Contraceptive Pills Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

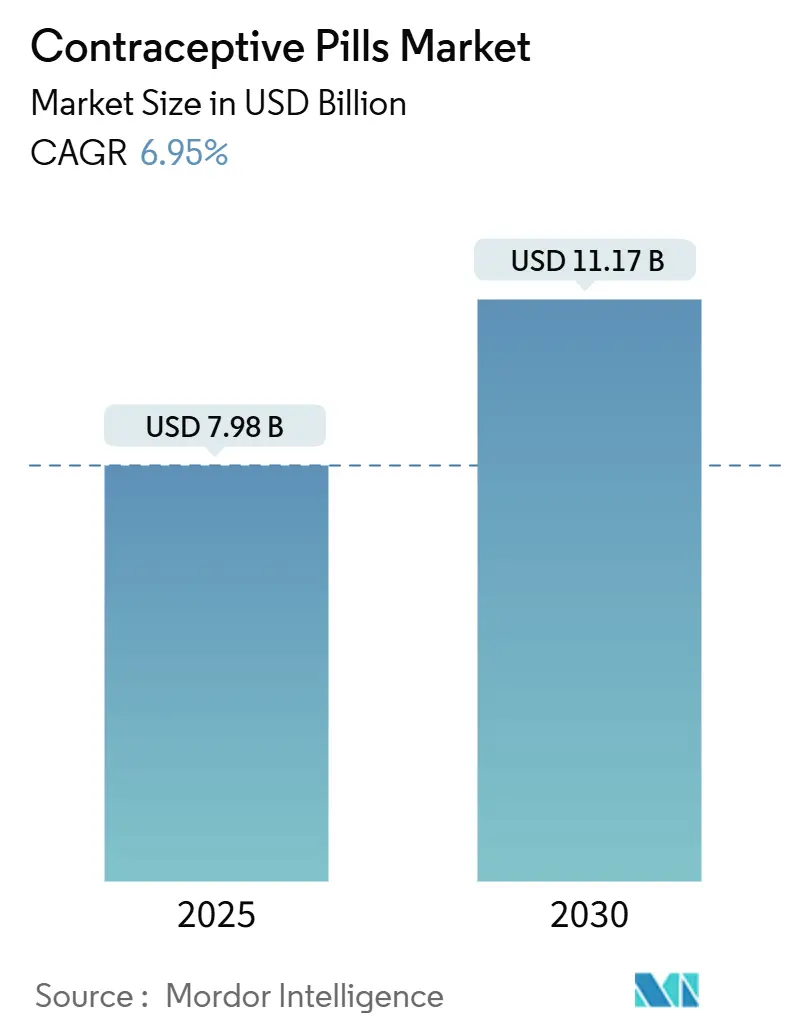

| Market Size (2025) | USD 7.98 Billion |

| Market Size (2030) | USD 11.17 Billion |

| Growth Rate (2025 - 2030) | 6.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contraceptive Pills Market Analysis by Mordor Intelligence

The contraceptive pills market reached USD 7.98 billion in 2025 and is forecast to climb to USD 11.17 billion by 2030, advancing at a 6.95% CAGR. The jump to over-the-counter availability in several countries, led by the United States Food and Drug Administration (FDA) approval of Perrigo’s Opill, is rewriting traditional prescription-based growth paths. Softening price points for generics, expanding telehealth distribution, and rising demand for low-dose estrogen formulations are widening the user base while intensifying price competition. Strategic consolidation among originator companies and fast-moving direct-to-consumer (DTC) start-ups is creating a two-tier competitive field that rewards scale on one end and nimble digital execution on the other. Late-stage product pipelines center on progestin-only pills (POPs) and extended-cycle regimens that promise clinical differentiation without raising costs.

Key Report Takeaways

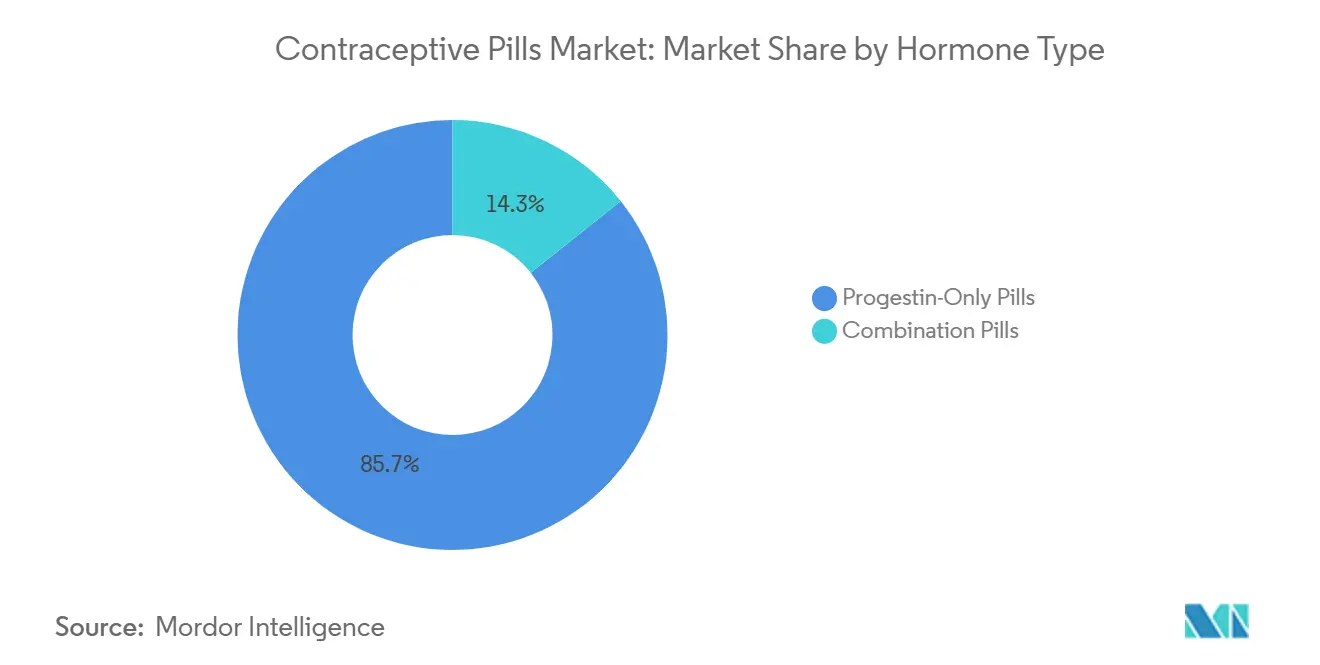

- By hormone type, combination pills accounted for 85.7% of the contraceptive pills market share in 2024, while progestin-only pills are projected to expand at a 7.97% CAGR through 2030.

- By dosage regimen, the traditional 28-day cycle held 57.3% of the contraceptive pills market size in 2024; extended/continuous cycles are on course for the fastest 9.23% CAGR to 2030.

- By category, generics commanded 61.3% of the contraceptive pills market size in 2024, whereas branded pills trail but are adding value-added services to offset pressure.

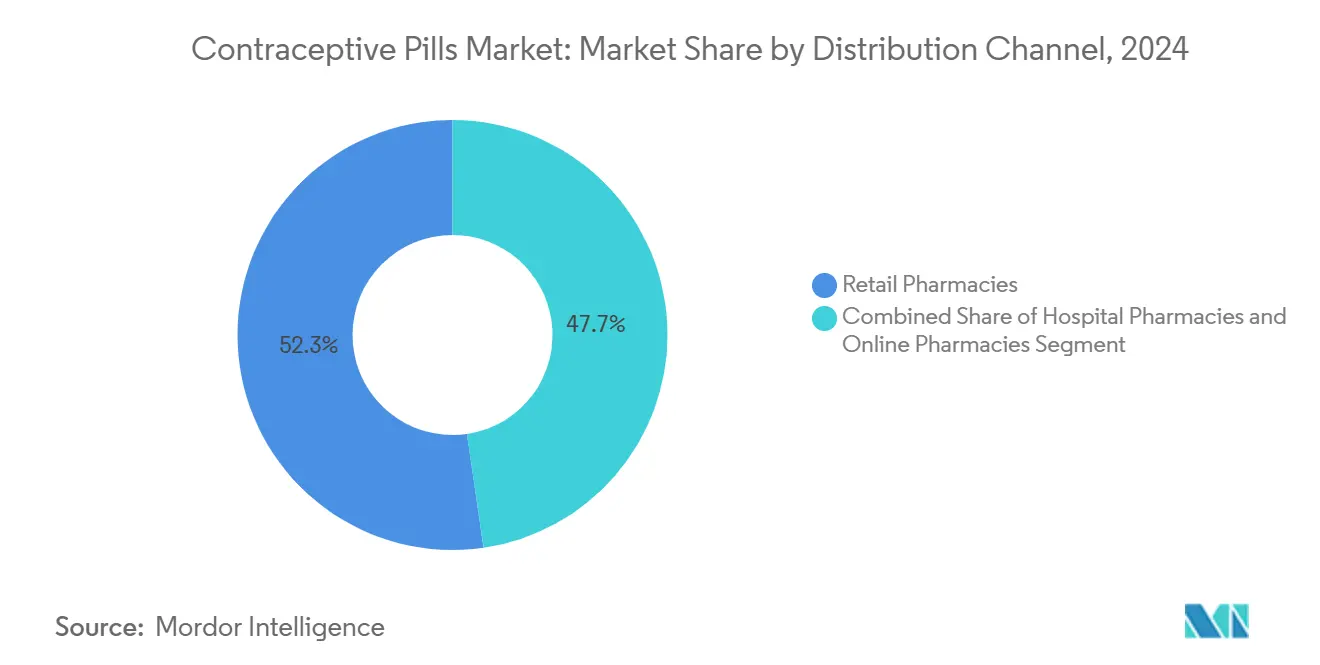

- By distribution channel, retail pharmacies led with 52.3% of the contraceptive pills market share in 2024, yet online pharmacies are advancing at a 9.75% CAGR between 2025-2030.

- By age group, women aged 25-34 controlled 43.6% of the contraceptive pills market size in 2024; the 15-24 cohort delivers the quickest 8.25% CAGR outlook.

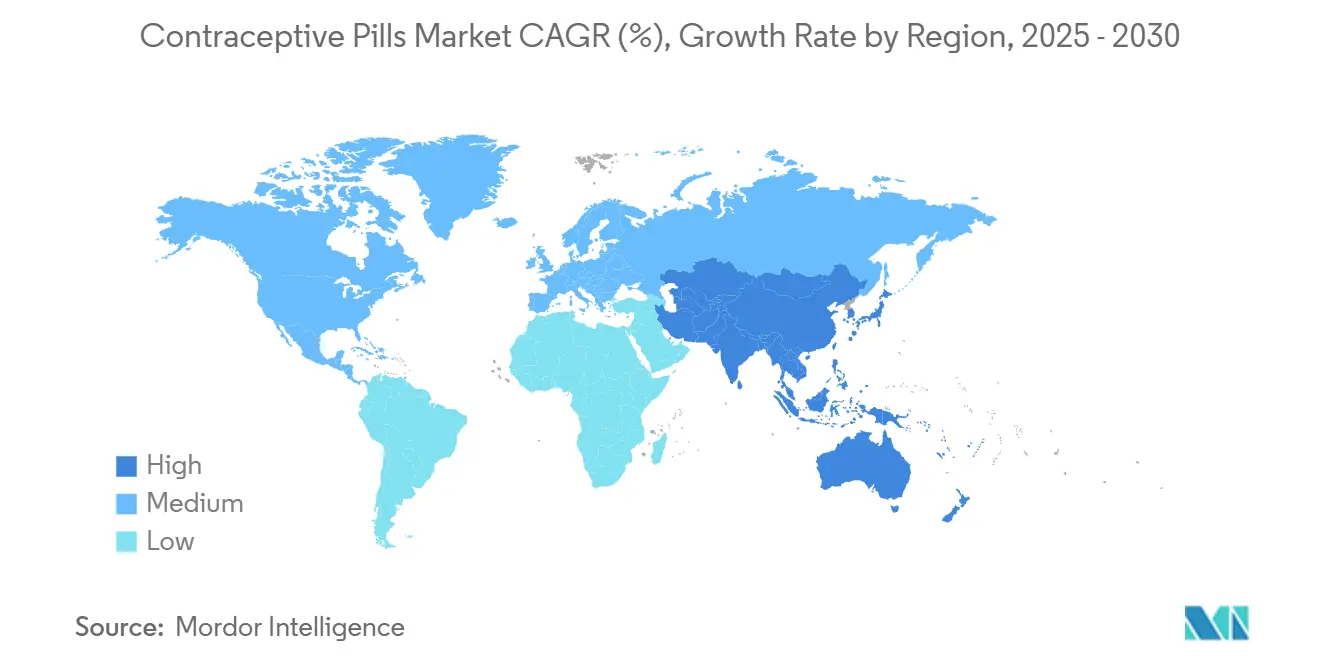

- By geography, North America captured 36.67% of global revenue in 2024, while Asia-Pacific is forecast for the fastest 8.85% CAGR through 2030.

Global Contraceptive Pills Market Trends and Insights

Driver Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for low-dose estrogen formulations | 1.20% | Global; pronounced in North America and Europe | Medium term (2-4 years) |

| Government initiatives and policies for family planning and reproductive health | 0.90% | Global; strong in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Shift toward tele-prescription and DTC platforms | 1.50% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Delayed family planning and high rate of unintended pregnancies | 0.80% | Global; higher in developed regions | Medium term (2-4 years) |

| Product innovation and new formulations | 1.10% | Global; early uptake in North America and Europe | Medium term (2-4 years) |

| Over-the-counter switch approvals expanding retail access | 1.00% | North America and Europe; gradual global rollout | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Low-dose Estrogen Formulations

Cardiovascular safety signals identified in large cohort studies have pushed manufacturers toward minimal-dose estrogen products, halving thromboembolic risk without compromising efficacy[1]Morten Schmidt, Vera Ehrenstein, Gunnar Lauge Nielsen, Henrik Toft Sørensen, “Cardiovascular Risks of Combined Oral Contraceptives: A Nationwide Cohort Study,” BMJ, bmj.com . Prescription switches accelerated after FDA guidance on lowering estrogen exposure in hormonal contraceptives[2]FDA Staff, “Estrogen and Estrogen/Progestin Drug Products to Treat Vasomotor Symptoms and Vulvar and Vaginal Atrophy,” U.S. Food and Drug Administration, fda.gov. Pharmaceutical pipelines now emphasize 10–20 µg ethinyl estradiol ranges, giving physicians clinical incentives to recommend lower-risk brands. Strong marketing around gentler side effect profiles broadens uptake among women over 35 and those with cardiovascular concerns, adding steady volume to the contraceptive pills market.

Government Initiatives and Policies for Family Planning and Reproductive Health

Mandates that require insurers to reimburse over-the-counter pills without copays are removing residual cost barriers in the United States[3]Department of Health and Human Services, “Enhancing Coverage of Preventive Services Under the Affordable Care Act,” Federal Register, federalregister.gov. Parallel moves in Asia-Pacific to bundle oral contraceptives into universal coverage programs stretch demand into semi-urban clinics. Thirty U.S. states plus the District of Columbia authorize pharmacists to prescribe contraceptives, sidestepping appointment bottlenecks and lifting regional prescription fill rates. These policy levers compound in markets where fertility reduction remains a national objective, bolstering long-term unit sales.

Shift Toward Tele-Prescription and DTC Platforms

Subscription-based brands such as Hims & Hers and Ro recorded double-digit revenue growth by combining algorithmic prescribing with convenient home delivery, improving adherence rates. The digital model undercuts office-visit costs and appeals to Gen Z, helping the contraceptive pills market capture patients who might otherwise lapse.

Delayed Family Planning and High Rate of Unintended Pregnancies

Average maternal age at first birth keeps climbing, particularly in OECD countries, extending contraceptive pill use over longer reproductive timelines. Extended-cycle regimens appeal to career-focused women seeking reduced withdrawal bleeding, and 24/4 dosing has demonstrated superior pregnancy-prevention outcomes over 21/7 schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mounting litigation risk linked to hormone-related adverse events | -0.70% | North America & Europe | Medium term (2-4 years) |

| Emergence of long-acting reversible contraceptives (LARCs) | -1.20% | Global; sharper in developed markets | Long term (≥ 4 years) |

| Challenges associated with product misconceptions, misinformation, and adherence issues | -0.50% | Global; higher in developing regions | Short term (≤ 2 years) |

| Cultural and religious opposition in select regions | -0.60% | Middle East, Africa, conservative pockets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mounting Litigation Risk Linked to Hormone-Related Adverse Events

Class-action suits tied to thrombotic events and newly flagged psychiatric outcomes continue to dent brand reputations, exemplified by thousands of Depo-Provera filings in U.S. courts. Escalating legal reserves weigh on budgets for marketing and innovation, tempering the growth slope of the contraceptive pills market.

Emergence of Long-Acting Reversible Contraceptives (LARCs)

IUDs and implants offer up to 10-year protection with failure rates below 1%, attracting users who prioritize convenience. An uptick to 10.4% LARC usage among U.S. women aged 15-49 signals substitution that directly siphons volume from daily pills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hormone Type: Combination Pills Remain Dominant Amid POP Momentum

Combination formulations controlled 85.7% of the contraceptive pills market share in 2024, underpinned by favorable reimbursement histories and clinician familiarity. Yet progestin-only pills are expanding at a 7.97% CAGR that outstrips the overall contraceptive pills market. The July 2023 FDA clearance of OTC Opill, which reached shelves in March 2024, validated POP safety profiles for self-administration and emboldened copycat applications[4]ACOG Staff, “First Over-the-Counter Daily Contraceptive Pill Released,” American College of Obstetricians and Gynecologists, acog.org . Clinical data from a 2025 Danish cohort study linking combined estrogen exposure with doubled ischemic stroke risk is accelerating physician rotation toward estrogen-free options.

Pharmaceutical pipelines now target refined POP delivery—film-coated tablets, biodegradable implants, and vaginal rings—that mitigate breakthrough bleeding but maintain systemic neutrality. Originator companies are also filing for expanded indications, such as acne reduction, to offset narrowing combination margins. Taken together, these trends should lift the progestin-only slice of the contraceptive pills market size significantly by 2030.

By Dosage Regimen: Extended Cycles Disrupt Traditional Patterns

The classic 28-day pack still captured 57.3% of the contraceptive pills market size in 2024, but extended/continuous schedules are on pace for an 9.23% CAGR, the quickest among all regimens. Women cite fewer bleeding episodes, lower cramp frequency, and better lifestyle fit as purchase motivators. Randomized trials demonstrate that 24/4 dosing lowers pregnancy incidence more effectively than 21/7 protocols while sustaining similar side-effect tolerability.

DTC platforms amplify awareness through personalized app reminders, nudging consumers to ask for extended cycles during virtual consults. Manufacturers are answering with flexible packs—four annual withdrawal bleeds—that encourage brand switching without raising manufacturing costs. Wider acceptance could push extended cycles toward a double-digit share of the contraceptive pills market by the decade’s close.

By Category: Generic Dominance Reshapes Pricing Dynamics

Generics owned 61.3% of the contraceptive pills market size in 2024 and will likely widen that edge at an 8.65% CAGR through 2030 as patent cliffs multiply. Regulatory agencies openly crack down on “pay-for-delay” deals, such as the FTC’s action against Warner Chilcott, ensuring cheaper alternatives arrive swiftly. Insurers and DTC pharmacies favor generics to trim formulary costs, steering volume away from branded SKUs.

Branded incumbents counter with novel estrogen-progestin ratios, tamper-evident dispensers, and loyalty programs that bundle teleconsultation credits. Although these tactics safeguard niche revenue, generic price erosion continues to anchor lower average selling prices across the contraceptive pills market.

By Distribution Channel: Online Pharmacies Challenge Retail Supremacy

Brick-and-mortar outlets held 52.3% of the contraceptive pills market share in 2024, but online channels are scaling at a 9.75% CAGR, energized by integrated telehealth models. Restrictions on reproductive health services in some U.S. states, following the Dobbs decision, triggered prescription declines in local pharmacies yet rerouted demand to mail-order providers. The convenience of smartphone ordering, discreet packaging, and auto-refill logistics converge to improve adherence and retention for monthly users.

Retail chains are experimenting with hybrid approaches—digital ordering plus in-store pickup—but must still navigate patchwork pharmacist-prescribing laws. As more jurisdictions grant over-the-counter status to oral contraceptives, the online segment stands to absorb incremental volume, raising its slice of the contraceptive pills market by mid-decade.

By Age Group: Younger Demographics Drive Innovation

Women aged 25-34 commanded 43.6% of the contraceptive pills market in 2024, reflecting peak fertility postponement. However, the 15-24 cohort is the fastest-rising segment at a 8.25% CAGR as targeted awareness campaigns and school-based sex-education syllabi gain traction. A 2024 study in Ethiopia showed younger women remain 31% less likely to use pills than those aged 25-34, pointing to notable headroom for gains.

Manufacturers align marketing with influencer-led formats and app-connected reminder devices, weaving convenience into lifestyle. For women over 45, clinical guidance shifts toward progestin-only or non-hormonal methods, yet symptom management opportunities spur research into low-dose regimens that straddle contraception and perimenopausal relief. Collectively, age-specific strategies broaden the demand surface of the contraceptive pills market.

Geography Analysis

North America led with 36.67% of the contraceptive pills market in 2024, catalyzed by progressive regulatory shifts and broad insurance coverage. The OTC launch of Opill at USD 19.99 has widened pharmacy-checkout access and chipped away at prescription gatekeeping. Yet, policy divergence is stark; states that enacted full abortion bans recorded a 4.1% drop in oral pill fills within a year, underscoring how legal climates modulate regional sales. The contraceptive pills market size is likely to keep expanding as more states empower pharmacists to dispense without a physician's note.

Asia-Pacific posts the fastest 8.85% CAGR for 2025-2030 as government-backed family-planning drives intersect rising female workforce participation. Urban India, Indonesia, and Vietnam headline volume growth, while rural pockets still battle supply gaps. Variations in contraceptive prevalence across demographics persist, but structural investments in public-sector distribution and mobile health units should narrow disparities.

Europe maintains a high baseline of contraceptive prevalence, yet safety-driven shifts toward low-dose estrogen and emerging POPs rekindle moderate value growth. Eastern European reimbursement reforms present fresh volume avenues, whereas Western Europe emphasizes differentiated formulations with minimal side effects.

The Middle East and Africa and South America together represent an under-penetrated frontier for the contraceptive pills industry. Urbanization and female-education gains support incremental adoption, but cultural resistance and logistics shortfalls still hinder uniform access. Funding partners such as UNFPA and USAID increased contraceptive procurement spending to USD 237 million in FY 2023, supporting improved supply reliability.

Competitive Landscape

The contraceptive pills market is moderately concentrated. Bayer, Pfizer, and Organon collectively command substantial revenue via cross-portfolio breadth and geographic reach. Organon alone attributed USD 1.8 billion—28% of its 2024 turnover—to women’s health. Perrigo’s FDA-sanctioned OTC launch created a new competitive angle that compels legacy firms to streamline Rx-to-OTC switch strategies or risk ceding share.

Generic manufacturers, particularly in India and Israel, flood mature molecules at aggressive price points. Telehealth unicorns Ro and Hims & Hers weaponize data analytics to personalize pill selection, leading many first-time users to skip traditional physician pathways altogether. Forward-looking incumbents court digital partnerships, integrate refill tracking apps, and pilot adherence gamification to preserve relevance.

White-space innovation focuses on hormone-free modalities and male contraceptive candidates such as YCT-529 now in Phase 2 trials, signaling future threat vectors beyond today’s oral category. Firms able to bundle multichannel distribution with next-generation science stand to fortify positions as the contraceptive pills market evolves.

Contraceptive Pills Industry Leaders

Bayer AG

Pfizer Inc.

Abbvie Inc.

Organon & Co.

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Organon filed with the FDA to extend Nexplanon’s duration of effectiveness to five years, strengthening its LARC proposition.

- April 2025: Phase 2 human trials for YCT-529, a hormone-free male oral pill, commenced in New Zealand, aiming for late-2025 read-outs.

- March 2025: Pharmacist prescribing authority reached 30 U.S. states plus DC, broadening behind-the-counter access.

- March 2025: Pharmac announced funding for desogestrel (Cerazette) in New Zealand, expanding national POP availability.

Global Contraceptive Pills Market Report Scope

As per the scope of the report, Contraceptive pills are medications taken by women to prevent pregnancy. They typically contain hormones like estrogen and progestin that regulate or inhibit ovulation. These pills also thicken cervical mucus to block sperm entry.

The contraceptive pills market is segmented by Hormone Type (Progestin-Only Pills and Combination Pills), Dose Regimen (21- Day Cyle, 24- Day Cycle, 28- Day Cucle, and Extended Cycle), Category (Generic and Branded), Distribution Channel(Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), Age Group (15 – 24 Years, 25 – 34 Years, 35- 44 Years, and 44+ Years) and geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Progestin-Only Pills | |

| Combination Pills | Monophasic |

| Biphasic | |

| Triphasic | |

| Other Combination Formulations |

| 21-Day Cycle |

| 24-Day Cycle |

| 28-Day Cycle |

| Extended / Continuous Cycle |

| Generic |

| Branded |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| 15 - 24 Years |

| 25 -34 Years |

| 35 - 44 Years |

| 45 + Years |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Hormone Type | Progestin-Only Pills | |

| Combination Pills | Monophasic | |

| Biphasic | ||

| Triphasic | ||

| Other Combination Formulations | ||

| By Dosage Regimen | 21-Day Cycle | |

| 24-Day Cycle | ||

| 28-Day Cycle | ||

| Extended / Continuous Cycle | ||

| By Category | Generic | |

| Branded | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Age Group | 15 - 24 Years | |

| 25 -34 Years | ||

| 35 - 44 Years | ||

| 45 + Years | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the contraceptive pills market ?

The contraceptive pills market was valued at USD 7.98 billion in 2025 and is projected to reach USD 11.17 billion by 2030.

Which region leads global sales?

North America held 36.67% of global revenue in 2024, supported by favorable regulation and broad insurance coverage.

Which is the fastest growing region in contraceptive pills market ?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

How fast are online pharmacies growing in the space ?

Online pharmacies record a 9.75% CAGR for 2025-2030, the quickest among all distribution channels thanks to telehealth integration.

Why are progestin-only fills in focus?

Progestin-only pills show lower cardiovascular risk, gained OTC approval through Opill, and are expanding at a 7.97% CAGR.

Page last updated on: