Asia-Pacific Flooring Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

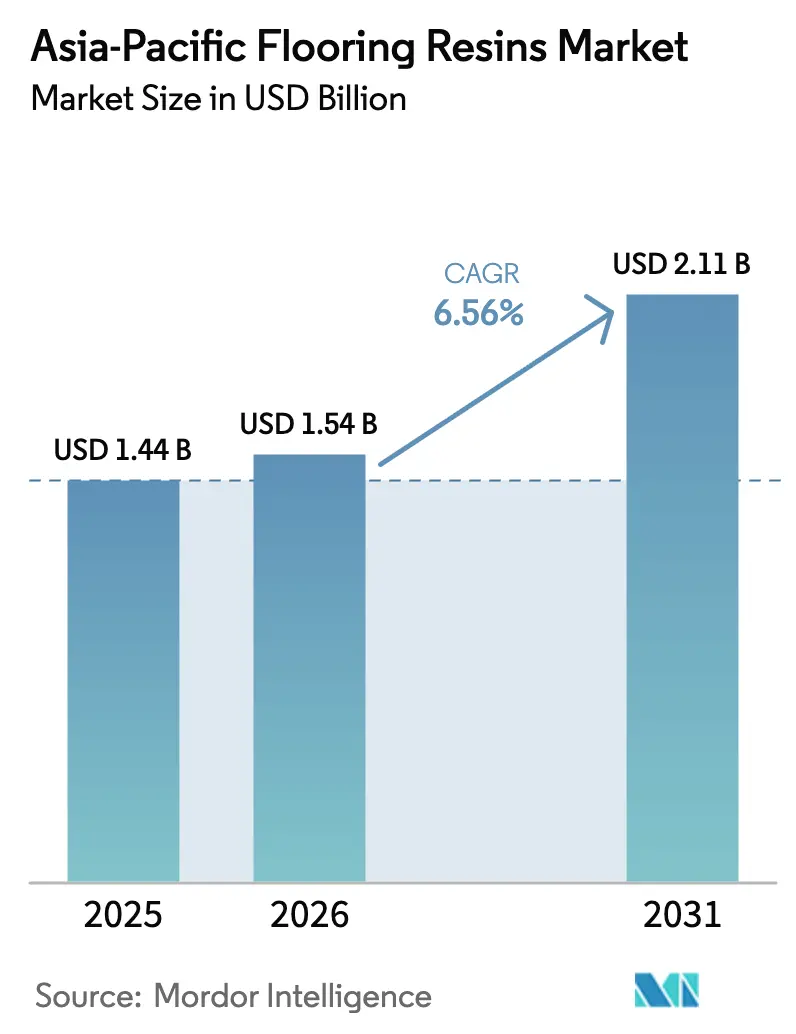

| Base Year Market Size (2025) | USD 1.44 Billion |

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Flooring Resins Market Analysis by Mordor Intelligence

Asia-Pacific Flooring Resins Market size in 2026 is estimated at USD 1.54 billion, growing from 2025 value of USD 1.44 billion with 2031 projections showing USD 2.11 billion, growing at 6.56% CAGR over 2026-2031. Continued industrial expansion, rapid urbanization, and an accelerating pipeline of commercial real-estate projects underpin demand for high-performance resin flooring across factories, logistics centers, and modern retail venues. Stricter VOC regulations in China, Japan, and South Korea are shifting procurement toward water-borne and high-solids chemistries that meet sustainability mandates while minimizing downtime. Intensifying supply-chain localization by global manufacturers is spurring new resin production capacity across Singapore, Vietnam, and Indonesia, enhancing regional product availability and price competitiveness. Meanwhile, mega airport projects and e-commerce fulfillment hubs are creating niche opportunities for quick-cure, abrasion-resistant systems that extend asset life cycles and reduce maintenance costs.

Key Report Takeaways

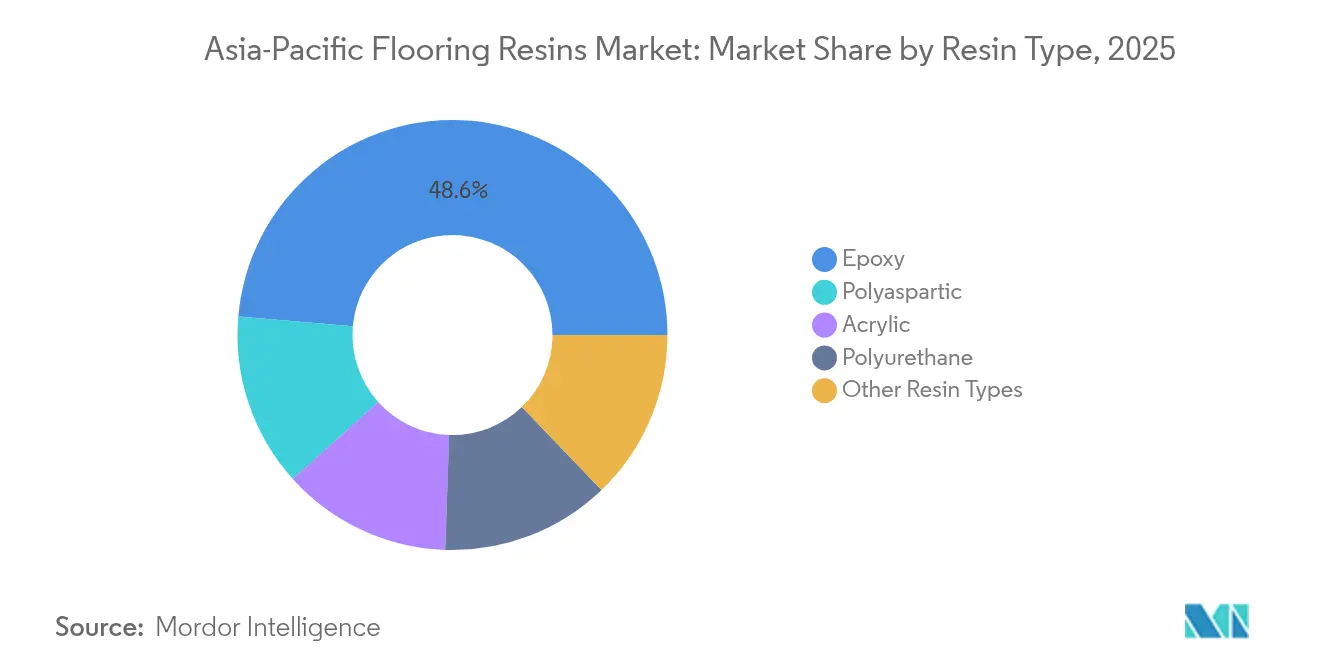

- Epoxy captured 48.62% of the Asia-Pacific flooring resins market share in 2025, while polyaspartic systems are forecast to expand at a 7.41% CAGR through 2031.

- Industrial and institutional buildings accounted for 62.47% of the Asia-Pacific flooring resins market size in 2025; the commercial segment is projected to advance at a 6.97% CAGR to 2031.

- China commanded 47.78% of regional revenue in 2025, whereas Vietnam is poised to grow the fastest at a 7.21% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Flooring Resins Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and commercial real-estate boom | +1.8% | China, India, Indonesia, Vietnam | Medium term (2-4 years) |

| Stringent VOC norms pushing water-borne resins | +1.2% | Japan, South Korea, Australia, China | Long term (≥ 4 years) |

| Expansion of manufacturing facilities | +1.5% | ASEAN core, spill-over to India and China | Medium term (2-4 years) |

| Mega airport expansion projects | +0.8% | Singapore, Malaysia, Thailand, Indonesia | Short term (≤ 2 years) |

| E-commerce fulfillment centers | +1.1% | China, India, Southeast Asia logistics corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Commercial Real-Estate Boom

Asia-Pacific cities are absorbing millions of new residents annually, resulting in record levels of office, retail, and hospitality construction that drive spending on decorative yet durable floors. Indonesia’s construction sector contributed 9.86% to the national GDP in 2023 and secured an IDR 422.7 trillion (USD 27.7 billion) infrastructure allocation for 2024, reinforcing the near-term project pipeline[1]Business-Indonesia, “Indonesia’s Construction Sector Remains Sturdy,” business-indonesia.org. Malaysia echoed this trend, logging 14.6% construction growth in the first half of 2024, driven by data-center and transit projects. Developers across Thailand anticipate 3-4% annual growth in construction spending through 2026, with 35% of the total earmarked for commercial properties. Urban migration fuels demand for visually appealing resin terrazzo and polyurethane top-coats that blend aesthetics with abrasion resistance. Large footprints and tight handover schedules in new malls intensify interest in polyaspartic systems that cure within hours, enabling quicker tenant fit-outs and earlier revenue capture.

Stringent VOC Norms Pushing Water-Borne Resins

Asia-Pacific regulators are converging on lower VOC thresholds, forcing flooring resin suppliers to reformulate their products. Shanghai’s mandatory paint emission standards, effective as of December 2024, impose stringent solvent limits on local manufacturers. South Korea withdrew exemptions for four common VOC diluents in 2023 and now levies penalties up to KRW 10 million for non-compliance. Japan’s indoor-air regulations cap formaldehyde at 0.08 ppm, prompting widespread demand for low-odor, low-emission coatings. Global producers are responding: Sika and BASF jointly introduced an epoxy hardener featuring up to 90% lower VOCs than legacy systems in 2025[2]Sika, “Epoxy Hardener Launch,” sika.com . Contractors gain compliance and safety benefits, while owners secure ESG credentials and healthier indoor environments, reinforcing adoption of water-borne and high-solids chemistries across premium office towers and public facilities.

Expansion of Manufacturing Facilities in the Asia-Pacific Region

Foreign direct investment in ASEAN manufacturing surpassed USD 124 billion from 2022 to 2023, as electronics, automotive, and battery producers diversified beyond coastal China. Vietnam ranks second globally on the 2025 Asia manufacturing attractiveness index due to robust FTAs and logistics upgrades that favor export-oriented plants. Indonesia’s downstream industrialization raised nickel output from less than 800,000 tons in 2020 to 2.03 million tons in 2023, generating new processing floors that require chemical-resistant resin overlays. These projects specify epoxy ESD coatings or polyurethane screeds to safeguard sensitive electronics and withstand the impact of heavy mobile equipment. Local-for-local production by multinationals such as Sika in Singapore and Xi’an shortens lead times and reduces tariff exposure, further accelerating product penetration.

Mega Airport Expansion Projects Across the Globe

Airports upgrading capacity across Southeast Asia require seamless, low-maintenance surfaces that are tolerant of rolling loads, security scanners, and 24/7 pedestrian traffic. Resin terrazzo deployed at Hamad International Airport spans 140,000 m² and offers a 40-year lifespan, compared to 12 years for vinyl alternatives. Upcoming terminals in Changi, Kuala Lumpur, and Bangkok reference similar performance benchmarks, creating a niche for high-build epoxy terrazzo and UV-stable polyaspartics. Suppliers offering turnkey specification support and global fire-rating compliance gain preferred-bidder status. The scale and visibility of airport contracts also provide marketing proof points that influence commercial developers, multiplying downstream demand.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile BPA and MDI input prices | -0.9% | China manufacturing hubs, ASEAN importers | Short term (≤ 2 years) |

| Disposal challenges of solvent-borne systems | -0.5% | Japan, South Korea, Australia, Singapore | Long term (≥ 4 years) |

| Shortage of certified resin-floor installers | -0.7% | Emerging Asia, particularly Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile BPA and MDI Input Prices

Epoxy and polyurethane formulators rely on BPA and MDI feedstocks, whose prices fluctuate with supply additions and freight bottlenecks. China commissioned 600,000 tons per year of new BPA capacity in the first half of 2024; however, persistent oversupply led producers to incur losses of CNY 842 per ton during January–May 2024. Conversely, MDI and TDI quotations increased by USD 200-300 per ton across ASEAN in January 2025, amid higher energy and logistics costs. Such volatility complicates inventory planning and contract pricing, forcing manufacturers to hedge raw-material exposures or implement quarterly price escalators. Sudden cost spikes can squeeze contractor margins on fixed-price projects, delaying flooring upgrades in price-sensitive sectors.

Disposal Challenges of Solvent-Borne Systems

Strict waste-management rules in Australia, Japan, and Singapore have raised disposal fees for solvent-contaminated containers, increasing ownership costs for legacy systems. Plants operating under ISO 14001 scrutiny prefer water-borne alternatives that minimize hazardous waste generation. Municipal incinerators in Tokyo and Seoul levy surcharges on paint sludge exceeding VOC thresholds, nudging asset owners toward compliant formulations. Suppliers still selling high-solvent chemistries face declining addressable markets and potential liability for improper waste handling, pressuring them to accelerate green-chemistry research and development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Polyaspartic Challenge

Epoxy held the lion’s share at 48.62% of the Asia-Pacific flooring resins market in 2025, underpinned by proven adhesion, chemical resistance, and cost efficiency across production halls and warehouses. Polyaspartic chemistries, although smaller in volume, are on a 7.41% CAGR growth trajectory to 2031, driven by the benefits of next-day return-to-service, which resonate with fast-track retail and airport refurbishments. Water-borne acrylics are gaining favor in education and healthcare facilities seeking low-odor installation, while polyurethane maintains a niche for elastic and impact-modulating surfaces in automotive assembly lines.

Regulatory and climatic factors equally shape technology migration. Hot, humid monsoons in Southeast Asia challenge traditional epoxies, whereas polyaspartics cure even at 0 °C, enabling year-round installation in northern China and alpine Japan. Supply-side innovation centers on high-solids hardeners that slash VOC output by up to 90%, helping asset owners satisfy green-building certifications. Competitive dynamics favor integrated suppliers capable of offering hybrid systems, epoxy primers topped with polyaspartic clear coats, balancing performance and cost.

By End-Use Sector: Industrial Leadership Meets Commercial Growth

Industrial and institutional facilities generated 62.47% of 2025 regional sales, mirroring the proliferation of semiconductor fabs, EV battery plants, and food-processing lines that require hygienic, chemical-resistant floors. The Asia-Pacific flooring resins market share for this end-use is projected to decline slightly as commercial spaces outpace industrial buildings in growth terms. Retail, hospitality, and office projects are forecast to grow at a 6.97% CAGR to 2031, driven by consumer-centric urban redevelopment in megacities such as Shanghai, Jakarta, and Ho Chi Minh City. Decorative epoxy terrazzo and metallic pigments attract developers eager to differentiate high-foot-fall venues while preserving abrasion resistance.

Infrastructure nodes, from subway stations to data centers, present a hybrid demand: industrial-grade thickness combined with stringent aesthetic and ESD control requirements. Residential adoption, though nascent, is expanding within luxury condominiums in Australia and Japan, where homeowners value seamless, low-maintenance surfaces. Overall, diversification across end-use sectors insulates suppliers from single-sector cycles and encourages a broader product line.

Geography Analysis

China retained its leadership position with 47.78% of regional revenue in 2025, buoyed by its dense manufacturing base and local availability of BPA feedstock, which lowers epoxy costs. Beijing’s tighter VOC rules, first deployed in Shanghai, accelerate the shift to water-borne systems, compelling local formulators to invest in emission-compliant lines.

Southeast Asia provides the strongest momentum. Vietnam is the fastest-growing geography at a 7.21% CAGR, leveraging its role as a China-plus-one hub for electronics, furniture, and apparel exports. Industrial park developers often specify ESD epoxy and chemical-resistant polyurethane floors to meet the requirements of multinational tenants. Indonesia follows closely, supported by nickel-processing expansions aligned with EV battery supply chains and the construction boom linked to its new capital city relocation. Malaysia and Thailand benefit from semiconductor and logistics investments, respectively, each of which catalyzes demand for cleanroom-grade and high-load screed systems.

Mature markets, such as Japan, South Korea, and Australia, exhibit a slower but steady uptake, with a focus on premium and sustainable offerings. Formaldehyde and VOC restrictions encourage specification of high-solids epoxies and polyaspartics that can meet LEED or BREEAM criteria. Australia’s mining expansions in Western Australia and Queensland sustain polyurethane screed consumption for ore-handling facilities. India, though still fragmented, presents long-term upside as government housing and smart-city programs gradually raise standards for flooring durability and aesthetics.

Competitive Landscape

The Asia-Pacific flooring resins industry is moderately fragmented, leaving ample room for local specialists to emerge. Strategic mergers and acquisitions are reshaping the field: Saint-Gobain’s USD 1.025 billion acquisition of FOSROC consolidates its presence in India and the Gulf, broadening its reach into specialty construction chemicals. Domestic challengers are upping capacity and product diversity, targeting mid-tier contractors through value-priced lines. Competitive advantage hinges on technical service networks that train applicators and troubleshoot onsite issues, a decisive factor given the installer shortage. Sustainability is the new battleground; firms that can document their carbon footprints and utilize circular-economy resins win specifications in government projects. Emerging niches, such as data centers and pharmaceutical flooring, favor suppliers offering ESD control, antimicrobial additives, and low-particle-shedding finishes. Price competition in the commodity epoxy market has intensified, but premium segments remain less elastic, allowing innovators to defend their margins through proprietary additives and turnkey installation packages.

Asia-Pacific Flooring Resins Industry Leaders

RPM International Inc.

Sika AG

Mapei S.p.A

Thermax Limited

Nippon Paint Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Atul Ltd completed a capacity expansion of its liquid epoxy resin facility, increasing the capacity by 50,000 tonnes/year, from 30,000 to 80,000 tonnes/year.

- March 2024: Grasim Industries Limited, a subsidiary company of Aditya Birla Group, in its Chemical business, inaugurated the expansion project of 123,000 tonnes of Epoxy resins and formulation capacity at Vilayat, Gujarat, boosting the overall capacity of Advanced Materials to 246,000 tonnes per annum.

Asia-Pacific Flooring Resins Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Acrylic, Epoxy, Polyaspartic, Polyurethane are covered as segments by Sub Product. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam are covered as segments by Country.| Acrylic |

| Epoxy |

| Polyaspartic |

| Polyurethane |

| Other Resin Types |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Geography | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Market Definition

- END-USE SECTOR - Flooring resins consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of flooring resin products based on epoxy, polyaspartic, polyurethane, acrylic, and other resins are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms