Forage Sorghum Seed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

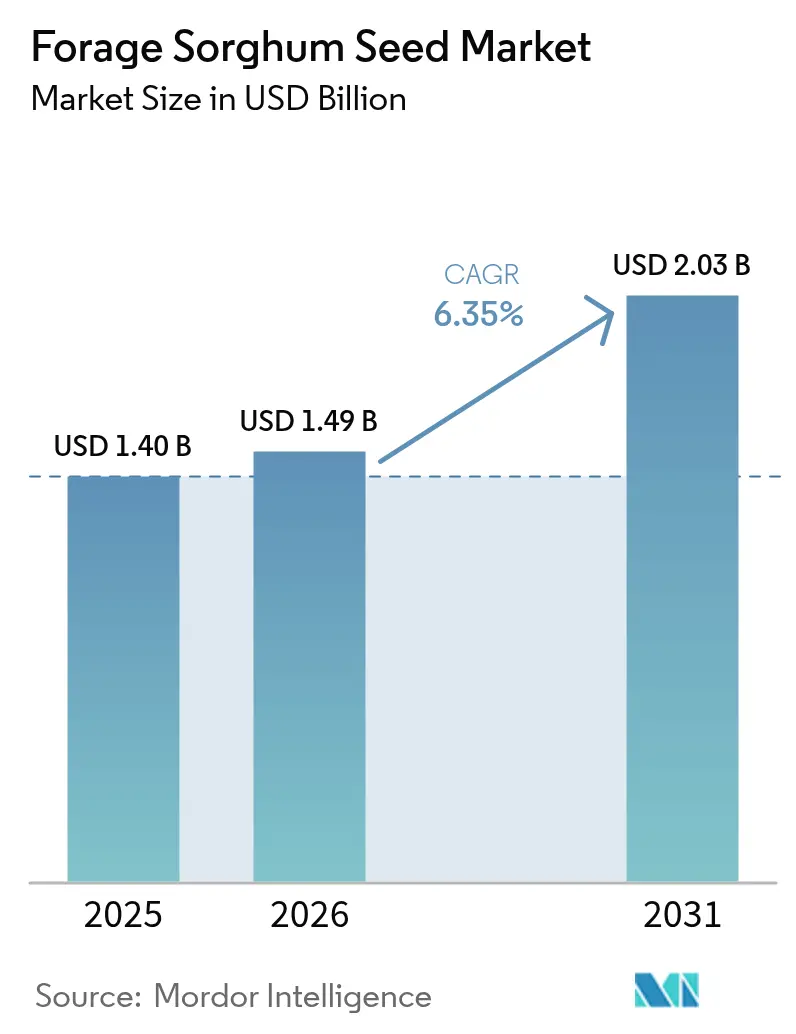

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

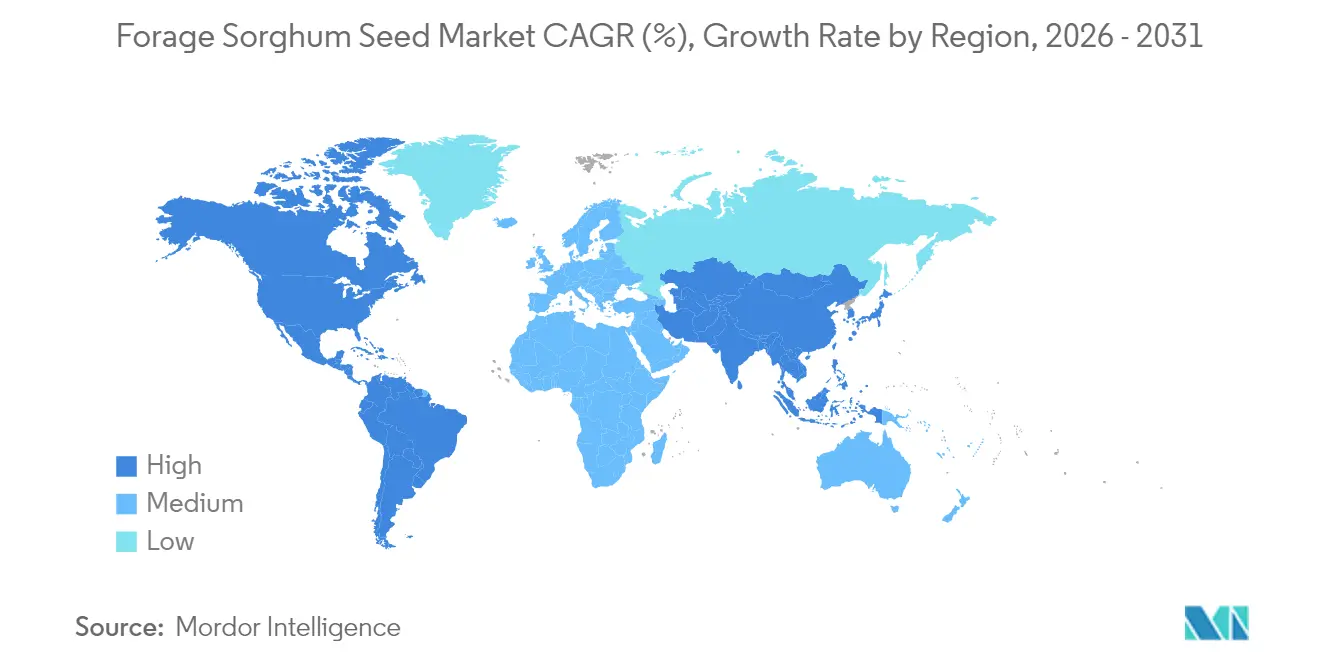

| Fastest Growing Market | Africa |

| Largest Market | North America |

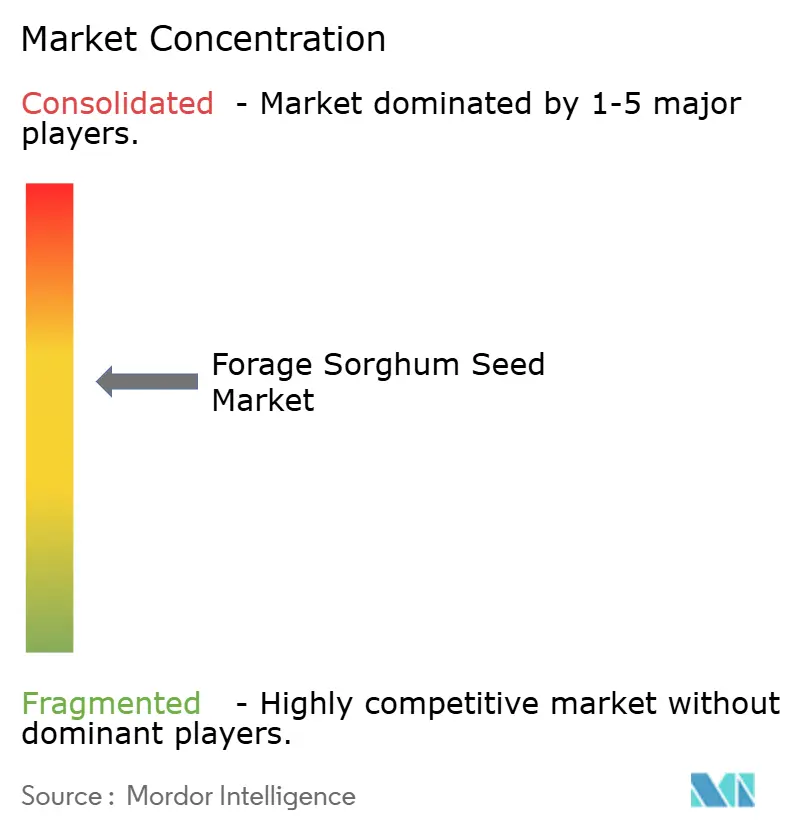

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forage Sorghum Seed Market Analysis by Mordor Intelligence

The forage sorghum seed market size is expected to grow from USD 1.40 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.03 billion by 2031 at 6.35% CAGR over 2026-2031. Rising water scarcity, expanding dairy and beef herds, and the crop’s superior water-use efficiency compared with corn are steering acreage toward forage sorghum across key producing regions. Brown-mid-rib (BMR) hybrids are gaining traction because they match corn-silage performance while lowering irrigation demand, while photoperiod-sensitive cultivars nearly double biomass yields over perennial energy crops. Carbon-credit programs are unlocking additional revenue streams as the crop’s low-input profile dovetails with climate-smart agriculture incentives.

Key Report Takeaways

- By geography, North America led the forage sorghum seed market with a 31.70% share in 2025, while Africa is projrcted to register the fastest growth at a 9.79% CAGR through 2031.

- The forage sorghum seed market remains concentrated, with players including Corteva Agriscience, UPL Limited, Bayer AG, KWS SAAT SE & Co. KGaA, and RAGT Semences SAS.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Forage Sorghum Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global demand for animal protein | +1.8% | Asia-Pacific and Africa | Medium term (2-4 years) |

| Superior drought-tolerance vs. corn driving acreage shifts in arid zones | +1.5% | North America, Middle East, Africa, and Australia | Long term (≥ 4 years) |

| BMR (brown-mid-rib) hybrids boosting feed digestibility | +1.2% | North America and Europe | Medium term (2-4 years) |

| Carbon-credit programs rewarding low-input fodder crops | +0.8% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| On-farm biogas projects creating pull for high-yield silage crops | +0.7% | Europe and North America, expanding to Asia | Medium term (2-4 years) |

| Development of photoperiod-sensitive cultivars extending harvest window | +0.9% | Temperate and subtropical regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Demand for Animal Protein

Meat and dairy consumption is climbing sharply in emerging economies, lifting demand for high-quality forage that can deliver protein with lower water footprints. Major importers nowadays direct 83% of sorghum consumption to feed, with China alone accounting for 87% of global trade[1]Source: Scientific Research Publishing, “Chinese Domestic Supply and Demand for Grain Sorghum,” scirp.org. Sorghum provides comparable animal performance to corn while using 60% less water, positioning it as a preferred feed grain in water-stressed markets. Malaysia’s policy push to lessen feed imports by promoting domestic sorghum, with potential yields of 79.98 metric tons per hectare, illustrates the trend [2].Source: Food and Fertilizer Technology Center, “Sorghum as a New Source of Animal Feed in Malaysia,” ap.fftc.org.tw Protein-focused dairies benefit from BMR sorghum that can reach 11% crude protein with sound nitrogen management, rivaling premium alfalfa. These factors are shifting crop choices toward forage sorghum, especially where water is scarce, and protein demand is rising.

Superior Drought-Tolerance Vs. Corn Driving Acreage Shifts in Arid Zones

Water scarcity is prompting a structural shift from corn to sorghum in marginal environments. Under 20% deficit irrigation, sorghum sustains yields while corn declines steeply, confirming its resilience [3]Source: American Society of Agricultural and Biological Engineers, “Climate Change Impacts on Grain Sorghum Yield,” asabe.org. In the Texas High Plains, dwindling groundwater supplies are accelerating sorghum adoption for beef and dairy feed. Climate models show forage sorghum yields rising 0.53 megagrams per hectare per 1°C temperature increase, reinforcing its climate-proof appeal. Regions receiving 300-500 mm of annual rainfall stand out, where sorghum’s deeper roots and osmotic adjustment ensure yield stability. Australia’s anticipated 2.3 million-ton harvest, the second-highest in a decade, underscores the global acreage pivot.

BMR (Brown-Mid-Rib) Hybrids Boosting Feed Digestibility

Brown-mid-rib genetics are redefining forage quality standards. BMR sorghum cuts lignin 15-20%, elevating neutral-detergent-fiber digestibility and enabling milk outputs comparable with corn silage. Trials show harvesting eight weeks after heading maximizes sugar and starch accumulation, driving higher digestible energy. Economic gains include 15-25% feed-cost savings versus corn silage, lodging risk, and 10-15% lower yields necessitate careful hybrid selection. Nutritionists increasingly view BMR sorghum as suitable for high-producing herds when balanced with protein supplements, accelerating adoption in commercial dairies.

Carbon-Credit Programs Rewarding Low-Input Fodder Crops

Agricultural carbon markets are offering fresh income streams. USDA's (United States Department of Agriculture) interim rule on climate-smart agriculture crops used as biofuel feedstocks specifically includes sorghum, establishing technical guidelines that quantify greenhouse gas emission reductions and create market opportunities for producers adopting sustainable practices[4]Source: USDA, “Interim Rule on Climate-Smart Biofuel Feedstocks,” usda.gov. No-till sorghum systems increase soil organic carbon compared to conventional tillage, and pairing nitrogen fertilization with crop rotation further enhances this benefit. Sorghum Checkoff’s sustainability roadmap links soil health metrics to carbon intensity, directly influencing premiums in low-carbon markets. European studies report a 49% reduction in well-to-wheels emissions when sorghum-based bioethanol is used in conjunction with combined heat and power systems. These policy and price signals elevate sorghum’s profitability beyond traditional commodity returns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal sowing window limits double-cropping in temperate zones | -0.9% | North America and Europe, and temperate Asia | Short term (≤ 2 years) |

| Persisting prussic-acid toxicity concerns among cattle producers | -1.1% | Global, especially areas lacking extension services | Medium term (2-4 years) |

| Limited hybrid seed availability in smallholder markets | -0.8% | Africa, Asia, and Latin America smallholder regions | Long term (≥ 4 years) |

| Competition from improved sorghum-sudan grass blends | -0.6% | North America and Australia commercial forage operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal Sowing Window Limits Double-Cropping in Temperate Zones

Sorghum requires soil temperatures above 60°F, which narrows planting opportunities and reduces the feasibility of wheat-sorghum double-cropping in temperate zones. Early planting into cool soils can cut grain yields by up to 2,000 kg per hectare. The northern Corn Belt faces a clash between optimal sorghum planting dates and wheat harvest timing, hindering land-use efficiency. Cold-tolerant germplasm shows promise, but commercial release remains limited. Producers must either accept lower sorghum yields from early sowing or forgo the double-crop revenue. Extension guidance urges waiting until soils hit 65°F, further compressing the viable planting window.

Persisting Prussic-Acid Toxicity Concerns Among Cattle Producers

Sorghum contains dhurrin, which can release lethal hydrogen cyanide under stress, deterring risk-averse operators. Levels above 200 ppm HCN (Hydrogen Cyanide) are dangerous, especially in young plants and drought-stressed regrowth. Management tactics, such as delaying grazing until plants reach 18-24 inches or avoiding frost-stressed forage, mitigate the hazard, but testing costs and insurance gaps discourage adoption at Purdue. Dhurrin-free hybrids are under development, remain scarce, and may carry yield penalties. Until practical solutions reach scale, concerns about toxicity will limit uptake in certain regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

North America commanded 31.70% of the forage sorghum seed market size in 2025, reflecting well-established seed supply chains and advanced trait portfolios. The region’s outlook hinges on expanding dairy and feedlot demand coupled with heightened water-use restrictions. Producers are increasingly choosing BMR and herbicide-tolerant hybrids, while export-oriented elevators are ramping up sorghum shipments to Asia, thereby sustaining domestic seed demand. Nonetheless, a forecast decline in Chinese grain sorghum imports injects uncertainty, prompting growers to scout new export outlets across South and Southeast Asia.

Africa, the fastest riser at 9.79% CAGR, is converting sorghum from a food security staple to a cash crop. National programs in Nigeria, Sudan, and Ethiopia promote high-yield open-pollinated varieties to bolster seed demand. Hybrid penetration remains low, indicating untapped upside for seed companies well-positioned to deliver climate-resilient genetics. Smallholder access to certified seed, extension support, and financing will shape the region’s contribution to the forage sorghum seed market over the next decade.

The Asia-Pacific forage sorghum seed market is anticipated to grow due to livestock sector expansion and climate adaptation requirements. Indonesia's potential cultivation area of 68.5 million hectares (28.17 percent of total land area) represents significant growth opportunities, particularly in the Lesser Sunda and Sulawesi ecoregions. Malaysia's government initiatives to reduce feed import dependency through sorghum cultivation, with targeted benefit-cost ratios of 1.46, indicate strong policy support for market expansion.

Regulatory Landscape

Regulation for forage sorghum seed is shaped by national seed-quality standards, plant variety protection rules, and phytosanitary requirements that govern cross-border movement. In China, the State Administration for Market Regulation (SAMR) published the revised National Standard GB4404.1-2024 for cereal seeds (including sorghum) on October 28, 2024, with implementation from October 1, 2025. This is likely to increase supplier focus on quality indicators and production methods serving import-facing channels.

International trade flows also depend on phytosanitary compliance under the International Plant Protection Convention (IPPC) and the WTO SPS Agreement, which anchor measures to prevent the spread of seed-borne pests and weeds relevant to sorghum seed lots. Variety testing and registration practices are guided by UPOV Technical Guidelines for Sorghum bicolor (TG/122), while national certification and release systems, including SANSOR in South Africa and KEPHIS in Kenya under the Seeds and Plant Varieties Act, set minimum requirements for germination, purity, and certification schemes. These requirements can affect time-to-market for new hybrids and stewardship-managed trait platforms.

Competitive Landscape

The forage sorghum seed market remains concentrated, with key players including Corteva Agriscience, UPL Limited, Bayer AG, KWS SAAT SE & Co. KGaA, and RAGT Semences SAS. Innovative Seed Solutions joint venture, pooling genetics and production assets. The sorghum seed industry's technology differentiation primarily revolves around herbicide tolerance traits, with three main platforms: Corteva's Inzen, Advanta's iGrowth, and S&W's Double Team.

These platforms establish competitive advantages through their stewardship requirements and trait licensing agreements. Market expansion opportunities exist in developing regions, particularly in Africa and Asia, where hybrid seed adoption remains low and open-pollinated varieties continue to dominate smallholder farming systems.

The industry's competitive dynamics are evolving with the adoption of precision agriculture, as companies develop digital platforms and data analytics to enhance variety selection and agronomic guidance. Additionally, specialty breeding companies are emerging as market disruptors by focusing on specific applications, such as biogas production and carbon sequestration. These companies use photoperiod-sensitive genetics and BMR traits to target premium pricing in sustainability markets. Industry-wide quality standards, maintained by organizations such as AOSCA (Association of Official Seed Certifying Agencies), ensure genetic purity and product quality. While these standards benefit established companies with robust quality control systems, they may create entry barriers for smaller competitors.

Forage Sorghum Seed Industry Leaders

Corteva Agriscience

UPL Limited

Bayer AG

RAGT Semences SAS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product development aimed at dual-use demand (silage plus bioenergy or biogas) is creating whitespace for forage sorghum hybrids positioned beyond traditional fodder, particularly where water constraints and on-farm energy projects influence crop choice. A concrete example is the March 2026 launch of Embrapa Corn and Sorghum and Latina Seeds giant forage sorghum hybrid BRS 662 (LAS6002F), targeting silage and biogas. It is commercialized with an initial 10,000-bag production run, along with a stated scale-up plan for the next cycle, indicating a more industrialized go-to-market approach for high-biomass genetics.

There is also room to expand seed demand through programs and practices that connect forage sorghum to resource-efficiency outcomes and measurable performance. In the United States, forage sorghum is referenced in the 2026 Livestock Forage Program context as a water-conserving forage option, which supports adoption discussions in irrigation-limited regions. On the technology side, 2026 breeding and agronomy work highlights tools such as transgene-free genome editing approaches and seed treatments (for example, nano-priming) aimed at improving drought tolerance and forage performance. These pipelines target traits that address water scarcity, pest pressure, and feed-quality targets such as crude protein and digestibility.

Recent Industry Developments

- May 2026: UPL Limited reported continued expansion and positioning of its iGrowth sorghum production system across the Americas, highlighting breadth of managed hybrids in Brazil and North America. The update reinforces competitive intensity around herbicide-tolerant platforms that bundle seed, stewardship, and agronomic programs, which can shape hybrid choice in commercial forage and mixed-use sorghum acres.

- December 2025: UPL Limited (via its seed platform) completed the acquisition of Hybrid Seeds Vietnam Company Limited. The acquisition strengthens local seed operations and distribution reach in Vietnam, supporting broader Southeast Asia penetration where hybrid availability and channel access remain constraints for improved sorghum seed adoption.

- May 2024: S&W Seed Company launched Double Team Forage Sorghum, expanding its proprietary sorghum trait technology portfolio. By offering a non-GMO weed control solution applied directly to the crop, the launch sharpened trait-based differentiation for forage sorghum and gave growers another pathway to manage weed pressure without shifting away from sorghum in water-stressed rotations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of forage sorghum seed used to plant sorghum grown mainly for livestock feed uses like silage, hay, and grazing. The sizing reflects commercial seed demand across major producing and consuming countries, reported in USD and aggregated to a global total.

Scope exclusions: Excludes grain sorghum seed demand intended mainly for human food channels and non-seed inputs such as fertilizers, crop protection chemicals, and farm machinery.

Segmentation Overview

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- Spain

- Poland

- Ukraine

- Rest of Europe

- Asia-Pacific

- China

- India

- New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a clean map of where forage sorghum is planted and how it is used, and then linking that to seed demand logic. Public sources were used to anchor the demand pool, including FAOSTAT area and production series, USDA crop and feed notes, and national agriculture ministries that publish crop acreage and seed program updates.

We also referenced sources such as OECD Seed Schemes, international trade and customs statistics for seed movements, and peer reviewed agronomy journals that report seeding rates and yield responses under drought and heat conditions. Company annual reports, investor decks, and reputable press were used to understand distribution structure and pricing direction, while a paid subscription for company financials and a patent database helped validate where breeding activity and product launches are concentrated. These examples are not exhaustive, and many other public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking the real buying pattern of forage sorghum seed and the practical pricing that farmers and distributors see in each region. We spoke with a mix of seed producers, regional distributors, agronomists, and large farm operators across APAC, EMEA, and the Americas so assumptions on acreage mix, replacement cycles, and hybrid adoption could be adjusted, and then reconciled back to the modeled totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 50% |

| Mid tier: 49% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 19% | Managers: 50% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where crop area suitable for forage sorghum and observed adoption in feed systems are converted into seed volume and then into value using region typical pricing. To keep the model realistic, we then used selective bottom-up checks like sampled price points from distributors, a limited supplier roll up view in key countries, and channel feedback on annual volumes, which were used to tune the global total.

Inputs that mattered most included forage sorghum acreage trends, seeding rates by planting method, hybrid versus conventional split, average pack price movement by region, and the share of output routed to silage and grazing systems. Weather variability and water stress indicators were also tracked because they influence switching toward sorghum in dry seasons and affect ordering timing.

For forecasting, scenario analysis was used so drivers like livestock herd growth, irrigated area constraints, and seed price inflation could be flexed without forcing one straight line outcome. Where bottom-up information was thin, gaps were handled by using proxy countries with similar cropping systems, and then adjusting with interview based correction factors before final aggregation.

Data Validation & Update Cycle

Model outputs were cross checked against independent signals such as crop area reports, trade flows for seed categories, and observed price direction in major producing regions. When a country total looked out of line, the assumptions were re-opened and rechecked, followed by a second-pass review to confirm that the adjustment did not create a mismatch elsewhere.

Before sign-off, a multi-step internal review is completed so calculation logic, units, and currency conversions are consistent across regions. The report is refreshed annually, and interim updates are triggered when material events occur, such as major policy shifts, sharp weather-led acreage swings, or notable seed pricing changes. Right before delivery, a fresh review pass is done so clients receive the latest updated view.

Mordor Intelligence's Global Forage Sorghum Seed Market Estimate Compared With Other Published Estimates

Published market values for forage sorghum seed can look far apart even when they sound like they measure the same thing, since firms do not always count the same seed uses, time windows, and price basis. Differences also come from how planting area is translated into seed demand, and whether figures are anchored to agronomy realities or to broad agriculture spending pools.

The benchmark table shows a wide spread mainly because some estimates appear to blend forage sorghum with adjacent sorghum seed uses and then stretch pricing with longer forecast windows, which changes the current year picture. In Mordor Intelligence's model, value is tied to forage-use planting only, and it is built from regional acreage-to-seed conversions with interview-checked seeding rates and price points, which helps avoid counting grain-oriented demand as forage seed revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.49 B (2026) | |

| Global Consultancy A | USD 1.13 B (2024) | Uses an earlier base year and a slower stated growth window, and the scope detail is limited, which can understate regions where hybrid adoption and pricing are higher. |

| Industry Publisher B | USD 3.27 B (2024) | Likely uses a broader definition with additional seed types and end uses, plus a wider demand pool that can fold in adjacent sorghum categories, which inflates the total versus forage-only planting. |

Taken together, the spread is best explained by scope boundaries, base-year selection, and how acreage, seeding rates, and price progression are treated. By keeping the calculation steps traceable to planting-driven demand signals and then rechecking assumptions through interviews, the final number stays practical to reproduce and easier to compare across regions year to year.

Key Questions Answered in the Report

How large is the forage sorghum seed market in 2026?

It is valued at USD 1.49 billion and is projected to reach USD 2.03 billion by 2031.

What is the anticipated CAGR for forage sorghum seed through 2031?

The market is forecast to grow at a 6.35% CAGR during 2026-2031.

Which region currently leads forage sorghum seed sales?

North America holds 31.70% of global sales, anchored by the United States Southern Plains.

Which region is growing fastest in forage sorghum seed adoption?

Africa is anticipated to register a 9.79% CAGR through 2031.

What makes forage sorghum attractive versus corn silage?

Sorghum delivers comparable feed value while using roughly 60% less water, supporting climate-resilient production, making sorghum attractive versus corn silage.

Page last updated on: