Indonesia Flooring Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

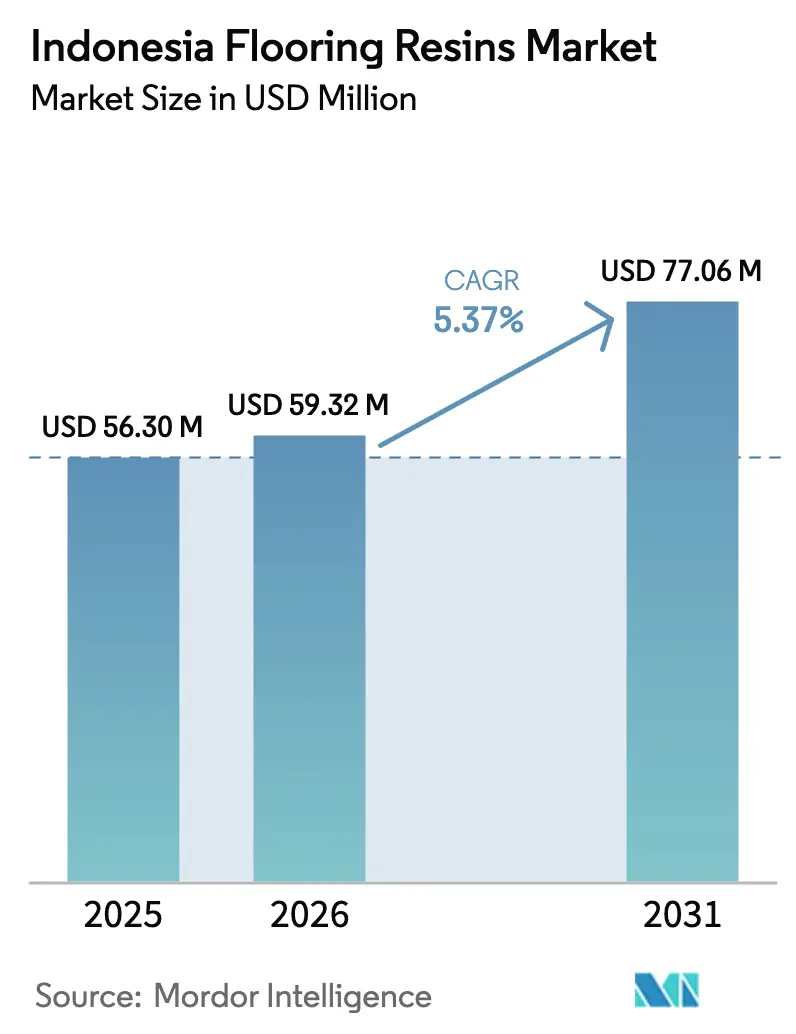

| Base Year Market Size (2025) | USD 56.30 Million |

| Market Size (2026) | USD 59.32 Million |

| Market Size (2031) | USD 77.06 Million |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Flooring Resins Market Analysis by Mordor Intelligence

The Indonesia Flooring Resins Market size in 2026 is estimated at USD 59.32 million, growing from 2025 value of USD 56.30 million with 2031 projections showing USD 77.06 million, growing at 5.37% CAGR over 2026-2031. Robust government infrastructure spending, a rising pipeline of industrial estates, and strict green-building mandates continue to reinforce demand for high-performance coatings across the Indonesia flooring resins market. Organized suppliers deepen their foothold by pairing locally blended epoxy and polyurethane systems with on-site technical service, thereby mitigating import duty volatility and skills gaps. At the same time, the popularity of polyaspartic fast-cure coatings is broadening specification choices, especially for 24/7 e-commerce warehouses that cannot afford extended downtime. Supply-chain recalibration toward domestic resin finishing coupled with tariff hedging strategies is expected to cushion the industry against short-term feedstock price swings emanating from China.

Key Report Takeaways

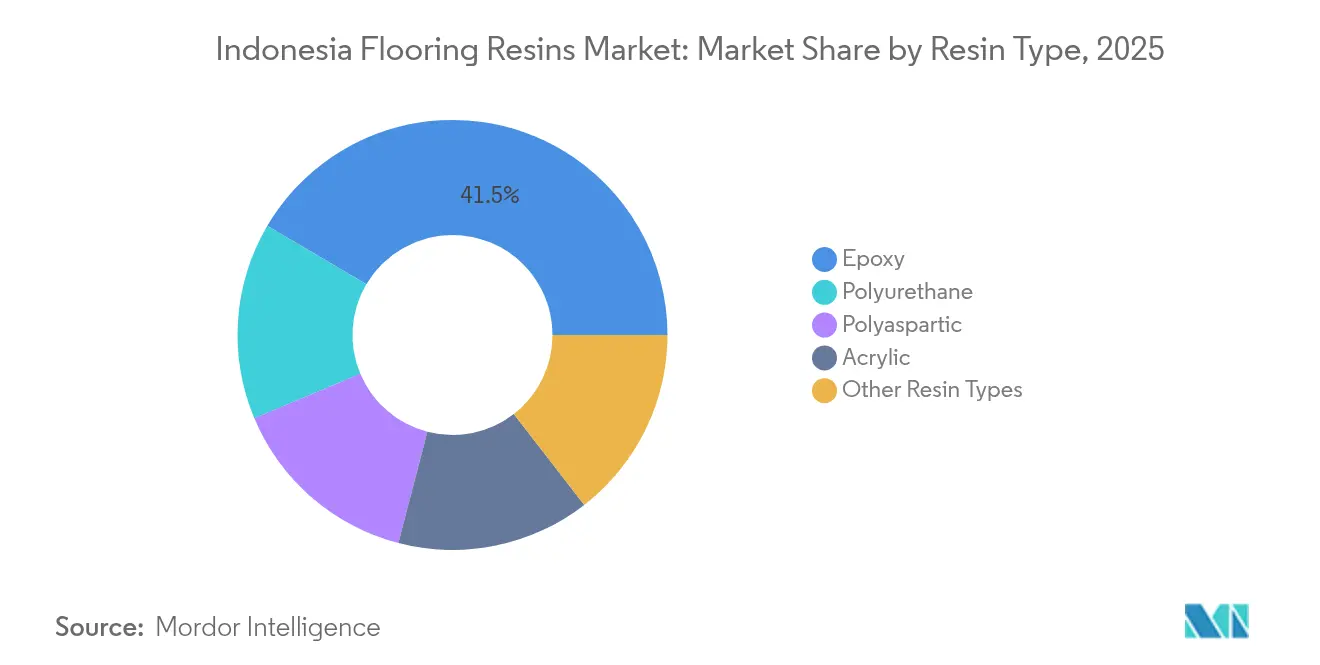

- By resin type, epoxy held 41.52% of the Indonesia flooring resins market share in 2025. Polyurethane is projected to grow at a 6.89% CAGR through 2031.

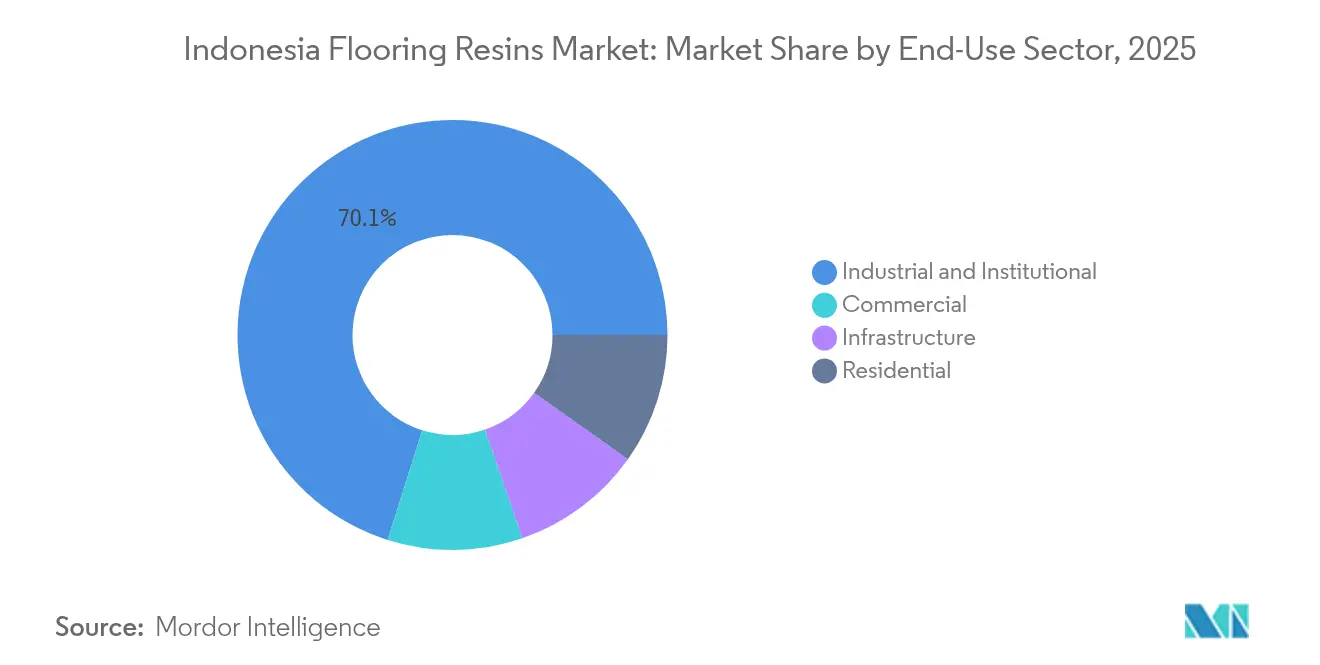

- By end-use sector, industrial and institutional applications accounted for 70.12% share of the Indonesia flooring resins market size in 2025. Commercial applications are forecast to expand at a 6.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Flooring Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led mega-infrastructure pipeline | +1.80% | Java & Sumatra corridors | Medium term (2-4 years) |

| Expansion of manufacturing clusters and industrial estates | +1.50% | Java industrial belt, Batam, Medan | Medium term (2-4 years) |

| Shift toward low-VOC and green building materials | +1.20% | Jakarta, Bandung, major urban centers | Long term (≥ 4 years) |

| Rapid growth in e-commerce warehousing requiring high-durability floors | +1.00% | Greater Jakarta, Surabaya logistics hubs | Short term (≤ 2 years) |

| Emerging popularity of polyaspartic fast-turnaround coatings in tropical climates | +0.80% | National coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Mega-Infrastructure Pipeline

Public works spending totaling USD 410 billion for 2020-2024 and the rollout of 200 priority sites continue to set the demand floor for epoxy and polyurethane systems in the Indonesia flooring resins market[1]Maike Kirsch, “Adapting Infrastructure to Changing Climatic Conditions: The Case of Indonesia,” OECD, oecd.org . The USD 35 billion Nusantara capital project reinforces long-dated order visibility for terminal buildings, transit hubs, and administrative complexes that require durable and chemical-resistant finishes. Infrastructure owners now specify low-carbon, recyclable resin options to comply with “Building with Nature” guidelines, steering formulators toward bio-based hardeners and recycled fillers. Contractors are increasingly bundling supply agreements with certified applicator training to ensure specification fidelity and reduce lifecycle maintenance costs. As these flagship projects progress to interior works, flooring resin volumes are poised to follow a staggered yet firm procurement curve over the next three years.

Expansion of Manufacturing Clusters and Industrial Estates

Foreign capital inflows unlocked by Presidential Regulation 10/2021 stimulate factory construction across automotive, electronics, and textiles, anchoring resin offtake in the Indonesia flooring resins market. Electronics facilities demand anti-static epoxy floors with surface resistivity of 10^6–10^9 ohm, while battery assembly lines require polyurethane overlays that tolerate electrolyte spills. In Batam and West Java, anchor tenants now negotiate vendor-managed inventory programs to secure color-matched batches and minimize production downtime. Forward-buying of key additives such as cycloaliphatic amines has become common as buyers hedge against feedstock volatility. These procurement patterns add volume stability and encourage resin manufacturers to localize blending plants near high-growth estates.

Shift Toward Low-VOC and Green Building Materials

Regulation 02/2015 from the Ministry of Public Works bans formaldehyde and chlorinated flame retardants, pushing formulators to develop zero-solvent, water-borne polyurethane dispersions. Jakarta alone counts 389 green-certified buildings spanning 25 million m², and developers report 3%-5% rental premiums for LEED-aligned properties. Flooring resin suppliers use third-party eco-labels to win bids, often pairing them with life-cycle cost models that demonstrate lower scrubbing frequency and energy savings. End-users are also receptive to bio-based diluents sourced from palm kernel oil, a readily available local feedstock. As tenant demand for healthy interiors rises, the premium for certified low-VOC systems is narrowing, accelerating mainstream adoption.

Emerging Popularity of Polyaspartic Fast-Turnaround Coatings in Tropical Climates

High humidity and year-round rainfall undermine traditional epoxy film formation, but polyaspartic esters tolerate 90% relative humidity without blushing. Parking decks and beachfront resorts increasingly switch to these systems for their graffiti resistance and aliphatic UV stability. Contractors report up to 40% labor savings because a full two-coat system can be installed in a single shift. Suppliers target cost parity with premium epoxies by optimizing amine-blocking additives and leveraging domestic isocyanate distillation. Conference proceedings from the 2024 ASEAN Coating Innovation forum forecast polyaspartic volumes to triple by 2028, signaling a structural shift in high-performance segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile epoxy feedstock prices linked to China supply swings | -1.50% | Nationwide industrial centers | Short term (≤ 2 years) |

| Lack of certified flooring applicators causing performance failures | -1.20% | Secondary cities | Medium term (2-4 years) |

| Rising import duties on specialty resins and additives | -0.80% | Premium segments nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Epoxy Feedstock Prices Linked to China Supply Swings

Epichlorohydrin and bisphenol-A spot prices spiked 27% in 2024, pressuring gross margins for local formulators that source 70% of inputs from China[2]International Trade Administration, “Indonesia – Import Tariffs,” trade.gov . While the average MFN duty on chemicals is 8.1%, bound rates of 37.3% leave policymakers room to raise levies abruptly, adding another layer of uncertainty. Small and midsize applicators hesitate to quote fixed-price contracts longer than 60 days, which in turn slows conversion of project pipelines into purchase orders. Resin makers respond by negotiating toll-blending deals with regional producers in Thailand and Malaysia to diversify supply. Some EPC contractors bundle price-adjustment clauses indexed to the ICIS epoxy benchmark, partially transferring risk downstream.

Rising Import Duties on Specialty Resins and Additives

Indonesia’s protectionist shift since 2023 has already seen duty hikes on select polymer modifiers and color pastes, raising landed costs for premium systems by 4%-7%. Domestic formulators pass through some of the increase, but price-sensitive customers pivot back to lower-spec coatings or even ceramic tiles. Multinationals with ASEAN production hubs mitigate exposure via bonded-storage arrangements, yet SMEs lack similar options. The resulting two-tier pricing landscape could slow premiumization of the Indonesia flooring resins market if additional tariffs materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Polyurethane Challenge

Epoxy systems commanded 41.52% of the Indonesia flooring resins market share in 2025. Their grip on heavy-duty manufacturing, aviation hangars, and cold-storage floors stems from tensile strengths above 50 MPa and excellent chemical resistance. Nonetheless, polyurethane’s 6.89% forecast CAGR positions it as the prime disruptor, thanks to elongation at break exceeding 70% that cushions seismic shocks and thermal cycling. Polyaspartic hybrids, while still niche, bridge the gap by marrying epoxy adhesion with polyurethane flexibility and 90-minute return-to-service, making them attractive for hospital corridors that cannot close for extended renovations. Acrylic resins maintain traction in price-conscious residential refurbishments where decorative flakes outweigh structural performance.

Second-order shifts reinforce polyurethane’s climb. Green-building drives low-VOC demand that solvent-free PU dispersions meet without costly add-ons. Coastal resorts specify aliphatic PU topcoats for UV stability, while electronics assemblers adopt PU-cement composites that endure aggressive cleaning agents. Collectively, these factors chip away at epoxy’s lead, ensuring intensified R&D around bio-based isocyanates and water-borne hardeners to widen polyurethane’s addressable scope within the Indonesia flooring resins market.

By End-Use Sector: Industrial Leadership with Commercial Acceleration

Industrial and institutional sites accounted for 70.12% of the Indonesia flooring resins market size in 2025. Automotive, food & beverage, and public-sector buildings specify multi-layer epoxy builds exceeding 3 millimeters to handle forklift loads, acids, and disinfectants. Government procurement frameworks often pre-qualify vendors possessing ISO 14025 environmental product declarations, narrowing competition to organized manufacturers with global certifications. Meanwhile, the commercial segment’s 6.68% forecast CAGR rides Indonesia’s e-commerce surge, pushing demand for antislip, high-gloss floors that improve pick-rate efficiency in fulfilment centers. Hospitals and retail malls add to commercial momentum as they refresh interiors to win foot traffic in post-pandemic environments.

Although residential uptake remains modest, premium condominiums in Jakarta start to showcase thin-film decorative epoxy terrazzo as an alternative to marble, signaling longer-term diversification. Infrastructure projects—ports, airports, and mass-transit stations—round out demand with heavy-duty polyurethane concrete that resists jet fuel and de-icing salts. Hence, while industrial orders anchor baseline volume, commercial and infrastructure niches inject incremental growth and higher margin potential across the Indonesia flooring resins market.

Geography Analysis

Java dominates the Indonesia flooring resins market, led by Greater Jakarta’s concentration of HQ offices, logistics centers, and 389 green-certified buildings. West Java’s textile parks and East Java’s automotive corridor further contribute to more than 60% of national resin consumption. The tight clustering near Tanjung Priok and Tanjung Perak ports shortens supply chains, encouraging vendors to maintain just-in-time depots for tinting and additive tweaks.

Sumatra provides the next wave of expansion. Palm-oil processing complexes around Medan require food-grade polyurethane floors that withstand fatty-acid exposure, while new container terminals at Belawan enhance import agility for specialty pigments. South Sumatra’s mining support facilities also specify static-dissipative overlays for explosive zones, adding a safety-driven niche to the Indonesia flooring resins market.

Kalimantan’s spotlight comes from the USD 35 billion Nusantara capital, which is slated to deploy seamless resin floors across civic structures and transport interchanges. Sulawesi’s nickel-based stainless-steel mills in Morowali turn to heavy-gauge epoxy screeds that resist metal shavings and high-temperature washdowns. However, inter-island logistics barriers—ranging from limited cold-chain containers to high cabotage charges—infl ate delivered costs by up to 15%, tempering adoption outside Java. Ongoing liberalization in logistics services aims to resolve bottlenecks and could gradually level regional price disparities within the Indonesia flooring resins market.

Competitive Landscape

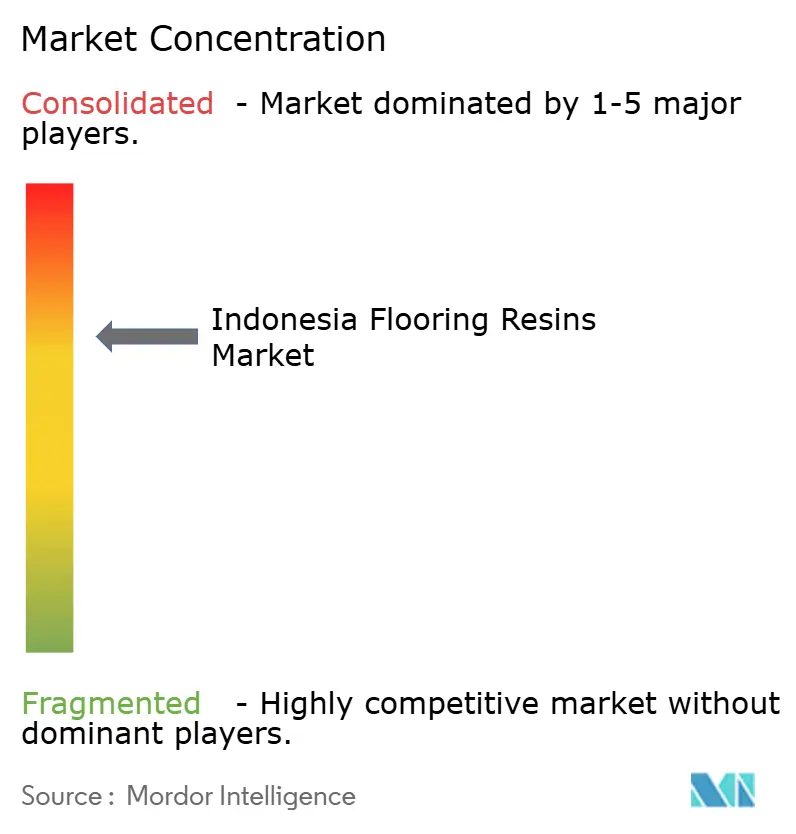

The Indonesia flooring resins market exhibits moderately fragmented concentration. Multinationals such as RPM International, Sherwin-Williams, and Sika capitalize on proprietary resin chemistries and global sourcing leverage to serve premium tiers of the Indonesia flooring resins market. Their regional technical centers in Singapore and Malaysia channel R&D advances—like self-leveling epoxy with nanoparticle abrasion modifiers—into Indonesian specifications. Local champions PT Propan Raya and PT KCCI Chemtech Indonesia counter by offering custom color fast-turn services and economical solvent-cut epoxies tailored to smaller contractors.

Technical service is a decisive battleground. Leading players run mobile “floor clinics” that audit substrate moisture and recommend primer packages, alleviating the applicator skills gap that causes 90% of failures. Sustainability credentials create another wedge: Sika’s E-1 low-emission label and Sherwin-Williams’ LEED-v4 compliant recipes regularly secure public-sector tenders. RPM International’s Q2 FY2025 record Performance Coatings sales of USD 380.1 million underscore the pull of high-performance flooring in ASEAN projects, a trend expected to cascade into Indonesia as its new Indian plant comes on-line in H2 FY2025.

Digital channels are reshaping reach. Tokopedia’s business storefront now lists ready-mix epoxy kits, letting SMEs in Makassar order directly and bypass multiple distributors. Yet institutional buyers still favor full-service contracts bundled with warranties, preserving the relevance of established network contractors. Given the combined share of the top five players hovers near 45%, rivalry will likely intensify around mid-tier polyurethane products where brand equity and price strike a delicate balance in the Indonesia flooring resins market.

Indonesia Flooring Resins Industry Leaders

RPM International Inc.

Sika AG

Saint-Gobain

PT Propan Raya I.C.C

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain has finalized the acquisition of FOSROC, a leading global construction chemicals company with a strong geographic presence in India, the Middle East, and the Asia-Pacific region. This acquisition is expected to strengthen Saint-Gobain's position in the Indonesia flooring resin market by enhancing its product offerings and expanding its regional footprint.

- May 2023: Sika has completed the acquisition of MBCC Group after securing all necessary regulatory approvals. This move strengthens Sika's global presence, enhances its construction lifecycle offerings, and accelerates sustainable transformation. The acquisition is anticipated to boost the Indonesia flooring resin market by introducing innovative solutions and promoting sustainability.

Indonesia Flooring Resins Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Acrylic, Epoxy, Polyaspartic, Polyurethane are covered as segments by Sub Product.| Acrylic |

| Epoxy |

| Polyaspartic |

| Polyurethane |

| Other Resin Types |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential |

Market Definition

- END-USE SECTOR - Flooring resins consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of flooring resin products based on epoxy, polyaspartic, polyurethane, acrylic, and other resins are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms