Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

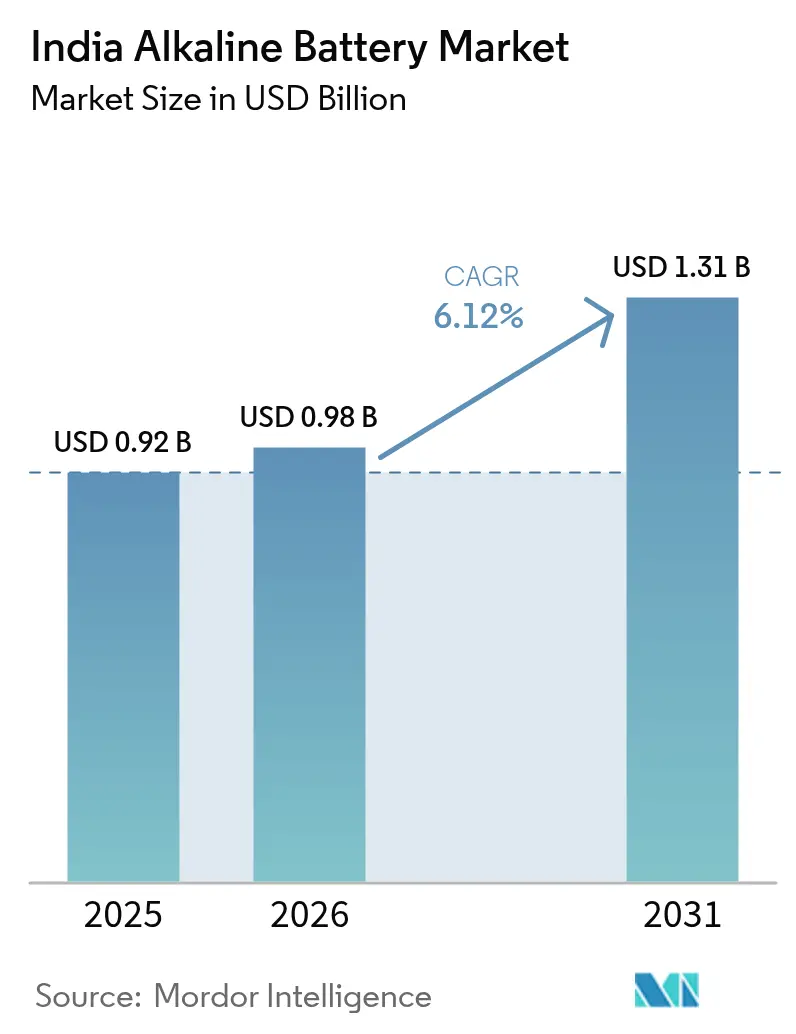

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

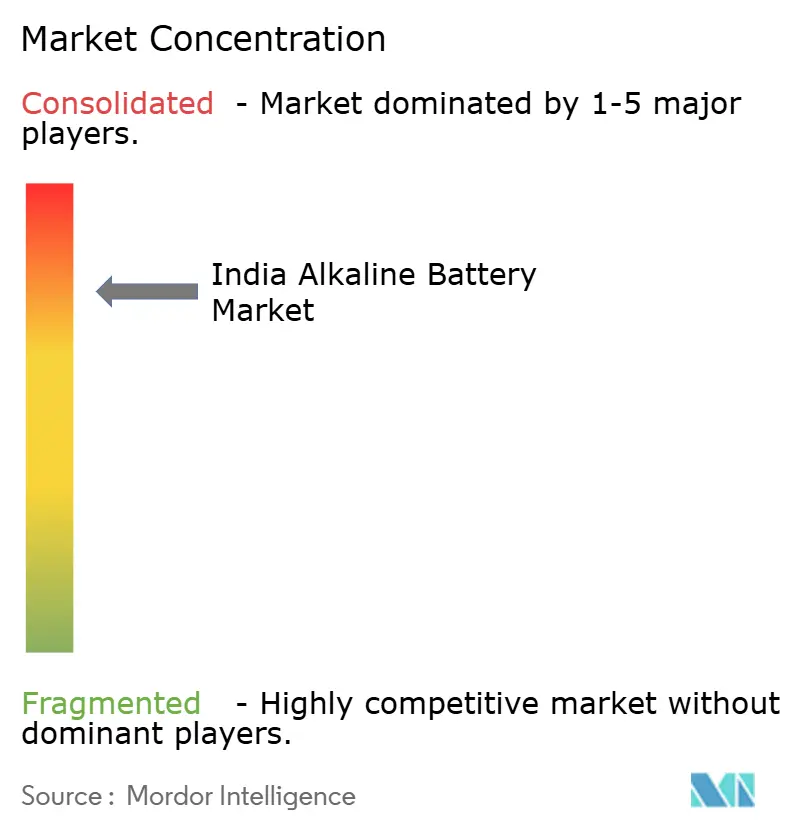

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Alkaline Battery Market Analysis by Mordor Intelligence

The India Alkaline Battery Market size was valued at USD 0.92 billion in 2025 and estimated to grow from USD 0.98 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

Rising disposable incomes, expanding consumer-electronics penetration, and a structural shift away from zinc-carbon chemistry are steering demand toward longer-lasting alkaline cells. E-commerce platforms, organized retail expansion, and defense procurement increase addressability, while Bureau of Indian Standards (BIS) compliance rules favor branded suppliers over unorganized trade. At the same time, rechargeable lithium-ion solutions are cannibalizing high-drain applications, prompting incumbents to pivot into premium alkaline niches and rechargeable portfolios. Extended Producer Responsibility (EPR) guidelines, volatile potassium-hydroxide inputs, and counterfeit batteries temper the growth outlook but also accelerate consolidation among compliant players.

Key Report Takeaways

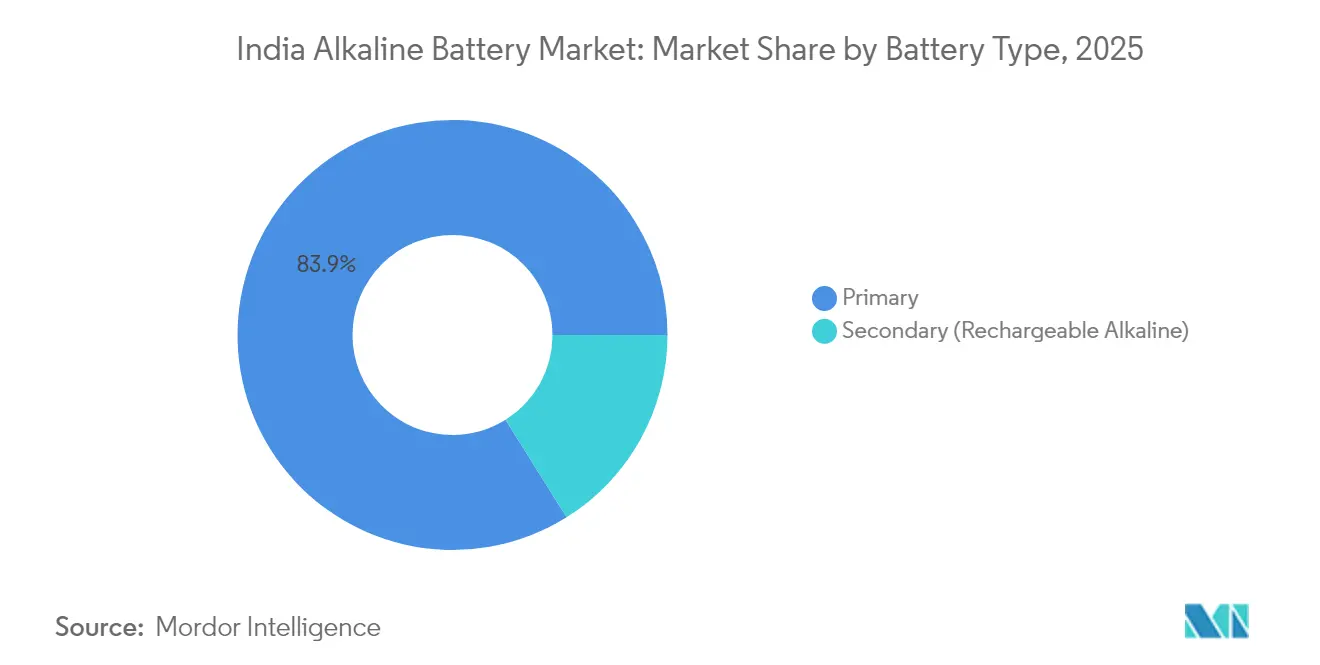

- By battery type, primary cells led with 83.90% of the India Alkaline Battery market share in 2025, while secondary (rechargeable alkaline) units are forecast to accelerate at an 11.05% CAGR through 2031.

- By size, AA (LR6) batteries accounted for 40.35% of the India Alkaline Battery market size in 2025, whereas 9-volt formats are projected to expand at a 9.62% CAGR between 2026 and 2031.

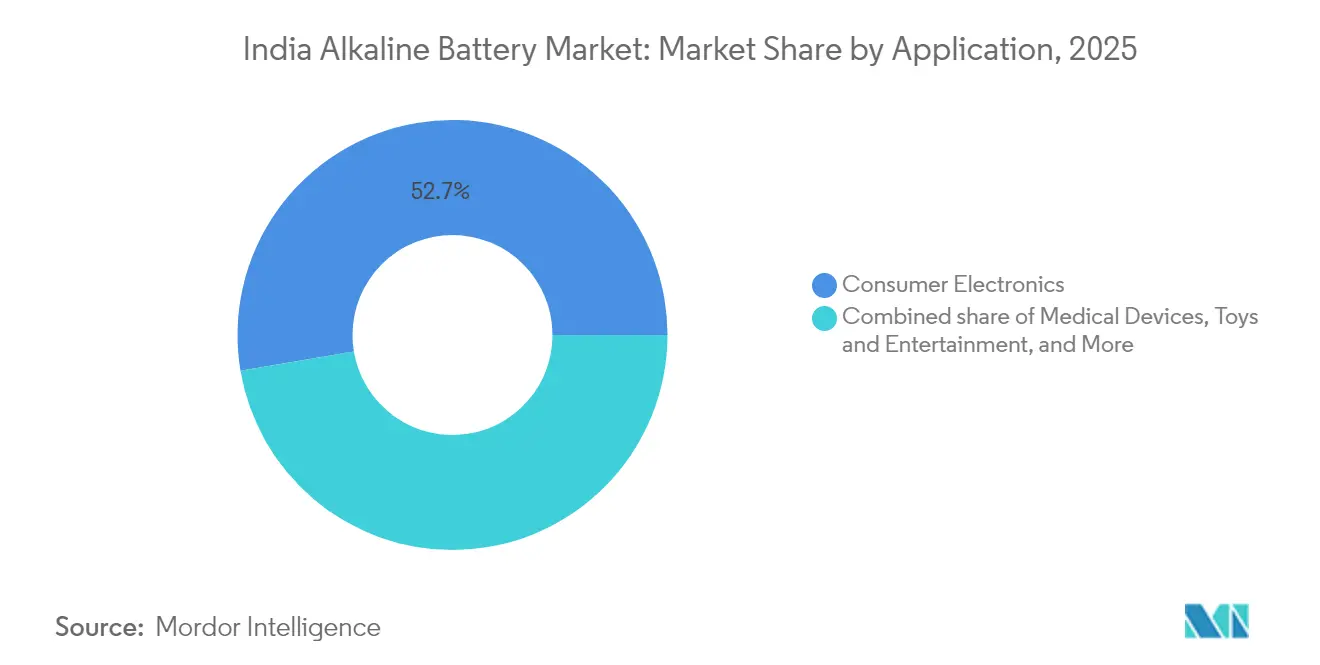

- By application, consumer electronics commanded a 52.65% share of the India Alkaline Battery market size in 2025, and medical devices are poised for a 9.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Alkaline Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in consumer electronics penetration & disposable income | 1.2% | Pan-India, with urban concentration in metros and Tier-1 cities | Medium term (2-4 years) |

| Rural electrification outages driving portable power demand | 0.8% | Rural and semi-urban areas, particularly Uttar Pradesh, Bihar, Jharkhand, and Northeastern states | Long term (≥ 4 years) |

| Defense procurement of rugged alkaline cells for border surveillance | 0.3% | Border regions including Jammu & Kashmir, Ladakh, Arunachal Pradesh, and Rajasthan | Long term (≥ 4 years) |

| Rapid growth in e-commerce & organized retail channels | 0.9% | Urban and Tier-2 cities with high internet penetration and logistics infrastructure | Short term (≤ 2 years) |

| Shift from zinc-carbon to alkaline on cost & energy density | 1.5% | Pan-India, with faster adoption in urban metros and Tier-1/Tier-2 cities; gradual penetration in rural markets | Medium term (2-4 years) |

| Toy manufacturing clusters' compliance needs (lead-free) | 0.4% | Manufacturing clusters in Maharashtra, Tamil Nadu, Gujarat, and Karnataka with BIS IS 15644:2006 enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge In Consumer Electronics Penetration & Disposable Income

Disposable-income gains and an expanding installed base of battery-powered devices continue to widen the customer pool for the India Alkaline Battery market. Remote controls, toys, wall clocks, wireless peripherals, and digital thermometers dominate the replacement cycle, and a three-fold price premium over zinc-carbon translates to three-to-ten-times longer runtime for alkaline cells. Eveready’s alkaline revenue rose 90.8% year-on-year in Q3 FY25 as it pursued a 53% market-share target within four years. Mid-market entrant Nippo Thor followed with a 3-4% share after only 11 months on the shelf. Yet lithium-ion powerpacks have captured earbuds, smartwatches, and Bluetooth speakers, constraining alkaline’s headroom in the fastest-growing electronics segments. Manufacturers respond by deepening penetration in moderate-drain uses where rechargeability confers minimal benefit.

Rural Electrification Outages Driving Portable Power Demand

Intermittent grid supply in large swaths of rural India sustains a sizable opportunity for the India Alkaline Battery market. Despite a cumulative renewable-energy capacity of 220 GW, frequent load-shedding in Uttar Pradesh, Bihar, Jharkhand, and the Northeast prompts households to stockpile batteries for torches, radios, and emergency lanterns.[1]Ministry of New and Renewable Energy, “Annual Report 2025,” mnre.gov.in Alkaline chemistry offers superior shelf life and cold-weather performance, especially valuable in storage-heavy consumption patterns. Eveready’s new Jammu plant positions the firm near defense zones and rural markets in North India, trimming logistics costs and bolstering cold-chain supply. Rooftop solar adoption adds a paradoxical boost, as users attach alkaline-powered backup lights for the monsoon season or nighttime outages. Nevertheless, ongoing grid upgrades and declining prices for rechargeable lanterns may cap rural alkaline demand beyond the medium term.

Rapid Growth In E-Commerce & Organized Retail Channels

Digital marketplaces and big-box outlets are reshaping distribution economics for the India Alkaline Battery market. Amazon, Flipkart, Zepto, and Blinkit publish transparent pricing, customer reviews, and instant delivery options that shift buyers away from unbranded zinc-carbon cells traditionally sold at kiranas. Organized chains such as Reliance Retail and DMart allocate end-aisle displays and bundle promotions that elevate brand salience for alkaline SKUs. Indo National targets a near-doubling of revenue over five years, citing e-commerce reach as a central pillar in its growth thesis. Platform-owned private labels like Amazon Basics introduce price-competitive alternatives, intensifying the need for incumbents to emphasize superior leakage protection and BIS certification.

Shift From Zinc-Carbon To Alkaline On Cost & Energy Density

Alkaline batteries deliver up to ten times longer service life than zinc-carbon equivalents, cutting replacement frequency and total lifetime cost for moderate-drain devices. As disposable incomes rise, urban consumers increasingly value performance over initial outlay, pushing the India Alkaline Battery market deeper into mainstream retail channels. Eveready expanded alkaline capacity to underpin its shift from a zinc-carbon defensive stance to an aggressive share-capture strategy. Scalability benefits also emerge as higher unit volumes lower per-cell manufacturing costs, narrowing the premium and hastening the chemistry transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Li-ion adoption cannibalizing primary alkaline sales | -0.6% | Urban metros and Tier-1 cities with high consumer electronics adoption | Short term (≤ 2 years) |

| EPR & single-use battery waste regulations tightening | -0.4% | Pan-India, with enforcement concentrated in urban municipal corporations | Medium term (2-4 years) |

| Volatile KOH supply chain inflating input costs | -0.3% | Pan-India impact on manufacturing costs, affecting all alkaline battery producers with domestic and imported potassium hydroxide sourcing | Short term (≤ 2 years) |

| Counterfeit low-grade cells eroding brand trust | -0.5% | Rural and semi-urban areas with unorganized retail dominance; Tier-3 cities and districts with limited BIS enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Li-Ion Adoption Cannibalizing Primary Alkaline Sales

Rechargeable lithium-ion packs expand at a 22.7% CAGR in India, displacing single-use cells in earbuds, power tools, and portable speakers. In urban cores, a rechargeable AA-equivalent lithium-ion cell can replace fifty or more alkaline units over its life, tipping the value equation sharply. Eveready and Indo National hedge the risk by acquiring stakes in lithium-ion producers and broadening flash-light portfolios that maintain customer ties post-alkaline. Cannibalization remains most acute in metros where USB-C charging is pervasive; rural markets lag because of charger scarcity and higher perceived up-front costs.

EPR & Single-Use Battery Waste Regulations Tightening

The Battery Waste Management Rules 2022 require 90% collection of portable cells by 2026-27 and a minimum 5% recycled content by 2027-28, scaling to 20% by 2030-31.[2]Ministry of Environment, Forest and Climate Change, “Battery Waste Management Rules 2022,” moefcc.nic.in Alkaline recycling yields low-value metals, rendering compliance a cost rather than a profit center. Producers must fund reverse logistics, certify collection audits, and integrate recycled zinc and manganese into supply chains despite limited domestic availability. For smaller players, regulatory overhead invites market exit, while compliant majors can leverage scale to absorb costs and differentiate on sustainability messaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Primary Cells Retain Lead While Rechargeable Niche Grows

Primary cells represented 83.90% of India's Alkaline Battery market share in 2025, reinforcing their dominance in moderate-drain devices such as remote controls and flashlights. The India Alkaline Battery market anticipates incremental substitution toward rechargeable formats, yet mass adoption remains restrained by charger availability gaps and higher first-purchase pricing. Eveready's 46.3% alkaline sales jump in Q4 FY25 underscores ongoing migration from zinc-carbon to single-use alkaline across all channels.

Rechargeable alkaline batteries are projected to expand at an 11.05% CAGR through 2031, albeit from a low installed base. They win favor in industrial instrumentation and professional lighting, where reusability offsets cost and where lithium-ion faces certification or safety hurdles at extreme temperatures. BIS IS 16046 standards support certification, but nickel-metal hydride and lithium-ion still outpace secondary alkaline in energy density.

By Size: AA Cells Dominate, 9-Volt Formats Accelerate

AA cells controlled 40.35% of the India Alkaline Battery market size in 2025, bolstered by the largest installed device base and ubiquitous channel presence. Competitive pricing, Duracell AA ten-packs at INR 205-256, keeps momentum strong, while local brands narrow the premium gap. AAA, C, and D categories serve flashlights, radios, and larger lanterns, but LED efficiency gains shrink these volumes over time.

The fastest trajectory belongs to 9-volt batteries, forecast to grow 9.62% CAGR through 2031, propelled by smoke-detector mandates, glucometers, and security sensors that demand assured runtime and leak-proof performance. Premium positioning enables higher margins, and suppliers leverage differentiated marketing that stresses safety compliance and long shelf life.

By Application: Consumer Electronics Drive Volume; Medical Devices Emerge

Consumer electronics contributed 52.65% of India's Alkaline Battery market demand in 2025, spanning hundreds of millions of remote controls and toys. However, high-growth wearables now rely exclusively on lithium-ion, restricting alkaline's upside in the most dynamic categories. Brands, therefore, focus on reinforcing performance messaging in moderate-drain peripherals and bundling batteries with device sales through e-commerce promotions.

Medical devices represent the fastest-growing end-use, advancing at a 9.95% CAGR as point-of-care diagnostics penetrate home-health settings. Reliable voltage delivery, sterilization constraints, and extended shelf life support alkaline preference in glucometers, pulse oximeters, and portable ECG monitors. Government health programs that distribute diagnostic kits to primary health centers further widen rural uptake.

Geography Analysis

Urban metros and Tier-1 cities absorbed roughly 64.40% of India's Alkaline Battery market demand in 2025, thanks to higher spending power, concentrated organized retail networks, and same-day e-commerce fulfillment. Maharashtra, Tamil Nadu, Gujarat, Karnataka, and Delhi-NCR together accounted for half of national consumption, while Eveready’s Jammu plant unlocks distribution efficiency for North India and border-state defense customers.

Rural and semi-urban regions delivered about 35.60% of volume, underpinned by grid-reliability gaps and zinc-carbon substitution as incomes rise. Distribution relies on multi-tier wholesaler networks that expose the market to counterfeit batteries lacking BIS IS 15063 certification. Quick-commerce and organized retail expansion into Tier-2 and Tier-3 cities gradually improves brand availability, lifting alkaline share in historically underserved areas.

Strategic demand arises in Ladakh, Arunachal Pradesh, Sikkim, and Rajasthan, where defense agencies procure alkaline packs for surveillance and communication gear. Extreme-temperature performance remains essential, and proximity to Eveready’s Jammu facility reduces lead times. Enforcement of Battery Waste Management Rules is strongest in Delhi, Mumbai, and Bengaluru, offering compliant players a regulatory moat and pushing non-conforming units out of organized channels.

Competitive Landscape

The India Alkaline Battery market is moderately concentrated: Eveready and Indo National jointly command roughly 75% of the broader dry-cell segment, yet the premium alkaline share historically skewed toward Duracell at nearly 70% of the high-end tier. Eveready’s INR 1.8 billion Jammu plant marks a decisive bid for majority alkaline leadership, while Indo National’s Nippo Thor scales rapidly from a 3-4% slice to a 20-25% revenue target within eighteen months. Duracell’s 2025 licensing pact with Satya International to produce automotive and inverter batteries across 59 countries signals diversification as EPR regulations raise compliance costs in single-use portfolios.

Private-label incursions from Amazon Basics intensify price pressure, exploiting platform data to segment customers and bundle subscription replenishment. Quick-commerce operators Zepto and Blinkit compress delivery windows to hours, raising per-capita battery turnover in urban enclaves. Regulatory oversight sharpened when the Competition Commission of India fined Panasonic Energy and Geep Industries INR 9.64 crore in 2018 for cartel behavior, cautioning vendors against exclusive tendering in institutional channels. Compliance with BIS toy-safety and battery-performance codes filters out counterfeit imports, but enforcement in rural districts remains inconsistent, keeping a gray market alive.

India Alkaline Battery Industry Leaders

Duracell Inc.

Indo National Limited

Eveready Industries India Ltd.

Panasonic Energy India Co Ltd.

Geep Industries Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Parliament was informed that the India government is backing the creation of a 50 GWh capacity through the Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell (ACC) battery storage. Furthermore, in addition to those applying under the PLI ACC scheme, a minimum of 10 manufacturers have collectively declared plans for a capacity of approximately 178 GWh in the country over the coming five years.

- November 2025: Eveready Industries India Ltd has launched its latest innovation, the Eveready Ultima Lithium series. This new series represents the pinnacle of the company's battery technology. Tailored for high-drain, tech-savvy devices, the Ultima Lithium batteries come in both AA and AAA formats, boasting a lifespan that's up to 15 times longer than traditional alkaline cells.

- March 2025: In a bid to bolster its "Make In India" initiative, Eveready has unveiled plans to invest INR 1.8 billion in establishing a new alkaline battery manufacturing unit in Jammu, India. This facility, set to commence operations in the latter half of FY26, will not only enhance production capacity but also cater to B2B and OEM sales, marking a significant milestone as India's inaugural unit of its kind.

India Alkaline Battery Market Report Scope

Alkaline batteries, utilizing potassium hydroxide (KOH) as their electrolyte, stand apart from zinc-carbon batteries that rely on acidic electrolytes. Their superior energy density, extended shelf life, and enhanced performance have made alkaline batteries a popular choice.

The India Alkaline Battery Market is segmented by battery type, size, application, and geography. By battery type, the market is segmented into primary alkaline batteries and secondary (rechargeable) alkaline batteries. By size, the market is segmented into AA (LR6), AAA (LR03), 9-volt, C, D, coin, and specialty batteries. By application, the market is segmented into consumer electronics, industrial and commercial devices, medical devices, toys and entertainment, and lighting and flashlights. The report covers market size and forecasts for all segments, with market estimation and projections provided in terms of value (USD).

By Battery Type

| Primary |

| Secondary (Rechargeable Alkaline) |

By Size

| AA (LR6) |

| AAA (LR03) |

| 9-Volt |

| C |

| D |

| Coin and Specialty |

By Application

| Consumer Electronics |

| Industrial and Commercial Devices |

| Medical Devices |

| Toys and Entertainment |

| Lighting and Flashlights |

| By Battery Type | Primary |

| Secondary (Rechargeable Alkaline) | |

| By Size | AA (LR6) |

| AAA (LR03) | |

| 9-Volt | |

| C | |

| D | |

| Coin and Specialty | |

| By Application | Consumer Electronics |

| Industrial and Commercial Devices | |

| Medical Devices | |

| Toys and Entertainment | |

| Lighting and Flashlights |

Key Questions Answered in the Report

How large is the India Alkaline Battery market in 2026?

It stands at USD 0.98 billion and is projected to hit USD 1.31 billion by 2031.

Which battery type dominates sales?

Primary alkaline cells account for 83.90% of 2025 demand, supported by remote controls, toys, and flashlights.

Why are 9-volt batteries growing fastest?

Smoke-detector mandates, medical devices, and security sensors need leak-proof, longer-life power, driving a 9.62% CAGR through 2031.

What role does e-commerce play in distribution?

Platforms like Amazon and Flipkart provide transparent pricing and same-day delivery, accelerating branded-battery penetration, especially in Tier-1 and Tier-2 cities.

How will new EPR rules affect the sector?

Producers must collect 90% of sold batteries by 2026-27 and integrate recycled content, raising compliance costs and encouraging consolidation.

Which companies lead the competitive landscape?

Eveready Industries, Indo National (Nippo), and Duracell hold the largest branded shares, with Eveready targeting a majority stake via its new Jammu plant.

Page last updated on: