Epoxy Flooring Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

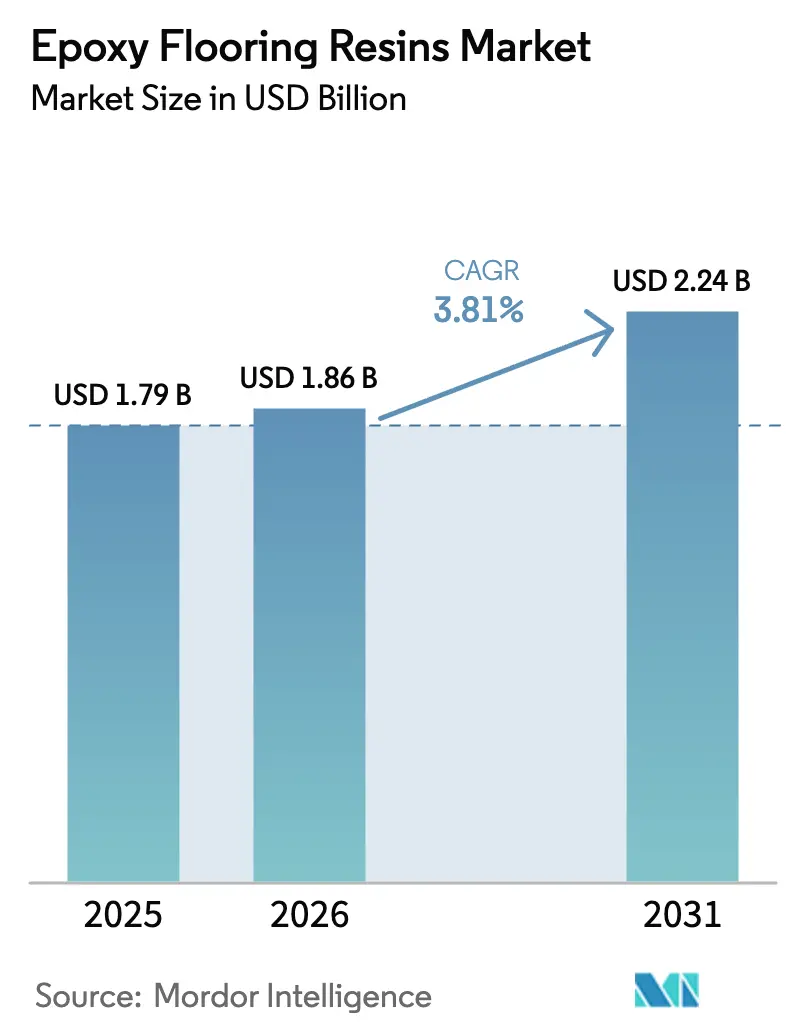

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

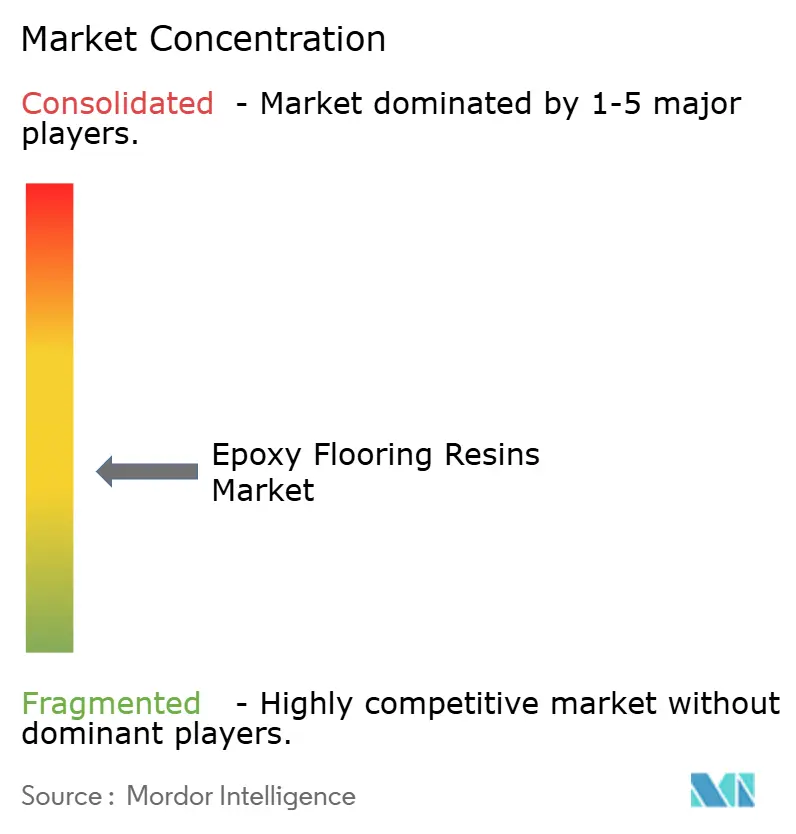

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epoxy Flooring Resins Market Analysis by Mordor Intelligence

The Epoxy Flooring Resins market size is expected to grow from USD 1.79 billion in 2025 to USD 1.86 billion in 2026 and is forecast to reach USD 2.24 billion by 2031 at 3.81% CAGR over 2026-2031. Demand remains firm as retrofit activity accelerates in pharmaceutical and food plants, while government-funded logistics and EV-battery megaprojects favor the technology’s long service life over initial cost savings. Competitive pressures from alternative chemistries and fluctuations in raw-material supply chains temper headline growth, yet innovations in low-VOC products and mandates for carbon-neutral construction keep the epoxy flooring resins industry firmly on an expansion path. Contractors’ dominance in system specification and installation entrenches technical service as a primary differentiator, and vertical integration remains the leading strategy for shielding margins from the volatility of bisphenol-A and epichlorohydrin.

Key Report Takeaways

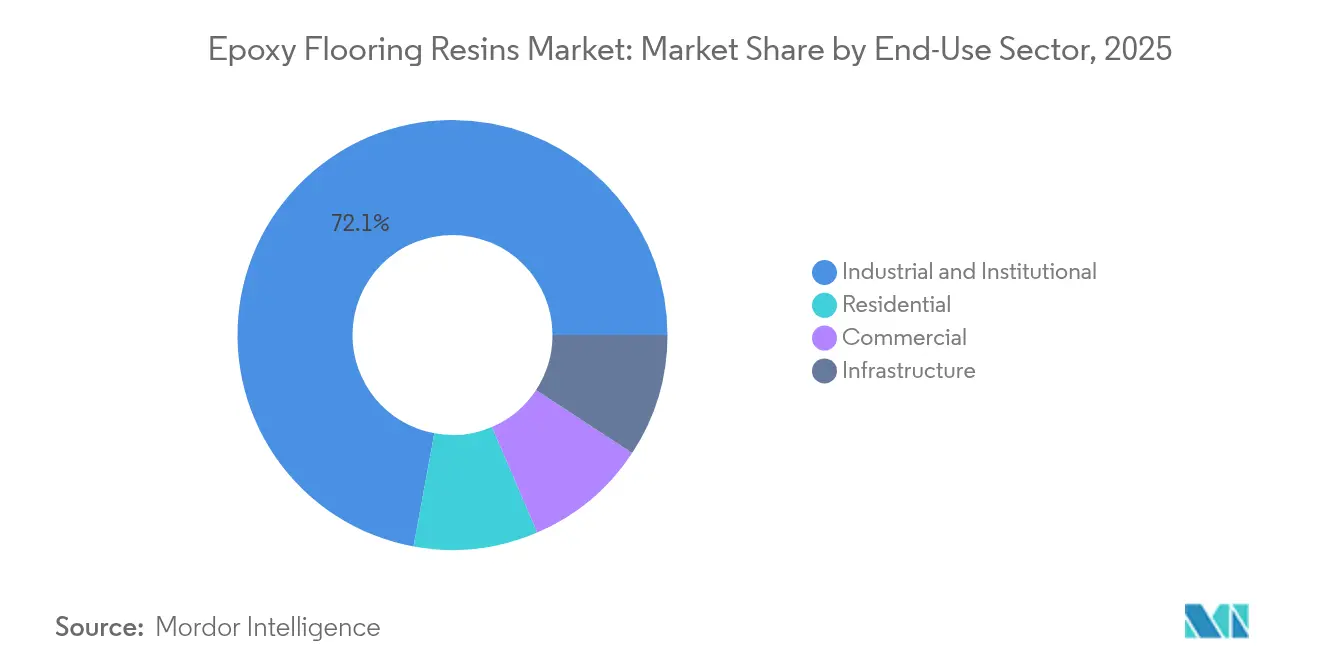

- By end-use sector, Industrial and Institutional applications led with 72.10% of the Epoxy Flooring Resins market share in 2025; commercial usage is projected to post the fastest CAGR of 4.33% through 2031.

- By distribution channel, the Direct/Contractor route accounted for 93.65% of the Epoxy Flooring Resins market in 2025, while it's expected to grow at a CAGR of 3.88% during the forecast period (2026-2031).

- By geography, Asia-Pacific captured 41.00% revenue in 2025; Middle East & Africa is set to advance at a 3.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epoxy Flooring Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating retro-fit demand for hygienic, seamless floors in food and pharma plants | +0.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Government-funded megaprojects in logistics and EV-battery factories | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Shift to low-VOC 100%-solids and water-borne epoxy systems | +0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Anti-dumping duties on Asian epoxy resins tightening Western supply | +0.3% | North America & EU | Short term (≤ 2 years) |

| Carbon-neutral construction mandates favouring longer-life epoxy floors | +0.5% | Global, led by EU regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Retrofit Demand for Hygienic, Seamless Floors in Food and Pharma Plants

Pharmaceutical cleanrooms and USDA-regulated food facilities are replacing legacy tile and vinyl flooring with seamless, antimicrobial epoxy floors to meet increasingly stringent contamination control requirements. Ford’s BlueOval SK Battery Park integrated 1.8 million ft² of specialized epoxy systems validated for particulate and chemical resistance, demonstrating how large-scale industrial investments now embed flooring into upfront compliance planning. The epoxy flooring resins market gains pricing power because owners prioritize proven, certified systems over low-bid options. Many North American and European plants built in the 1990s are now reaching the end of their lifespans, causing a synchronized replacement cycle as regulators intensify audits. Meanwhile, epoxy suppliers that pair documentation packages with contractor training secure repeat business.

Government-Funded Megaprojects in Logistics and EV-Battery Factories

Sovereign wealth and industrial policy are redirecting capital toward export logistics parks and battery gigafactories that demand chemical-resistant, electrostatic-safe floors. Oman’s SOHAR Port polymer complex typifies Middle Eastern diversification initiatives, each specifying 20-year warranties that only premium epoxy systems can meet[1]TRADEARABIA, “SOHAR Port Polymer Complex Breaks Ground,” tradearabia.com. These projects often exceed 500,000 ft² per facility, generating sudden spikes in regional resin consumption that test installer capacity. In the Asia-Pacific region, subsidies for EV supply chains concentrate multiple plants within a single province, anchoring long-term demand for advanced epoxy chemistries that can tolerate electrolyte spills and thermal cycling.

Shift to Low-VOC 100%-Solids and Water-Borne Epoxy Systems

The US EPA’s 2025 embodied-carbon label pushes owners to select low-emission coatings, accelerating a chemistry transition already underway in Europe. Modern water-borne dispersions reduce VOCs by 90% while achieving compressive strength parity with solvent-based types, thereby widening their acceptance in hospitals and schools. Formulating these systems requires precise particle-size control and surfactant optimization, skills that are often concentrated among vertically integrated suppliers. The learning curve for contractors remains a hurdle; extended cure windows and altered flow properties necessitate retraining, giving resin makers with robust field-support teams a competitive advantage. As the epoxy flooring resins market integrates sustainability metrics into bid documents, specification rates for low-VOC systems climb across North America and parts of Asia.

Anti-Dumping Duties on Asian Epoxy Resins Tightening Western Supply

US anti-dumping tariffs ranging from 15% to 234% on Chinese epoxy imports have redrawn sourcing maps, pushing buyers toward regional producers or specialty importers with lower duty exposure[2]BLOOMBERG, “U.S. Imposes Anti-Dumping Tariffs on Epoxy Resin Imports,” bloomberg.com. European Commission actions mirror the trend, aiding domestic plants that previously competed largely on service. Commodity-grade flooring resins bear the brunt of cost inflation, whereas niche grades for the semiconductor and pharmaceutical industries retain premium pricing elasticity. The epoxy flooring resins market thus witnesses near-term supply tightening in the West, amplifying opportunities for mid-tier manufacturers willing to localize capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile bisphenol-A and epichlorohydrin prices compressing margins | -0.7% | Global, with acute impact in APAC manufacturing | Short term (≤ 2 years) |

| UV-induced yellowing limiting use in sun-exposed areas | -0.4% | Global, particularly affecting outdoor applications | Medium term (2-4 years) |

| Skilled-installer shortage raising project delays/costs in mature markets | -0.5% | North America & EU mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Bisphenol-A and Epichlorohydrin Prices Compressing Margins

Feedstock costs for bisphenol-A and epichlorohydrin fluctuate with the fundamentals of phenol, acetone, propylene, and chlorine supply, which rarely move in sync. Flooring-grade resin contracts, which are often fixed three to six months ahead, expose suppliers to margin erosion when spot spikes occur. Asian commodity producers, already operating on thin spreads, struggle most, but even integrated Western firms hedge only part of their exposure. Buyers in the epoxy flooring resins market are increasingly open to index-linked clauses, yet structural price risk persists until broader petrochemical capacity additions stabilize feedstock balances.

UV-Induced Yellowing Limiting Use in Sun-Exposed Areas

Standard bisphenol-A resins can amber after prolonged UV exposure, restricting usage on exterior walkways and atriums with skylight glazing. Although HALS-enhanced topcoats and UV-curable overlays mitigate the effect, added cost and application complexity deter price-sensitive owners. Research programs in Japan and South Korea focus on novel cycloaliphatic backbones to improve color stability, but commercialization remains several years out. Until then, polyurethane-cement hybrids and PMMA systems retain share in outdoor segments, holding back incremental volume growth for the epoxy flooring resins market in architectural applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-Use Sector: Industrial Retrofit Underwrites Growth

Industrial and Institutional facilities accounted for 72.10% of 2025 demand, underscoring how hygiene, chemical resistance, and heavy-load durability keep these operators tied to epoxy flooring resins market solutions. Segment volume will expand at a steadier pace as mandatory clean production standards proliferate across the pharmaceutical and food industries. The Commercial category, though smaller, carries the highest 4.33% CAGR thanks to data-center build-outs requiring electrostatic discharge suppression. Emerging retail formats adopt seamless floors that accelerate nightly cleaning, adding incremental square footage. Infrastructure projects, such as intermodal freight terminals, prefer 6–8 mm self-levelling formulations capable of withstanding forklift abrasion, while Residential uptake remains niche outside high-end garages. Overall, performance differentiation drives specification toward proprietary antimicrobial, low-outgassing, or static-dissipative systems, rather than one-size-fits-all products, which raises average selling prices across the epoxy flooring resins market.

Second-generation antimicrobial additives, once exclusive to medical centers, are now penetrating beverage bottling lines, where biofilm prevention is crucial. Semiconductor fabs require ultra-low silicones to minimize photolithography defects, and battery plants require dielectric-strength certification prior to commissioning. Such tailored chemistries thin the supplier field to firms controlling polymer design and application know-how. Consequently the epoxy flooring resins market size for niche-engineered grades is projected to outpace commodity formulas through 2030, even if the latter still anchor bulk tonnage.

By Distribution Channel: Contractors Cement a Technical Gatekeeper Role

Direct/Contractor sales captured 93.65% of the Epoxy Flooring Resins market in 2025, as system outcomes hinge on meticulous substrate preparation, mix ratios, and ambient condition control. Contractors routinely bundle surface grinding, vapour-barrier application, and long-tail warranties, pushing resin procurement into a turnkey services model. Manufacturers nurture exclusivity by certifying installers, co-branding projects, and offering job-site technical reps, tactics that heighten switching costs. The epoxy flooring resins market size linked to this channel could rise in proportion to the number of industrial owners who continue to outsource floor maintenance under long-term service agreements.

DIY and e-commerce portals sell garage-kit gallons but rarely exceed 3% share outside North America. Growth here remains capped by the high failure rate of homeowner applications lacking moisture-content testing or proper primer selection. Some formulators now pilot two-part pouches and video guidance to expand addressable demand, yet sustained entry into professional segments looks distant. In emerging economies, informal installer networks occasionally bypass formal distributors, but large end-users still funnel purchases through certified applicators to secure warranty coverage, reinforcing the contractor-centric structure of the epoxy flooring resins market.

Geography Analysis

The Asia-Pacific region retained 41.00% of 2025 revenue, as Chinese and Indian capacity expansions in pharmaceuticals, electronics, and automotive sectors extensively specified chemical-resistant industrial floors. Provincial subsidies for “little giant” advanced-manufacturing plants accelerate square-footage additions, and regional resin overcapacity keeps pricing competitive, encouraging wider adoption. Anti-dumping pushback in Western markets redirects some Chinese output to Southeast Asia, where Vietnam and Indonesia absorb product for warehousing and assembly hubs. The epoxy flooring resins market size accruing to the Asia-Pacific region is therefore expected to expand steadily, while maintaining its dominant share.

North America offers a mature yet resilient demand stream anchored in retrofit activity and stringent air-quality rules that favor low-VOC technologies. Semiconductor and EV-battery megaprojects in Texas, Arizona, and Tennessee each consume tens of thousands of gallons of static-dissipative or chemical-resistant grades. Canadian oil-sand service shops and Mexican maquiladora plants expand regional relevance, though installer shortages challenge schedule adherence. Owners’ insistence on 10- to 20-year warranties sustains premium-grade penetration and positions the epoxy flooring resins market as a reliable growth avenue despite relatively modest new-build volumes.

Europe continues to layer carbon-neutral mandates on new construction, linking public-sector funding to Environmental Product Declarations and end-of-life recyclability. Germany’s automotive foundries upgrade floors to withstand e-mobility battery-chemistry spills, while France retrofits hospitals under its “Ma Santé 2025” plan. Eastern European member states tap EU cohesion funds to modernize logistics corridors, fuelling medium-term uptake. The epoxy flooring resins market thus balances slow overall economic growth with policy-driven specification momentum and a steady pivot to water-borne systems.

Middle East & Africa, the fastest-growing region at a projected 3.99% CAGR, benefits from sovereign-wealth-fund diversification into petrochemicals, renewables and large-scale tourism. Saudi Arabia’s NEOM and the United Arab Emirates (UAE)’s hydrogen-ammonia terminals both commit to chemical-resistant, UV-stable floors that endure desert conditions. In Africa, copper smelters in Zambia and citrus-processing plants in South Africa adopt 100%-solids formulations to fight acid attack and thermal shock. These projects collectively raise regional contractor sophistication and anchor long-run expansion of the epoxy flooring resins market.

Competitive Landscape

The Epoxy Flooring Resins Market is moderately fragmented, as the top five suppliers leverage backward integration to stabilize feedstock costs and protect supply during shocks in bisphenol-A and epichlorohydrin. Strategic partnerships between resin suppliers and manufacturers of surface preparation equipment accelerate the push toward turnkey project delivery. Digital color-matching scanners, now standard on decorative retail floors, are migrating into industrial projects to simplify QA sign-off. As demand clusters around data centers and battery plants, suppliers deepen stock points near construction hotspots to trim lead times. Sustained M&A appetite suggests further consolidation, particularly among ancillary additives and grinding-tool makers, as players seek to capture a larger share of the epoxy flooring resins market value chain.

Epoxy Flooring Resins Industry Leaders

RPM International Inc.

Sika AG

The Sherwin-Williams Company

Nippon Paint Holdings Co., Ltd.

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF and Sika jointly developed a new amine building block for curing epoxy resins, commercially available under BASF’s Baxxodur EC 151 brand. This new development is particularly interesting for flooring applications.

- March 2025: Westlake Corporation announced that Westlake Epoxy launched several new products at the European Coatings Show (ECS) 2025 in Germany. Westlake Epoxy introduced its newly developed EpoVIVE portfolio of products, which feature lower VOC (volatile organic compounds) waterborne epoxy resin dispersions.

Global Epoxy Flooring Resins Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Asia-Pacific, Europe, Middle East and Africa, North America, South America are covered as segments by Region.| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Direct / Contractor |

| DIY and E-commerce |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | Canada |

| Mexico | |

| United States | |

| Europe | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Distribution Channel | Direct / Contractor | |

| DIY and E-commerce | ||

| By Geography | Asia-Pacific | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Market Definition

- END-USE SECTOR - Epoxy flooring resins consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of epoxy-based flooring resin products for the lobby, factory, store, garage, and hallways among others are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms