Heated Humidifiers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

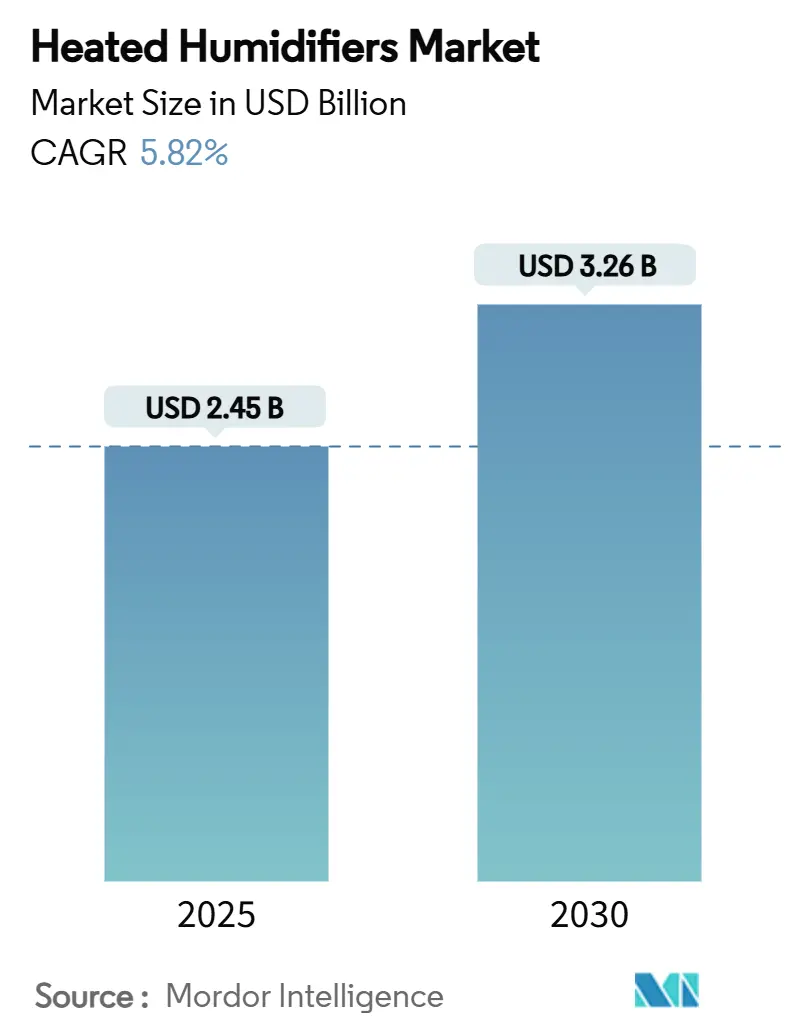

| Market Size (2025) | USD 2.45 Billion |

| Market Size (2030) | USD 3.26 Billion |

| Growth Rate (2025 - 2030) | 5.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heated Humidifiers Market Analysis by Mordor Intelligence

The heated humidifiers market size reached USD 2.45 billion in 2025 and is forecast to climb to USD 3.26 billion by 2030, advancing at a 5.82% CAGR. This expansion reflects the importance of precision-controlled moisture delivery in ventilatory care, especially as hospitals and home-care providers seek to cut infection rates, improve patient comfort, and align with decarbonization targets. Widening COPD and sleep-apnea prevalence, accelerated ventilator installations after COVID-19, and the spread of AI-enabled closed-loop systems collectively sustain demand. Regional momentum differs: North America leads on reimbursement depth, Europe on decarbonization mandates, and Asia-Pacific on rising disease burden. Competition remains moderate because core heating technology is mature, yet supply-chain strains around medical-grade nichrome raise switching costs and spur innovation in ultrasonic alternatives. Home-care reimbursement revisions and hospital infection-control protocols anchor long-term opportunities.

Key Report Takeaways

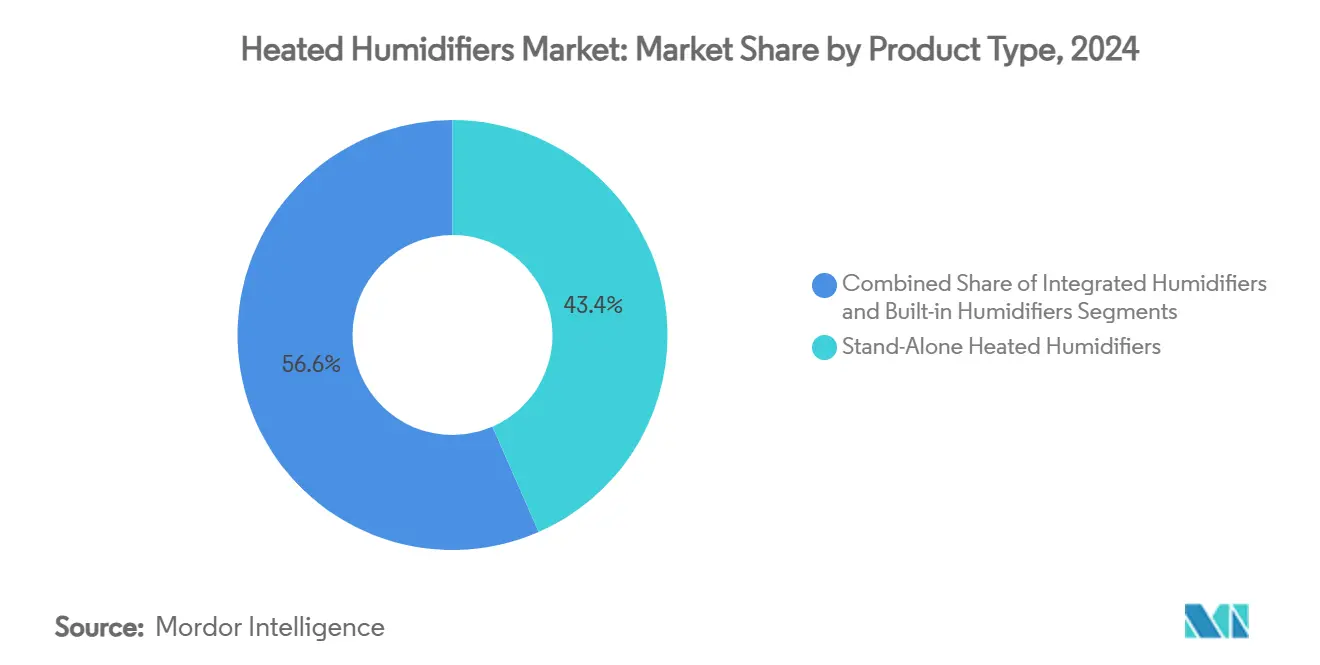

- By product type, stand-alone heated humidifiers led with 43.44% of the heated humidifiers market share in 2024 while integrated units are projected to expand at a 9.63% CAGR to 2030.

- By respiratory support modality, invasive ventilation accounted for 47.83% share of the heated humidifiers market size in 2024; high-flow nasal cannula/non-invasive ventilation is forecast to post an 8.33% CAGR through 2030.

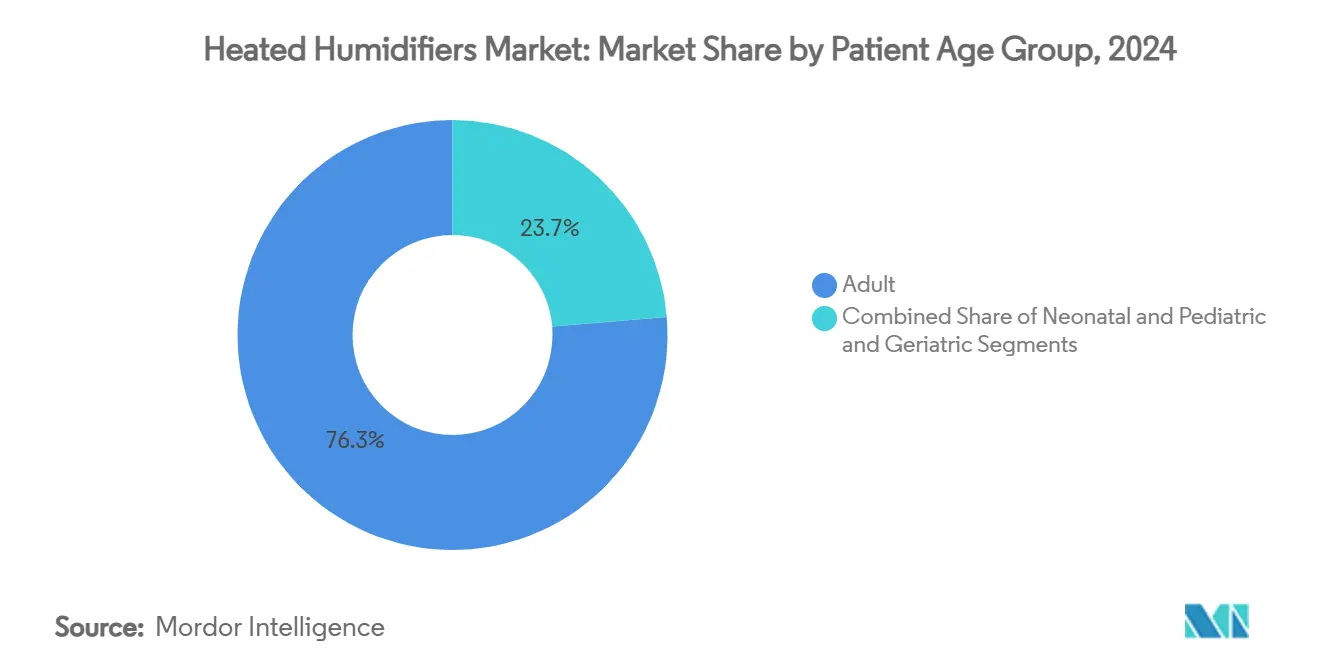

- By patient age group, adults held 76.34% share of the heated humidifiers market size in 2024, while geriatric demand is expected to grow at 7.12% CAGR between 2025-2030.

- By end user, hospitals captured 66.86% revenue share in 2024; home-care settings are advancing at an 8.47% CAGR through 2030 thanks to wider reimbursement and connected-device adoption.

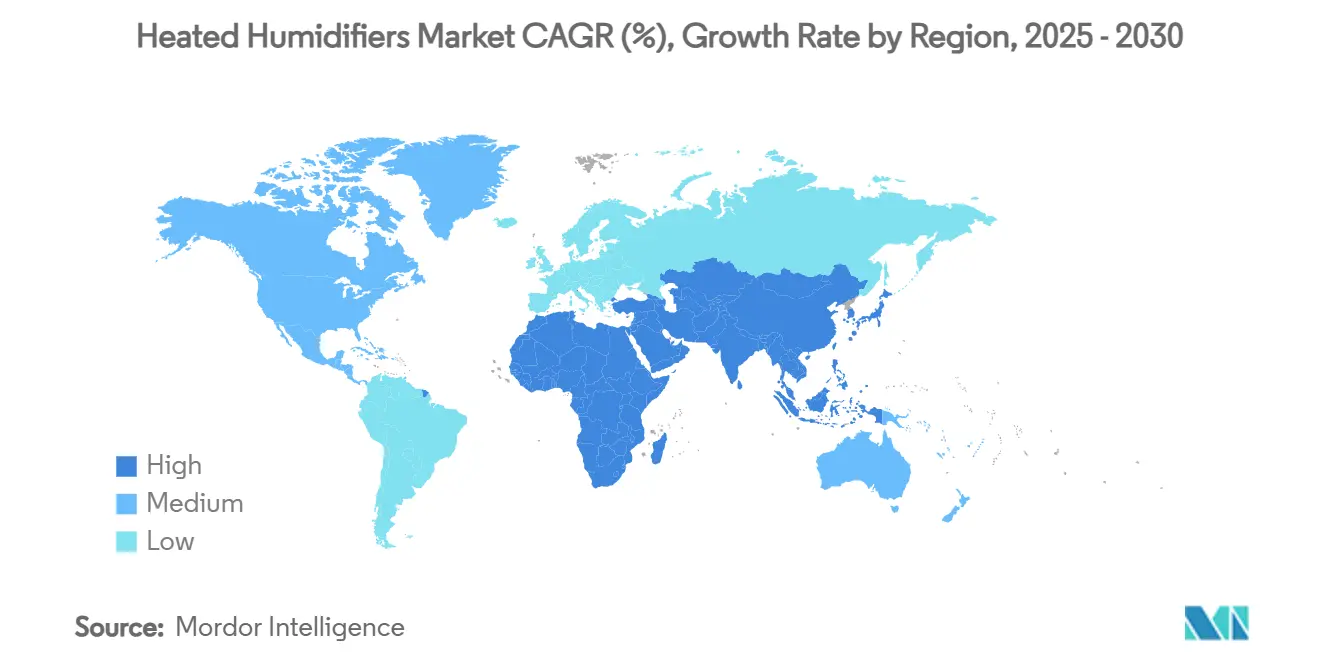

- By geography, North America retained a 38.25% share in 2024, whereas Asia-Pacific is projected to register a 7.18% CAGR to 2030 on the back of expanded healthcare access.

Global Heated Humidifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COPD & sleep-apnea surge raises ICU and CPAP demand | +1.2% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Post-COVID ventilator and HFNC adoption | +0.8% | Global with emphasis on APAC | Medium term (2-4 years) |

| Home-care reimbursement expansion | +0.6% | North America, Europe, spreading to APAC | Medium term (2-4 years) |

| Hospitals shift to integrated humidification | +0.7% | Developed healthcare systems | Short term (≤ 2 years) |

| Energy-efficient ultrasonic heating | +0.4% | Europe, North America, global rollout | Long term (≥ 4 years) |

| AI-assisted closed-loop humidification | +0.5% | North America, Europe, early APAC uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of COPD & Sleep-Apnea Cases Driving ICU and CPAP Installations

Global COPD and sleep-apnea prevalence elevates demand for heated humidifiers across hospitals and homes. Roughly 1 billion people now suffer from obstructive sleep-apnea, expanding the addressable base beyond acute-care environments.[1]Tetyana Kendzerska, “Epidemiology of Obstructive Sleep Apnea,” Journal of Clinical Medicine, mdpi.com ResMed logged 11% revenue growth in Q1 2025 as sleep-device uptake rose, underscoring how home-sleep therapy feeds equipment purchases. AI-driven COPD screening in primary care enables earlier intervention, channeling more patients toward long-term humidification therapy. Continuous-operation capability and clinical-grade performance have become minimum design expectations, especially for aging demographics.

Surge in Ventilator and HFNC Adoption Post-COVID-19

The pandemic permanently altered ventilatory practice. High-flow nasal cannula therapy, which humidifies oxygen to enhance mucociliary clearance, cut intubation rates and shortened ICU stays, prompting sustained procurement of integrated humidification modules.[2]Ernesto Escalante, “High-Flow Nasal Cannula in COVID-19: A Literature Review,” Canadian Journal of Respiratory Therapy, pubmed.govHospitals now bake surge-capacity planning into capital budgets, specifying scalable humidification infrastructure that can serve both invasive and non-invasive modalities.[3]Chunxia Wang, “High-Flow Nasal Cannula Oxygen Therapy: Physiological Mechanisms and Clinical Applications in Children,” Frontiers in Medicine, frontiersin.org

Expansion of Home-Based Respiratory Care Reimbursement Frameworks

US Medicare and several private payers added new billing codes for home respiratory equipment in 2025, explicitly covering advanced humidification devices that meet defined efficacy standards. Fisher & Paykel’s F&P my820 launch aims directly at this segment, pairing hospital-grade humidification with consumer-friendly controls. Improved reimbursement also supports pulmonary rehabilitation in rural areas, pushing manufacturers to develop rugged, low-maintenance units.

Hospital Shift Toward Integrated Humidification to Cut Circuit-Related Infection Costs

Randomized trials show heated humidifiers lower ventilator-associated pneumonia incidence to 15.69% versus 39.62% for HMEs, translating into USD 40,000 saved per avoided case. Real-time monitoring and automated condensate handling align with value-based-care incentives, accelerating replacement of passive HMEs in high-acuity wards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher device & consumable cost vs HMEs | -0.9% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Condensate-associated infection-control workload | -0.5% | Global, acute in resource-limited sites | Medium term (2-4 years) |

| Green-hospital initiatives favor passive units in low-acuity wards | -0.3% | Europe & North America, growing global | Long term (≥ 4 years) |

| Tight supply of medical-grade nichrome heating elements | -0.7% | Global, all manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Device & Consumable Cost Versus Heat-Moisture Exchangers (HMEs)

A pivotal randomized trial found heated-water humidification cost USD 5,625 per patient versus USD 2,605 for HMEs, steering budget-constrained buyers toward passive options. Inflation-driven materials surcharges now absorb up to 20% of revenue for some ventilator manufacturers, intensifying price sensitivity in emerging markets.

Condensate-Associated Infection-Control Workload

Active humidification produces condensate that must be drained to prevent bacterial growth. In understaffed ICUs this maintenance burden diverts clinical resources, slowing replacement of HMEs despite better moisture delivery. Automated drainage features are under development but add upfront cost and regulatory complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stand-Alone Units Dominate Amid Integration Push

Stand-alone units generated 43.44% of heated humidifiers market share in 2024. Hospitals value their plug-and-play nature and ability to retrofit legacy ventilators without major capital outlay. Integrated models are poised to post a 9.63% CAGR as ICU remodels emphasize workflow simplification. Built-in humidifiers maintain demand for transport and emergency carts where footprint matters. Stand-alone vendors highlight cross-device compatibility, whereas integrated-platform suppliers stress closed-loop automation and infection-control compliance.

Growth reflects a balancing act between flexibility and efficiency. Clinicians welcome unified touchscreens and fewer tubing connections because these cut setup time and error risk. Yet multi-specialty hospitals still stock stand-alone pools for neonatal, adult, and transport overlaps. Pricing strategy increasingly hinges on software features—temperature presets, adaptive alarms, and EMR connectivity—that raise perceived value while masking hardware commoditization.

By Respiratory Support Modality: Invasive Ventilation Leads, HFNC Accelerates

Invasive ventilation captured 47.83% share of the heated humidifiers market size in 2024 as long-duration intubations mandate active humidification to curb mucosal injury. High-flow nasal cannula and non-invasive ventilation collectively are set for an 8.33% CAGR, buoyed by workflow alignment with early-intervention protocols during COVID-19 peaks. CPAP/BiPAP continues steady expansion in sleep therapy, and anaesthesia/transport niches prize compactness and battery endurance.

Clinical protocols now escalate patients from HFNC to invasive only when oxygenation goals fail, expanding the installed base of humidifiers that can toggle between modes. Manufacturers differentiate through modality-specific disposables—dual-heating wires for HFNC, low-volume chambers for paediatrics. Reimbursement coding clarity for HFNC in many OECD countries further accelerates adoption.

By Patient Age Group: Adult Dominance with Rapid Geriatric Upswing

Adults accounted for 76.34% of 2024 demand, yet geriatric usage will climb at 7.12% CAGR as comorbidity-laden seniors require prolonged respiratory support. Neonatal and paediatric segments, though smaller, compel high-precision controls to guard against airway injury. Device makers integrate algorithmic safeguards that cap humidity spikes, critical for fragile lung tissue in premature infants.

Population ageing magnifies home-therapy volumes; oxygen concentrator packages increasingly bundle humidifiers that auto-sanitize to reduce caregiver workload. In paediatrics, heated-humidified HFNC has proven effective in easing bronchiolitis, reinforcing guidelines that mandate active moisture in paediatric wards.

By End User: Hospitals Still Core, Home-Care Surges

Hospitals retained 66.86% of 2024 revenue, banking on ICU refresh cycles and infection-control mandates. The home-care channel, propelled by 8.47% CAGR, benefits from updated DMEPOS codes, cloud-linked compliance tracking, and consumer expectation of medical-grade comfort. Clinics and ASCs adopt mid-tier humidifiers to manage post-op respiratory support, while emergency services value shock-proof housings and low power draw.

Connected ecosystems top procurement wish-lists: cellular modems and API hooks allow respiratory therapists to adjust settings remotely, cutting readmissions. Manufacturers courting home-care add consumer-oriented UX—touch-glide controls, voice prompts—and quieter fans to minimize bedroom disruption.

Geography Analysis

North America’s installed base of ventilators underpins high replacement demand, and sustainability grants offset the capex of ultrasonic upgrades. Canada’s single-payer model now reimburses home CPAP humidifiers at par with hospital units, expanding residential uptake.

Asia-Pacific’s market leap mirrors rising COPD incidence tied to urban pollution and tobacco consumption. China links humidification adoption to Grade III hospital accreditation, while India’s Production Linked Incentive scheme subsidizes local assembly.

Europe pursues decarbonization; hospitals winning Green Deal funds must document annual kilowatt reductions, steering tenders toward ultrasonic or hybrid units. Latin America’s universal health programs in Brazil and Colombia purchase stand-alone units in bulk for ICU expansions, yet foreign-exchange swings challenge continuous supply.

Competitive Landscape

Fisher & Paykel Healthcare, ResMed, and Philips collectively control a substantial but far-from-dominant share, keeping the heated humidifiers market moderately fragmented. These leaders focus on integrated platforms that bundle humidification, filtration, and digital monitoring. ResMed spends 7% of revenue on R&D to fuse machine-learning algorithms with hardware, aiming for individualized humidity profiles. Fisher & Paykel leverages deep chamber design expertise and regulatory goodwill earned during pandemic ventilator shortages.

Mid-tier firms attack niches: Vapotherm targets transport and paediatrics, Hamilton Medical pushes AI-embedded ICU ventilators, and Carepod courts HSA/FSA shoppers seeking wellness-aligned devices. Supply chain upheaval favors larger players that can dual-source nichrome or pivot to ultrasonic modules quickly. Meanwhile Philips’ recall-driven shortfall in sleep-therapy devices has opened share gains for ResMed, Drive DeVilbiss, and regional brands.

M&A activity underscores strategic realignment. Teleflex’s vascular unit divestiture signals focus on high-growth respiratory lines, while Vyaire’s asset sales create white-space for disruptive startups. Software differentiation now counts as much as heating-element IP, shifting competitive battlegrounds toward firmware, cloud connectivity, and clinical-decision algorithms.

Heated Humidifiers Industry Leaders

Fisher & Paykel Healthcare

Koninklijke Philips N.V.

ResMed

Teleflex

Vapotherm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Carepod humidifiers became HSA/FSA eligible for U.S. consumers with qualifying conditions, broadening retail accessibility.

- February 2025: Vadi Medical introduced the VH-500 respiratory humidifier in Taiwan, featuring a dual-heating architecture for stable dew-point control.

- August 2024: Fisher & Paykel Healthcare released the F&P my820 System, its first purpose-built home mechanical-ventilation humidifier.

Global Heated Humidifiers Market Report Scope

| Stand-Alone Heated Humidifiers |

| Integrated Humidifiers |

| Built-in Humidifiers |

| Invasive Mechanical Ventilation |

| Non-Invasive Ventilation / HFNC |

| CPAP / BiPAP |

| Others (Anaesthesia, Transport) |

| Adult |

| Neonatal and Pediatric |

| Geriatric |

| Hospitals |

| Clinics & ASCs |

| Home-care Settings |

| Long-term Care Facilities |

| Emergency & Transport Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Stand-Alone Heated Humidifiers | |

| Integrated Humidifiers | ||

| Built-in Humidifiers | ||

| By Respiratory Support Modality | Invasive Mechanical Ventilation | |

| Non-Invasive Ventilation / HFNC | ||

| CPAP / BiPAP | ||

| Others (Anaesthesia, Transport) | ||

| By Patient Age Group | Adult | |

| Neonatal and Pediatric | ||

| Geriatric | ||

| By End User | Hospitals | |

| Clinics & ASCs | ||

| Home-care Settings | ||

| Long-term Care Facilities | ||

| Emergency & Transport Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the heated humidifiers market in 2030?

The heated humidifiers market is forecast to reach USD 3.26 billion by 2030 at a 5.82% CAGR.

Which product category currently leads sales?

Stand-alone units command the largest share at 43.44% because they retrofit easily with existing ventilators.

Why are ultrasonic humidifiers gaining attention?

They cut electricity use by about 93%, helping hospitals meet decarbonization targets without compromising performance.

How will home-care reimbursement changes influence demand?

New billing codes in the U.S. and Europe fund advanced home humidifiers, driving an expected 8.47% CAGR in the segment.

Which region is growing fastest?

Asia-Pacific is expanding at 7.18% CAGR thanks to wider healthcare access and rising respiratory disease prevalence.

What major restraint could slow adoption in cost-sensitive markets?

Higher upfront and consumable costs versus passive HMEs remain a significant barrier, particularly where budgets are tight.

Page last updated on: