High Altitude Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

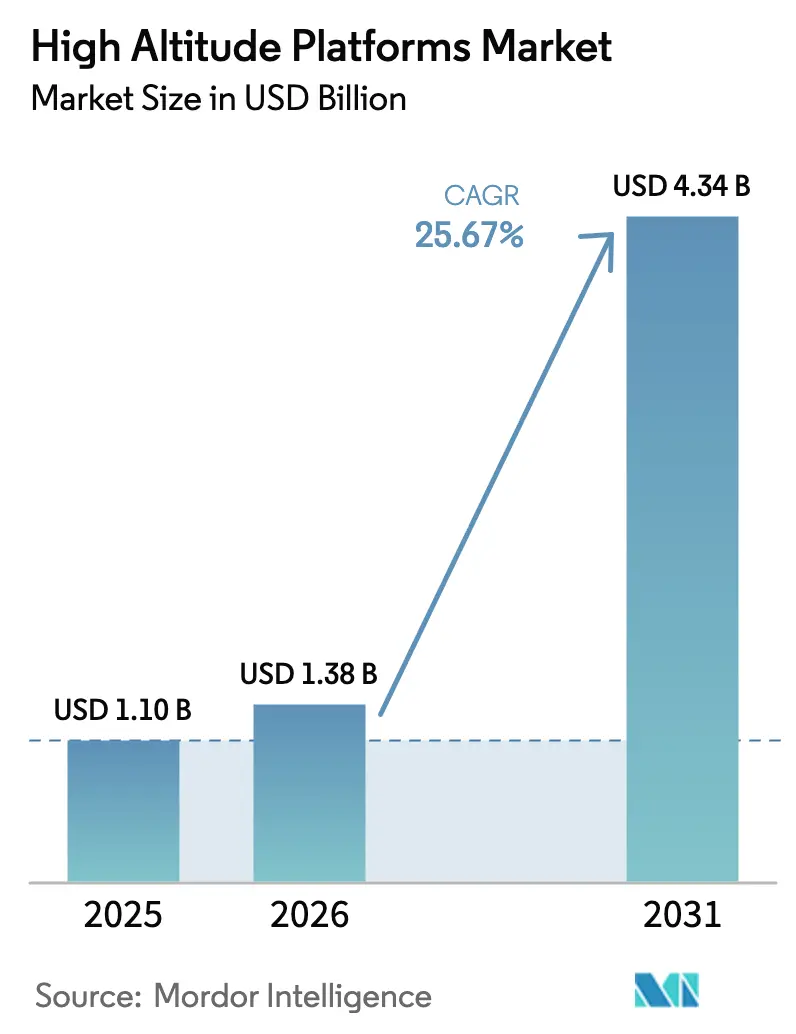

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 25.67% CAGR |

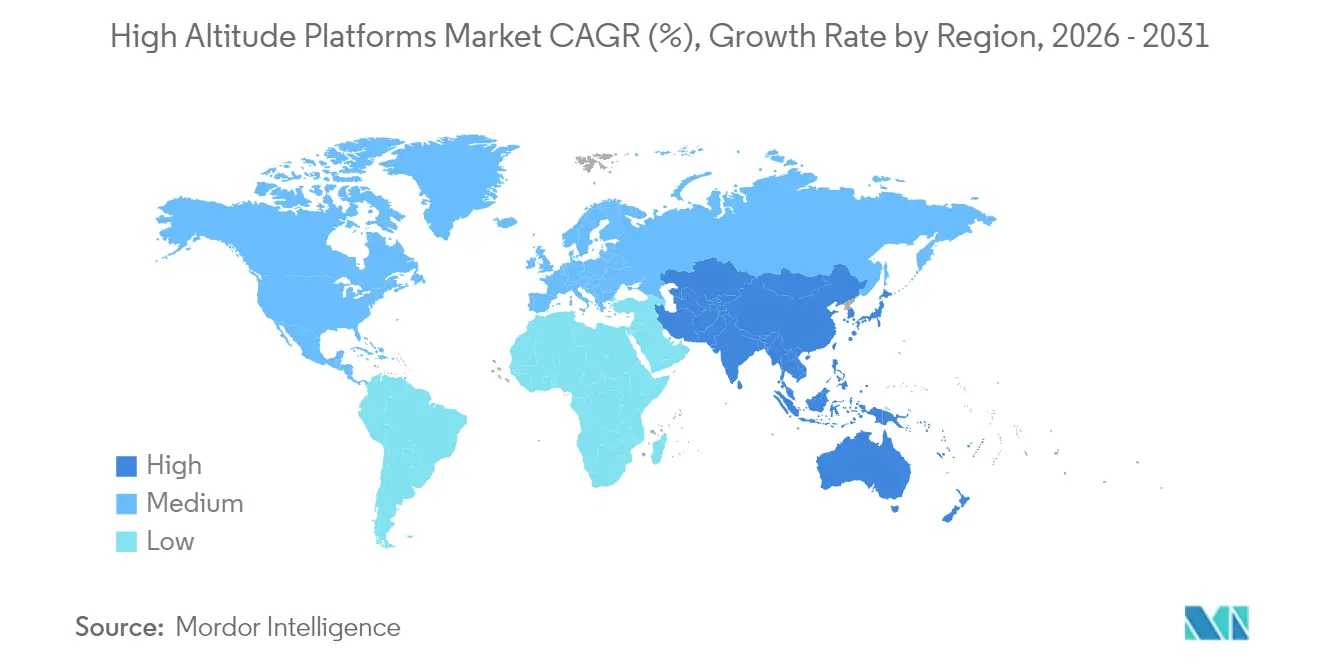

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Altitude Platforms Market Analysis by Mordor Intelligence

The high-altitude platforms market size in 2026 is estimated at USD 1.38 billion, growing from 2025 value of USD 1.1 billion with 2031 projections showing USD 4.34 billion, growing at 25.67% CAGR over 2026-2031. Two structural forces, rapid 5G densification and expanding climate-monitoring mandates, give platform operators a clear growth runway. Telecom carriers see stratospheric relays as a rapid way to fill rural coverage gaps, whereas government agencies rely on persistent sensing for defense, environmental, and emergency missions. Endurance breakthroughs in solar-powered airframes lower operating costs, and an emerging software layer converts raw flight data into actionable insights, both of which enhance the return on investment for commercial buyers. Hardware designs once limited to demonstrations are now entering certified production runs, a transition hastened by defense programs that absorb early development risk. Consolidation is underway as aerospace primes acquire nimble start-ups to secure intellectual property and accelerate platform certification.

Key Report Takeaways

- By platform type, solar-powered fixed-wing UAVs led with 45.62% of the high altitude platforms market share in 2025, while hybrid airships recorded the fastest 27.15% CAGR through 2031.

- By application, telecommunications and 5G backhaul captured 38.05% of the high-altitude platforms market size in 2025, whereas environmental and climate monitoring is growing at a 27.20% CAGR to 2031.

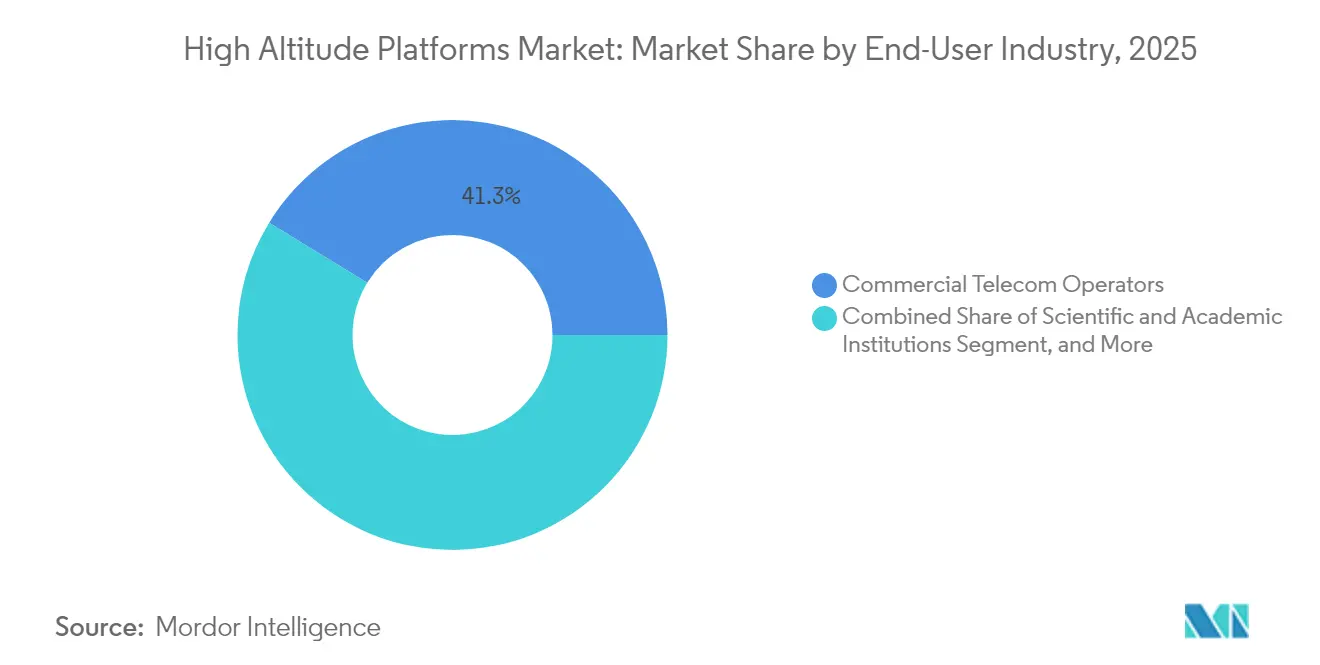

- By end-user, commercial telecom operators held a 41.25% revenue share in 2025, and scientific institutions are expected to expand at a 28.40% CAGR through 2031.

- By component, air-vehicle hardware accounted for 31.85% of 2025 spending; however, software and analytics services are projected to grow at a 28.05% CAGR to 2031.

- By geography, North America accounted for 35.05% of the revenue in 2025, and the Asia-Pacific region is projected to advance at a 28.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Altitude Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G/6G coverage expansion needs | +4.20% | Global, with early gains in North America and Asia-Pacific | Short term (≤ 2 years) |

| Surge in ISR demand for contested airspace | +3.80% | North America and Europe, spill-over to Middle East | Medium term (2-4 years) |

| Lower-cost persistent EO/remote-sensing alternatives | +3.10% | Global, with early adoption in scientific institutions | Medium term (2-4 years) |

| Advances in high-density solar and battery tech | +2.90% | Global, with manufacturing concentration in Asia-Pacific | Long term (≥ 4 years) |

| Regulatory green-lighting of stratospheric spectrum | +2.70% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Climate-change monitoring mandates | +2.40% | Global, with emphasis on Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G 6G coverage expansion needs

Mobile operators must close rural gaps without building fiber backhaul, so they adopt stratospheric relays that deliver direct-to-device signals, thereby reducing tower budgets. NTT DOCOMO’s USD 100 million equity stake in AALTO HAPS exemplifies carrier-led funding that accelerates commercial service launch.[1]Peter B. de Selding, “Stratospheric-platform startup AALTO raises USD 100 million,” SpaceIntelReport, Jun 3 2024, spaceintelreport.comIndonesian tower firm Mitratel is planning similar deployments, an early indicator that emerging markets will leapfrog straight to airborne backhaul. The business case strengthens as solar systems cut energy costs and cloud orchestration automates flight paths, allowing operators to scale nationally with fewer ground crews. With the spectrum now allocated under ITU WRC-23 rules, carriers have regulatory clarity to enter into long-term service contracts. Together, these factors position stratospheric systems as the lowest dollar-per-bit approach for remote coverage over the next two years.

Surge in ISR demand for contested airspace

Defense ministries require persistent sensing above missile engagement ceilings yet beneath satellite orbits. The US Army HADES and UK Project Aether programs supply that capability by funding year-long demonstrations of multi-sensor payloads that identify electronic emitters in denied zones. Stratospheric dwell time surpasses that of traditional UAVs, extending mission windows to weeks, which reduces sortie counts and crew fatigue. Militaries also value the lower signature relative to low-Earth orbit satellites, which limits detection by adversaries. NATO allies have responded by co-funding EuroHAPS, a EUR 43 million hybrid airship initiative, which spreads the R&D cost across 21 partners and aims to create shared standards for secure communications links. These moves will lift procurement volumes through the medium term.

Lower cost persistent EO and remote sensing alternatives

Research agencies and disaster-response groups need near-continuous imagery but cannot afford large satellite constellations. Sceye’s agreement with NASA and USGS illustrates how a single stratospheric vehicle can deliver high-resolution data at a fraction of the cost of satellite revisits.[2]Sceye, “Sceye Partners with NASA and USGS,” Sceye, Nov 7 2024, sceye.com Continuous presence enables methane leak detection, wildfire tracking, and glacier retreat measurement, producing environmental intelligence that satellites capture only every several days. Because the platform can remain stationary above a region for weeks, it reduces data gaps during cloudy periods that hinder optical satellite collection. Procurement appetite therefore rises among public climate programs and insurance firms that price weather risk, fueling adoption in the next four years.

Advances in high-density solar and battery technology

New photovoltaic cells exceed 30% efficiency, and lithium-sulfur batteries boast double the previous energy density, enabling platforms to harvest and store power that covers overnight cycles. Sceye’s 2024 diurnal flight demonstrated continuous stratospheric station-keeping without fuel, a milestone that eliminates recurring refueling trips and halves operating expenses.[3]Sceye, “Future of Non-Terrestrial Infrastructure,” Sceye, Sep 20 2024, sceye.com Efficient power means heavier payloads or longer loiter with no weight penalty. Component suppliers clustered in Japan, South Korea, and China are scaling up cell production, which is expected to reduce the per-watt cost by 15% in the long term. These gains broaden mission profiles from simple relay to complex multi-sensor operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stratospheric platform reliability and survivability issues | -2.80% | Global, with higher impact in harsh climate regions | Medium term (2-4 years) |

| ATC and spectrum interference concerns | -2.10% | Global, with regulatory complexity in dense airspace regions | Short term (≤ 2 years) |

| High upfront CAPEX versus satellites and LEO constellations | -1.90% | Global, with cost sensitivity in emerging markets | Medium term (2-4 years) |

| Skills shortage in stratospheric flight operations | -1.60% | Global, with acute shortages in specialized technical roles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stratospheric platform reliability and survivability issues

Extreme cold, radiation, and jet-stream turbulence stress airframes beyond the typical design limits of a UAV. Unplanned descents result in total asset loss, so insurers charge steep premiums, thereby raising entry barriers. Operators combat this by adding redundancies; however, extra weight reduces payload margin and delays certification. Reliability records remain sparse, which keeps some commercial customers waiting until multi-year performance data emerges, moderating adoption in the medium term.

ATC and spectrum interference concerns

Civil aviation authorities must integrate slow-moving platforms that hover above 60,000 ft yet share vertical lanes with ascent and descent paths. The FCC declined to issue dedicated HAPS rules in the 70, 80, and 90 GHz bands, making proponents rely on ad-hoc waivers that extend approval timelines.[4]Federal Communications Commission, “Modernizing 70 80 90 GHz Bands,” Federal Register, Apr 29 2024, federalregister.gov Coordinating spectrum with existing services requires complex studies and international notifications, consuming resources and introducing schedule risk for early deployments. Until a harmonized framework matures, some geographies impose tight corridor restrictions, limiting platform coverage areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Solar power drives endurance revolution

Solar-powered fixed-wing aircraft generated the largest contribution to the high-altitude platforms market size in 2025, accounting for 45.62% of the revenue due to their multiday endurance and lower energy costs. Airbus Zephyr demonstrated several 25-day flights, convincing telecom operators that a month-long loiter is commercially viable. The Zephyr and BAE PHASA-35 lines have entered low-rate production, resulting in a falling unit price as suppliers scale up composite wing fabrication. The hybrid airship subcategory is the fastest-growing, with a 27.15% CAGR, as buoyant lift supports heavier multi-sensor arrays, benefiting ISR missions that require wide-aperture radar. Thales Stratobus and the EuroHAPS demonstrator each carry a payload of over 250 kg, making them attractive for government science programs. Over the forecast, solar fixed-wing craft will remain volume leaders, while hybrid airships capture niche heavy-lift demand that satellites cannot meet.

Platform selection now hinges on flight duration, payload mass, and regulatory path. Solar designs clear environmental tests more quickly because they produce zero emissions and a minimal acoustic footprint, factors that shorten permitting cycles in protected habitats. Hybrid airships accept slower certification progress in exchange for unmatched lift, allowing bundled telecom and radar payloads on a single hull. Aerostat and balloon demand holds steady for line-of-sight video and weather sonde work, but lacks the growth trajectory seen in uncrewed aircraft.

By Application: Climate monitoring accelerates beyond connectivity

Telecommunications still accounted for 38.05% of the high-altitude platforms market share in 2025, reflecting the urgent need for 5G backhaul in areas where terrestrial towers are blocked. Direct-to-device trials in Indonesia and Mexico validated the service model, and roaming agreements with satellite operators reduce risk for mobile carriers. Even so, environmental and climate monitoring is expanding at the fastest rate, with a 27.20% CAGR, underwritten by public funding that rewards high temporal resolution. Government climate acts in the United States and the European Union earmark grants for methane plume mapping and wildfire early warning, missions that stratospheric craft perform better than polar satellites due to their continuous dwell.

ISR remains integral, especially for maritime border surveillance, where long stares simplify vessel identification. Earth-observation imagery gains from onboard edge processors that compress data before downlink, saving bandwidth. Precision navigation remains small yet strategic, providing timing backup in GNSS-degraded zones. As mission diversity widens, service providers bundle multi-tenant payloads, squeezing extra revenue per airframe.

By End-User Industry: Scientific institutions drive innovation

Commercial telecom operators led spending at 41.25% in 2025, driven by the lower total cost of ownership compared to fiber in sparsely populated zones. They sign multi-year capacity leases that help platform firms secure construction debt. Scientific and academic institutions post a 28.40% CAGR because grants now prioritize sustained atmospheric chemistry sampling and greenhouse gas mapping. Sceye’s deal with USGS showcases the model, pairing a public research mission with a private platform provider.

Defense and homeland security customers remain steadier buyers, favoring ruggedized airframes and secure datalinks. Government disaster-response agencies also utilize stratospheric vehicles for post-hurricane communications restoration, capitalizing on their fast launch and relocation capabilities. This broadened end-user mix insulates suppliers from swings in any single sector and pulls forward software development tailored to varied payloads.

By Component: Software analytics transforms value creation

Air-vehicle hardware still dominated 2025 spending at 31.85%, but growth decelerated as design cycles stabilized and parts transitioned to repeatable manufacturing. Software and analytics services are projected to rise 28.05% per year, transforming sensor output into products such as methane heatmaps or spectrum congestion dashboards. The high-altitude platforms market size for software climbed sharply after Aerostar released its Thunderstorm mission-planning suite, which automates route updates based on weather feeds.

Payload instruments shrink yet gain resolution, letting operators swap cameras for synthetic aperture radar mid-mission through modular bays. Power and propulsion gains emerge from lightweight gallium-arsenide panels and lithium-sulfur packs sourced in Japan and South Korea. Ground control shifts to cloud hosts, reducing fixed assets at operator sites and enabling remote crew scheduling.

Geography Analysis

North America generated 35.05% of 2025 revenue, driven by US defense RDT&E contracts and Federal Communications Commission experimental licenses that mitigate spectrum use risks. The National Spectrum Strategy Implementation Plan earmarked studies for dynamic sharing that explicitly mention stratospheric systems. Sceye secured a USD 525 million valuation on its Series C round, indicating investor confidence in the region. Canada supports wildfire monitoring missions over boreal forests, and Mexico evaluates telecom coverage along coastal corridors. Robust aerospace supply chains in Arizona, Alabama, and Quebec ensure quick turnaround for program modifications.

The Asia-Pacific region is the fastest-growing arena, with a 28.90% CAGR. Japanese consortium funding of AALTO HAPS and South Korea’s Spectrum Plan 2024-2027, which reserves bands for experimental flights, reinforces a supportive policy environment. China’s broader low-altitude economy strategy lists hybrid airship corridors in Guangdong and Hainan, while India negotiates technology transfer agreements for joint platform assembly. Island nations such as Indonesia seek immediate telecom benefits, and their geography makes stratospheric deployments more economical than subsea cable spurs.

Europe sustains steady uptake anchored by the EuroHAPS project and the United Kingdom’s Project Aether. The European Union's Green Deal objectives emphasize the importance of continuous environmental data, and the European Union Aviation Safety Agency collaborates on common airworthiness guidance, streamlining multi-country missions. Germany’s DLR validated wildfire imaging with its MACS-HAP camera over Greece in 2024, hinting at commercial demand for agricultural analytics. Collaborative procurement pools demand across smaller states, giving suppliers a larger combined addressable market.

Competitive Landscape

The market exhibits moderate fragmentation, although acquisition momentum is increasing. Airbus spun out AALTO to draw external capital while retaining design leverage. Thales Alenia Space partners with L-band satellite operator Inmarsat to layer stratospheric repeaters onto existing orbital fleets. AeroVironment integrates edge AI chips from Qualcomm to differentiate on onboard processing.

Technology competition centers on endurance and payload flexibility. New entrants like Sceye use proprietary laminated composite envelopes that reduce mass and deliver month-long station-keeping, challenging legacy airframes built from aluminum spars. Software capabilities are now decisive, and vendors that marry flight control, data fusion, and API access garner premium contracts.

Joint ventures proliferate to bridge the skill sets of the aerospace and telecom industries. Raven Industries and Nokia collaborated on a prototype direct-to-device link that achieved 50 Mbps downstream over rural South Dakota, demonstrating that multidisciplinary expertise yields faster commercialization. Suppliers unable to offer integrated solutions risk being excluded from the growth tier and becoming component subcontractors.

High Altitude Platforms Industry Leaders

Airbus Defence and Space GmbH

Thales Alenia Space France SAS

AeroVironment, Inc.

HAPSMobile Inc.

Sceye Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Sceye signed a partnership with NASA and USGS to deliver high-resolution climate data, leveraging stratospheric persistence to map methane super-emitters, which expands its environmental client base.

- October 2024: Mira Aerospace unveiled two stratospheric payloads targeting Middle East deployments, signaling geographic expansion and diversification beyond telecom into environmental imaging.

- September 2024: Sceye completed a renewable-energy-powered diurnal flight, eliminating refueling cycles and validating indefinite loiter, a key milestone for achieving cost parity with satellites.

- June 2024: AALTO HAPS secured USD 100 million from a Japanese consortium led by NTT DOCOMO, funding commercial service trials in Asia. The deal grants carriers early access to backhaul capacity, positioning AALTO for rapid market entry.

Global High Altitude Platforms Market Report Scope

| Solar-Powered Fixed-Wing UAV |

| Tethered Aerostat |

| Un-tethered Balloon |

| Hybrid Airship |

| Telecommunications and 5G Backhaul |

| Intelligence, Surveillance and Reconnaissance (ISR) |

| Earth Observation and Remote Sensing |

| Environmental and Climate Monitoring |

| Navigation and Positioning |

| Commercial Telecom Operators |

| Defense and Homeland Security Agencies |

| Government and Public Safety |

| Scientific and Academic Institutions |

| Platform Air-Vehicle Hardware |

| Payload Instruments |

| Power and Propulsion Systems |

| Ground Control Stations |

| Software and Analytics Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform Type | Solar-Powered Fixed-Wing UAV | ||

| Tethered Aerostat | |||

| Un-tethered Balloon | |||

| Hybrid Airship | |||

| By Application | Telecommunications and 5G Backhaul | ||

| Intelligence, Surveillance and Reconnaissance (ISR) | |||

| Earth Observation and Remote Sensing | |||

| Environmental and Climate Monitoring | |||

| Navigation and Positioning | |||

| By End-User Industry | Commercial Telecom Operators | ||

| Defense and Homeland Security Agencies | |||

| Government and Public Safety | |||

| Scientific and Academic Institutions | |||

| By Component | Platform Air-Vehicle Hardware | ||

| Payload Instruments | |||

| Power and Propulsion Systems | |||

| Ground Control Stations | |||

| Software and Analytics Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the high altitude platforms market?

The high altitude platforms market size is USD 1.38 billion in 2026.

How fast is the market expected to grow by 2031?

The market is forecast to expand to USD 4.34 billion by 2031, reflecting a 25.67% CAGR.

Which application area is projected to grow the quickest?

Environmental and climate monitoring is advancing at 27.20% CAGR to 2031.

Which region will see the highest growth?

Asia-Pacific leads with a 28.90% CAGR through 2031.

Who are the leading companies in this space?

Airbus Defence and Space, Thales Alenia Space, AeroVironment, Sceye, and AALTO HAPS are prominent players with varied platform offerings.

Why are telecom operators investing in stratospheric systems?

Stratospheric platforms deliver 5G coverage over remote areas at lower cost than terrestrial towers and avoid the need for expensive fiber backhaul.

Page last updated on: