Impact Investing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

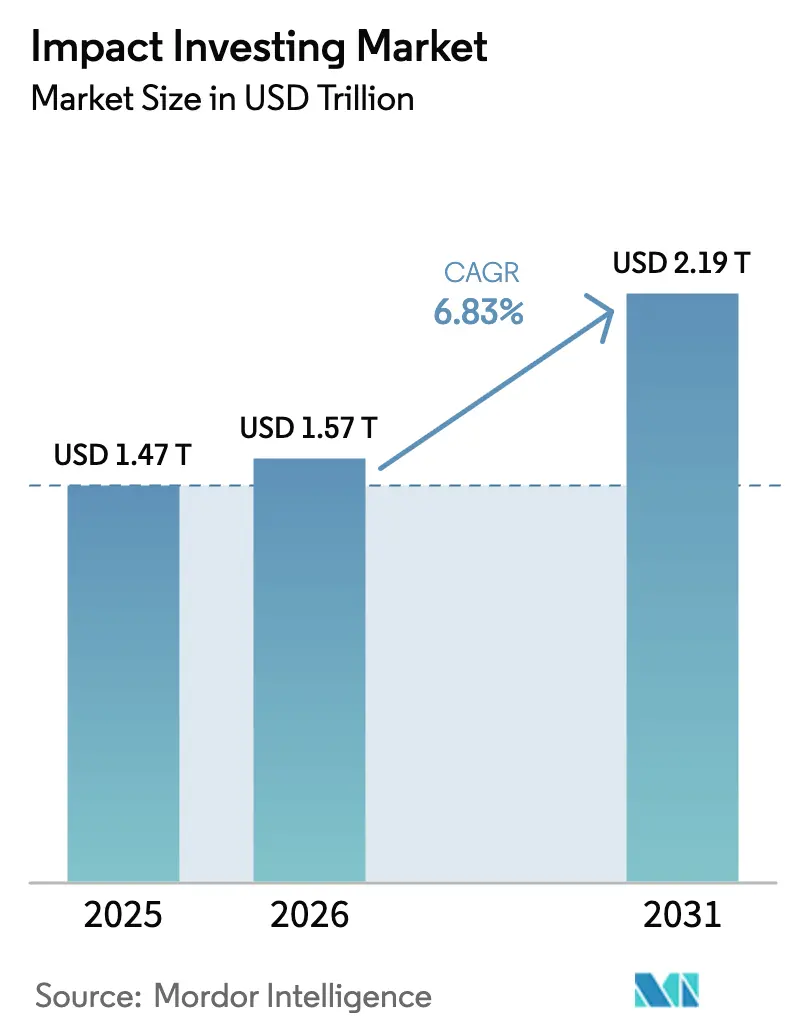

| Market Size (2026) | USD 1.57 Trillion |

| Market Size (2031) | USD 2.19 Trillion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

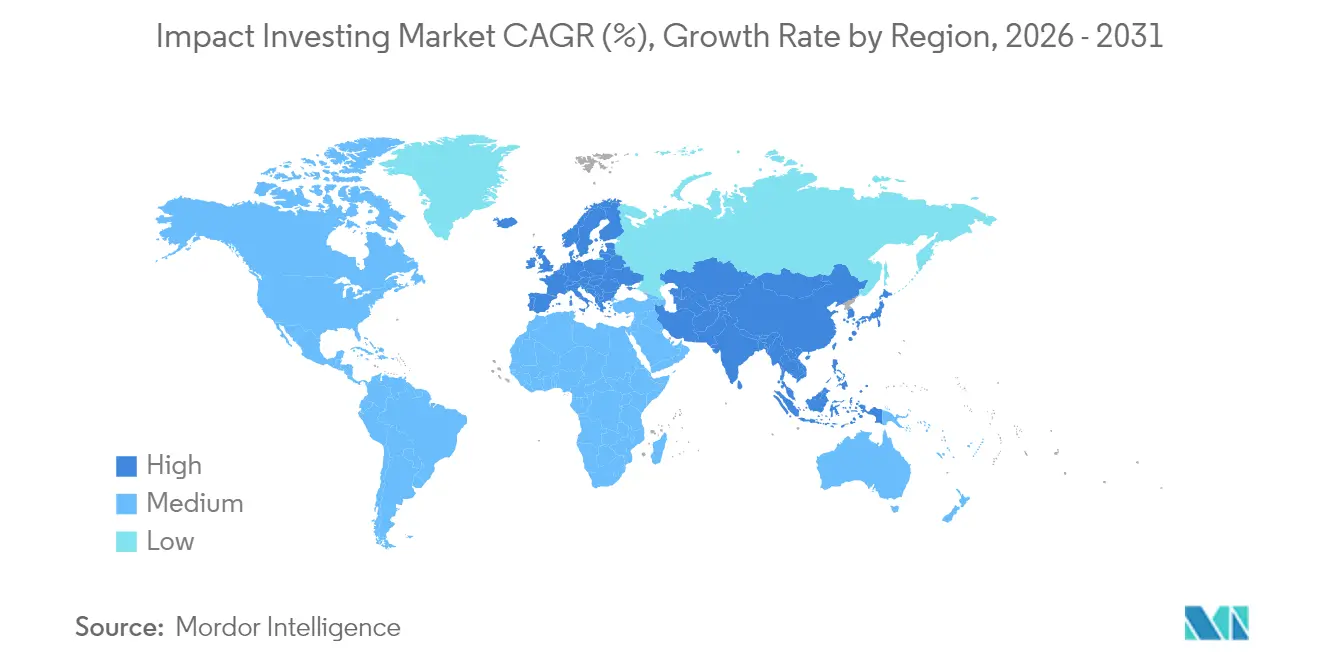

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Impact Investing Market Analysis by Mordor Intelligence

Impact Investing Market size in 2026 is estimated at USD 1.57 trillion, growing from 2025 value of USD 1.47 trillion with 2031 projections showing USD 2.19 trillion, growing at 6.83% CAGR over 2026-2031.

The numbers confirm the shift from philanthropic origins toward a core institutional allocation strategy that now shapes mainstream portfolio construction across developed economies. Mandatory sustainability disclosure rules, expanding sovereign green bond programs, and rising demand for measurable outcomes are aligning regulatory signals and investor behavior, creating strong tailwinds for the impact investing market. Private equity is gaining traction as the preferred vehicle for deep impact measurement, while technology-enabled fund distribution improves retail access and feeds fresh liquidity into the ecosystem. Fragmented competition, combined with persistent exit-market constraints, is setting the stage for both consolidation and innovation as specialist managers seek scale through acquisitions and tokenization platforms.

Key Report Takeaways

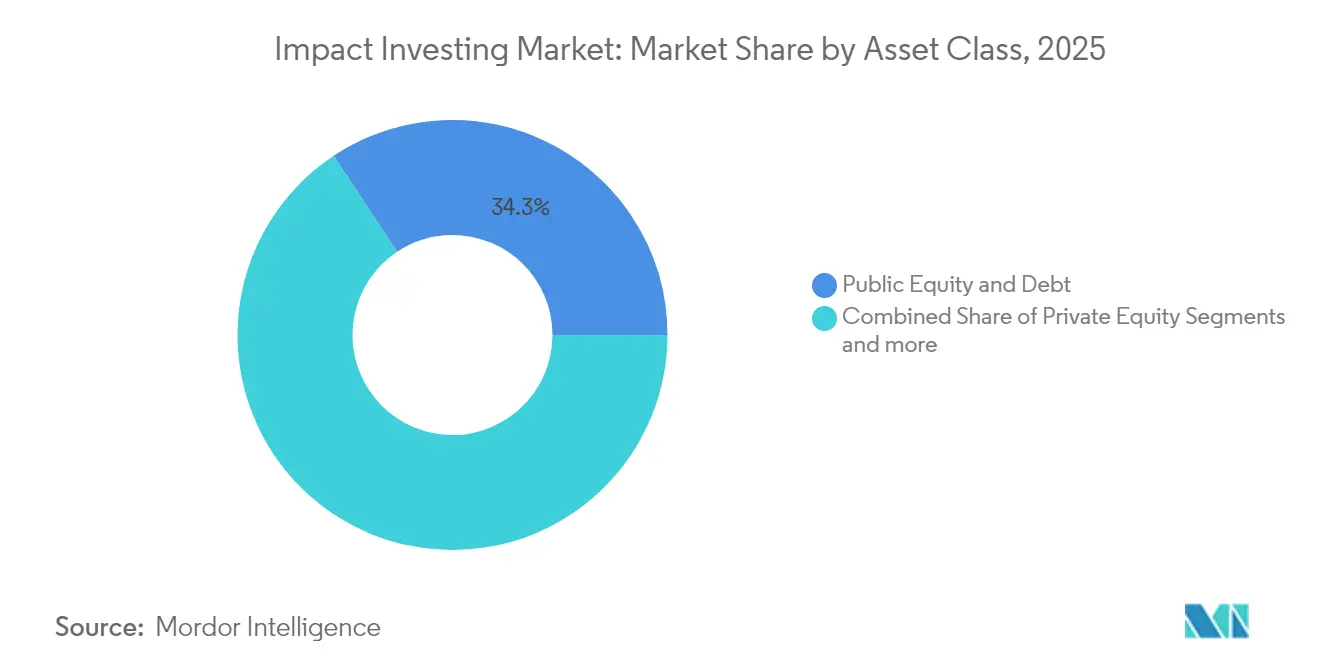

- By asset class, public equity and debt instruments led with 34.32% revenue share of the impact investing market in 2025, while private equity is forecast to grow at 11.03% CAGR through 2031.

- By investor type, institutional investors held 41.92% of the impact investing market share in 2025, and individual investors are projected to expand at 10.38% CAGR to 2031.

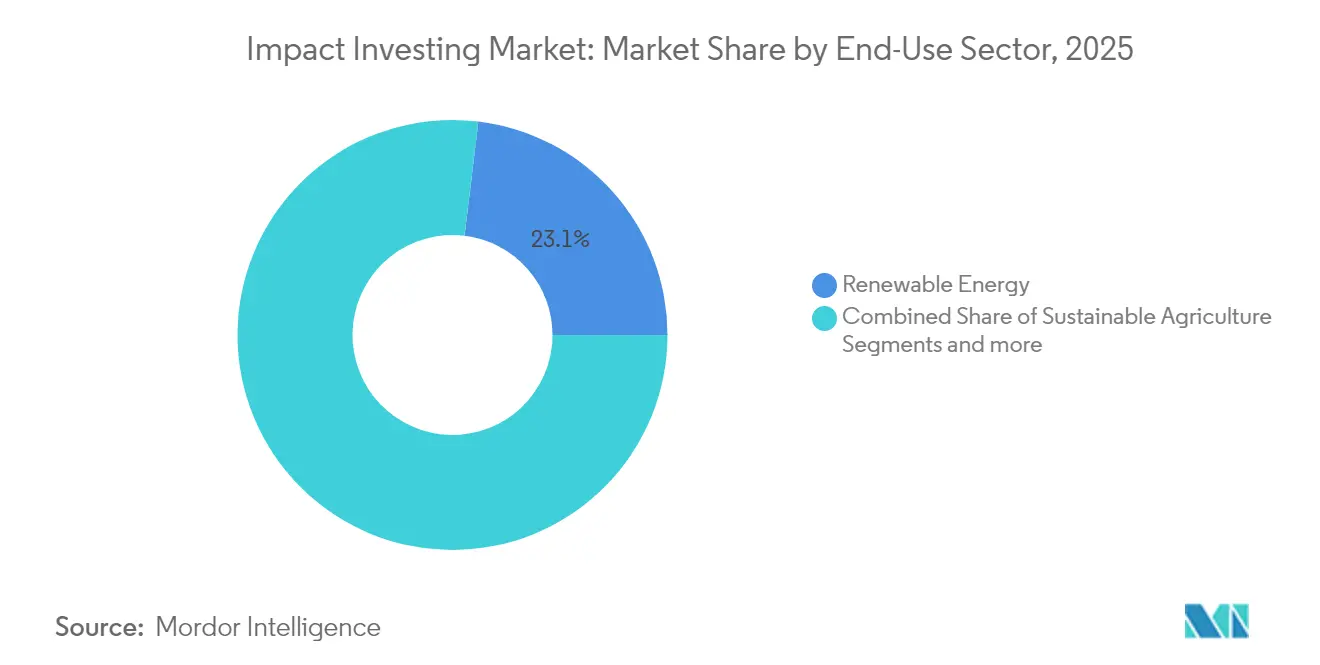

- By end-use sector, renewable energy controlled 23.08% of the impact investing market size in 2025; sustainable agriculture is on track for a 9.33% CAGR between 2026 and 2031.

- By geography, Europe accounted for 33.21% of the impact investing market in 2025, while Asia Pacific is set to register an 8.70% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Impact Investing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream ESG regulation mandates | +1.8% | Global, led by EU and North America | Medium term (2-4 years) |

| Institutional portfolio re-allocation to private impact vehicles | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Retail wealth platforms adding impact sleeves | +1.2% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Outcome-based blended-finance structures de-risking returns | +0.9% | Emerging markets, spill-over to developed | Medium term (2-4 years) |

| Tokenised impact funds lowering entry tickets | +0.7% | Global, early adoption in tech-forward markets | Short term (≤ 2 years) |

| Climate-linked insurance payouts unlocking new asset classes | +0.6% | Global, concentrated in climate-vulnerable regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream ESG Regulation Mandates

The EU Corporate Sustainability Reporting Directive obliges nearly 50,000 European companies to publish audited impact metrics from 2024, transforming non-financial data from a voluntary disclosure into a fiduciary requirement [1]European Commission, “Directive (EU) 2022/2464 as regards corporate sustainability reporting,” eur-lex.europa.eu . Large US asset managers, therefore, pre-position portfolios for an eventual SEC climate rule, even as debate continues in Congress. Regulators are also adjusting insurance capital rules so that climate-resilient assets attract lower solvency charges, effectively rewarding allocations into verified impact strategies. As these harmonised standards spread, the impact investing market benefits from a policy-driven expansion of eligible capital, especially through pension plans that now see climate risk as a core duty. The combined effect is a structural rise in demand for third-party verified impact vehicles able to satisfy tougher audit requirements.

Institutional Portfolio Re-allocation to Private Impact Vehicles

Pension funds are lifting alternative exposure targets toward 20% by 2030 as they seek illiquidity premiums and measurable outcomes unavailable in public securities. The Canada Pension Plan Investment Board alone plans to deploy CAD 130 billion into sustainable assets by 2030, a clear illustration of the scale potential. Private impact vehicles offer tighter governance and direct project oversight, enabling investors to link carried interest with social or environmental milestones. This capability alleviates regulators’ concerns about greenwashing and improves investment committee confidence. With historical data now showing 200–400 basis points of excess return for fully-priced private impact funds, portfolio strategists no longer see an opportunity-cost penalty. Larger allocations are therefore expected to come from sovereign wealth funds that treat impact investing market exposure as a strategic diversification play in a maturing low-carbon economy.

Retail Wealth Platforms Adding Impact Sleeves

Digital brokerages and robo-advisers lower traditional ticket sizes through fractional shares, making the impact investing market accessible to millions of retail accounts. Morgan Stanley’s Investing with Impact platform managed USD 75 billion by 2023 and continues to gain traction among millennials seeking values-aligned portfolios [2]Morgan Stanley, “Investing with Impact Platform Crosses USD 75 Billion,” morganstanley.com . Robinhood is piloting the on-chain tokenization of 200 blue-chip equities, promising 24-hour liquidity plus smart-contract enforcement of ESG screens. Platform features such as automated impact scoring and real-time carbon dashboards drive customer stickiness while lowering the advice burden for human advisers. As regulatory guidance on crypto-securities clarifies, this retail flow is expected to amplify price discovery in verified impact assets and reinforce transparency norms across the broader impact investing industry.

Outcome-based Blended-Finance Structures De-risking Returns

The World Bank’s new guarantee framework reduces political and currency risk through unfunded risk participation facilities that trigger payouts only if pre-defined impact milestones fail, aligning incentives among all capital providers. Development finance institutions now price blended credit at market rates, signaling confidence in project fundamentals. Structured vehicles that combine junior catalytic capital with senior commercial tranches leverage public funds by as much as four to one, closing the bankability gap for projects in climate adaptation and gender inclusion. Because returns hinge on objectively verified outcomes, performance risk is shared rather than transferred, which appeals to institutional mandates wary of concessionary optics. The approach effectively widens the investable universe for the impact investing market and supports growth in underserved geographies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-washing litigation risk inflating compliance costs | -1.1% | Global, concentrated in litigious jurisdictions | Short term (≤ 2 years) |

| Limited depth of exit markets for impact assets | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Data scarcity on real-time impact KPIs | -0.6% | Global, severe in developing economies | Long term (≥ 4 years) |

| Rising interest rates dampening concessional capital supply | -0.9% | Global, particularly affecting DFI funding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Green-washing Litigation Risk Inflating Compliance Costs

Heightened regulator vigilance has produced sizeable fines against funds that failed to substantiate marketing claims, with the SEC bringing multiple high-profile actions since 2024 [3]U.S. Securities and Exchange Commission, “Enforcement in ESG Funds,” sec.gov . European enforcement under SFDR escalated in 2025 through random audits of Article 9 funds, leading many managers to upgrade data systems and hire third-party verifiers. Compliance spend across the impact investing market is rising 15–20% each year, and litigation insurance premiums have doubled, deterring smaller entrants. Investors now demand granular KPI disclosures plus independent assurance, lengthening reporting cycles, and compressing margins. Although stricter policing curbs reputational risk, it also removes capital from productive deployment during protracted legal proceedings.

Limited Depth of Exit Markets for Impact Assets

Extended holding periods create vintage concentration and mismatch pension fund liquidity schedules. The Blue Earth Capital and British International Investment secondary deal in April 2025 supplied welcome liquidity but underscored the scarcity of scaled buyers. Listing options are narrow because public markets still apply discounted cash flow models that ignore social premiums. Without broader exit pathways, capital recycling slows, dampening overall growth in the impact investing market. Dedicated impact-focused SPACs have shown mixed performance, and regulatory delays have further hindered issuance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Private Equity Disrupts Public Market Dominance

Public equity and debt retained 34.32% of the impact investing market in 2025, a legacy of investor familiarity with listed securities. Private equity, however, is projected to compound at 11.03% through 2031, reflecting a decisive appetite for direct ownership that improves influence over on-the-ground operations. Private debt is gathering pace as banks retreat from capital-intensive developmental lending, transferring origination opportunities to specialist credit funds. Real-asset vehicles, including timber and regenerative agriculture, benefit from clear linkages between asset performance and measurable ecosystem outcomes, reinforcing the portfolio diversification case.

Operational value-creation is central to private equity theses, with managers implementing impact management systems akin to operational excellence programs in traditional buy-outs. TPG Rise’s acquisition of MIRATECH improved emissions abatement at industrial clients while delivering above-benchmark EBITDA growth, exemplifying how operational levers translate into verified impact . Fund managers are also experimenting with tokenised feeder funds that cut administrative overhead and facilitate quicker closings. Cash management strategies remain conservative; impact-aligned money market funds preserve liquidity but accept lower yields to avoid exposure to firms without robust ESG credentials. Over the horizon, the anticipated launch of regulated impact-focused secondary exchanges promises to shorten holding periods and further bolster the impact investing market.

By Investor Type: Individual Participation Accelerates Institutional Dominance

In 2025, institutional investors held 41.92% of total assets, demonstrating their advanced capabilities in identifying customized investment structures and securing fee reductions. Conversely, individual investors are experiencing a compound annual growth rate (CAGR) of 10.38%, indicating an increasing interest from retail investors as digital wealth management platforms broaden access to investment opportunities. Family offices serve as innovative asset allocators, frequently testing specialized strategies prior to their adoption by larger public pension funds. This trend highlights the evolving landscape of investment management, where both institutional and individual investors are adapting to new market dynamics. The rise of digital channels is pivotal in transforming the investment landscape, making it more inclusive for retail participants.

Generational wealth shifts compound the trend. Surveys reveal that 70% of millennial high-net-worth individuals intend to direct a majority of their portfolios toward purpose-aligned strategies by 2030. Platforms embed social-media style dashboards that compare real-time carbon savings or job-creation metrics against peers, fuelling friendly competition and reinforcing engagement. Institutional allocators still enjoy due diligence advantages, but the collective voice of retail investors can now sway shareholder resolutions and influence proxy voting outcomes inside listed impact funds. This convergence of capital sources blurs traditional segmentation lines and enriches data networks that underpin the broader impact investing market.

By End-Use Sector: Agriculture Innovation Challenges Energy Incumbency

Renewable energy captured 23.08% of 2025 allocations thanks to supportive feed-in tariffs, rising corporate power-purchase agreements, and sovereign climate commitments. Yet, sustainable agriculture posts the fastest expansion at 9.33% CAGR, signifying investor recognition that resilient food systems are critical to adaptation agendas. Microfinance and MSME lending benefit from digital origination platforms that slice underwriting costs by half, translating into higher risk-adjusted yields. Healthcare impact strategies align with value-based payment reforms, while education technology plays a role in addressing the global skills gap through scalable SaaS models.

Blended finance is pivotal to agri-finance growth. Catalytic first-loss tranches absorb weather and price shocks, unlocking commercial senior debt at competitive coupons. KKR Global Impact’s focus on controlled-environment agriculture demonstrates how operational efficiencies and resource-use metrics resonate with institutional investors. Carbon credit pre-purchase agreements further enhance revenue visibility for regenerative farming projects, smoothing cash flows and satisfying performance-linked note structures. The continued maturation of verification protocols should attract mainstream insurers keen to diversify climate risk pools, solidifying agriculture as a core pillar of the impact investing market.

Geography Analysis

Europe commanded 33.21% of the impact investing market in 2025, supported by a unified regulatory environment that standardises reporting and mobilises sovereign green-bond capital. Development banks in Germany and France co-finance large-scale renewable infrastructure, crowding in institutional investors through partial guarantees. The United Kingdom sustains its role as a structuring hub, leveraging regulatory sandboxes to pilot performance-linked securitisations that improve data transparency. Nordic nations demonstrate high per-capita allocations, reflecting deep societal commitment to sustainability and supportive pension regimes. Despite macro headwinds, European managers benefit from domestic demand that offsets slower fundraising in other regions.

Asia Pacific is the fastest-growing region at 8.70% CAGR, propelled by China’s 2060 carbon-neutral pledge and India’s expansive solar auction pipeline. Singapore positions itself as a gateway for regional capital flows, offering tax incentives for impact fund domiciliation and collaborating with multilaterals on blended-finance platforms. Japan’s aging demographic drives healthcare investments, while South Korea’s Green New Deal channels fiscal stimulus into smart-grid upgrades. Currency volatility remains a challenge, but bilateral swap lines and multilateral guarantees are mitigating FX risk. As regulatory frameworks improve, Asia Pacific could account for nearly a quarter of global allocations by 2031, reshaping the centre of gravity within the impact investing market.

North America maintains steady growth underpinned by large pension funds that now integrate climate risk into fiduciary duty interpretations. The United States still grapples with political polarisation over ESG, yet state-level policies and corporate net-zero commitments sustain underlying demand. Canada leads in clarity, with regulators publishing guidance that aligns impact objectives with solvency requirements for pension plans. Mexico’s nascent green-bond market attracts cross-border investors seeking diversification with impact credentials, though liquidity remains episodic. As private-equity style structures proliferate, the region’s share of the impact investing market is expected to remain stable, with upside contingent on harmonised federal disclosure mandates.

Competitive Landscape

In 2024, the top five managers oversaw only a portion of the assets, highlighting a fragmented landscape abundant in specialized franchises. BlackRock’s acquisitions of Global Infrastructure Partners and HPS Investment Partners represent an inorganic strategy aimed at bolstering in-house impact measurement and private-market expertise. The firm now integrates proprietary climate-risk analytics across all portfolios, signaling that impact considerations are no longer siloed products but core allocation filters. TPG Rise differentiates through an operational alpha model that ties carry to audited impact milestones, attracting limited partners comfortable with performance-linked economics. KKR Global Impact targets thematic clusters such as sustainable agriculture and circular economy, leveraging the parent platform’s deal-sourcing network for proprietary origination.

Technology is becoming a competitive moat. Managers deploy machine-learning engines to ingest satellite imagery, IoT sensors, and supply-chain ledgers, converting raw data into auditable impact dashboards presented to regulators and investors. Patent filings around automated impact validation rose 18% in 2024, indicating a race to secure intellectual property rights over verification algorithms. Tokenised fund shares grant early-mover platforms an edge in distribution, particularly among younger investors. Consolidation is expected to accelerate as bulge-bracket firms acquire boutiques to meet institutional mandate requirements without lengthy track-record incubation. Nevertheless, niche players that specialise in underserved geographies or thematic depths are likely to retain defensible positions by offering differentiated sourcing pipelines that large houses struggle to replicate.

Fee compression pressures are emerging, driven by institutional bargaining power and the commoditisation of basic ESG integration. Managers commanding outsized economics do so only when they demonstrate verified impact performance and differentiated data granularity. As regulator-mandated disclosures improve comparability, alpha will increasingly hinge on the ability to underwrite complex impact pathways rather than on traditional financial engineering alone. The competitive environment, therefore, rewards innovation in both measurement technology and structured finance, reinforcing the dynamic evolution of the impact investing market.

Impact Investing Industry Leaders

BlackRock

TPG Rise

LeapFrog Investments

Triodos Investment Management

Bridges Fund Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Triodos Investment Management launched a biodiversity restoration fund committing EUR 500 million to nature-based carbon projects.

- November 2024: Corporate venture capital arms executed USD 30 billion of secondary sales, indicating rising reliance on impact-focused liquidity solutions.

- October 2024: BlackRock finalized the operational integration of Global Infrastructure Partners, creating a combined USD 150 billion private-markets platform with enhanced impact analytics.

- September 2024: Vestmark partnered with BlackRock to embed impact screens in model portfolios available to the advisory network.

Global Impact Investing Market Report Scope

Impact investments involve financial choices with the dual objectives of delivering a financial return while also producing a measurable and beneficial social and environmental impact. Impact investing is segmented by type, end user, and region.

By type, the market is segmented into institutional and individual investors. By end user, the market is segmented into education, agriculture, healthcare, and climate tech. By region, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. The report offers market size and forecasts of the impact investing market in terms of value in USD for all the above segments.

| Private Equity |

| Private Debt |

| Natural and Real Assets |

| Public Equity and Debt |

| Cash & Cash Equivalents |

| Fund Structures & Others |

| Institutional Investors |

| Individual Investors |

| Renewable Energy |

| Sustainable Agriculture |

| Micro-finance & MSME Lending |

| Healthcare |

| Ed-Tech & Vocational Training |

| Sustainable Infrastructure |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Asset Class | Private Equity | |

| Private Debt | ||

| Natural and Real Assets | ||

| Public Equity and Debt | ||

| Cash & Cash Equivalents | ||

| Fund Structures & Others | ||

| By Investor Type | Institutional Investors | |

| Individual Investors | ||

| By End-Use Sector | Renewable Energy | |

| Sustainable Agriculture | ||

| Micro-finance & MSME Lending | ||

| Healthcare | ||

| Ed-Tech & Vocational Training | ||

| Sustainable Infrastructure | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the impact investing market?

The market stood at USD 1.57 trillion in 2026 and is projected to reach USD 2.19 trillion by 2031, translating into a 6.83% CAGR.

Which asset class is growing fastest within the impact investing market?

Private equity is expanding at 11.03% CAGR through 2031 because direct ownership allows fuller impact measurement and higher illiquidity premiums.

Why is Europe leading the impact investing market?

Europe commands 33.21% market share due to stringent disclosure mandates such as CSRD and a robust sovereign green-bond pipeline that channels capital into verified projects.

What restrains faster growth of impact investing?

Key headwinds include green-washing litigation risks that inflate compliance costs, shallow exit markets that lengthen holding periods, data gaps in developing economies, and higher interest rates that limit concessional funding pools.

How are retail investors accessing impact opportunities?

Digital platforms enable fractional ownership of tokenised funds and offer automated impact screening, driving a 10.38% CAGR in individual investor participation.

Which sector shows the highest growth potential?

Sustainable agriculture leads with 9.33% CAGR through 2031 as investors finance resilient food systems and climate-smart farming initiatives.

Page last updated on: