atmanirbhar Bharat policy is funneling incentives toward new tinplate lines in Odisha and West Bengal. Cold-chain infrastructure roll-outs underpin processed food demand in Punjab, Haryana, and Uttar Pradesh, giving processors a reason to upgrade from plastic pouches to metal cans that withstand retort sterilization.

Urban hubs such as Delhi NCR, Mumbai, Bengaluru, and Chennai concentrate premium consumption tiers where aluminium cans gain share on brand image grounds. Rural markets are more price sensitive, yet the proliferation of mini-cans and single-serve tins is gradually widening rural penetration. The northeastern region remains under-served due to logistics bottlenecks, though rail-freight corridor upgrades could unlock growth. Export prospects mainly target South Asian neighbors that lack domestic can-making capability but adhere to similar BIS standards, positioning Indian suppliers as near-shore partners.

Competitive Landscape

The India metal packaging market displays a moderate concentration in which global majors Crown, Ball, and Ardagh compete with domestic leaders Hindustan Tin Works, Kaira Can Company, and The Tinplate Company of India. Top five firms collectively command near-60% revenue, leaving a long tail of regional specialists in decorative tins and custom pails. International groups bring proprietary lightweighting and coating IP, while local players wield cost agility and local customer intimacy.

Strategy is converging on lightweight two-piece aluminium cans, BPA-free linings, and circular-economy tie-ups with recyclers. Hindalco’s USD 10 billion downstream capex will feed captive coil to converters, trimming import dependency and stabilizing alloy quality. Crown has taken a 40% stake in Kaira Can to leverage domestic distribution, and Ball has added 1.2 billion units of capacity at Sanand to chase energy-drink growth. Domestic mid-caps are installing Industry 4.0 sensors to boost yield and meet BIS traceability norms.

Price volatility in primary aluminium and tinplate is amplifying procurement complexity. Larger converters hedge via LME contracts, whereas smaller firms pool demand to secure fixed-price slabs. The shift to EPR compliance rewards vertically integrated players that can issue recycling certificates, strengthening their negotiating leverage with brand owners. Niche opportunities persist in pharmaceutical twist-off caps and decorative sweets tins, where design complexity and regulatory hurdles deter new entrants.

India Metal Packaging Industry Leaders

Hindustan Tin Works Ltd.

Zenith Tins Private Limited

Ball Corporation

Nikita Containers Pvt Ltd

Deccan Cans and Printers Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Bureau of Indian Standards issued IS 17839:2025, a test protocol for BPA-free can coatings, setting migration limits that align with EU thresholds.

- September 2024: Hindalco Industries announced a USD 2.8 billion downstream aluminium expansion spanning Gujarat and Odisha, targeting can stock. Project completion is slated for 2027.

- August 2024: Crown Holdings acquired a 40% interest in Kaira Can Company for USD 85 million, gaining local market access and distribution scale.

- July 2024: Ball Corporation invested USD 120 million to lift capacity at its Sanand plant by 1.2 billion cans annually to serve craft beer and energy-drink brands.

India Metal Packaging Market Report Scope

Metal packaging, aluminum and steel, crafts containers for diverse products. These metals, favored for their strength and durability, are the go-to choice for packaging food, beverages, cosmetics, chemicals, and pharmaceuticals. Metal packaging significantly extends product shelf life by offering robust protection against light, air, and moisture. Moreover, its high recyclability positions metal packaging as a more eco-friendly alternative to plastics.

India's Metal Packaging Market is segmented into material type (aluminum, steel), by product type (cans (food cans, beverage cans, aerosol cans), bulk containers, shipping barrels, drums, caps, and closures, and other product types ), and by end-user industry (beverage, food, paints, and chemicals, industrial and other end-user industries). The market sizes and forecasts are in terms of value (USD) for all the above segments.

By Material Type

| Aluminium |

| Steel |

| Tin |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Decorative Cans | |

| Bulk Containers | |

| Drums and Barrels | |

| Caps and Closures | |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Paints, Coatings and Chemicals |

| Pharmaceuticals and Healthcare |

| Industrial |

| Other End-user Industries |

By Coating Type

| Epoxy Phenolic |

| Acrylic |

| Polyester |

| BPA-Free Alternatives |

| Other Coating Types |

| By Material Type | Aluminium | |

| Steel | ||

| Tin | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Decorative Cans | ||

| Bulk Containers | ||

| Drums and Barrels | ||

| Caps and Closures | ||

| Other Product Types | ||

| By End-User Industry | Food | |

| Beverage | ||

| Paints, Coatings and Chemicals | ||

| Pharmaceuticals and Healthcare | ||

| Industrial | ||

| Other End-user Industries | ||

| By Coating Type | Epoxy Phenolic | |

| Acrylic | ||

| Polyester | ||

| BPA-Free Alternatives | ||

| Other Coating Types | ||

Key Questions Answered in the Report

What is the current value of the India metal packaging market?

The market stands at USD 10.81 billion in 2026 and is projected to reach USD 14.24 billion by 2031.

Which material dominates Indian metal packaging?

Aluminium leads with a 62.24% share because of its light weight and high recycling rate.

Which end-user segment will grow fastest?

Industrial applications such as paints and chemicals are expected to rise at a 7.45% CAGR to 2031.

Why is BPA-free coating gaining traction?

Rising consumer health awareness and stricter FSSAI migration limits are pushing converters toward BPA-substitute chemistries.

How is EPR influencing packaging choices?

EPR mandates penalize non-recyclable formats, so brands increasingly pick metal containers that have established recycling streams.

What are the main geographic production hubs?

Gujarat, Maharashtra, and Tamil Nadu host about 65% of national manufacturing capacity because of smelter proximity and industrial demand.

Page last updated on: