Permethrin Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

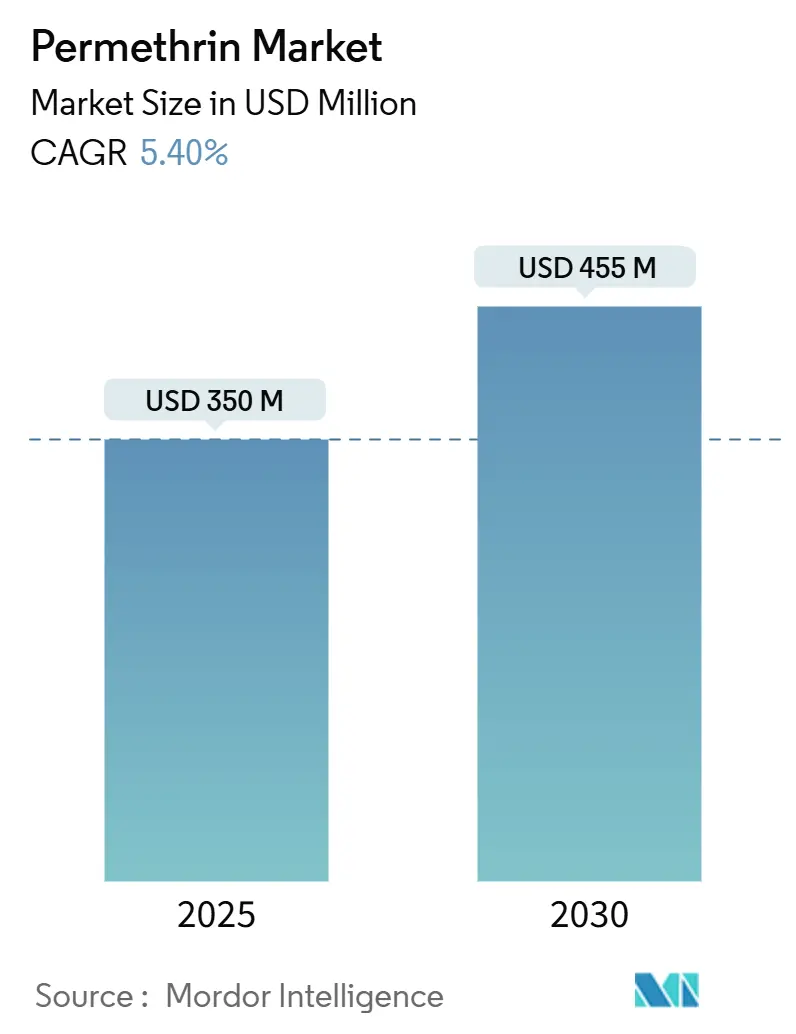

| Market Size (2025) | USD 350 Million |

| Market Size (2030) | USD 455 Million |

| Growth Rate (2025 - 2030) | 5.40% CAGR |

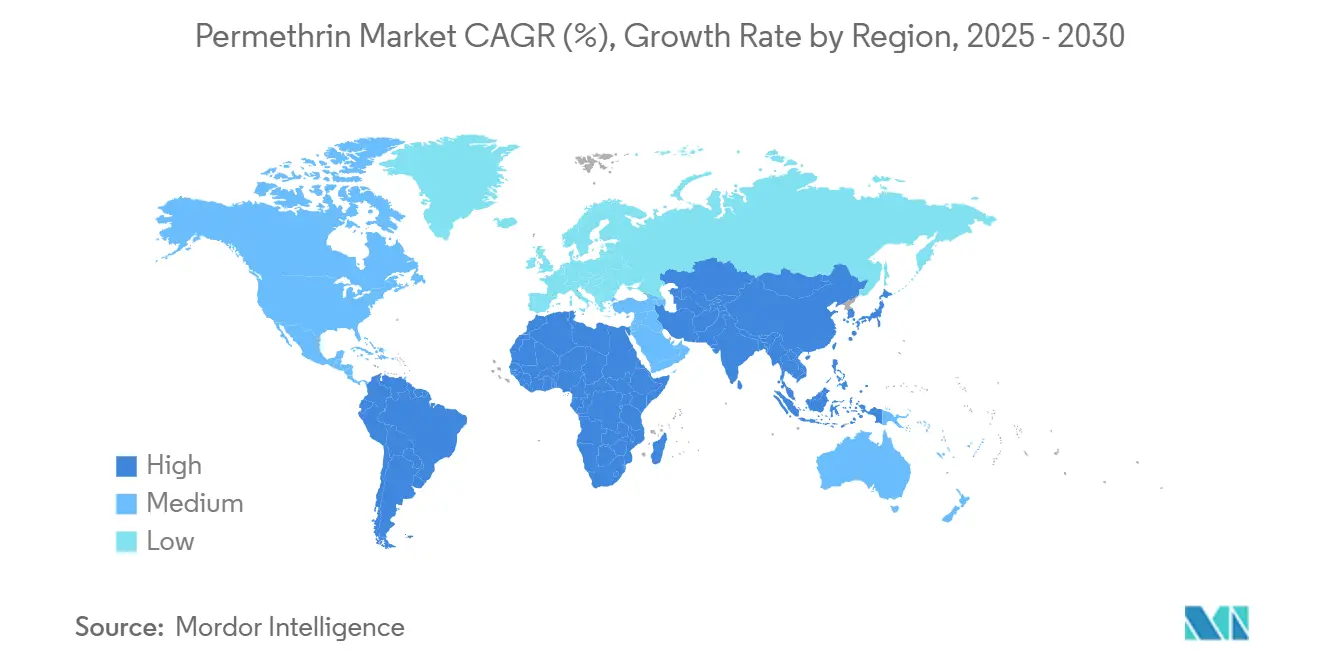

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

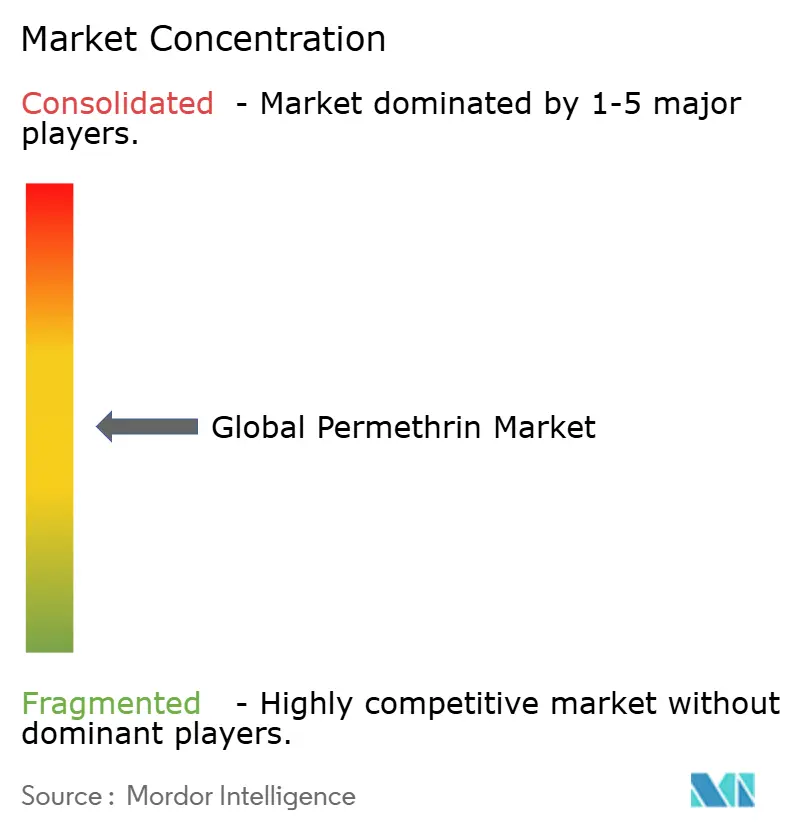

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Permethrin Market Analysis by Mordor Intelligence

The permethrin market size for agricultural applications stands at USD 350 million in 2025 and is forecast to reach USD 455 million by 2030, registering a CAGR of 5.4% over the period. This moderate expansion rests on the compound’s continued role in integrated pest-management programs, the steady rollout of precision-application tools, and regulatory shifts that phase out older organophosphates while tightening aquatic-toxicity thresholds in Europe [1]Source: U.S. Environmental Protection Agency, “EPA Releases Updates on Organophosphate Pesticides Dicrotophos, Dimethoate, and Tetrachlorvinphos,” epa.gov. Field data point to a durable value proposition: permethrin delivers broad-spectrum control against bollworms, armyworms, and other lepidopteran pests that increasingly resist neonicotinoids. Demand also benefits from UAV-enabled ultra-low-volume spraying that lowers labor costs and improves droplet deposition, a key concern on large cotton operations in Brazil and the Sunbelt states. At the same time, the sector faces counterweights, notably the rapid commercialization of microbial larvicides and the emergence of RNA-interference seed treatments that promise highly selective pest suppression. Overall, the permethrin market shows resilience because legacy chemistries exit faster than biologicals can scale, and growers still value the chemistry’s knock-down speed and compatibility with tank mixes.

Key Report Takeaways

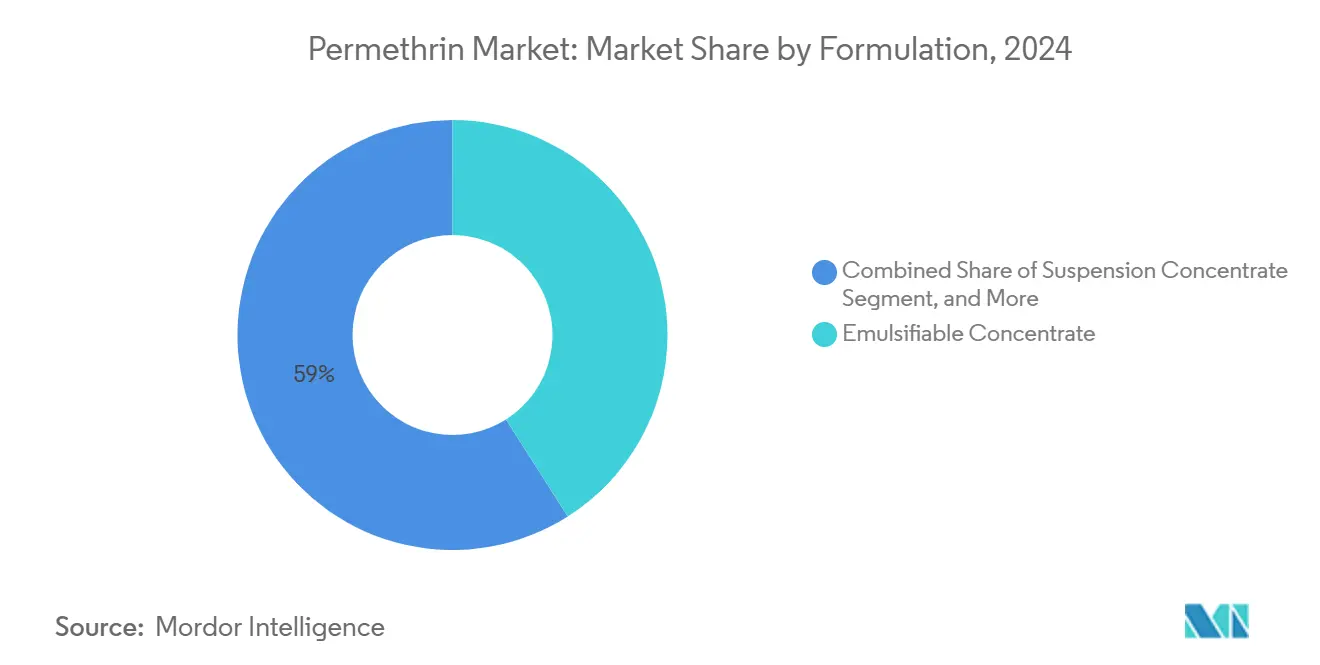

- By formulation, emulsifiable concentrates led with 41.0% of the permethrin market share in 2024, and suspension concentrates are projected to post the highest CAGR at 5.5% through 2030.

- By crop type, cotton accounted for 46.3% of the permethrin market size in 2024 and is projected to advance at a 6.0% CAGR through 2030.

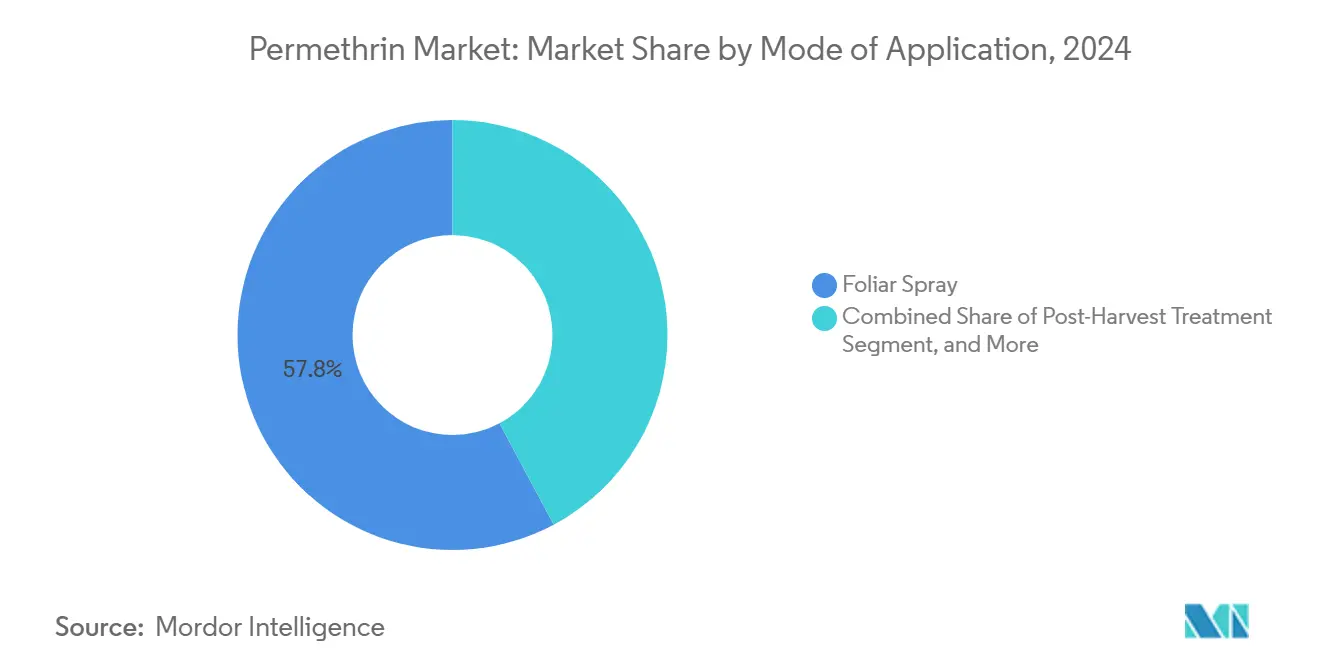

- By mode of application, foliar spray captured 57.8% of the market size in 2024 and is projected to expand at a 4.5% CAGR through 2030.

- By geography, the Asia-Pacific region held 38.5% of the market share in 2024, and Africa recorded the strongest regional CAGR at 7.0% for the forecast period.

Global Permethrin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on older organophosphates increasing pyrethroid reliance | +1.2% | North America and Europe | Medium term (2–4 years) |

| Rising resistance to neonicotinoids in key crop pests | +0.9% | Asia-Pacifica and South America | Long term (≥ 4 years) |

| Growth of cotton acreage in South America | +0.8% | Brazil and Argentina | Short term (≤ 2 years) |

| Drone-based ultra-low-volume permethrin spraying | +0.6% | United States and China | Medium term (2–4 years) |

| Integration with RNA-interference seed treatments | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Regenerative-transition certifications allowing limited synthetic use | +0.3% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Ban on Older Organophosphates Increasing Pyrethroid Reliance

National and supranational regulators are accelerating the phase-down of organophosphate insecticides, creating a replacement window for pyrethroids within existing crop-protection programs. In June 2024, the U.S. Environmental Protection Agency tightened safety margins for dicrotophos and dimethoate, which forces cotton growers to reconfigure spray calendars[2]Source: U.S. Environmental Protection Agency, “EPA Releases Updates on Organophosphate Pesticides Dicrotophos, Dimethoate, and Tetrachlorvinphos,” epa.gov. The European Union’s surface-water directive sets cumulative-exposure caps that practically bar organophosphates near canals and irrigation channels. As retailers update stewardship guidelines, distributors report a quick pivot to pyrethroid lines that match equipment already in place. The bulk of volume growth materializes in the first two years as old stocks are depleted; thereafter, growth levels moderate but remain positive because pyrethroids function as rotation partners for newer biologicals.

Rising Resistance to Neonicotinoids in Key Crop Pests

Field monitoring confirms escalating resistance among Helicoverpa species and corn earworm populations to imidacloprid and thiamethoxam, eroding the effectiveness of seed-coating regimens that dominated the 2010s. Extension specialists in the North China Plain and the Indo-Gangetic belt now recommend pyrethroid tank mixes within 40 days of crop emergence. Similar advisories are emerging in the southern United States where past reliance on at-plant neonicotinoids is no longer delivering threshold-level control. These shifts prolong the permethrin market’s relevance by locking the compound into alternate-chemistry rotations on cotton, soybean, and cereal acres.

Growth of Cotton Acreage in South America

Brazilian growers are expanding cotton for export, with planted area slated to hit 1.87 million hectares in marketing year 2024/25, a 13% leap over the prior campaign[3]Source: Foreign Agricultural Service, “Brazil: Cotton and Products Annual,” fas.usda.gov. Argentine producers, meanwhile, benefit from a 20% cut in export duties, spurring area recovery in Chaco and Santiago del Estero. Cotton remains a high-input crop: average insecticide passes the top nine per season, roughly double the spray frequency on corn. Local distributors report robust call-offs for permethrin as growers seek a cost-effective option amid currency volatility; nearly 70% of purchases are prepaid in local currency to lock in price before planting.

Drone-Based Ultra-Low-Volume Permethrin Spraying

The adoption of quadrotor UAVs (Unmanned Aerial Vehicles) is scaling, particularly among large operations in Texas, United States, and Mato Grosso, Brazil. Controlled trials demonstrate that UAV applications achieve droplet coverage of 75.47–77.86% at 10 L/ha volumes, surpassing the coverage of boom sprayers applying 30 L/ha. This efficiency encourages the use of suspension-concentrate permethrin that resists sedimentation during flight. Manufacturers are reformulating with narrower particle-size distributions to secure label approvals that reference drone-specific nozzle types. Dealers foresee double-digit growth for drone-compatible packs, a trend that offsets volume declines in conventional tractor-borne applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent aquatic-toxicity regulations in Europe | -0.8% | European Union and spillover North America | Short term (≤ 2 years) |

| Rapid rise of biological larvicides in high-value produce | -0.6% | North America and Europe | Medium term (2–4 years) |

| Increasing evidence of pyrethroid resistance in Helicoverpa spp. | -0.5% | Asia-Pacific and South America | Long term (≥ 4 years) |

| Supply-chain risk from Chinese cis-permethrin intermediates | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Aquatic-Toxicity Regulations in Europe

The European Union’s Directive 2013/39/EU sets maximum concentration thresholds of 0.0008 mg/L for certain pyrethroids in surface waters[4]Source: European Parliament and Council, “Directive 2013/39/EU of 12 August 2013,” eur-lex.europa.eu. Enforcement has intensified since May 2025, with member states lowering buffer-zone exemptions. Label revisions now require 20-meter vegetative stripes adjacent to waterways, restricting large-scale foliar applications on oilseeds in northern France. Distributors estimate a 7.0% contraction in permethrin sales in the Danube basin for 2025 as growers switch to microbial larvicides that carry no water-toxicity flags.

Rapid Rise of Biological Larvicides in High-Value Produce

Premium fruit and vegetable sectors command residue-free certifications, prompting greenhouse operators in Almería and California’s Central Valley to adopt Bacillus thuringiensis and Beauveria bassiana formulations. The global biopesticide segment grew 11% in 2024 and captured 5% of total crop-protection spend, pressuring synthetic volumes. Retail chains reinforce the shift by imposing private-label residue ceilings that are stricter than Codex guidelines, accelerating synthetic-to-bio substitution for crops sold under premium brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Suspension Concentrates Drive Innovation

The emulsifiable concentrates maintained market leadership, accounting for a 41.0% share of the permethrin market size in 2024. The suspension concentrates are projected to grow at a 5.5% CAGR, driven by adoption curves that favor shear-stable formulations. Uptake has been strongest in the southern United States, where farm-service providers annually retrofit drone fleets during winter off-seasons to accommodate evolving spray delivery systems.

Wettable powders continue to serve a vital role in smallholder-dominated regions across the Asia-Pacific, where low-cost sachets integrate well with knapsack sprayers. However, concerns over inhalable dust exposure and operator safety limit their resurgence in larger-scale or regulated markets. To address these challenges, formulators are now experimenting with polymeric dispersants that maintain particle sizes below 3 µm for up to 90 days, ensuring dose uniformity and flowability even after prolonged storage in humid, tropical warehouse environments.

By Crop Type: Cotton Dominance Reinforced by Resistance Pressures

Cotton’s centrality continues; the crop consumed 46.3% of the permethrin market size in 2024 and is on track for a 6.0% CAGR through 2030. Brazilian demand is projected to increase during the forecast period, driven by a surge in Mato Grosso’s acreage and the implementation of integrated pest management mandates. Cereals and grains, the second-largest band share, deliver stable baseline demand, especially in China’s wheat belt, where farmers time permethrin applications at the flag-leaf stage to manage aphid flights.

Oilseeds and pulses represent a modest, but they illustrate strategic value. Growers in India rely on permethrin during flowering to suppress pod borers that undermine export-grade chickpea premiums. Fruits and vegetables remain contested terrain, with biocontrol agents rapidly chipping away at permethrin’s foothold, yet certain stone-fruit orchards in Georgia still deploy the molecule against plum curculio during tight phenological windows when beneficial insects are sparse.

By Mode of Application: Drone Technology Transforms Application Methods

Foliar spray continues to dominate, capturing 57.8% of the agricultural permethrin market size in 2024, and it is anticipated to fastest growing at a CAGR of 4.5% through 2030, underpinned by entrenched mechanized spraying infrastructure across major farming economies. This mode of application remains the backbone of pest control in cotton, cereals, and vegetables, offering rapid knockdown and ease of integration with existing field operations. Yet, the foliar segment is also evolving: UAV-based (drone) applications are gaining meaningful traction, with permethrin-treated acreage. This shift is driven by labor constraints, precision targeting, and coverage efficiency, particularly in fragmented farms and hard-to-reach terrains across Asia-Pacific, North America, and South America.

Post-harvest treatments, while smaller in volume, command some of the highest gross margins in the permethrin value chain. Grain elevators and storage operators leverage permethrin’s residual efficacy to extend storage intervals, a compelling advantage in years of volatile ocean freight rates or export bottlenecks. The chemistry’s utility as a grain-protectant makes it a strategic asset in bulk storage management, especially in tropical regions prone to weevils and moth infestations.

Geography Analysis

The Asia-Pacific region anchors global demand, accounting for 38.5% of the permethrin market share in 2024. This domination of the region is largely due to the extensive cultivation of cotton and rice across China and India. Both countries possess established permethrin synthesis capacity, shielding local distributors from supply-chain tremors. Still, India’s insecticide industry is watching resistance trends; preliminary bioassays in Andhra Pradesh show kdr allele frequencies approaching 0.37, nudging consultants to advocate for alterations with chlorantraniliprole.

Africa's growth stood out at a 7.0% CAGR, benefiting from intensifying cotton programs in Burkina Faso and Ghana. Governments back subsidized spray calendars that include at least two pyrethroid passes, reflecting limited access to premium chemistries. NGOs active in the Sahel support integrated pest management projects that retain permethrin as a cost-effective component, while introducing pheromone traps and refugia.

Europe faces mounting regulatory pressure as the European Union targets a 50% reduction in chemical pesticide use by 2030, redirecting CAP (Common Agriculture Policy) subsidies toward biocontrols and precision technologies. Northern European cereal growers are adjusting their neonicotinoid (NG) spray programs, often excluding permethrin near water bodies to comply with the 20-meter buffer rule, which reduces the treated acreage. In North America, adoption of precision-spray tools on maize and soybean fields supports steady demand, with distributors incentivizing use through bundled stewardship training and rebates. South America's momentum is driven by cotton expansion, particularly in Mato Grosso, where the use of technical permethrin has surged. Meanwhile, in the Middle East, permethrin is strategically integrated into greenhouse IPM programs alongside biopesticides like Beauveria, balancing efficacy with export residue limits.

Competitive Landscape

The permethrin market reflects an oligopolistic structure, with Syngenta Group, Bayer AG, BASF SE, FMC Corporation, and Sumitomo Chemical Co., Ltd. as the top five suppliers. Syngenta Group has recently expanded its leadership through the success of its PLINAZOLIN insecticide line, showcasing its ability to refresh portfolios with novel modes of action. Bayer is emphasizing RNAi-based innovations, such as ledipasvir/sofosbuvir, in its 2025 strategy while maintaining its core pyrethroid brands amid growing generic competition.

BASF SE is actively strengthening its presence in South America by introducing six new active ingredients in Brazil, including the Vinquo insecticide, in response to growing regional demand for permethrin. FMC Corporation is pursuing diversification through biological inputs, as highlighted by its 2024 distribution partnership with Ballagro, which aims to expand microbial offerings compatible with permethrin in resistance management programs.

Generic pressure remains strong, particularly from Chinese formulators exporting competitively priced emulsifiable concentrates to Africa and the Southeast Asia-Pacific region. However, recent disruptions like energy rationing have exposed supply chain risks. In response, Western distributors are shifting toward dual-origin sourcing, increasingly favoring Indian suppliers with improved environmental compliance. Strategic differentiation is now centered on formulation technology and application innovation, with companies launching drone-specific packs featuring QR-coded dosage calculators to support precision agriculture practices such as NDVI-based variable-rate scripts.

Permethrin Industry Leaders

BASF SE

FMC Corporation

Sumitomo Chemical Co., Ltd.

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sipcam Agro USA opened a 12,000 sq ft formulation plant in Mississippi to produce EC and SC insecticides. The investment boosts domestic permethrin supply for U.S. row crops, supporting demand for precision-ready formulations.

- January 2025: Sumitomo Chemical’s full acquisition of Kenogard S.A. strengthens its direct control over European distribution. This move enhances market access for its insecticide portfolio, potentially expanding permethrin-based product reach in Southern Europe.

- September 2024: BASF’s new focus on portfolio steering and capital allocation signals a shift toward high-margin, differentiated products. This could lead to reduced emphasis on mature actives like permethrin, impacting future investment in commodity insecticide lines.

- October 2024: The United States Environmental Protection Agency (EPA) issued cancellation orders under the Federal Insecticide, Fungicide, and Rodenticide Act (FIFRA) that remove certain permethrin stock-keeping units (SKUs), prompting distributors to realign their portfolios.

Global Permethrin Market Report Scope

| Emulsifiable Concentrate |

| Wettable Powder |

| Suspension Concentrate |

| Others |

| Cotton |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Others |

| Foliar Spray |

| Post-Harvest Treatment |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Formulation | Emulsifiable Concentrate | |

| Wettable Powder | ||

| Suspension Concentrate | ||

| Others | ||

| By Crop Type | Cotton | |

| Cereals and Grains | ||

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Others | ||

| By Mode of Application | Foliar Spray | |

| Post-Harvest Treatment | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

Why is cotton the largest consumer of agricultural permethrin?

Cotton demands intensive insect control to protect lint quality, and resistance to neonicotinoids pushes growers toward pyrethroids, elevating cotton’s 46.3% share of the permethrin market.

How will Europe’s aquatic-toxicity rules affect permethrin demand?

New buffer-zone mandates and stricter water-quality limits may trim European permethrin sales by up to 7 % over the next two years as growers switch to biological alternatives.

Which formulation type is growing the fastest?

Suspension concentrates lead with a projected 5.5% CAGR because they remain stable in drone tanks and meet precision-application needs.

Are biological larvicides a serious threat to the permethrin market?

Yes, biopesticides grow at roughly double the rate of synthetics, and residue-sensitive produce segments increasingly favor microbial options, constraining permethrin’s growth in those niches.

Page last updated on: