Hairy Cell Leukemia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

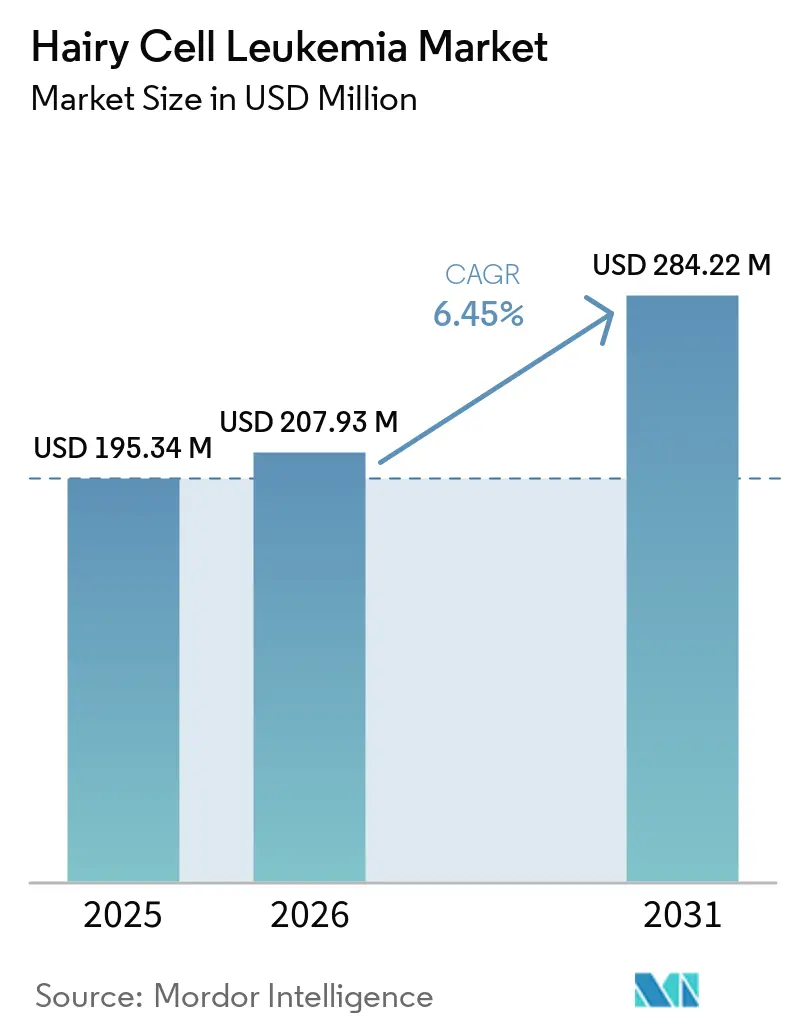

| Market Size (2026) | USD 207.93 Million |

| Market Size (2031) | USD 284.22 Million |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hairy Cell Leukemia Market Analysis by Mordor Intelligence

The Hairy Cell Leukemia Market size was valued at USD 195.34 million in 2025 and is estimated to grow from USD 207.93 million in 2026 to reach USD 284.22 million by 2031, at a CAGR of 6.45% during the forecast period (2026-2031).

Precision-oncology combinations focused on the BRAF V600E mutation are steadily replacing purine-analog monotherapy. Orphan-drug pricing flexibility continues to safeguard revenue despite the extremely small patient population. Clinical adoption is expanding due to advancements such as flow-cytometry minimal residual disease (MRD) monitoring, the reclassification of companion diagnostics, and the transition to a two-hour IV push administration of cladribine. North America remains the leader, supported by academic institutions, accelerated regulatory pathways, and payer alignment with off-label reimbursement guidelines. The Asia-Pacific region is advancing, driven by South Korea's planned expansion of hematology benefits in 2026 and China's upcoming update to its National Reimbursement Drug List in 2025, reflecting an increased willingness to cover ultra-rare therapies. However, ongoing supply shortages of fludarabine-based reagents and payer reluctance toward serial MRD testing present challenges to the otherwise positive growth trajectory.

Key Report Takeaways

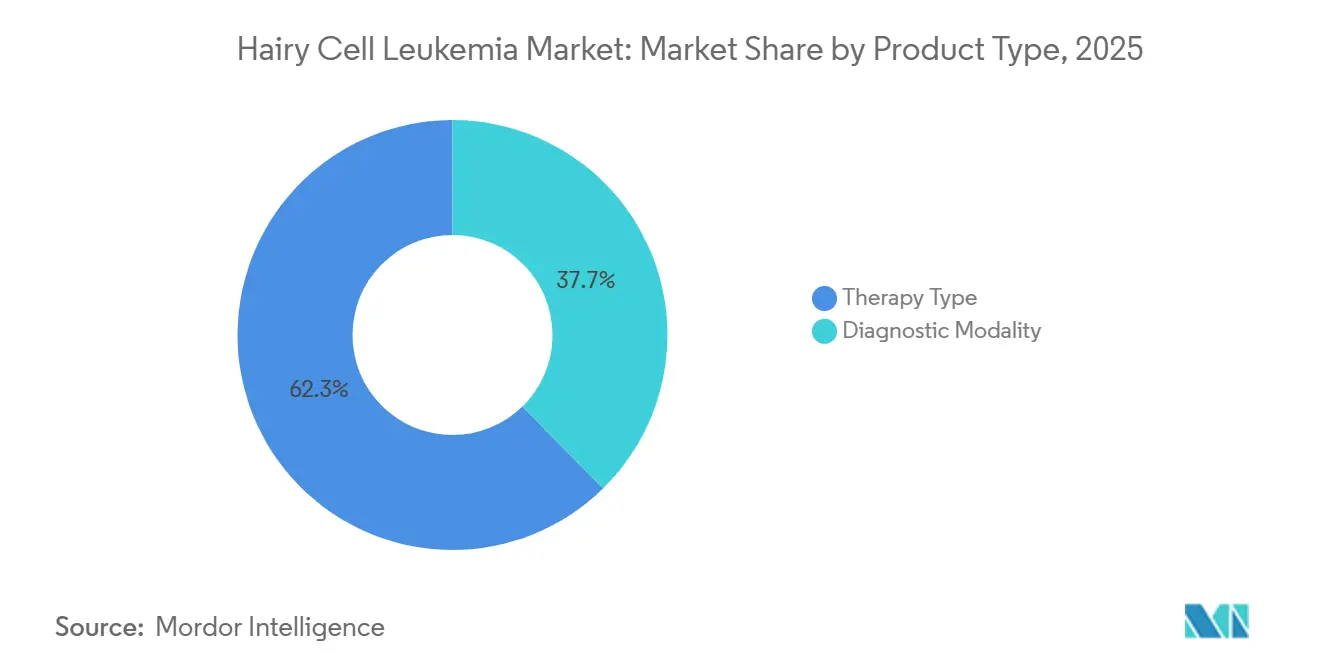

- By product category, therapy-type products led with 62.34% revenue share in 2025; diagnostic modalities are advancing at a 7.79% CAGR through 2031.

- By route of administration, intravenous delivery commanded 51.43% share of the hairy cell leukemia market size in 2025, while oral formulations are projected to expand at 7.96% CAGR over 2026-2031.

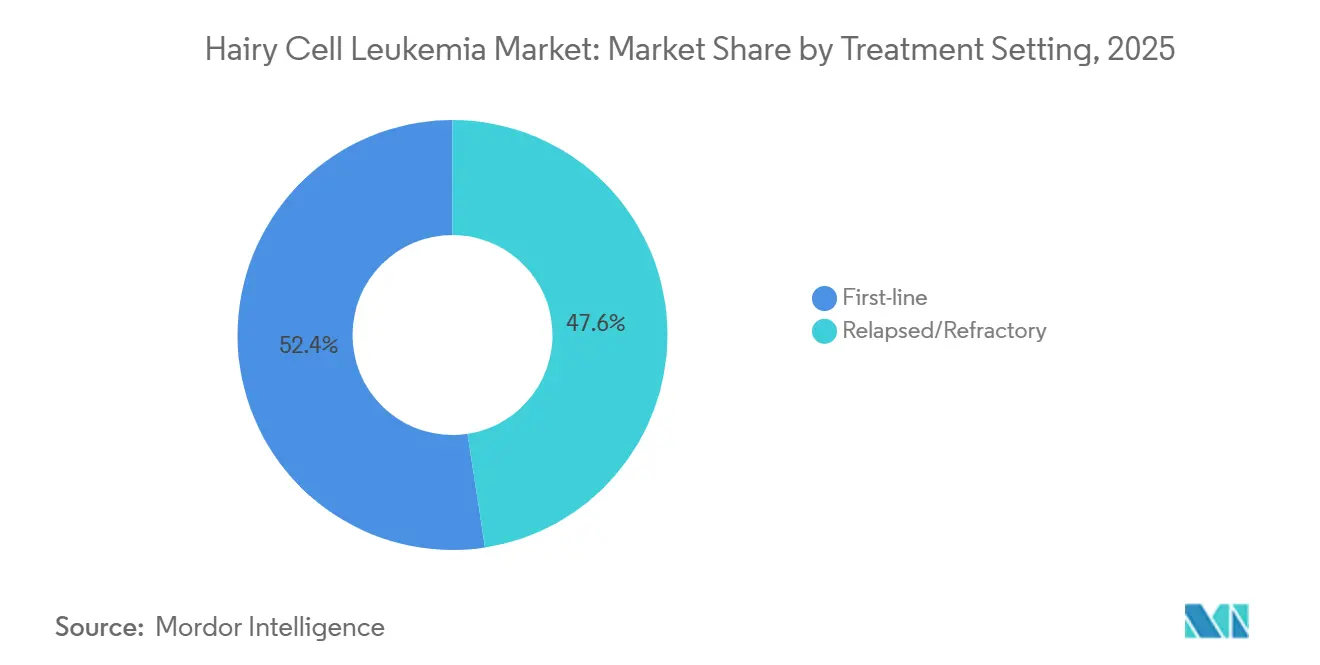

- By treatment setting, first-line therapy accounted for 52.41% of the hairy cell leukemia market share in 2025, and relapsed or refractory care is forecasted to grow at an 8.15% CAGR to 2031.

- By end user, hospitals held 55.45% share in 2025; diagnostic laboratories are projected to grow at a 7.89% CAGR through 2031.

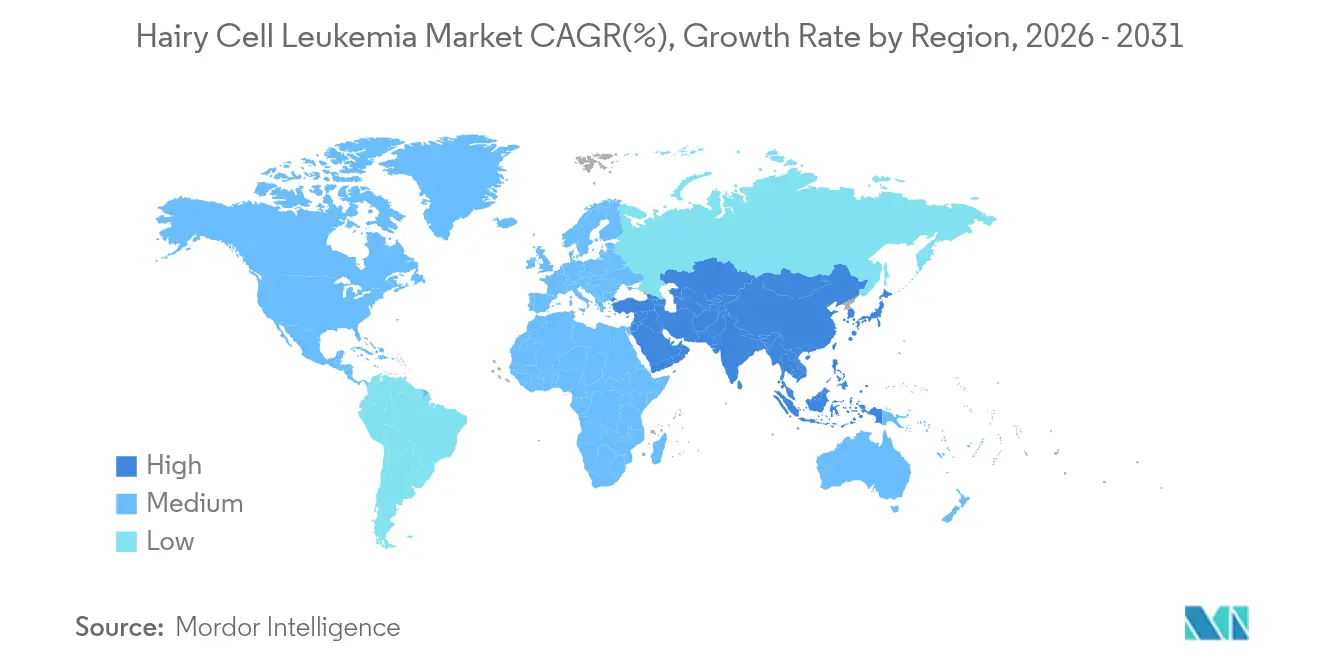

- By geography, North America captured 39.34% share in 2025, whereas the Asia-Pacific is projected to grow at 8.25% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hairy Cell Leukemia Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Wider adoption of MRD-guided retreatment | +1.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| BRAF V600E mutation-specific companion diagnostics | +1.5% | North America, EU core markets, Japan | Short term (≤ 2 years) |

| Rising incidence in ageing male population | +0.9% | Global, pronounced in North America and Europe | Long term (≥ 4 years) |

| Shift toward outpatient IV push formulations | +0.7% | North America, select EU markets | Medium term (2-4 years) |

| Orphan-drug pricing flexibility | +1.2% | North America, Germany, UK, Nordics | Short term (≤ 2 years) |

| AI-enabled digital pathology for rare cell detection | +0.6% | North America, Western Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MRD-Guided Retreatment Gains Traction

Bone-marrow MRD assays, capable of detecting BRAF V600E allele frequencies below 0.01%, are increasingly influencing the timing of salvage treatments. This advancement is reducing infection-related complications and lowering costs for pancytopenic patients. The adoption of Memorial Sloan Kettering’s Phase 2 protocol, which requires MRD assessment at six months, has accelerated this trend. Early intervention with targeted therapies is minimizing hospitalizations. However, the absence of standardized MRD cut-offs presents challenges in aligning with payer requirements. Draft guidance expected in late 2025 may help standardize endpoints, but reimbursement will remain contingent on national health-technology assessments.[1]Hannah Smith, “Bone marrow biopsy in geriatric patients above the age of 85 years: invaluable or unnecessary?,” Annals of Hematology, link.springer.com

Companion Diagnostics for BRAF V600E Mutation Take Center Stage

With over 95% of classic cases linked to the BRAF V600E mutation, confirming this alteration is essential before prescribing vemurafenib. The industry is shifting toward multiplex, clinic-ready testing, as demonstrated by recent partnerships to develop high-throughput flow assays. Regulatory changes, such as the reclassification of these diagnostics from Class III to Class II, are expected to shorten pre-market timelines. However, stricter analytical validation requirements are likely to increase development costs. In Europe, delays in IVDR enforcement until 2029 are creating a two-speed market, where U.S. laboratories are advancing MRD platforms while many European facilities await regulatory-compliant kits.

Ageing Male Demographic Sees Rising Incidence

The aging population is driving an increase in the absolute number of patients, despite a stable incidence rate of 0.3 per 100,000 individuals. This trend is particularly evident in the United States and Europe. With a male-to-female diagnosis ratio exceeding 4:1 and a median diagnosis age of 55, the aging male demographic is expected to sustain a gradual rise in demand.[2]Emily Green, “Pirtobrutinib after a Covalent BTK Inhibitor in Chronic Lymphocytic Leukemia,” New England Journal of Medicine, nejm.org While occupational exposures remain under investigation and sex-specific immune-surveillance theories lack conclusive trial data, demographic shifts are steadily influencing demand. However, the rarity of Hairy cell leukemia continues to impose supply-side constraints on the market.

Outpatient IV Push Formulations on the Rise

Two-hour cladribine infusions are delivering comparable complete-response rates of 92% to traditional five-day regimens while reducing febrile neutropenia cases by 50%.[3]Julia Clark, “A Sensitive NGS Assay to Detect Measurable Residual Disease,” HemaSphere, journals.lww.com In the United States, reimbursement policies that align with private-payer rates are driving the adoption of shorter infusion times. In contrast, European uptake remains slower due to payment structures tied to infusion duration. While oral vemurafenib offers further resource optimization, the concurrent need for rituximab infusions currently prevents the adoption of a fully oral treatment regimen.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Small patient pool limits trial economics | -0.8% | Global, acute in smaller EU states and APAC ex-Japan | Long term (≥ 4 years) |

| High relapse rates with purine-analog re-exposure | -0.5% | Global, higher where BRAF inhibitors lack access | Medium term (2-4 years) |

| Supply gaps for fludarabine-based reagents | -0.6% | North America, EU, Australia, New Zealand | Short term (≤ 2 years) |

| Slow reimbursement updates for ultra-rare tests | -0.7% | CEE, Latin America, select APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Small Patient Pool Limits Trial Economics

With a global prevalence of only 15,000 to 20,000 cases, even 80-patient Phase 2 studies require three years for enrollment. Per-patient costs exceed USD 45,000, double that of standard oncology trials, due to multi-center activation fees and centralized MRD testing.[4]Michael Davis, “Clinical Applications of Telemedicine Services Using a Regional Platform,” BMC Cancer, bmccancer.biomedcentral.com While regulators permit single-arm designs, European payers often reject data without randomized comparators, delaying market access timelines.

High Relapse Rates With Purine-Analog Re-Exposure

Second-line cladribine achieves a median progression-free survival of 8.2 years, a decline from 12.5 years observed after first-line therapy. Third-line remissions further decrease to 4.1 years. Increased cumulative myelosuppression significantly raises infection-related mortality risks. Off-label access to vemurafenib faces insurer denials in 38% of cases, causing delays in salvage therapy. Until randomized head-to-head data becomes available, the heavy reliance on purine-analogs continues to hinder market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Anchor Precision, Therapeutics Drive Revenue

In 2025, therapy-type products accounted for 62.34% of the revenue, highlighting the Hairy cell leukemia market's reliance on cladribine, pentostatin, rituximab, and emerging BRAF-inhibitor regimens. As MRD testing becomes standard, diagnostics are growing at a 7.79% CAGR, evolving from four-color flow panels to high-parameter spectral cytometry with a 0.01% sensitivity threshold. While the market for advanced diagnostics in Hairy cell leukemia is expanding more rapidly than drug revenue, it is starting from a smaller base.

Spectral instruments, combined with next-generation sequencing, allow for allele-specific PCR confirmation of BRAF V600E at a 0.001% variant-allele frequency, enabling clinicians to time salvage therapy accurately. However, the adoption of this workflow is inconsistent; by 2025, only 11 out of 28 EU countries reimbursed molecular tests. Yet, centralized reference labs are growing to bridge this gap. With unified MRD guidance on the horizon, diagnostics are poised to play a significant role in shaping the future market share of Hairy cell leukemia.

By Route of Administration: Oral Gains Ground, IV Retains Procedural Lock-In

In 2025, intravenous delivery accounted for 51.43% of spending, supported by established cladribine and rituximab protocols prevalent in community practice. However, oral vemurafenib is projected to expand at a 7.96% CAGR, gradually increasing the oral segment's share in the Hairy cell leukemia market. A two-hour IV push of cladribine reduces neutropenia risk compared to a five-day continuous infusion, also optimizing infusion chair usage for more profitable biologics, thus accelerating IV process innovation in the U.S.

While European adoption lags due to reimbursement codes favoring longer infusions, there is growing pressure to reduce inpatient stays. Subcutaneous rituximab, making up 8% of administration routes in 2025, could see an uptick as hospitals aim for better chair-time efficiency. Although oral therapies are challenging the IV's dominance, the ongoing need for combination rituximab infusions ensures IV's stronghold for the foreseeable future.

By Treatment Setting: First-Line Stability Masks Relapsed/Refractory Innovation

In 2025, first-line regimens accounted for 52.41% of revenue, driven by over 90% complete-remission rates from cladribine-rituximab combinations. While the market share for frontline therapy is set to see a slight decline, the relapsed/refractory segment is poised to grow at an 8.15% CAGR through 2031. A Phase 2 trial, pitting vemurafenib-obinutuzumab against cladribine-rituximab, could potentially alter the frontline landscape if it demonstrates comparable efficacy with reduced cytopenias.

However, regulatory decisions are not anticipated before 2029, likely preserving the current frontline landscape for the majority of the forecast period. Meanwhile, BRAF-inhibitor combinations in the salvage arena are not only hastening hematologic recovery but also attracting payer interest, despite their premium per-cycle pricing. Post-2029, if chemotherapy-free regimens secure label approval, the competitive landscape could undergo swift changes.

By End User: Hospitals Anchor Volume, Diagnostic Labs Capture Complexity

In 2025, hospitals accounted for 55.45% of the revenue, serving as the primary site for biopsies, infusions, and critical decisions, solidifying their role in the Hairy cell leukemia landscape. However, diagnostic laboratories are witnessing a 7.89% CAGR boost, driven by capital-heavy flow cytometry and next-generation sequencing tools, which hospitals struggle to justify given their limited sample volumes. A notable 2025 partnership between major diagnostic players underscores the advantages of centralized testing.

Prominent academic institutions are adopting hybrid models, offering both patient care and CLIA-certified molecular assays, collectively commanding 18% of the end-user revenue in 2025. As AI-driven digital pathology gains traction, reference labs equipped with cloud analytics stand to capture a larger market share. Yet, hospitals continue to dominate revenue streams, thanks to reimbursements tied to their procedures.

Geography Analysis

In 2025, North America accounted for 39.34% of the revenue, driven by Medicare's reimbursement for cladribine, rituximab, and the NCCN-listed off-label vemurafenib. These factors collectively support the Hairy Cell Leukemia market in the region. The U.S. benefits from a strong presence of academic institutions and the 2025 FDA orphan-drug fee waiver, which provides significant support to smaller sponsors. Meanwhile, Canada lags 12-18 months behind the U.S. due to Health Canada's requirement for explicit indications. Additionally, provincial formularies restrict access until cost-effectiveness reviews are completed.

Europe's 32% market share reflects regional disparities. Germany, with its 180-day automatic orphan-drug reimbursement rule, secures 28% of the region's sales. In contrast, Central and Eastern Europe face delays exceeding 24 months for national approvals. While the 2025 EU Joint Clinical Assessment aims to standardize evidentiary benchmarks, the negotiation of price-volume agreements remains under state jurisdiction. Although the Hairy Cell Leukemia market demonstrates stable potential, delayed MRD reimbursements in Poland and Bulgaria could hinder short-term growth.

Asia-Pacific, with an 8.25% CAGR, is fueled by South Korea's hematology reimbursement expansion in March 2026 and China's 2025 NRDL update, which signals a favorable stance towards targeted therapies. Japan's established orphan-drug framework facilitates quicker access. However, smaller ASEAN countries, lacking specialized hematopathology infrastructure, dampen the region's overall averages. Despite this, ongoing modernization among payers indicates a consistent growth trajectory for the Hairy Cell Leukemia market through 2031.

Competitive Landscape

The Hairy Cell Leukemia market remains moderately fragmented, with no single company commanding more than a 15% share. The availability of off-patent purine analogs, such as cladribine and pentostatin, marketed by various generics, further dilutes market concentration. Competition in diagnostic platforms is diverse, divided between global manufacturers and hospital laboratories.

Strategic integrations are transforming the market dynamics. Abbott's USD 2.3 billion acquisition of Exact Sciences in April 2026 expands its presence in oncology diagnostics while increasing exposure to risks in this ultra-niche segment. Becton Dickinson's collaboration with Labcorp demonstrates a vertical integration strategy, ensuring reagent pull-through as centralized labs scale MRD testing. Similarly, Pfizer's USD 65 million upfront agreement with Cartography Biosciences reflects growing interest in antigen-discovery platforms designed for rare B-cell cancers.

White-space opportunities are emerging in markets such as China and Brazil, where reimbursement frameworks are developing. Additional potential lies in addressing the needs of multiply relapsed patients intolerant to purine analogs and in advancing diagnostics with faster turnaround times. The FDA's reclassification of companion diagnostics could consolidate testing among a few large manufacturers, raising barriers for smaller kit developers. Meanwhile, extensions under the European IVDR may delay new entrants, potentially solidifying competitive positions until 2029. With the top five players accounting for approximately 45% of the revenue, the Hairy Cell Leukemia market remains competitive but requires substantial capital resilience to navigate its orphan-economics.

Hairy Cell Leukemia Industry Leaders

AstraZeneca PLC

F. Hoffmann-La Roche Ltd

Pfizer, Inc.

Gilead Sciences

Amgen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Updated Hairy Cell Leukemia and HCL Variant guidelines released by the Hairy Cell Leukemia Foundation stress precision medicine and individualized care.

- July 2025: The Hairy Cell Leukemia Foundation and The Leukemia & Lymphoma Society committed USD 5-7 million over five years to fund HCL research and a patient data registry.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Hairy Cell Leukemia (HCL) market refers to worldwide prescription revenues from drugs that treat classic or variant HCL, including purine-analog chemotherapy (cladribine, pentostatin), BRAF and BTK targeted agents, monoclonal antibodies, and recombinant immunotoxins, captured at ex-manufacturer prices and allocated to the year in which patients receive therapy. We count every labeled line of therapy but stop where use is purely off-label for other malignancies.

Scope Exclusions: Supportive care products, diagnostic assays, bone-marrow procedures, and hospital service fees sit outside this market.

Segmentation Overview

- By Therapy Type

- Chemotherapy (purine analogues)

- Targeted Therapy (BRAF, BTK, MEK inhibitors)

- Immunotherapy (mAbs, immunotoxins)

- Others (interferon-?, splenectomy)

- By Patient Type

- Classic HCL (cHCL)

- Variant HCL (HCL-V)

- SDRPL & other HCL-like disorders

- By Route of Administration

- Intravenous Infusion

- Sub-cutaneous Injection

- Oral

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with practicing hematologist-oncologists across North America, Europe, and Asia-Pacific, reimbursement advisors at national payers, and medical-affairs leads at three originator firms. Their insights on real-world retreatment rates, dose intensity, and access hurdles guided prevalence filters and price-erosion curves.

Desk Research

Our team first compiled disease-specific epidemiology and treatment adoption data from tier-one public sources such as SEER, CDC WONDER, Eurostat, WHO Global Health Observatory, and peer-reviewed journals that track BRAF V600E prevalence. Those figures were blended with regulatory records from FDA orphan-drug designations and EMA PRIME listings that flag future launch cohorts. We then pulled average selling prices, shipment values, and lifecycle timelines for key molecules from company 10-Ks, D&B Hoovers snapshots, and Dow Jones Factiva news archives to anchor revenue inputs. A quick scan of trade associations, the Leukemia & Lymphoma Society and European Hematology Association, helped us gauge treatment guidelines and patient pathway shifts. This list is illustrative; several additional statistics portals, patent filings, and investor decks supported fact-checking.

Market-Sizing & Forecasting

Our model begins with a prevalence-to-treated-patient build-up by region, multiplies that pool by therapy-line penetration, and reconciles the total against a top-down check that rolls up audited manufacturer HCL revenues. Supplier roll-ups for selected drugs validated unit volumes and highlighted regional under-reporting, which we corrected before finalizing the value. Key variables, diagnosed prevalence, first-line share captured by cladribine, uptake velocity of BRAF inhibitors, average treatment duration, and expected price declines after orphan-drug exclusivity, drive annual projections. Multivariate regression with scenario analysis projects future values, using epidemiology trends and macro oncology spend as covariates.

Data Validation & Update Cycle

Every revision passes three analyst reviews, gap checks against external sales trackers, and variance alerts that trigger call-backs to physicians when anomalies exceed five percent. Reports refresh yearly, and an interim sweep follows material label expansions or safety withdrawals.

Why Our Hairy Cell Leukemia Baseline Commands Reliability

Published HCL estimates often diverge because firms apply dissimilar therapy baskets, price levels, and refresh cadences.

By centering on drug-indication fit and aligning year tags with manufacturer invoicing, Mordor presents a balanced, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 125.26 Million (2025) | Mordor Intelligence | - |

| USD 130.70 Million (2023) | Global Consultancy A | Counts pre-launch pipeline sales proxies and mixes regional list prices without discount normalization |

| USD 280.00 Million (2024) | Industry Analyst B | Adds supportive care drugs and hospital infusions, inflating totals |

| USD 115.25 Million (2024) | Regional Research House C | Relies on limited public filings and assumes uniform prices across low- and high-income countries |

The comparison shows that scope breadth, price calibration, and update frequency explain most gaps. By grounding every figure in verifiable patient volumes and current invoices, Mordor Intelligence delivers a transparent baseline clients can track and replicate with confidence.

Key Questions Answered in the Report

How large is the hairy cell leukemia market in 2026?

The hairy cell leukemia market size stands at USD 207.9 million in 2026 and is forecast to reach USD 284.2 million by 2031 at a 6.45% CAGR.

Which region generates the most hairy cell leukemia revenue?

North America leads with 39.34% share in 2025, thanks to academic centers and favorable reimbursement.

What therapy type dominates Hairy cell leukemia treatment?

Therapy-type products, primarily cladribine, pentostatin, and rituximab, commanded 62.34% revenue share in 2025.

Are oral drugs gaining ground in Hairy cell leukemia care?

Yes, oral vemurafenib is projected to expand at 7.96% CAGR, gradually eroding IV dominance.

What is the fastest-growing geographic market segment through 2031?

Asia-Pacific is set to expand at an 8.25% CAGR as reimbursement frameworks mature.

Page last updated on: