Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Market Size (2025) | USD 741.20 Million |

| Market Size (2030) | USD 993.80 Million |

| Growth Rate (2025 - 2030) | 6.04% CAGR |

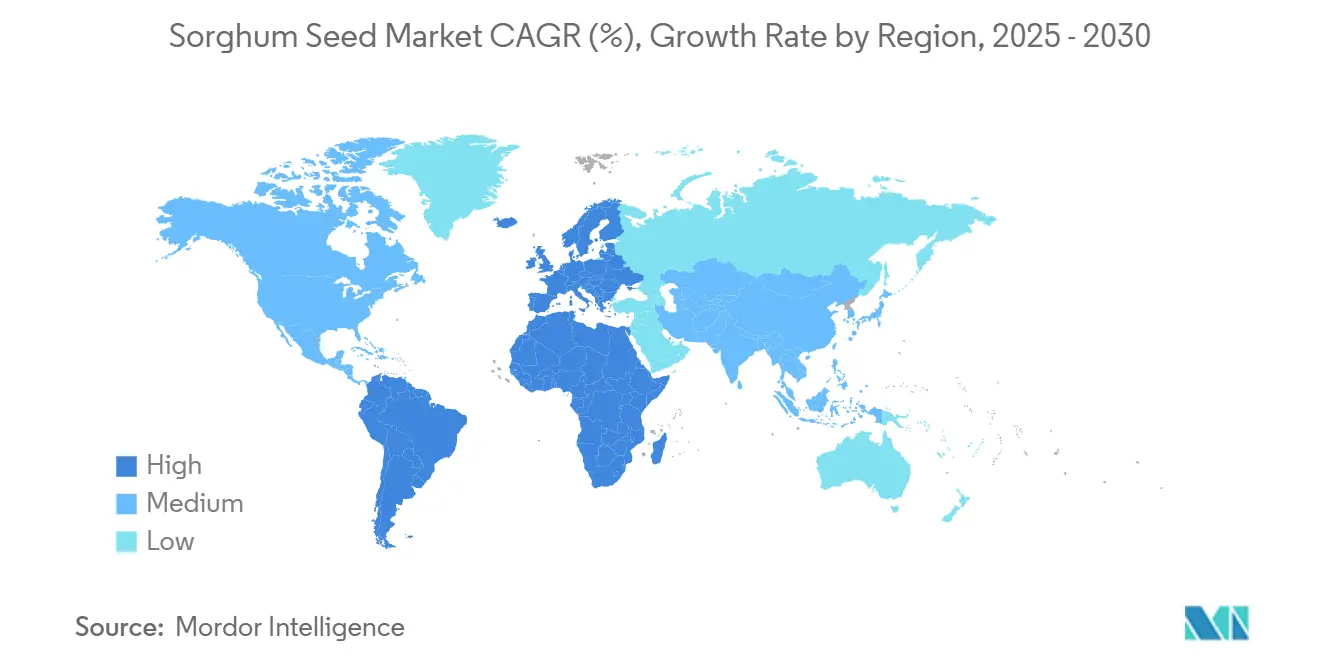

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sorghum Seed Market Analysis by Mordor Intelligence

The sorghum seed market size stands at USD 741.2 million in 2025 and is projected to reach USD 993.8 million by 2030, reflecting a 6.04% CAGR over 2025-2030. Current expansion rests on the crop’s dual use as both a food grain and an industrial feedstock, its innate drought tolerance, and its fit within climate-resilient farming systems. Rapid uptake in gluten-free packaged foods, widening use in first-generation and advanced bioethanol, and supportive public subsidies in drought-prone developing regions anchor near-term demand. Medium-term momentum will come from carbon-credit incentives tied to regenerative agriculture, while long-term growth will rely on hybrid genetics that deliver stable yields under erratic rainfall. Competitive strategy centers on marrying proprietary breeding with region-specific distribution, as acreage competition with corn and soybeans remains the single largest restraint.

Key Report Takeaways

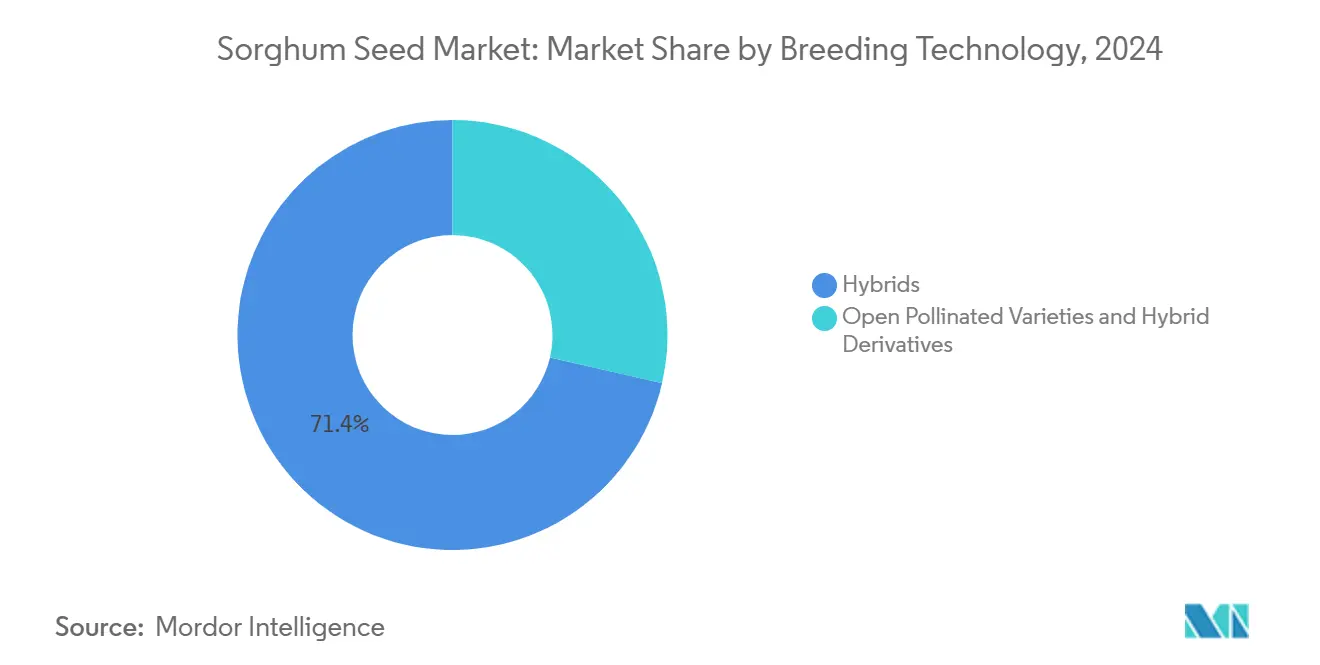

- By breeding technology, hybrids captured 71.4% sorghum seed market share in 2024 and are forecast to grow at 6.53% CAGR through 2030.

- By region, North America led with a 46.3% revenue share in 2024, while Europe is poised to expand at a 9.45% CAGR to 2030.

Global Sorghum Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for gluten-free grains in packaged foods | +1.2% | Global, high in North America and Europe | Medium term (2-4 years) |

| Growth in first-generation and advanced bioethanol mandates | +1.8% | North America, Brazil, and Europe | Long term (≥4 years) |

| Adoption of drought-tolerant crops amid climate volatility | +1.5% | Global, especially Africa and Asia-Pacific | Short term (≤2 years) |

| Public seed-replacement subsidies in Africa and South Asia | +0.9% | Sub-Saharan Africa, India, and Bangladesh | Medium term (2-4 years) |

| Expansion of sorghum use in pet food and aquaculture feed | +0.7% | Global, led by North America and Europe | Long term (≥4 years) |

| Regenerative-agriculture carbon-credit premiums | +0.4% | North America, Europe, and Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Gluten-Free Grains in Packaged Foods

Consumer interest in gluten-free wellness products has moved beyond a clinical need for celiac patients. Food processors now favor sorghum because its neutral flavor profile and nutrient density outperform traditional rice and corn substitutes. Contract premiums for white sorghum varieties create lucrative niches, and global regulatory clearances have removed commercial barriers. Seed firms respond by rolling out food-grade hybrids with higher protein and antioxidant levels, positioning the sorghum seed market for stable demand from breakfast cereals, snacks, and baked goods.

Growth in First-Generation and Advanced Bioethanol Mandates

Renewable-fuel blending targets in the United States, Brazil, and the European Union lock in demand for grain and biomass sorghum feedstocks.[1]Source: U.S. Environmental Protection Agency, “Renewable Fuel Standard Program Overview,” Environmental Protection Agency, epa.gov Sweet sorghum varieties enable dual-purpose harvesting of grain and stalk, improving farm economics on marginal land. Seed developers collaborate with biofuel processors to breed high-sugar, high-biomass hybrids, giving the sorghum seed market a steady offtake channel insulated from grain-only pricing cycles.

Adoption of Drought-Tolerant Crops Amid Climate Volatility

Sorghum’s water-use efficiency and ability to pause growth during drought confer a production edge over water-intensive cereals. Financial institutions increasingly factor crop drought resilience into loan underwriting, nudging farmers toward sorghum seed purchases. Public extension programs multiply the effect by showcasing side-by-side yield stability trials, accelerating early adoption in Asia-Pacific and Africa.

Public Seed-Replacement Subsidies in Africa and South Asia

Government schemes that reimburse up to 50% of hybrid seed costs transform traditional seed-saving regions into commercial seed buyers.[2]Source: Food and Agriculture Organization, “Smallholder seed systems and food security in developing countries,” Food and Agriculture Organization, fao.org International breeders now establish local stations to supply subsidy-eligible cultivars, linking technology transfer with local employment. Success hinges on last-mile distribution, prompting seed companies to invest in rural dealer training and demonstration plots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense acreage competition from corn and soybean | -2.1% | North America, South America, and Europe | Short term (≤2 years) |

| Seed-saving culture among smallholders limits hybrid sales | -1.2% | Africa, Asia-Pacific | Medium term (2-4 years) |

| Sub-optimal private R&D spending on sorghum traits | -0.8% | Global | Long term (≥4 years) |

| Stricter phytosanitary import rules for weed-seed contamination | -0.6% | Global trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Acreage Competition from Corn and Soybean

Higher per-acre returns from corn grain and soybean protein depress sorghum planting intentions in the world’s most productive zones.[3]Source: U.S. Department of Agriculture Economic Research Service, “Commodity Costs and Returns: Crop Production Costs and Returns,” United States Department of Agriculture, ers.usda.gov Grain elevators and transport corridors also favor corn-soy flows, forcing sorghum marketers to accept negative basis levels that erode farm-gate prices. Policy tweaks have narrowed insurance disparities, yet economic headwinds persist.

Sub-Optimal Private Research and Development Spending on Sorghum Traits

Global research budgets still skew toward larger crops, slowing transgenic and gene-edited trait rollouts in sorghum. Public institutes fill part of the gap, but commercialization lags without proprietary investment. The resulting innovation deficit tempers farmer enthusiasm, particularly for herbicide-tolerant packages commonplace in competing crops.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Sustain Premium Growth

Hybrids controlled 71.4% of the sorghum seed market in 2024 and are projected to advance at 6.53% CAGR to 2030, reflecting steady farmer preference for yield reliability under drought stress. Within hybrids, non-transgenic lines dominate because approval pathways for genetically modified sorghum remain complex in many importing nations. The segment’s revenue is highly sensitive to commodity price spreads, when corn prices fall relative to sorghum, hybrid adoption accelerates as growers seek risk mitigation. In contrast, open-pollinated varieties retain importance among smallholders who view seed re-purchase as unaffordable. Yield gaps of 15-20% versus hybrids persist, but improved open-pollinated breeding has narrowed the margin and strengthened the value proposition for cash-limited farmers.

Hybrid derivatives, including forage and sweet sorghum lines, expand the sorghum seed market size in specialized end-use streams such as livestock feed and bioethanol. Seed firms deploy marker-assisted selection to stack drought and standability traits, ensuring lodging resistance during high-biomass growth phases. Premium prices for sweet sorghum seed underpin breeder investment despite limited acreage, while forage sorghum gains in dairy regions where summer water restrictions cut corn silage output. As regulatory clarity around gene-editing advances, the segment may pivot toward (Clustered Regularly Interspaced Short Palindromic Repeats) CRISPR-edited lines that deliver pest tolerance without transgenic DNA.

Geography Analysis

North America held 46.3% of 2024 revenue, supported by Kansas, Texas, and Nebraska’s grain-sorghum corridor that seamlessly channels production into livestock feedlots and ethanol refineries. North America’s dominance stems from robust infrastructure and well-defined end-use channels. United States sorghum acreage clusters in the western Corn Belt, where annual rainfall often falls below corn’s evapotranspiration needs. Federal Conservation Reserve incentives now credit sorghum’s soil-building properties, adding an ecological revenue stream. Mexico’s northern states expand acreage to feed burgeoning poultry and swine complexes, leveraging hybrid imports through streamlined phytosanitary alignment with U.S. protocols.

Europe, though smaller today, posts the fastest regional growth at a 9.45% CAGR through 2030 as Common Agricultural Policy (CAP) reforms incentivize crop diversification. Europe’s rapid growth aligns with CAP eco-schemes that reward nitrogen-efficient and drought-resilient crops. France and Germany sponsor agronomy trials that compare sorghum water productivity against maize, and the findings favor sorghum in regions with summer water restrictions. Demand also rises from specialty human-food segments, where processors value sorghum’s allergen-free status.

Africa occupies a paradoxical position: vast agro-ecological suitability yet constrained commercial uptake. Nigeria and Ethiopia push hybrid demonstration projects, while South Africa’s commercial farms integrate high-sugar hybrids for rum distillation. Nevertheless, fragmented distribution and limited rural liquidity slow the sorghum seed market expansion. International seed companies collaborate with regional partners to shorten supply chains and localize seed production, addressing phytosanitary and logistics bottlenecks.

Competitive Landscape

The top five breeders, Corteva Agriscience, KWS SAAT SE, and others, command a modest share of global sales, defining a moderately concentrated field. Corteva leads with genomic-selection pipelines that speed hybrid release cycles by one year relative to conventional methods. Bayer’s joint venture with the International Crops Research Institute for the Semi-Arid Tropics (ICRISAT) exemplifies public-private alignment to tailor hybrids for African smallholders. KWS expands into tropical germplasm via its 2025 Sementes Biomatrix acquisition, strengthening South American positioning.

Mid-tier and regional players fill niche gaps. Advanta focuses on high-lysine forage sorghum, while Takii targets sweet sorghum for Japanese bioethanol ventures. Royal Barenbrug drills into European forage segments, and S&W Seed Company scales Australian production to serve both domestic and Middle East buyers. Intellectual-property activity signals intensifying rivalry: sorghum-related patent applications rose 40% in 2024. Gene editing promises faster trait stacking, yet disparate regulatory regimes introduce commercialization risk, tempering near-term deployment.

Strategically, companies pursue integrated models: breeding, seed multiplication, and downstream partnerships with biofuel refineries or pet-food processors. This vertical reach locks in demand and informs trait prioritization. As phytosanitary compliance costs escalate, anticipate selective acquisitions of smaller firms whose local germplasm and distribution networks lower regulatory friction.

Sorghum Seed Industry Leaders

Corteva Agriscience

KWS SAAT SE & Co. KGaA

Land O’Lakes Inc.

RAGT Group

Advanta Seeds (UPL Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Haryana Agricultural University has developed a new sweet sorghum variety named CSV 64-F, which offers high biomass yield and sugar content. This variety is tailored for ethanol production and supports sustainable bioenergy initiatives in India.

- October 2024: International Crops Research Institute for the Semi-Arid Tropics (ICRISAT) and the Sher-e-Kashmir University of Agricultural Sciences and Technology (SKUAST) have co-developed the first cold-tolerant sorghum variety tailored for Jammu and Kashmir, enabling cultivation in temperate zones. This breakthrough supports climate-resilient agriculture and expands sorghum’s geographic reach in India.

Global Sorghum Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Region

| Africa | By Breeding Technology | |

| By Country | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

| Asia-Pacific | By Breeding Technology | |

| Australia | ||

| Bangladesh | ||

| China | ||

| India | ||

| Myanmar | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Europe | By Breeding Technology | |

| France | ||

| Germany | ||

| Italy | ||

| Romania | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| Rest of Europe | ||

| Middle East | By Breeding Technology | |

| Iran | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Breeding Technology | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Breeding Technology | |

| Argentina | ||

| Brazil | ||

| Rest of South America | ||

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Region | Africa | By Breeding Technology | |

| By Country | Egypt | ||

| Ethiopia | |||

| Ghana | |||

| Kenya | |||

| Nigeria | |||

| South Africa | |||

| Tanzania | |||

| Rest of Africa | |||

| Asia-Pacific | By Breeding Technology | ||

| Australia | |||

| Bangladesh | |||

| China | |||

| India | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Europe | By Breeding Technology | ||

| France | |||

| Germany | |||

| Italy | |||

| Romania | |||

| Russia | |||

| Spain | |||

| Ukraine | |||

| Rest of Europe | |||

| Middle East | By Breeding Technology | ||

| Iran | |||

| Saudi Arabia | |||

| Rest of Middle East | |||

| North America | By Breeding Technology | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Breeding Technology | ||

| Argentina | |||

| Brazil | |||

| Rest of South America | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms