Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

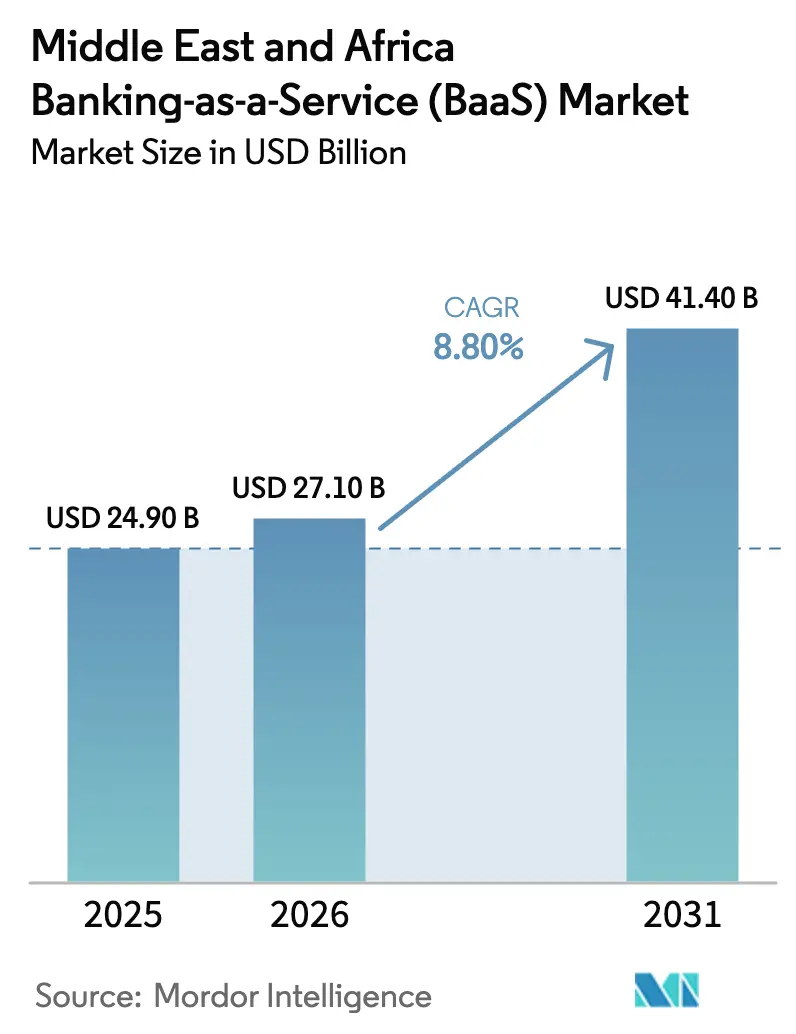

| Base Year Market Size (2025) | USD 24.90 Billion |

| Market Size (2026) | USD 27.10 Billion |

| Market Size (2031) | USD 41.40 Billion |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East & Africa Banking-as-a-Service (BaaS) Market Analysis by Mordor Intelligence

The Middle East & Africa Banking-as-a-Service Market size is projected to be USD 24.90 billion in 2025, USD 27.10 billion in 2026, and reach USD 41.40 billion by 2031, growing at a CAGR of 8.80% from 2026 to 2031.

API-centered stacks lead current deployments as banks standardize access to core capabilities through secure interfaces, while cloud-native architectures are scaling faster due to elastic capacity and regionally compliant data hosting. Nigeria is gaining share as open banking and real-time payments expand embedded finance use cases across consumer and SME channels. Payment Processing Services remain the largest service line by revenue, while Digital Banking Services post the fastest growth as institutions prefer integrated stacks that unify account management, card issuance, origination, and compliance. SME adoption is strong due to budget constraints and speed-to-launch needs that favor outsourced modules over in-house builds. Regulatory momentum in Saudi Arabia, the UAE, and Nigeria is compressing integration timelines by mandating third-party access and creating predictable onboarding rules for licensed providers[1]ICLG Editorial Team, “Fintech Laws and Regulations: Saudi Arabia,” ICLG, iclg.com.

Key Report Takeaways

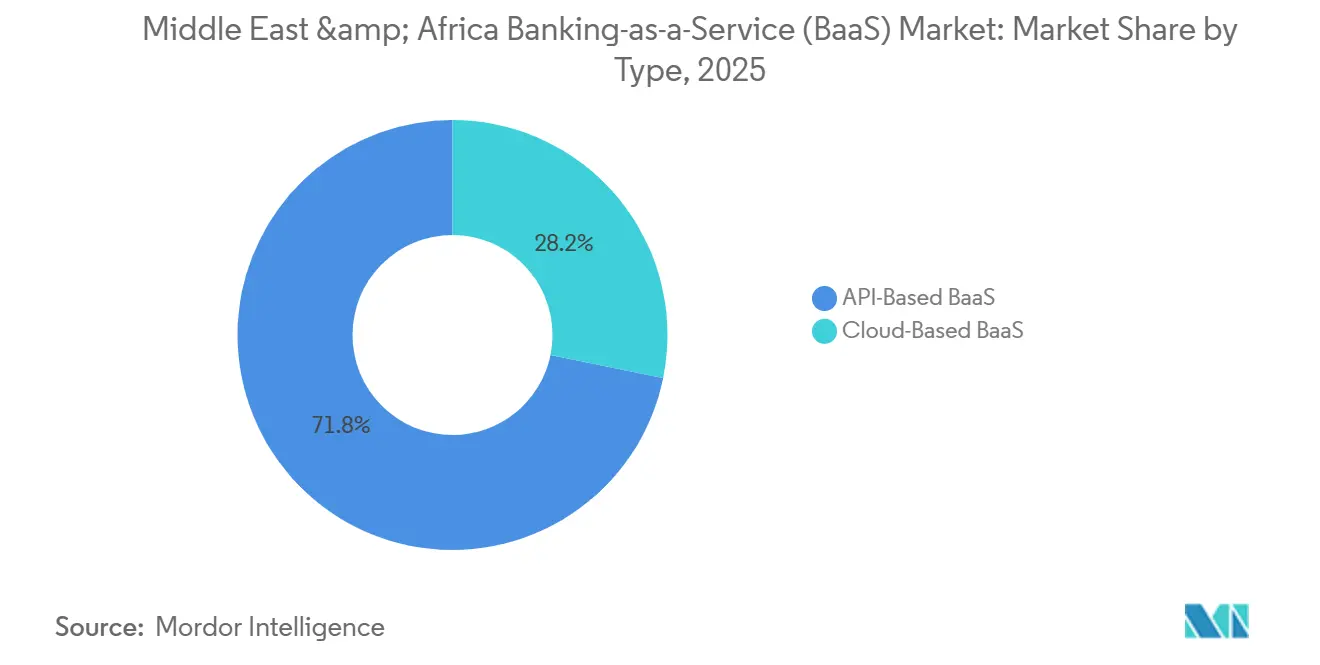

- By type, the Middle East and Africa Banking-as-a-Service Market was led by API-based platforms in 2025, while cloud-based architectures are projected to expand at a 22.8% CAGR through 2031.

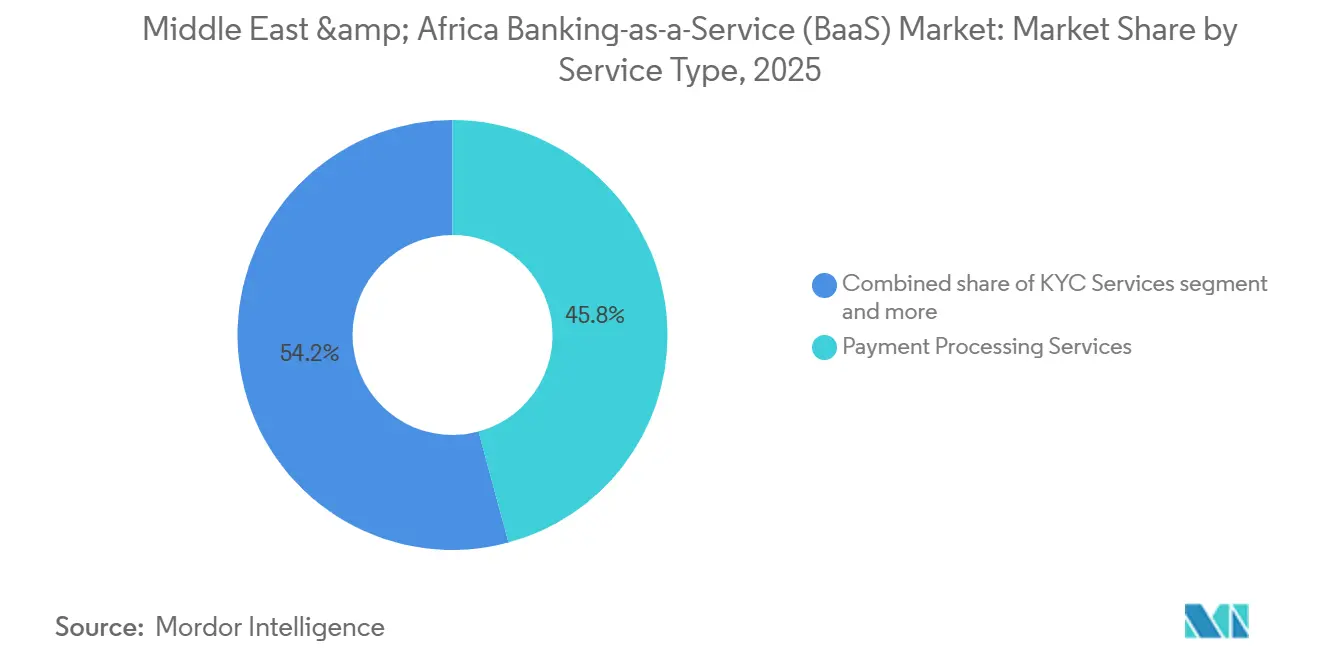

- By service type, Payment Processing Services led with 45.8% of the Middle East and Africa Banking-as-a-Service market share in 2025. Digital Banking Services are forecast to expand at a 25.9% CAGR through 2031.

- By enterprise size, SMEs accounted for a 64.5% share of the Middle East and Africa Banking-as-a-Service market size in 2025. SMEs are projected to grow at a 20.3% CAGR through 2031.

- By geography, Nigeria led with 19.4% of the Middle East and Africa Banking-as-a-Service market share in 2025. Nigeria is projected to post the fastest growth at a 26.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East & Africa Banking-as-a-Service (BaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fintech adoption by GCC banks | + 1.8% | UAE, Saudi Arabia, Bahrain, Kuwait | Medium term (2-4 years) |

| Open-banking regulations mandating API access | + 2.1% | Saudi Arabia, UAE, Bahrain, Nigeria | Short term (≤ 2 years) |

| Surge in mobile-first unbanked population | + 1.5% | Nigeria, Kenya, South Africa | Long term (≥ 4 years) |

| Cross-border payroll demand from expatriate workforce | + 0.9% | UAE, Saudi Arabia, Qatar, Bahrain, Kuwait | Medium term (2-4 years) |

| Islamic-compliant digital banking stacks | + 1.2% | Saudi Arabia, UAE, Bahrain, Nigeria | Medium term (2-4 years) |

| Government tech-free-zone incentives | + 0.7% | UAE, Saudi Arabia, Bahrain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Fintech Adoption by GCC Banks

Incumbents in the Gulf are shifting from building everything internally to selective partnerships that speed time to market for digital propositions while keeping regulatory control. Examples include banks and licensed BaaS providers collaborating on card issuing, real-time payments, and account modules, which align with sandbox programs that promote safe experimentation under supervisor oversight. This partnership model is strengthening product velocity in the Middle East and Africa Banking-as-a-Service Market, as banks use pre-certified modules rather than bespoke integrations for each launch. Regulatory programs led by SAMA and the CBUAE are important because they combine licensing clarity with cybersecurity and AML expectations that are consistent across cohorts[2]Pinsent Masons Editorial Team, “UAE Open Finance Regulation,” Pinsent Masons, pinsentmasons.com. The result is a more predictable commercialization path for BaaS propositions once pilot-stage evidence is in hand, especially across high-volume use cases like merchant payments and embedded accounts. As Gulf banks increase the mix of API-enabled services in their portfolios, they are prioritizing reusable components that lower future integration costs across adjacent product launches in the region.

Open-Banking Regulations Mandating API Access

Saudi Arabia’s Open Banking Framework and Payment Initiation Services standards require banks to expose standardized interfaces for account data and payment initiation to regulated third parties. That mandate shortens integration timelines for licensed BaaS providers because technical and consent requirements are aligned at the framework level rather than case by case. In the UAE, the Open Finance regulation that took effect in July 2025 set onboarding timelines for banks to collaborate with third-party providers, which catalyzed pre-integration between payment and account providers to meet compliance deadlines. A concrete example is NymCard’s February 2026 collaboration with Apaya to enable real-time account-to-account payments for UAE merchants, which demonstrates how open frameworks convert into new merchant acceptance options[3]NymCard Newsroom, “Apaya and NymCard Partner to Bring Open Finance-Powered Real-Time Payments to UAE Merchants,” NymCard, nymcard.com. Nigeria’s nationwide open banking rollout in August 2025 has created monetization opportunities for middleware orchestration across multiple partner banks, even as cross-border standards still vary by market. Regionally, open-banking revenue pools are expected to concentrate in Gulf markets where banks have the resources to absorb compliance costs, while aggregators bridge technical gaps for smaller markets and extend the addressable base for the Middle East and Africa Banking-as-a-Service Market.

Surge in Mobile-First Unbanked Population

Formal account penetration has improved across Sub-Saharan Africa, yet hundreds of millions of adults still operate outside traditional banking. Mobile money provides a parallel layer for payments and financial access, with very large transaction volumes occurring daily outside legacy core systems. This environment supports BaaS-based embedded finance because providers can slot credit, savings, and insurance micro-products directly into mobile workflows rather than requiring a full-service bank account. Markets like Ghana have improved onboarding by mandating national biometric ID for financial use cases, which reduces friction in KYC and accelerates activation timelines. These improvements expand the funnel for the Middle East and Africa Banking-as-a-Service Market by lifting the availability of verified identity data that can be shared via secure interfaces under customer consent. As mobile-money ecosystems continue to diversify into credit, savings, and merchant tools, embedded models that rely on BaaS rails become a primary route to scale.

Cross-Border Payroll Demand from Expatriate Workforce

Large expatriate populations in Gulf economies drive strong remittance flows, which encourage employers and platforms to adopt digital payroll and payout solutions with cross-border reach. On the receive side, African corridors remain significant and provide a stable opportunity for BaaS providers that bundle FX, compliance, and liquidity with real-time disbursement APIs. Settlement fragmentation remains a hurdle across Pan-African rails and GCC instant schemes, which requires BaaS players to manage multiple liquidity pools and multi-schema reconciliation. Network partnerships are evolving to close gaps, as seen in partnerships that enable direct remittance from the UAE to dozens of markets by using card-network infrastructure for last-mile delivery. This multi-rail architecture supports continued growth for the Middle East and Africa Banking-as-a-Service Market because employers and platforms can standardize payroll and payout flows through a single integration while routing dynamically by corridor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy core-bank integration complexity | - 1.3% | UAE, Saudi Arabia, South Africa | Short term (≤ 2 years) |

| Cybersecurity and data-sovereignty concerns | - 0.8% | Saudi Arabia, UAE, Qatar, Bahrain | Long term (≥ 4 years) |

| Scarcity of Arabic-language developer tools | - 0.6% | Saudi Arabia, UAE, North Africa | Medium term (2-4 years) |

| Fin-crime compliance talent shortage | - 0.4% | UAE, Saudi Arabia, Bahrain, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Core-Bank Integration Complexity

Banks with older cores face long change cycles, which slow the rollout of BaaS-enabled products that rely on near real-time orchestration rather than batch processing. Procurement and risk reviews extend timelines because banks verify not only technical fit but also data handling, resiliency, and audit artifacts before allowing traffic into production. Data-residency rules add steps because financial data processed by third parties must be stored and managed in-country, which requires either approved domestic cloud regions or on-premise controls. Even when providers are licensed and pre-integrated, banks still perform extensive due diligence on encryption, access control, and breach response to meet supervisory expectations. In practice, these constraints push many banks to prioritize integrations that deliver immediate impact on customer experience or cost-out, while deferring non-critical modules. The effect is uneven adoption across product lines, which tempers the near-term trajectory of the Middle East and Africa Banking-as-a-Service Market despite steady regulatory support.

Scarcity of Arabic-Language Developer Tools

Arabic NLP and localized developer ecosystems are still maturing for domains like adverse media screening, PEP detection, and customer service automation. Product teams often need bilingual developers who can connect English-based frameworks with Arabic business logic and user interfaces, and this talent pool is limited across several jurisdictions. Compliance adds another layer because consent and disclosures must be provably clear in Arabic, which means international vendors need to localize UI content and quality assurance to meet audits. In North Africa, dialect differences within Arabic increase the need for careful UX design to avoid drop-offs during onboarding and KYC flows. These localization demands add cost and slow time to market for new modules, which weighs on the pace of expansion for the Middle East and Africa Banking-as-a-Service Market in segments that depend on automated customer interaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: API Orchestration Dominates While Cloud Scales

API-based BaaS leads current deployments as banks and licensed providers favor standardized interfaces that make core capabilities easier to access and reuse across product lines. This pattern supports resource allocation toward orchestration middleware that optimizes uptime and cost by routing across multiple modules under a single control plane. The ongoing shift to open frameworks in Gulf markets strengthens the Middle East and Africa Banking-as-a-Service Market since consistent consent and security rules simplify multiprovider integration. In parallel, regulators in the UAE have formalized Open Finance obligations, which accelerates adoption of pre-certified platforms and shrinks the build-versus-buy cycle for banks. As institutions standardize account information and payment initiation endpoints, the economics of modular stacks improve, and providers can deliver features like spend analytics and embedded insurance through the same integration. This evolution gives both incumbents and fintechs a predictable path to launch and scale in multiple markets under clear supervisory expectations.

Cloud-based architectures are gaining momentum due to elastic capacity and the availability of in-country cloud regions that satisfy data-residency and security requirements. In this context, cloud-native BaaS is projected to grow at a 22.8% CAGR through 2031, reflecting a scale-up phase where providers can add AI-enabled fraud, AML, and support modules without heavy infrastructure investments. Banks are adopting hybrid models that keep sensitive tier-1 workloads on-premise while running analytics and decisioning in the cloud to balance performance and regulatory comfort. Platform providers are aligning roadmaps to this hybrid reality by offering deployment flexibility and native connectors that simplify migration and workload placement. As open-banking maturity increases, orchestration layers will further streamline module selection and lifecycle management, which should support continued expansion of the Middle East and Africa Banking-as-a-Service Market across both greenfield and legacy environments.

By Service Type: Payments Lead but Full-Suite Banking Accelerates

Payment Processing Services led with 45.8% of the Middle East and Africa Banking-as-a-Service market share in 2025, reflecting high transaction volumes across real-time account-to-account rails and card-based acceptance. Across Africa and the Gulf, instant payment schemes process large volumes, which shifts competitive focus toward uptime, authorization rates, and settlement speed. To preserve unit economics as fees compress, providers are bundling value-added services such as FX optimization, smart routing, reconciliation APIs, and dispute automation. Partnerships with network and issuer platforms are enabling new flows like merchant-initiated account-to-account payments, which widen acceptance beyond traditional cards. These shifts support consistent scale for the Middle East and Africa Banking-as-a-Service Market in merchant and gig-economy disbursements.

Digital Banking Services are projected to be the fastest-growing line at a 25.9% CAGR through 2031 as institutions prefer integrated stacks that unify accounts, cards, lending, and compliance in a single integration. Embedded finance models in telecom, ride-hailing, and retail are using BaaS rails to deliver accounts and credit at point of need, which creates a distribution edge over standalone banking apps. Identity and compliance modules are also advancing through vendor capabilities in biometric verification and risk screening tailored for regional regulations. This progression increases attach rates for complementary services like spend analytics and savings automation, thereby expanding revenue per customer. The combination of scalable infrastructure and maturing open frameworks is set to add depth to the Middle East and Africa Banking-as-a-Service market size within full-suite digital banking offerings.

By Enterprise Size: SME Velocity Versus Large-Enterprise Value

SMEs accounted for 64.5% share of the Middle East and Africa Banking-as-a-Service market size in 2025 as resource-constrained firms adopt off-the-shelf financial modules to accelerate customer onboarding, payments, and lending. Strong SME take-up is driven by embedded lending at checkout, invoice-based working capital, and API-driven cash-flow underwriting that shortens decision times from weeks to hours. As SME adoption compounds, providers are increasing cross-sell into payroll, expense management, and FX, lifting lifetime value even where average ticket sizes are smaller. Bank partnerships also scale SME access by offering white-labeled modules for account opening and transaction monitoring. These dynamics establish SMEs as a durable growth engine for the Middle East and Africa Banking-as-a-Service Market across both bank-led and platform-led channels.

SMEs are also set to expand at a 20.3% CAGR through 2031, supported by digitization mandates and the proliferation of embedded finance within enterprise software used by smaller businesses. Large enterprises create high-value deals in payroll, treasury, and supply-chain finance, which often require hybrid deployments with rigorous data segregation and audit trails. Vendor investments in Islamic finance automation, such as profit-sharing modules and Sharia-compliant product templates, enable corporate-grade offerings in markets where religious compliance is mandatory. As corporate systems integrate letters of credit, guarantees, and collections into ERPs using standardized messages, BaaS platforms are positioned to provide orchestration and monitoring for these flows. The blend of SME-led velocity and enterprise-led value helps the Middle East and Africa Banking-as-a-Service industry move from point solutions toward platform relationships that can span multiple product lines.

Geography Analysis

Nigeria held a 19.4% share in 2025 and is projected to grow at a 26.8% CAGR through 2031, supported by leadership in Africa’s e-payment transaction volumes and the commercial rollout of open banking. Nationwide open banking rules, effective August 2025, create consistent standards for licensed aggregators to orchestrate APIs across multiple banks, which expands embedded use cases across consumer and SME segments. Real-time payment activity remains high, and BaaS providers are leveraging this velocity to layer lending, savings, and merchant tools. The Nigeria trajectory underscores how regulatory clarity and transaction scale support steady share gains within the Middle East and Africa Banking-as-a-Service Market.

The UAE is advancing through formal Open Finance regulation, which took effect in July 2025 and set onboarding expectations for banks collaborating with third-party providers. Providers pre-integrated to open frameworks are already launching new payment options such as merchant account-to-account acceptance. Saudi Arabia continues to scale under Vision 2030 with active sandbox and open-banking initiatives, and payment initiation standards published in September 2024 guide new product launches. In both Gulf markets, data residency and cybersecurity standards shape deployment choices, which favors providers that support in-country cloud regions and robust audit controls. These conditions sustain a predictable investment environment, which benefits the Middle East and Africa Banking-as-a-Service Market as more banks standardize on API-first models.

South Africa shows strong technical capability but faces higher onboarding and compliance costs for certain cross-border and sanctions-sensitive flows, which places a premium on accurate screening and exception handling. In the broader region, there is momentum in identity and payments modernization, such as biometric mandates for financial onboarding that reduce KYC friction and enable faster account activation. Egypt’s banking sector is modernizing cross-border payments, demonstrated by new integrations that cut settlement times and reduce nostro balances for institutions expanding digital services. West and East African corridors are also improving through wallet tokenization and card–wallet interoperability, which widens access beyond traditional banked populations. These steps widen the base of addressable users and transactions for the Middle East and Africa Banking-as-a-Service Market and help unify experiences across previously disconnected systems.

Competitive Landscape

The provider landscape is fragmented by jurisdiction and license scope, which limits the ability of any one platform to achieve pan-regional dominance. Local entity requirements in Gulf markets and country-by-country approvals in Africa shape how BaaS platforms enter and scale, often via hub-and-spoke strategies anchored in compliant free zones and strong bank partnerships. This results in a mix of domestic specialists and international vendors working with banks and non-bank platforms to deliver accounts, payments, and lending modules tailored to local rules. These conditions favor modular offerings that adapt to each regulator’s consent, data residency, and security requirements across the Middle East and Africa Banking-as-a-Service Market.

Several providers illustrate active scaling and product expansion. NymCard has expanded its capabilities and funding base while partnering to enable open-finance account-to-account payments for UAE merchants. PayTabs launched an AI-powered orchestration platform that targets large transaction volumes through dynamic routing and authorization optimization for merchants. Onafriq has added wallet tokenization and is piloting cross-border wallet-based transfers, which extend addressable users beyond traditional accounts. Temenos and Mambu continue to upgrade modules for payments and Islamic finance, which banks in the region are adopting to improve product flexibility and compliance. These moves show how technology depth and regulatory readiness determine scale outcomes in the Middle East and Africa Banking-as-a-Service Market.

Open finance approvals are accelerating first-mover advantages, as seen with providers that secured central bank recognition and launched merchant-facing payment flows in 2025 and 2026. Flutterwave’s stablecoin initiatives illustrate an emerging path to compress cross-border friction and costs, which could shift payout economics once rules for custody and reporting stabilize. Bank and fintech partnerships in Egypt are upgrading cross-border capabilities to reduce settlement times and liquidity needs, which demonstrates how enterprise-grade integrations are becoming mainstream. Together, these strategic moves highlight why technical readiness, licensing, and bank partnerships remain decisive in the Middle East and Africa Banking-as-a-Service Market.

Middle East & Africa Banking-as-a-Service (BaaS) Industry Leaders

NymCard

PayTabs

Flutterwave

Fawry

MFS Africa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NymCard partnered with Apaya to enable Open Finance-powered real-time account-to-account payments for UAE merchants through the Al Tareq framework.

- February 2026: MFS Africa/Onafriq enabled Visa digital wallet tokenization for card issuers across the CEMEA region, allowing wallets to transact via Visa credentials without physical cards.

- January 2026: ADCB Egypt launched modernized payments with Temenos, implementing Temenos Payments for SWIFT, moving from T+2 to same-day settlement and reducing nostro requirements.

- January 2026: Flutterwave partnered with Turnkey to power secure stablecoin wallets, building on an October 2025 strategy announcement focused on USD-pegged digital currency for cross-border trade.

Middle East & Africa Banking-as-a-Service (BaaS) Market Report Scope

The banking as-a-services (BaaS) market is an end-to-end model that enables digital banks and other third parties to connect directly with bank systems via API, allowing them to build banking offerings on top of the providers' regulated infrastructure while also unlocking the open banking opportunity, reshaping the global financial services landscape.

The baking-as-a-service market is segmented by type, by service type, by enterprise size, and by region. By type, the market is segmented into api-based baas and cloud-based baas. By service type, the market is segmented into payment process services, digital banking services, KYC services, customer support services, and others. By enterprise size, the market is segmented into small, and large enterprises. By region, the market is segmented into South Africa, GCC, Egypt, the rest of the Middle and Africa. The report offers market size and forecasts for the Middle East and Africa banking as-a-services market in value (USD) for all the above segments.

By Type

| API-Based BaaS |

| Cloud-Based BaaS |

By Service Type

| Payment Processing Services |

| Digital Banking Services |

| KYC Services |

| Customer Support Services |

| Others |

By Enterprise Size

| SMEs |

| Large Enterprises |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East & Africa |

| By Type | API-Based BaaS |

| Cloud-Based BaaS | |

| By Service Type | Payment Processing Services |

| Digital Banking Services | |

| KYC Services | |

| Customer Support Services | |

| Others | |

| By Enterprise Size | SMEs |

| Large Enterprises | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

Key Questions Answered in the Report

What is the Middle East and Africa Banking-as-a-Service market size and growth outlook to 2031?

The Middle East and Africa Banking-as-a-Service market size was USD 24.9 billion in 2025 and is projected to reach USD 41.4 billion by 2031 at a 8.8% CAGR over 2026-2031.

Which segments lead and which grow fastest within this market?

Payment Processing Services led by revenue in 2025, while Digital Banking Services are projected to grow the fastest at a 25.9% CAGR to 2031.

How is regulation shaping near-term BaaS deployments in MEA?

Open-banking and open finance rules in Saudi Arabia and the UAE are compressing integration timelines by standardizing consent, security, and onboarding for third parties, which accelerates commercialization.

Which countries show the strongest momentum for adoption through 2031?

Nigeria leads current share and is projected to be the fastest-growing geography due to open banking and real-time payment scale, while the UAE and Saudi Arabia benefit from mature regulatory frameworks and strong bank partnerships.

Why are SMEs a core demand driver for BaaS in MEA?

SMEs prefer modular financial capabilities to reduce build costs and launch quickly, accounting for 64.5% of adoption in 2025 and projected to grow at 20.3% CAGR through 2031.

What are the key barriers slowing BaaS scaling across the region?

Integration with legacy cores, data residency obligations, and scarcity of Arabic-language developer tools slow rollouts, which raises the bar for providers to support in-country hosting and localized compliance UX.

Page last updated on: