Flow Control in Semiconductor Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

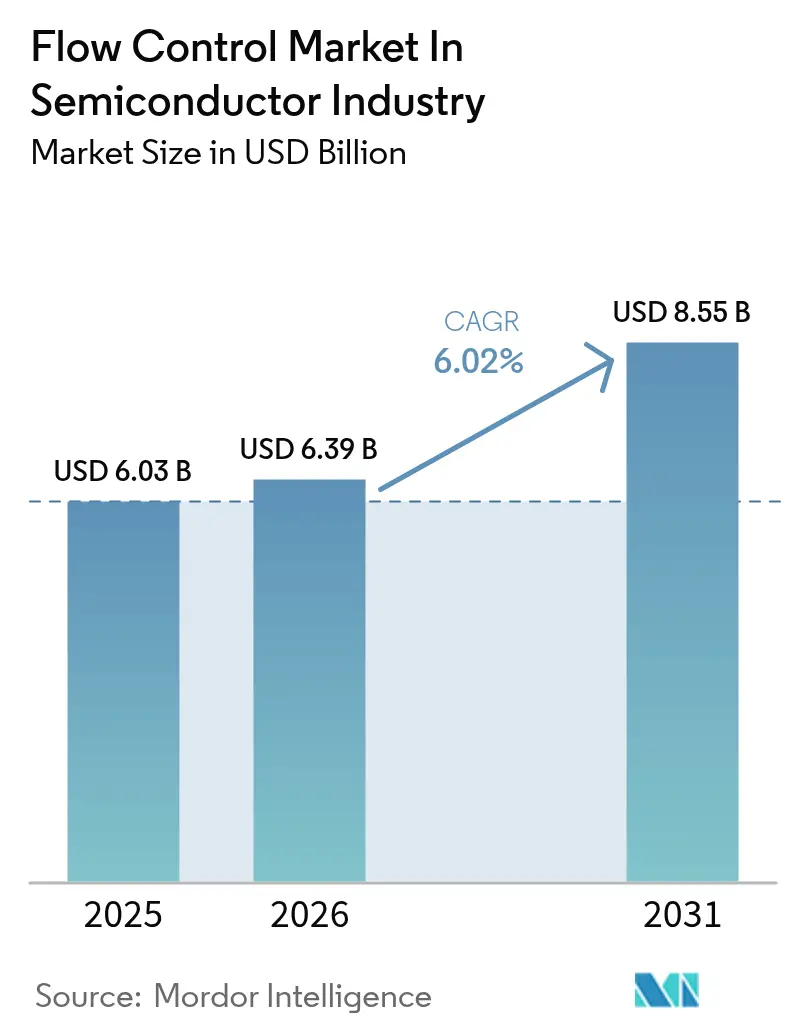

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 8.55 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flow Control in Semiconductor Industry Analysis by Mordor Intelligence

Flow control market size in semiconductor industry market size in 2026 is estimated at USD 6.39 billion, growing from 2025 value of USD 6.03 billion with 2031 projections showing USD 8.55 billion, growing at 6.02% CAGR over 2026-2031. This expansion mirrors the sector’s capital-intensive build-out, highlighted by TSMC’s USD 42 billion outlay for nine new fabs in 2025. Extreme ultraviolet (EUV) lithography adoption is the primary growth catalyst because it demands vacuum levels below 10⁻⁹ torr that legacy equipment cannot sustain, prompting widespread upgrades to ultra-high-purity valves, pumps, and sealing systems. Regional diversification is also boosting demand: SEMI tracks 18 new fabs starting construction in 2025, with the Americas and Japan leading at four projects each. Suppliers that offer localized service, rapid spares provisioning, and PFAS-free solutions gain clear competitive advantages as environmental rules tighten. Nonetheless, supply-chain fragility illustrated by Hurricane Helene’s hit to Spruce Pine quartz, which supports 70-90% of global high-purity quartz volumes remains a key risk

Key Report Takeaways

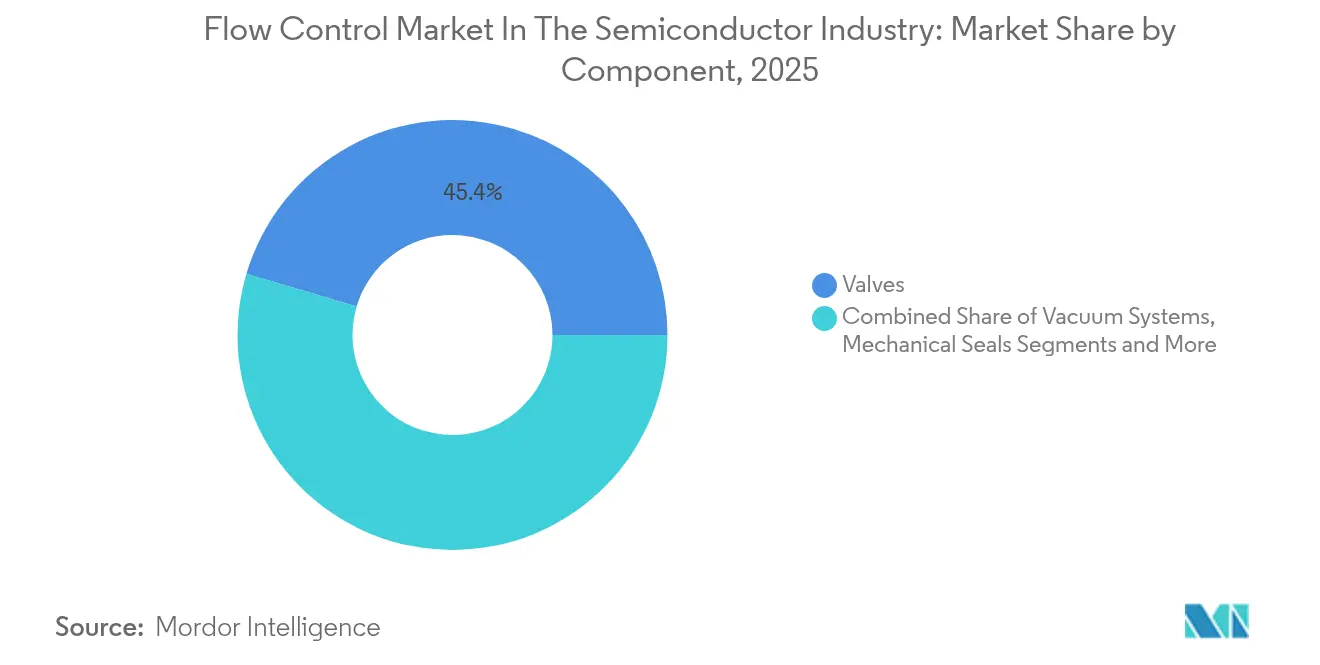

- By component, valves led with 45.40% revenue share in 2025, while vacuum systems are projected to expand at a 6.95% CAGR through 2031.

- By process step, deposition processes accounted for 20.80% of total demand in 2025; lithography is forecast to accelerate at an 7.6% CAGR to 2031.

- By flow medium, gas applications generated the highest 2025 revenue, whereas liquid-handling systems are expected to log the fastest growth rate (exact CAGR not disclosed) during 2026-2031.

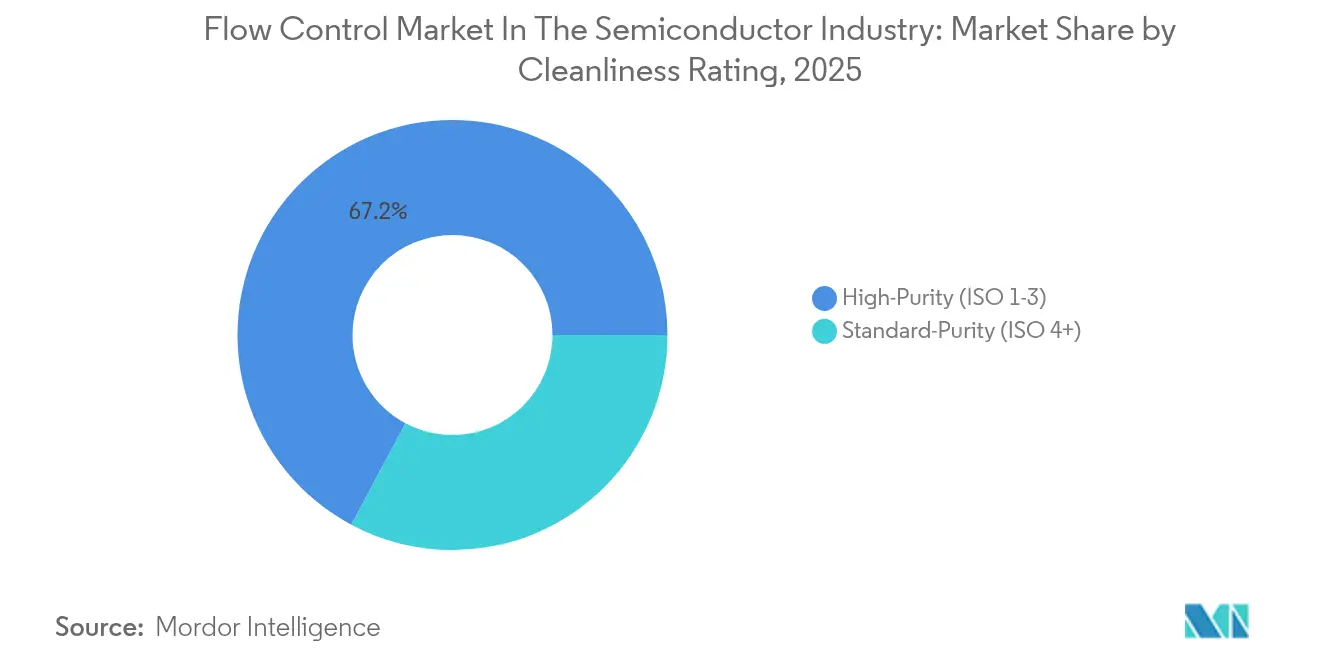

- By cleanliness rating, ISO 1-3 high-purity solutions captured the largest 2025 share and are also anticipated to post the strongest double-digit CAGR (exact figure not disclosed) through 2031.

- By valve actuation type, pneumatic valves held the majority share in 2025, while electric actuation is projected to record the highest CAGR (exact figure not disclosed) over the forecast period.

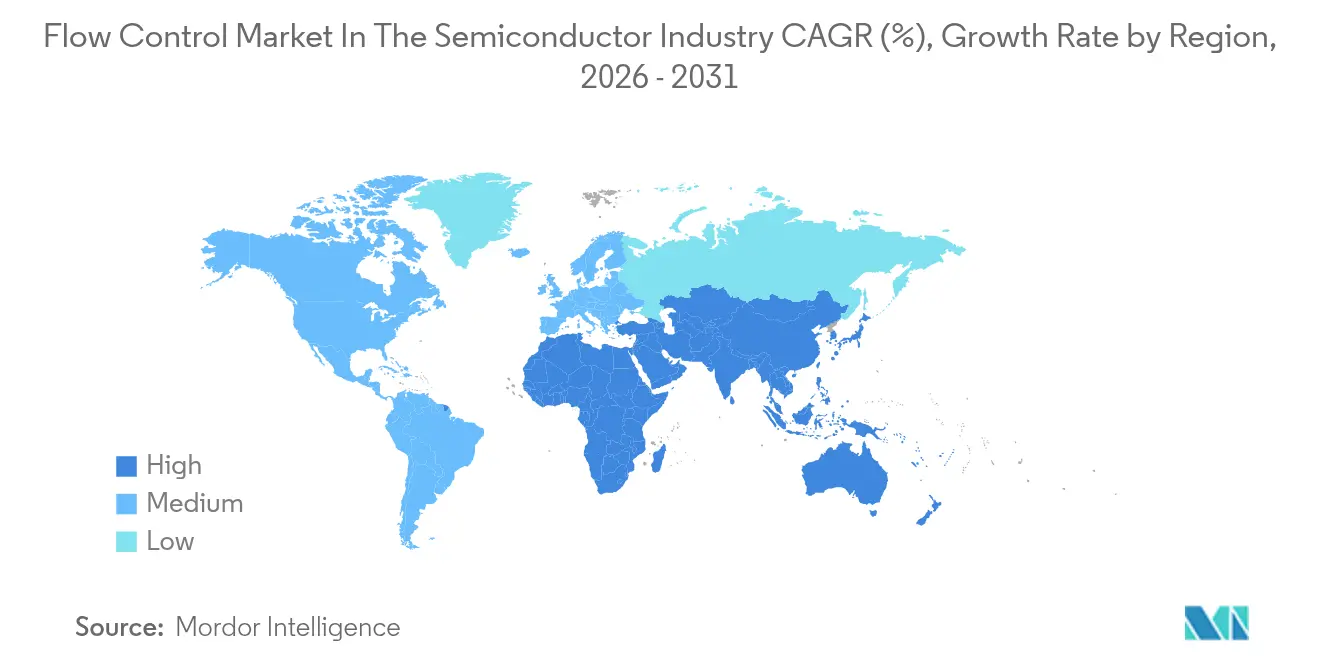

- By geography, Asia-Pacific commanded 33.60% of the semiconductor fluid handling market share in 2025, whereas South America is set to grow at the fastest 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flow Control in Semiconductor Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive EUV Lithography Vacuum Requirements in Korean and Taiwanese Fabs | +1.8% | Asia-Pacific core, spill-over to Americas | Medium term (2-4 years) |

| 3D-NAND Transition Beyond 200 Layers Boosting High-Flow ALD Valves (China) | +1.2% | China primary, global secondary | Long term (≥ 4 years) |

| U.S. CHIPS Act Fab Build-out Raising Chemical-Distribution Valve Demand | +1.4% | North America primary, allied nations secondary | Medium term (2-4 years) |

| Dry Vacuum Pump Adoption to Meet PFAS-Emission Rules (Japan) | +0.9% | Japan primary, EU secondary | Short term (≤ 2 years) |

| Hybrid-Bonding Packaging Needs Sub-1 Torr Micro-Flow Controls (Global) | +0.7% | Global | Long term (≥ 4 years) |

| IIoT-Enabled Smart Valves for Predictive Maintenance (Europe) | +0.6% | Europe primary, global adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive EUV Lithography Vacuum Requirements in Korean and Taiwanese Fabs

Korean and Taiwanese semiconductor manufacturers are driving unprecedented demand for ultra-high vacuum fluid handling systems as they scale EUV lithography capacity. TSMC's transition to High-NA EUV technology requires vacuum levels below 10^-11 torr, demanding specialized valve configurations that prevent hydrocarbon contamination during photoresist processing. Samsung's EUV roadmap includes 15 new EUV scanners by 2026, each requiring dedicated fluid handling infrastructure worth approximately USD 2-3 million per tool. The technical complexity stems from EUV's sensitivity to molecular contamination, where even trace amounts of organic compounds can degrade mirror reflectivity and reduce lithography yield.[1] ASML Public Affairs, “High-NA EUV Roadmap Details,” Asml.com

3D-NAND Transition Beyond 200 Layers Boosting High-Flow ALD Valves (China)

China's aggressive pursuit of 3D-NAND technology beyond 200 layers is creating substantial demand for high-flow atomic layer deposition valves capable of handling precursor delivery at unprecedented scales. YMTC's development of 232-layer 3D-NAND requires ALD processes with deposition rates exceeding 50 nm/hour, necessitating valve systems with flow rates 3-4 times higher than conventional 128-layer processes. The technical challenge lies in maintaining precursor uniformity across 300mm wafers while preventing cross-contamination between different chemical species. Chinese manufacturers are investing heavily in domestic fluid handling capabilities to reduce dependence on foreign suppliers, with companies like NAURA and AMEC developing indigenous valve technologies. However, the transition faces significant hurdles in high-purity material sourcing, as China imports over 80% of its fluoro-elastomer seals from Japanese and German suppliers.

U.S. CHIPS Act Fab Build-out Raising Chemical-Distribution Valve Demand

The U.S. CHIPS and Science Act is catalyzing unprecedented domestic semiconductor manufacturing expansion, driving substantial demand for chemical distribution valve systems across new fabrication facilities. GlobalFoundries announced a USD 16 billion investment to enhance U.S. chip manufacturing capabilities, with significant portions allocated to fluid handling infrastructure. Intel's foundry expansion includes specialized chemical delivery systems for advanced packaging processes, requiring valve configurations that can handle both traditional solvents and emerging materials like low-k dielectrics. The Act's emphasis on supply chain resilience is reshaping procurement strategies, with domestic content requirements driving partnerships between U.S. valve manufacturers and established equipment suppliers.

Dry Vacuum Pump Adoption to Meet PFAS-Emission Rules (Japan)

Japanese semiconductor manufacturers are accelerating adoption of dry vacuum pump systems to comply with increasingly stringent PFAS emission regulations, fundamentally altering fluid handling system architectures. The Japanese government's PFAS phase-out timeline requires elimination of perfluorooctanoic acid and related compounds from semiconductor processes by 2026, forcing manufacturers to redesign vacuum systems that traditionally relied on fluorinated lubricants. Tokyo Electron and other equipment manufacturers are developing alternative pump technologies using magnetic bearings and ceramic seals to eliminate PFAS-containing components entirely. The transition presents significant technical challenges, as dry vacuum systems typically exhibit lower pumping speeds and higher maintenance requirements compared to oil-sealed alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU PFAS Phase-Out Proposals Increasing Material Redesign Costs | -0.8% | Europe primary, global secondary | Short term (≤ 2 years) |

| Tight High-Purity Fluoro-Elastomer Supply Inflating Seal Prices | -1.1% | Global | Medium term (2-4 years) |

| Capex-Intensive Ultra-High-Vacuum Valves Limiting Adoption in South America | -0.4% | South America primary, emerging markets secondary | Long term (≥ 4 years) |

| 18-24 Month Qualification Cycles with Tier-1 Tool OEMs | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU PFAS Phase-Out Proposals Increasing Material Redesign Costs

EU plans to remove 4,000 fluorinated compounds by 2029, forcing valve makers to substitute DuPont Kalrez and similar seals. European firms report 40–80% higher material costs and 18–24 month qualification cycles while also navigating Dutch export controls effective April 2025.[2]Netherlands Ministry of Foreign Affairs, “Export Control Update April 2025,” Government.nl

Tight High-Purity Fluoro-Elastomer Supply Inflating Seal Prices

Global supply constraints in high-purity fluoro-elastomer materials are creating significant cost inflation pressures across the semiconductor fluid handling market, with seal prices increasing 25-35% since 2024. The supply bottleneck stems from limited production capacity concentrated among a few Japanese and German manufacturers, combined with Hurricane Helene's disruption of critical raw material supplies from North Carolina quartz mines. Sibelco and The Quartz Corp's temporary shutdown eliminated 70-90% of the world's high-purity quartz supply, creating cascading effects throughout the semiconductor materials supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Valves Sustain Leadership while Vacuum Systems Accelerate

Valves held 45.40% semiconductor fluid handling market share in 2025. Vacuum system revenue is rising at a 6.95% CAGR because EUV lithography and advanced packaging rely on ultra-high vacuum.

Demand for all-metal gate valves able to hold leak rates below 10⁻¹² mbar·l/s grows quickly, with VAT and Fujikin leading adoption. The semiconductor fluid handling market size for vacuum systems is poised to expand fastest, supported by new dry pumps with magnetic bearings that reach 2,000 l/s and exceed 50,000 hours MTBF.

Suppliers increasingly bundle valves, pumps, and mass-flow controllers in modular skids that cut fab install time by 30%. Predictive analytics embedded in smart valves improve throughput and extend seal life, reducing total cost of ownership for fab operators. R&D focus has shifted toward PFAS-free elastomers and electropolished wetted paths that meet ISO-1 cleanliness.

By Process Step: Deposition Dominates as Lithography Becomes High-Velocity

Deposition processes generated 20.80% of 2025 revenue, while lithography is growing at 7.6% CAGR and becoming the fastest driver of semiconductor fluid handling market demand.

Atomic-layer deposition requires millisecond valve switching with parts-per-billion impurity control. Selective deposition platforms from Applied Materials must alternate precursors rapidly, necessitating advanced valve manifolds. Conversely, the semiconductor fluid handling market size for lithography tools increases alongside High-NA EUV because contamination-free photoresist lines directly impact yield.

Etch, ion implant, and wet clean remain essential but mature; upgrades here primarily follow capacity additions. Load-lock upgrades tied to automated material transfer are experiencing renewed investment as 300 mm automation spreads to 200 mm fabs seeking productivity gains.

By Flow Medium: Gas Systems Dominate while Liquid Applications Grow

Gas management leads the semiconductor fluid handling market because deposition, etch, and clean steps rely on diverse gas chemistries. Liquid handling is smaller yet rising due to aggressive cleans and emerging liquid immersion exploratory projects in EUV.

Smart gas valves such as Emerson’s Sentronic series deliver control deviation under 0.5% with integrated data capture. On the liquid side, hybrid bonding packaging needs high-purity adhesive dispenses, spurring demand for corrosion-resistant pumps.

Improved data analytics enable sub-second flow correction, reducing process drift and boosting wafer yield. Suppliers develop application-specific alloys and coatings that endure fluorine exposure while minimizing metal ion leach-out.

By Cleanliness Rating: High-Purity Systems Capture Premium Spending

ISO 1-3 high-purity solutions outpace standard utility lines and command 3-5× pricing. Customers increasingly standardize on higher purity for all critical steps to eliminate yield loss risk.

SEMI E49.6 documentation requirements raise entry barriers and favor incumbent suppliers with proven ISO-1 fabrication and cleaning lines. Swagelok’s electropolished gas valves exemplify the premium segment. The semiconductor fluid handling market size associated with high-purity skids grows in parallel with advanced-node capacity.

By Valve Actuation Type: Pneumatic Retains Scale as Electric Gains Momentum

Pneumatic actuation is prevalent in legacy fabs for speed and reliability; however, electric actuators show the highest growth rate as sites aim to cut compressed-air energy demand.

Festo’s servo-controlled electric units deliver 0.1 mm accuracy and stream live diagnostic data, enabling true predictive maintenance. Energy efficiency programs push fabs toward electric or hybrid actuation to reduce pneumatic consumption, previously 15–20% of plant power draw.

Geography Analysis

Asia-Pacific held 33.60% semiconductor fluid handling market share in 2025, anchored by Taiwan and South Korea. TSMC’s nine-fab expansion and Samsung’s EUV scale-up are foremost demand engines. China remains a colossal growth prospect despite export controls, with YMTC and SMIC building indigenous supply chains. Japan’s equipment sector and materials expertise also sustain high valve and pump requirements. North America enjoys renewed momentum through the CHIPS Act. Intel, Micron, and GlobalFoundries projects each require USD 150–200 million in fluid systems, fostering regional clusters that shorten lead times and bolster resilience. Europe’s market confronts PFAS restrictions that inflate material redesign costs yet also create competitive moats for compliant suppliers; ASML’s Dutch base sustains specialized orders for EUV-ready components.

South America, led by Brazil, registers the fastest 7.55% CAGR as governments court semiconductor assembly and test investments to diversify supply chains. Infrastructure gaps and skills shortages remain hurdles but targeted incentives and multinational partnerships are stimulating incremental demand for modular, lower-cost fluid handling packages suited to emerging fab environments.

Competitive Landscape

The semiconductor fluid handling market shows moderate fragmentation. Vacuum pumps are concentrated with Edwards Vacuum, ULVAC, and Pfeiffer Vacuum, while valves are more dispersed among VAT, Fujikin, Swagelok, and regional specialists. Long qualification cycles and critical process roles create high switching barriers that stabilize supplier relationships.

Technology leadership now revolves around smart valves, predictive diagnostics, and PFAS-free materials. Suppliers pursue vertical integration to secure elastomers and precision machining capacity. Platform approaches that pre-assemble skids cut installation time and simplify procurement.

Collaborations between equipment OEMs and research institutes, such as ASML-imec, accelerate innovation in High-NA EUV support systems. Emerging niches—including quantum device processing and advanced heterogeneous packaging—offer white-space opportunities for agile entrants that can meet sub-ppm contamination thresholds and unique flow profiles.

Flow Control in Semiconductor Market Leaders

VAT Vakuumventile AG

Pfeiffer Vacuum GmbH

Atlas Copco

Flowserve Corporation

ULVAC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TSMC and University of Tokyo launched the TSMC-UTokyo Lab to enhance semiconductor research and education, marking TSMC's first university collaboration outside Taiwan. The lab will focus on materials, devices, processes, metrology, packaging, and circuit design research, with results contributing to TSMC's R&D and manufacturing capabilities while fostering next-generation semiconductor talent.

- June 2025: GlobalFoundries announced a USD 16 billion investment to reshore essential chip manufacturing in the U.S., aimed at accelerating AI growth and enhancing domestic semiconductor production capabilities. This initiative includes significant improvements in fluid handling processes critical for advanced semiconductor manufacturing.

- May 2025: Infineon Technologies introduced trench-based SiC superjunction technology, enhancing its CoolSiC product line for automotive drivetrains, EV charging, and energy systems. The technology enables higher efficiency and compact designs, with first products being 1200V ID-PAK packages for automotive traction inverters, with volume production expected in 2027.

- May 2025: Chemours announced a strategic agreement with Navin Fluorine to manufacture Opteo two-phase immersion cooling fluid for advanced data centers and AI hardware. The collaboration addresses growing demands for heat and energy management in data centers, with the fluid featuring ultra-low global warming potential and significantly reduced water and energy consumption.

Global Flow Control in Semiconductor Industry Report Scope

Flow controllers are electronic devices that monitor and maintain flow rate variables in process applications. They can be utilized in fluid flow systems with pumps and valves to enable greater control of flow variables. Dry vacuum pumps are essential in the semiconductor manufacturing process. Gases are injected into a chamber to react and produce a layer on the surface of a silicon wafer. The pump's job is to maintain a constant low pressure in the chamber to aid in forming the film.

The global flow control market in the semiconductor industry is segmented by type of component (vacuum, valves (ball, butterfly, gate, globe, and other valves), and mechanical seals) and country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Vacuum Systems | |

| Valves | Ball |

| Butterfly | |

| Gate | |

| Globe | |

| Other Valves | |

| Mechanical Seals | |

| Mass Flow Controllers | |

| Flow Meters |

| Deposition (PVD / CVD / ALD) |

| Etching and Dry Strip |

| Ion Implantation |

| Lithography |

| Wafer Cleaning and CMP |

| Metrology and Inspection |

| Load Lock and Transfer |

| Water and Waste Treatment |

| Gases |

| Liquids |

| High-Purity (ISO 1-3) |

| Standard-Purity (ISO 4+) |

| Manual |

| Pneumatic |

| Electric |

| Solenoid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Netherlands | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| South Korea | |

| Australia | |

| Japan | |

| India | |

| Southeast Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Africa | South Africa |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Vacuum Systems | |

| Valves | Ball | |

| Butterfly | ||

| Gate | ||

| Globe | ||

| Other Valves | ||

| Mechanical Seals | ||

| Mass Flow Controllers | ||

| Flow Meters | ||

| By Process Step | Deposition (PVD / CVD / ALD) | |

| Etching and Dry Strip | ||

| Ion Implantation | ||

| Lithography | ||

| Wafer Cleaning and CMP | ||

| Metrology and Inspection | ||

| Load Lock and Transfer | ||

| Water and Waste Treatment | ||

| By Flow Medium | Gases | |

| Liquids | ||

| By Cleanliness Rating | High-Purity (ISO 1-3) | |

| Standard-Purity (ISO 4+) | ||

| By Valve Actuation Type | Manual | |

| Pneumatic | ||

| Electric | ||

| Solenoid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Netherlands | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| South Korea | ||

| Australia | ||

| Japan | ||

| India | ||

| Southeast Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Africa | South Africa | |

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the semiconductor fluid handling market size in 2026?

The market stands at USD 6.39 billion in 2026.

What compound annual growth rate (CAGR) is forecast for 2026-2031?

A 6.02% CAGR is projected, taking the market to USD 8.55 billion by 2031.

Which component holds the largest share of the market?

Valves lead with 45.40% of semiconductor fluid handling market share in 2025.

How does EUV lithography affect demand for fluid handling equipment?

EUV tools require ultra-high vacuum levels below 10⁻⁹ torr, driving purchases of advanced valves, pumps, and high-purity seals.

Which geographic region is growing the fastest?

South America shows the quickest expansion at a 7.55% CAGR through 2031.

How are PFAS regulations shaping new product development?

Tightening PFAS bans, especially in Japan and the EU, are accelerating the shift to dry vacuum pumps and PFAS-free sealing materials.

Page last updated on: