Biomedical Pressure Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

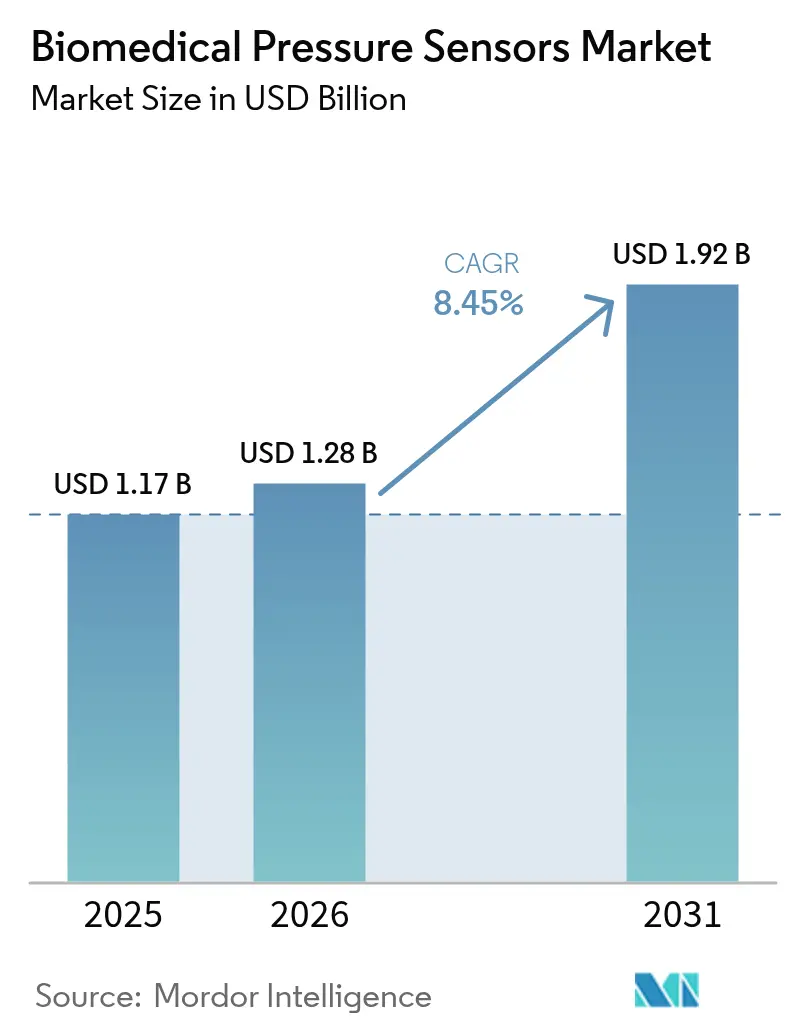

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

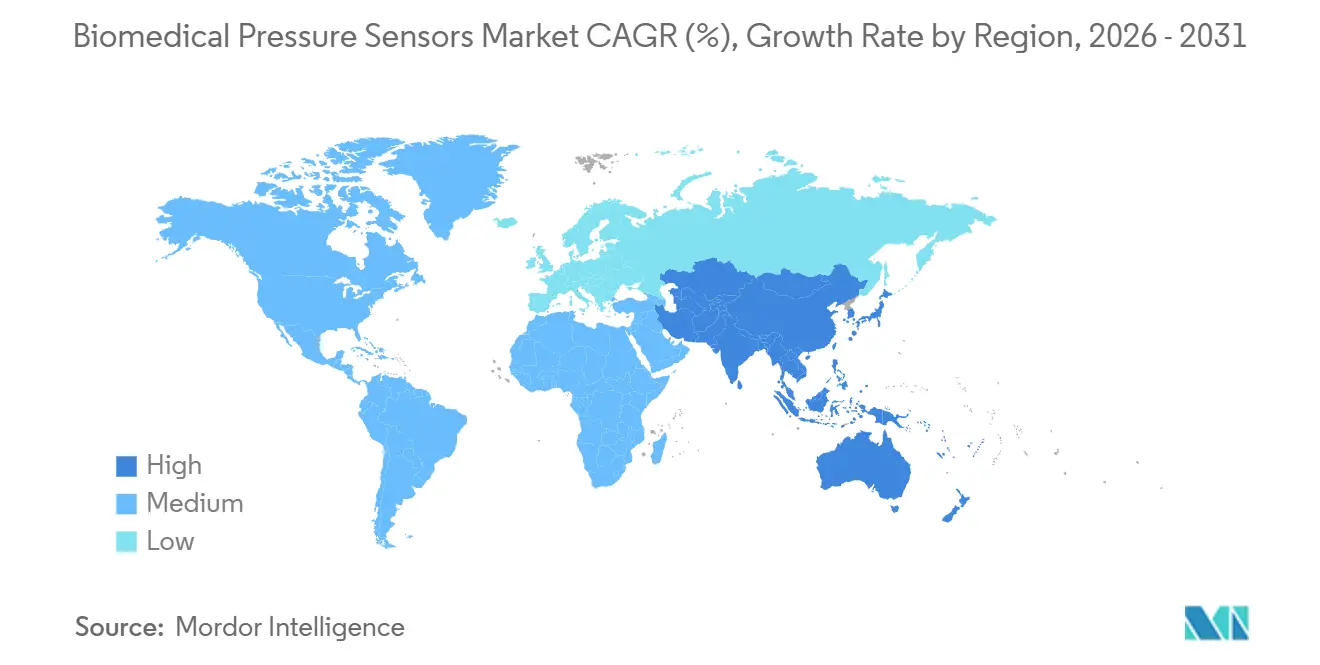

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomedical Pressure Sensors Market Analysis by Mordor Intelligence

The biomedical pressure sensors market size is expected to grow from USD 1.17 billion in 2025 to USD 1.28 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 8.45% CAGR over 2026-2031. Miniaturized MEMS designs below 2 millimeters now achieve sub-1% accuracy, enabling catheter-based and fully implantable devices. U.S. and European reimbursement for remote physiologic monitoring has accelerated first-time home-care deployments, while Healthy China 2030 and India’s Production Linked Incentive scheme are broadening the installed base in Asia-Pacific. Wireless passive architectures are closing the reliability gap with battery-powered telemetric designs, positioning the biomedical pressure sensors market for sustained double-digit growth in consumer wearables that deliver continuous blood-pressure data outside clinical environments. Consolidation among large device makers underscores the race to pair sensors with digital-twin software that predicts decompensation and guides therapy adjustments.

Key Report Takeaways

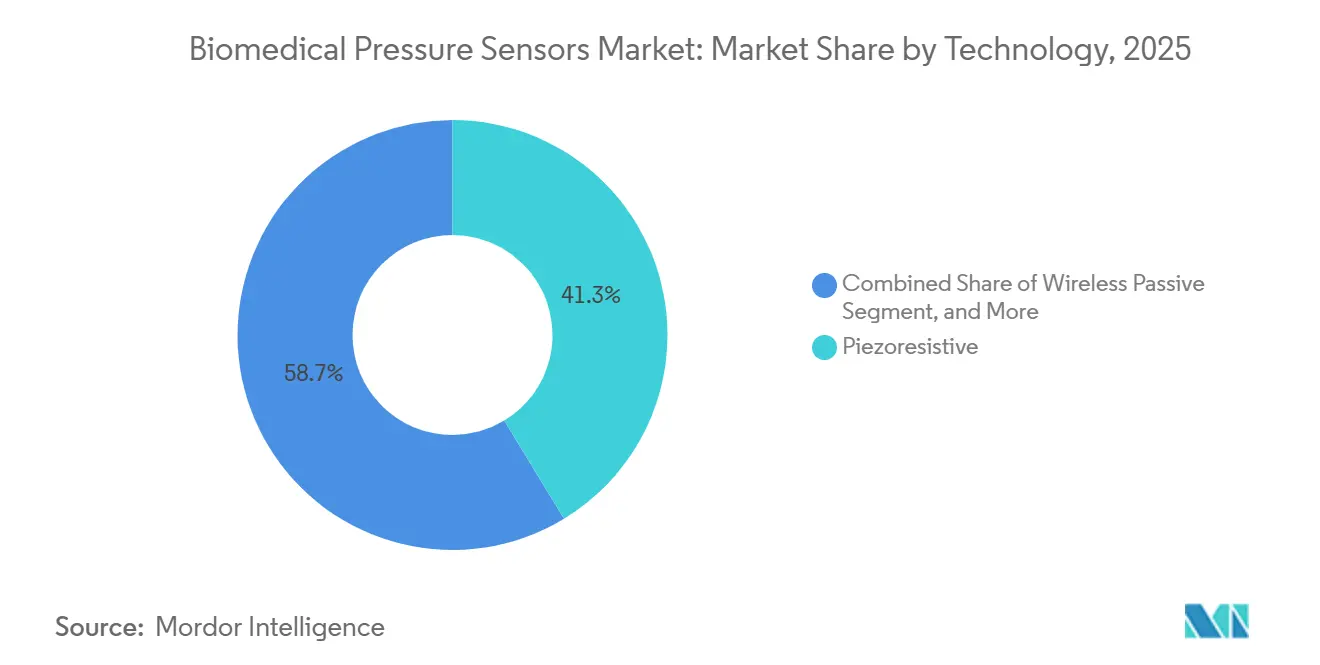

- By technology, piezoresistive architectures led with 41.32% of biomedical pressure sensors market share in 2025, while wireless passive sensors are projected to expand at an 11.41% CAGR through 2031.

- By application, monitoring held 36.82% of the biomedical pressure sensors market size in 2025, whereas fitness and wellness is forecast to grow at a 10.67% CAGR between 2026-2031.

- By end-user, hospitals and clinics accounted for 48.14% revenue in 2025; home-care settings represent the fastest trajectory at a 10.63% CAGR to 2031.

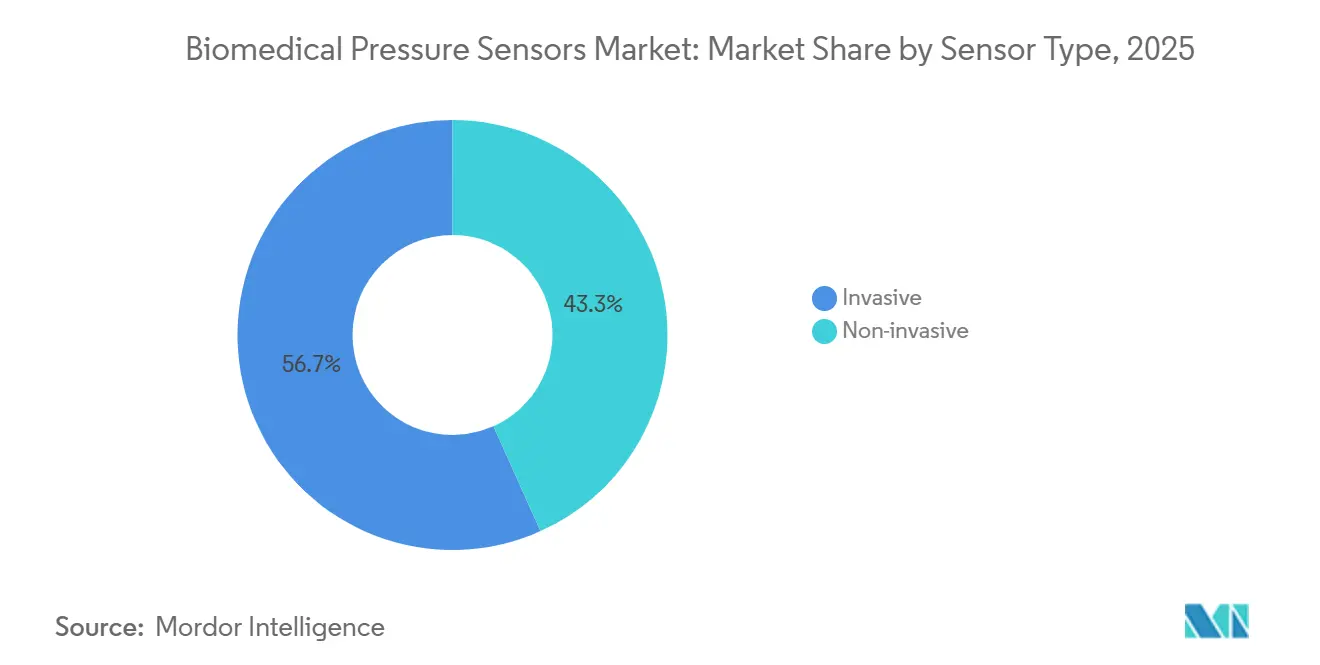

- By sensor type, invasive devices retained 56.72% share of the biomedical pressure sensors market size in 2025, yet non-invasive variants are advancing at a 9.23% CAGR over 2026-2031.

- By geography, North America captured 35.41% share in 2025, while Asia-Pacific is on track for a 10.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomedical Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases driving continuous physiological monitoring | +2.5% | Global, with pronounced effect in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Adoption surge in remote-patient-monitoring and tele-health pressure patches | +2.0% | North America and Europe, expanding to Asia-Pacific and Middle East | Medium term (2-4 years) |

| Miniaturization and MEMS breakthroughs enabling invasive/implantable devices | +1.5% | Global, led by advanced manufacturing hubs in United States, Germany, Japan, South Korea | Long term (≥ 4 years) |

| Integration with digital-twin haemodynamic-modelling platforms | +0.8% | North America and Europe, early adoption in academic medical centers | Medium term (2-4 years) |

| Force-feedback requirements in robotic minimally-invasive surgery | +0.7% | North America, Europe, and select Asia-Pacific markets (Japan, South Korea, Singapore) | Medium term (2-4 years) |

| Growing demand for low-cost, high-performance, reliable sensors | +0.5% | Global, strongest in price-sensitive markets across Asia-Pacific, South America, and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Driving Continuous Physiological Monitoring

Hypertension affected 1.28 billion adults in 2025, up 23% from 2019, while heart-failure prevalence reached 64 million worldwide, prompting long-term sensor implantation to guide medication titration.[1]World Health Organization, “Hypertension Dashboard,” who.int Uncontrolled hypertension contributed to 691,000 U.S. deaths in 2024, elevating demand for real-time pressure data that alerts clinicians before decompensation.[2]Centers for Disease Control and Prevention, “National Center for Health Statistics Mortality Data,” cdc.gov Diabetes and aging demographics further widen the patient pool, and Medicare’s CPT 99458 now reimburses USD 50 per patient each month for remote readings, accelerating adoption in cardiology practices. Continuous monitoring therefore remains the single largest growth catalyst for the biomedical pressure sensors market.

Adoption Surge in Remote-Patient-Monitoring and Tele-Health Pressure Patches

RPM enrollment reached 71 million Americans in 2025, with blood-pressure devices comprising 57% of episodes.[3]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule,” cms.gov FDA-cleared Bluetooth patches enable at-home arterial waveform capture, reducing hospitalizations by 57% in the CHAMPION cohort. The U.S. Department of Veterans Affairs deployed 120,000 LTE-enabled cuffs that cut hypertensive crises by 34%. German and Dutch payers mirrored U.S. reimbursement in 2024, extending momentum into Europe. AI-driven algorithms that identify destabilizing trends 48-72 hours in advance further embed sensors into tele-cardiology workflows, cementing the biomedical pressure sensors market as a linchpin of value-based care.

Miniaturization and MEMS Breakthroughs Enabling Invasive/Implantable Devices

TE Connectivity’s 1.8-millimeter IntraSense achieved 0.25% full-scale accuracy across a –40 °C to 125 °C window. STMicroelectronics’ silicon-on-insulator process cut parasitic capacitance by 40%, yielding 3.5 µA power draw and 7-10-year implant life. Capacitive MEMS arrays reached 0.1% non-linearity, opening precision ventilator control. IEEE-published prototypes with integrated wireless power coils now eliminate percutaneous leads, reducing infection rates once pegged at 18%. Collectively, these advances scale the biomedical pressure sensors market beyond critical-care wards into fully implanted chronic-disease solutions.

Integration With Digital-Twin Haemodynamic-Modelling Platforms

FDA-validated computational-modeling guidance in 2024 cleared the path for cardiovascular digital twins that ingest real-time pressure data to forecast decompensation seven days ahead with 82% sensitivity. Siemens Healthineers and Philips commercialized software that simulates intervention outcomes, trimming unnecessary catheterizations by 32%. HeartFlow’s FFRct rollout to 1,200 hospitals underscores market appetite for data-rich planning tools. With the International Medical Device Regulators Forum preparing AI validation standards, ecosystem alignment is progressing, lifting the long-term value proposition of biomedical pressure sensors market data feeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdictional safety and biocompatibility approvals | -1.2% | Global, particularly Europe (MDR), United States (FDA), Japan (PMDA), China (NMPA) | Long term (≥ 4 years) |

| Bio-fouling-driven signal drift in long-term implantables | -0.8% | Global, most acute in invasive sensor applications | Medium term (2-4 years) |

| Environmental impact on sensor stability (temperature, humidity, radiology) | -0.5% | Global, heightened in extreme-climate regions and high-radiation environments | Medium term (2-4 years) |

| Lack of meaningful product differentiation commoditising ASPs | -0.4% | Global, strongest pressure in mature markets (North America, Europe) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Safety and Biocompatibility Approvals

Europe’s MDR 2017/745 now demands full clinical evaluations, adding up to two years and USD 400,000 in testing costs per variant. Japan’s revised GCP ordinances require prospective trials, while China’s priority review favors domestic producers. Start-ups confronted by these hurdles saw venture funding dip 28% between 2024-2025. The cumulative drag subtracts 1.2 percentage points from biomedical pressure sensors market CAGR.

Bio-Fouling-Driven Signal Drift in Long-Term Implantables

Protein adsorption forms a fibrinogen film within minutes, derailing accuracy by up to 5 mmHg in the first week. Collagen encapsulation induces 3-8% hysteresis errors over months. Drug-eluting dexamethasone coatings cut capsule thickness 60% yet raise infection concerns. Quarterly recalibration inflates follow-up costs, muting uptake in resource-constrained systems and restraining biomedical pressure sensors market revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wireless Passive Architectures Gain Ground Despite Piezoresistive Dominance

Wireless passive sensors are forecast to grow at 11.41% CAGR during 2026-2031, propelled by inductive and ultrasound interrogation that removes battery replacement surgeries. Piezoresistive designs still commanded 41.32% biomedical pressure sensors market share in 2025 because their 200 Hz bandwidth captures high-fidelity arterial waveforms. The biomedical pressure sensors market size for wireless passive devices is projected to climb from USD 0.26 billion in 2026 to USD 0.49 billion by 2031. Fiber-optic and capacitive variants hold niche roles where MRI compatibility or long-term drift resistance outweigh cost. Continuous MEMS innovation should narrow unit-cost gaps, accelerating the shift toward battery-free architectures.

In clinical settings, piezoresistive transducers remain indispensable for cardiac surgery, yet major purchasers now pilot passive pulmonary-artery implants for chronic heart-failure monitoring. Self-calibrating prototypes that maintain 0.1% accuracy across 24 months could further displace incumbent technologies by late-decade. Manufacturers must, however, validate wireless energy coupling against MDR electromagnetic-compatibility clauses, a gating step that may stagger rollouts across regions.

By Application: Fitness and Wellness Outpaces Traditional Clinical Monitoring

Monitoring represented 36.82% of 2025 revenue, but growth has leveled in OECD intensive-care units where device penetration exceeds 85%. Conversely, the fitness and wellness segment is slated for a 10.67% CAGR to 2031, lifting its biomedical pressure sensors market size from USD 0.18 billion in 2026 to USD 0.30 billion by 2031. Consumer demand for unobtrusive, cuff-less blood-pressure tracking fuels this trajectory.

Wearables now integrate optical tonometry and machine learning to reach 5-mmHg accuracy, winning CE marking in 2025. Diagnostic and therapeutic niches still rely on invasive sensors for gold-standard precision, yet procedure-volume declines in cardiac catheterization temper their expansion. Industrial bioprocess applications add steady incremental demand, but remain peripheral to core healthcare revenue streams of the biomedical pressure sensors market.

By Sensor Type: Non-Invasive Designs Narrow the Accuracy Gap

Invasive devices held 56.72% of the biomedical pressure sensors market size in 2025, valued at USD 0.65 billion, given their beat-to-beat fidelity during shock states. Non-invasive sensors, projected to grow at 9.23% CAGR, should lift their revenue share to 48% by 2031. The biomedical pressure sensors market share for oscillometric cuffs may shrink as finger photoplethysmography and radial-tonometry watches achieve validation under updated AMA protocols.

Hybrid systems such as Edwards ClearSight combine an initial arterial-line calibration with finger optics, sustaining 5-mmHg accuracy for 12 hours. Regulatory distinctions—Class II for invasive and Class I/II for most non-invasive devices—accelerate commercialization of cuff-less monitors, yet clinicians still favor direct catheters when patient hemodynamics are unstable.

By End-User: Home-Care Settings Redefine Market Geography

Hospitals and clinics generated 48.14% of 2025 revenue as ICUs depend on disposables for septic shock and ARDS monitoring. Nonetheless, home-care settings are forecast to post a 10.63% CAGR, boosting their biomedical pressure sensors market size from USD 0.24 billion in 2026 to USD 0.40 billion by 2031. CMS reimbursement removed economic barriers for implantable pulmonary-artery sensors, resulting in 12,000 implants in Q1-2025 alone.

Ambulatory surgery centers favor single-use disposables, while elite sports organizations instrument athletes for exertional hypertension surveillance. Research institutes capture a steady 9% share thanks to NIH’s USD 47 million in 2025 grants. FDA draft human-factors guidance effective 2026 will require 95% task-success among seniors, shaping future design language for at-home devices.

Geography Analysis

North America contributed 35.41% of global revenue in 2025, underpinned by Medicare’s USD 50 monthly reimbursement and 6,090 U.S. hospitals equipped for invasive monitoring. Canada invested USD 880 million to outfit rural clinics with wireless cuffs, and Mexico procured 45,000 monitors for mass hypertension screening, supporting 9.1% CAGR in the region. The biomedical pressure sensors market benefits from USMCA regulatory harmonization that trims clearance lead-times by up to nine months.

Asia-Pacific is projected to grow at 10.32% CAGR through 2031, driven by China’s USD 2.2 trillion Healthy China budget and India’s 5% subsidies for domestic production. Japan’s public insurers now reimburse 80% of implantable-sensor costs, while South Korea pays KRW 30,000 monthly for home cuffs. Mutual recognition between Australia and New Zealand speeds launches, yet ASEAN’s non-binding directive forces country-by-country filings, elongating timelines for multinationals.

Europe held 28% share in 2025, with Germany covering RPM for 4.2 million patients. The NHS bought 180,000 wireless monitors under its cardiovascular mortality plan. MDR compliance costs, however, add EUR 80,000-150,000 annually per device family, challenging smaller entrants. South America and MEA markets post high-single-digit growth aided by Brazil’s ANVISA approvals and Saudi Vision 2030 hospital builds, yet currency volatility and limited regulatory capacity temper acceleration.

Competitive Landscape

The biomedical pressure sensors market is moderately concentrated; the top five suppliers controlled roughly 42% revenue in 2025. Edwards Lifesciences’ USD 1 billion acquisition of Endotronix secured wireless-pulmonary intellectual property, while Boston Scientific’s USD 14.5 billion Penumbra deal broadened neuro-vascular sensing reach. Large conglomerates leverage global distribution and regulatory muscle, whereas niche innovators differentiate via fiber-optic or battery-free designs.

Component vendors TE Connectivity and Honeywell target commoditized segments with sub-USD 10 sensors, pressuring mid-tier margins. Chinese newcomers armed with ISO 13485 certificates challenge incumbents on price, pushing Western firms to pivot toward software-enhanced value propositions. Emerging disruptors Aktiia and Biobeat attracted a combined USD 50 million in 2025-2026 funding rounds, underscoring investor appetite for cuff-less wearables.

Intellectual-property filings emphasize piezoelectric harvesting and RF backscatter, with 14 U.S. patent families issued in 2024-2025. Ongoing compliance with IEC 60601-1 and ISO 14971 prolongs time-to-market, reinforcing advantages for diversified industry leaders. Overall, competition revolves around integrating sensors with analytic platforms that translate raw pressure data into actionable clinical guidance, a trend redefining value creation in the biomedical pressure sensors industry.

Biomedical Pressure Sensors Industry Leaders

Resonetics LLC

Medtronic plc

Edwards Lifesciences Corporation

Sensirion Holding AG

TE Connectivity Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Abbott received FDA premarket approval for its CardioMEMS HF System with extended wireless range, reducing transmission failures by 34%.

- February 2026: Boston Scientific completed its USD 14.5 billion acquisition of Penumbra, entering neuro-vascular pressure sensing.

- January 2026: Siemens Healthineers launched the Atellica VTLI Analyzer with integrated flow-rate pressure sensors, cutting sample errors by 22%.

- November 2026: Philips gained FDA clearance for IntelliVue X3 monitors using disposable capacitive diaphragms to curb infection risk.

Global Biomedical Pressure Sensors Market Report Scope

Biomedical pressure sensors are used in applications that target three major respiratory disorders: asthma, chronic obstructive pulmonary disease, and sleep apnea. They are used in diagnostic equipment to measure the pressure of air expelled from the lungs and therapeutic equipment, such as oxygen therapy equipment, nebulizers, and ventilators.

The Medical Pressure Sensors Market Report is Segmented by Technology (Self-calibrating, Fiber-optic, Telemetric, Capacitive, Wireless Passive, Piezoresistive), Application (Diagnostic, Therapeutic, Medical Imaging, Monitoring, Fitness and Wellness, Other Applications), End-user (Hospitals and Clinics, Ambulatory Surgery Centres, Home-care Settings, Sports and Fitness Facilities, Research Institutes), Sensor Type (Invasive, Non-invasive), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| Self-calibrating |

| Fiber-optic |

| Telemetric |

| Capacitive |

| Wireless Passive |

| Piezoresistive |

| Diagnostic |

| Therapeutic |

| Medical Imaging |

| Monitoring |

| Fitness and Wellness |

| Other Applications |

| Invasive |

| Non-invasive |

| Hospitals Clinics |

| Ambulatory Surgery Centres |

| Home-care Settings |

| Sports and Fitness Facilities |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Technology | Self-calibrating | |

| Fiber-optic | ||

| Telemetric | ||

| Capacitive | ||

| Wireless Passive | ||

| Piezoresistive | ||

| By Application | Diagnostic | |

| Therapeutic | ||

| Medical Imaging | ||

| Monitoring | ||

| Fitness and Wellness | ||

| Other Applications | ||

| By Sensor Type | Invasive | |

| Non-invasive | ||

| By End-user | Hospitals Clinics | |

| Ambulatory Surgery Centres | ||

| Home-care Settings | ||

| Sports and Fitness Facilities | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the biomedical pressure sensors market be by 2031?

It is forecast to reach USD 1.92 billion by 2031, expanding at an 8.45% CAGR from 2026-2031.

Which technology segment is growing fastest?

Wireless passive architectures are projected for an 11.41% CAGR because they eliminate battery-related replacement surgeries.

Why is Asia-Pacific considered the most attractive growth region?

China’s CNY 16 trillion Healthy China investment and India’s 5% manufacturing subsidies are lifting regional demand, supporting a 10.32% CAGR through 2031.

What is the main regulatory hurdle for new entrants?

Europe’s MDR 2017/745 adds up to two years of clinical evaluation and significant compliance costs, delaying commercialization.

How are wearable devices impacting adoption?

Consumer wearables validated to within 5 mmHg accuracy are shifting monitoring from hospitals to homes, driving the fastest-growing fitness and wellness application segment.

Which companies are leading recent consolidation?

Edwards Lifesciences and Boston Scientific have made billion-dollar acquisitions to secure wireless and neuro-vascular sensing capabilities respectively.

Page last updated on: