Glacial Acetic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 12.38 Million tons |

| Market Volume (2031) | 16.12 Million tons |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

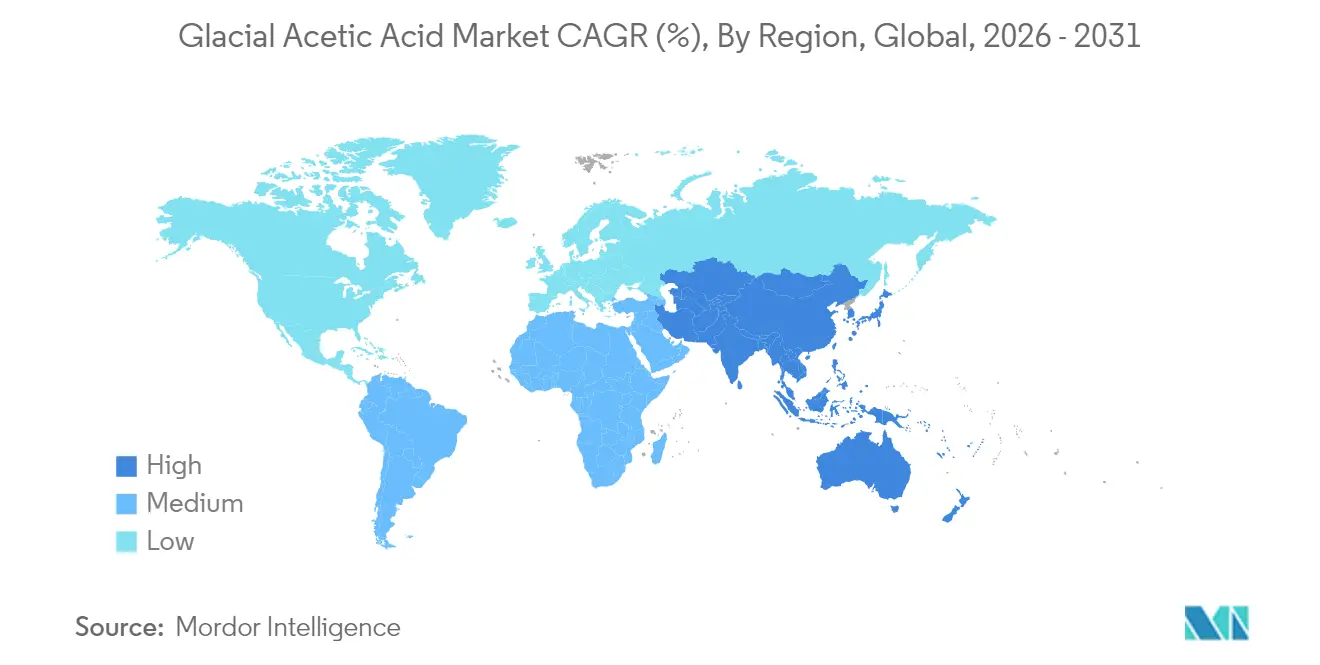

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glacial Acetic Acid Market Analysis by Mordor Intelligence

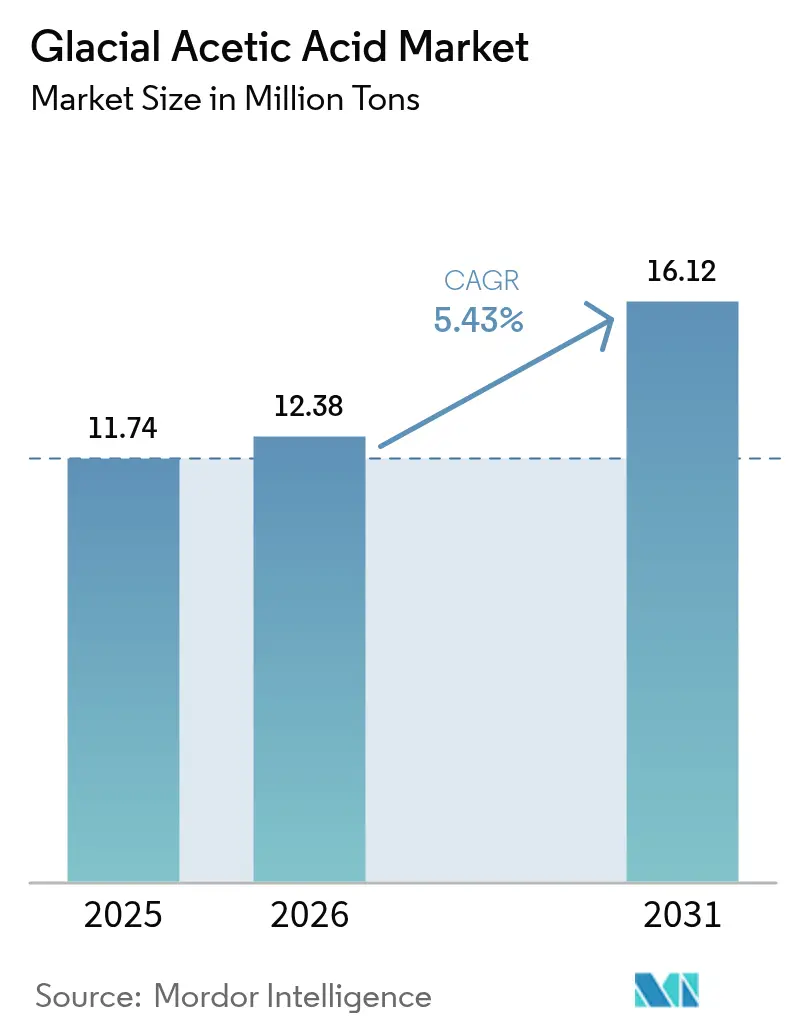

The Glacial Acetic Acid market size is expected to grow from 11.74 Million tons in 2025 to 12.38 Million tons in 2026 and is forecast to reach 16.12 Million tons by 2031 at 5.43% CAGR over 2026-2031. Volume growth is anchored in vinyl acetate monomer (VAM) demand, pharmaceutical excipient uptake, and resilient consumption in food preservation. Bio-based production technologies are moving into commercial scale, loosening the traditional link between acetic acid output and fossil feedstocks and positioning early adopters for margin protection. Regional production shifts toward Asia-Pacific are changing trade flows as North American and European producers lean into specialty grades. Methanol price volatility and tighter occupational-safety norms are challenging unintegrated players, yet integrated firms with captive methanol or alternative feedstocks continue to defend profitability. Strategic investments in low-carbon processes and ultra-high-purity grades have emerged as competitive differentiators, particularly for companies targeting electronics and pharmaceutical customers.

Key Report Takeaways

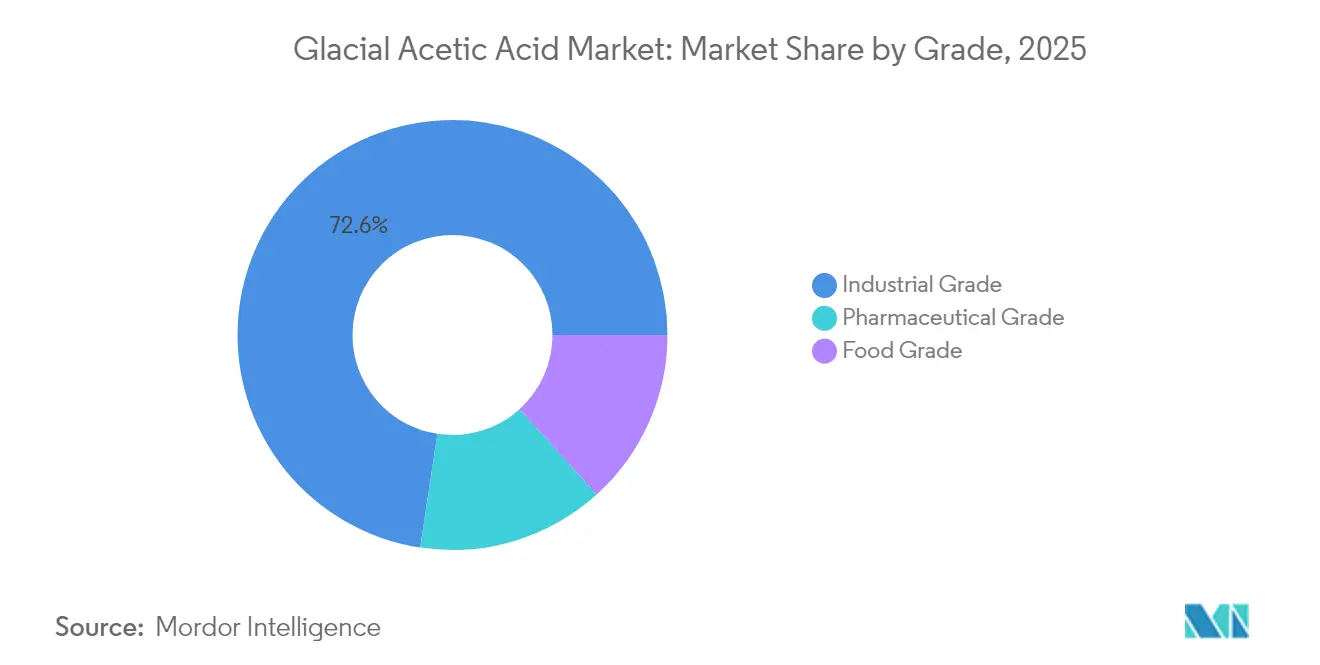

- By grade, Industrial Grade led with 72.60% of the glacial acetic acid market share in 2025, while Pharmaceutical Grade is projected to expand at a 6.82% CAGR to 2031.

- By application, VAM production accounted for 34.70% of the glacial acetic acid market size in 2025 and Solvents are growing at a 6.43% CAGR through 2031.

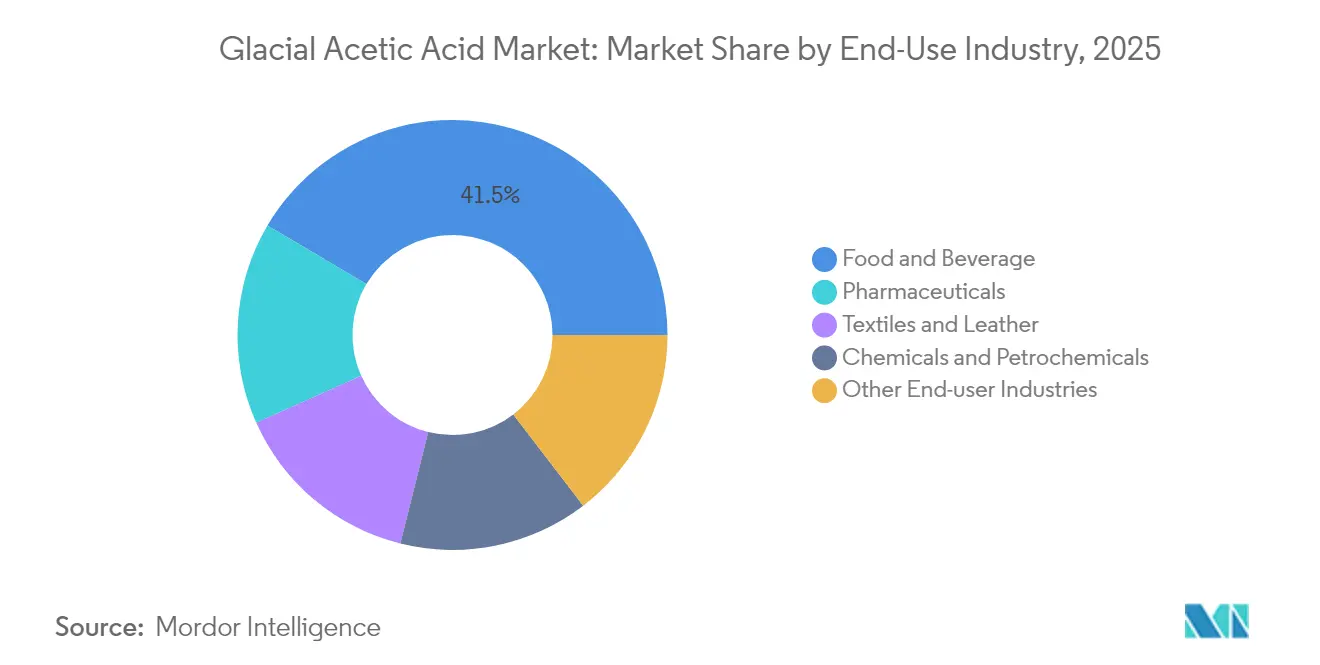

- By end-use industry, Food and Beverage held 41.50% of the glacial acetic acid market size in 2025 and Pharmaceuticals posts the highest 6.69% CAGR to 2031.

- By region, Asia-Pacific captured 62.60% of the glacial acetic acid market share in 2025 and advances at a 6.72% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glacial Acetic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Production Capacity in Asia-Pacific to Serve Vinyl Acetae Momomer( VAM) Demand | +1.8% | Asia-Pacific with spillover to North America | Medium term (2-4 years) |

| Increasing Adoption of Bio-based Feedstock in Acetic Acid Manufacturing | +1.2% | Global with early moves in Europe and North America | Long term (≥ 4 years) |

| Rising Demand from Pharmaceutical Excipients in Emerging Economies | +0.9% | Asia-Pacific, notably India and China | Medium term (2-4 years) |

| Growth of Solvent Applications in Adhesives and Sealants | +0.7% | Global with concentration in Asia-Pacific | Short term (≤ 2 years) |

| Textile Industry Revival in Southeast Asia Boosting Acetic Acid Dyeing Agents | +0.5% | Vietnam and Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Production Capacity in Asia-Pacific to Serve Vinyl Acetate Monomer Demand

- Asia-Pacific producers are adding large-scale acetic acid units to secure VAM feedstock. Jiangsu Sopo’s 450 kt expansion and GNFC’s planned 200 kt unit illustrate the region’s push toward self-sufficiency[1]Federation of Indian Petroleum Industry, “Acetic Acid: A Versatile Chemical – Production Processes and Advancements,” fipi.org.in. This capacity wave is tilting global trade balances and nudging North American and European suppliers toward higher-value derivatives. As VAM demand in adhesives, paints, and flexible packaging climbs, integrated producers in China, India, and Japan are locking in scale advantages. Downstream converters benefit from shorter supply chains and reduced freight costs, adding momentum to regional manufacturing.

Increasing Adoption of Bio-based Feedstock in Acetic Acid Manufacturing

Commercialization of carbon-capture and biomass-based routes is lowering life-cycle emissions. Again’s flue-gas-to-acetic-acid process reduces reliance on methanol and attracts sustainability-driven buyers, while New Iridium’s photochemical route targets cellulosic waste streams. Producer interest in these pathways is also a hedge against methanol volatility and tightening carbon regulations. Long-term offtake agreements with consumer-goods companies seeking low-carbon ingredients further underpin investment cases.

Rising Demand from Pharmaceutical Excipients in Emerging Economies

Pharmaceutical grade glacial acetic acid benefits from capacity upgrades at Indian and Chinese active pharmaceutical ingredient (API) clusters. High-purity material is essential for acetaminophen, antibiotic intermediates, and injectable formulations. As local drug makers transition from bulk generics to complex therapies, purity thresholds tighten, creating premium margins for suppliers certified to current Good Manufacturing Practices.

Growth of Solvent Applications in Adhesives and Sealants

Silicone sealant formulations and advanced adhesive systems employ glacial acetic acid as a reactive solvent that accelerates cure time and improves moisture resistance. Regulatory pressure on volatile organic compounds (VOC) is shifting demand toward formulations where acetic acid offers lower toxicity and predictable evaporation rates[2]GJ Chemical, “Glacial Acetic Acid Now Available in Bulk,” gjchemical.com . Construction rebound in Asia and infrastructure renewal in North America support near-term volume gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Methanol Feed-stock Prices | –1.2% | Global, highest impact where producers lack captive methanol | Short term (≤ 2 years) |

| Stringent Occupational-Safety Norms Limiting Handling and Storage | –0.6% | North America and Europe with gradual extension to Asia-Pacific | Medium term (2-4 years) |

| Supply–Demand Imbalances Causing Price Suppression | –0.8% | Global, most pronounced in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Methanol Feedstock Prices

Methanol spot prices swung sharply during 2024, compressing producer margins and complicating capacity planning. Unintegrated plants were hardest hit, prompting renewed interest in hedging tools and alternative feedstocks. Completion of Methanex’s acquisition of OCI’s methanol assets is expected to shift global bargaining power toward integrated giants.

Stringent Occupational-Safety Norms Limiting Handling and Storage

Updated U.S. Environmental Protection Agency rules require enhanced emission controls and upgraded ventilation in acetic acid handling areas. Compliance costs estimated at USD 455 million across the synthetic organic chemical sector are forcing smaller processors to reassess capital budgets[3]U.S. Environmental Protection Agency, “Regulatory Impact Analysis for SOCMI,” epa.gov . Similar frameworks are under review in the European Union, suggesting broader global adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharmaceutical Purity Commanding Premium

Industrial Grade dominated the glacial acetic acid market with a 72.60% share in 2025 as bulk producers supplied VAM plants and downstream chemical syntheses. The segment’s scale delivers cost leadership, yet profit sensitivity to methanol prices remains. Pharmaceutical Grade, though smaller, is on track for a 6.82% CAGR, reflecting stricter impurity limits in API synthesis and injectable formulations. Recent capacity additions in India’s Gujarat region illustrate producer moves to capture this higher-margin pool.

Demand for ultra-high-purity material in semiconductor wet processes is emerging as a lucrative niche. Linewidth reduction in advanced nodes heightens sensitivity to metallic contaminants, so producers able to deliver parts-per-billion impurity levels can command significant premiums. These offerings create a two-tier pricing environment in which standard pharmaceutical grade supports volume while electronics grade secures profitability. The opportunity aligns with national strategies in Japan and South Korea to safeguard chip-supply sovereignty, offering suppliers stable offtake commitments.

By Application: VAM Production Dominates Volume, Solvents Accelerate Growth

VAM production accounted for 34.70% of 2025 volumes, cementing its status as the anchor application for the glacial acetic acid market. Adhesives, paints, and flexible packaging all rely on VAM-derived polymers, linking acetic acid demand to construction and consumer-goods cycles. Capacity expansions in China and India ensure regional VAM assets are fully backward-integrated, preserving competitive position.

The Solvent segment is expanding at a 6.43% CAGR through 2031 as acetic-acid-based systems gain share in adhesives, sealants, and pharmaceutical formulations. Producers are tailoring solvent blends to comply with regional VOC standards and to enhance bond performance under humid conditions. Although the segment is smaller than VAM in tonnage, its higher price points and customer stickiness bolster margins, making it a strategic focus area.

By End-Use Industry: Food and Beverage Holds Scale, Pharmaceuticals Drive Momentum

Food and Beverage captured 41.50% of the glacial acetic acid market size in 2025, anchored in preservative and flavoring uses across condiments and pickled goods. Clean-label consumer trends support steady volume as manufacturers rely on acetic acid’s antimicrobial efficacy. Producers targeting this segment emphasize consistent sensory profiles and regulatory compliance.

Pharmaceuticals represent the fastest-growing end-use, rising at a 6.69% CAGR. Demand emanates from API makers and contract manufacturing organizations in Asia-Pacific, with procurement teams favoring vendors accredited to WHO and U.S. FDA standards. Chemicals and Petrochemicals remain the second-largest outlet, tied to VAM and downstream acetate esters, while Textile and Leather applications are rebounding in Southeast Asia due to garment production shifts

Geography Analysis

Asia-Pacific held 62.60% of the glacial acetic acid market in 2025 and is advancing at a 6.72% CAGR through 2031. China holds a significant share of the global methanol capacity, supported by state-linked financing and integrated methanol sourcing. India is scaling domestic output, and joint-venture discussions such as INEOS Acetyls with GNFC underline the nation’s import-replacement agenda. Japan and South Korea concentrate on high-purity niches for electronics and pharmaceuticals, fetching premium pricing.

North America ranks second by volume, anchored in the chemical and food industries. Department of Energy grants for bio-based acetic acid projects enable technology pilots that could lower carbon intensity and partially insulate the region from methanol swings. Trade policy uncertainty adds a cautionary tone, as tariff shifts may affect downstream polymer exports.

Europe shows mature demand with a tilt toward specialty grades and climate-aligned processes. Fit for 55 legislation spurs investment in low-carbon acetyls, while competitive pressure from Asian imports suppresses commodity-grade margins. Germany and the United Kingdom remain the largest European consumers, leveraging strong pharmaceutical and food sectors. The Middle East benefits from low-cost feedstocks and rising construction activity, especially under Saudi Arabia’s Vision 2030, whereas South America progresses more modestly with incremental growth in Brazil and Argentina.

Competitive Landscape

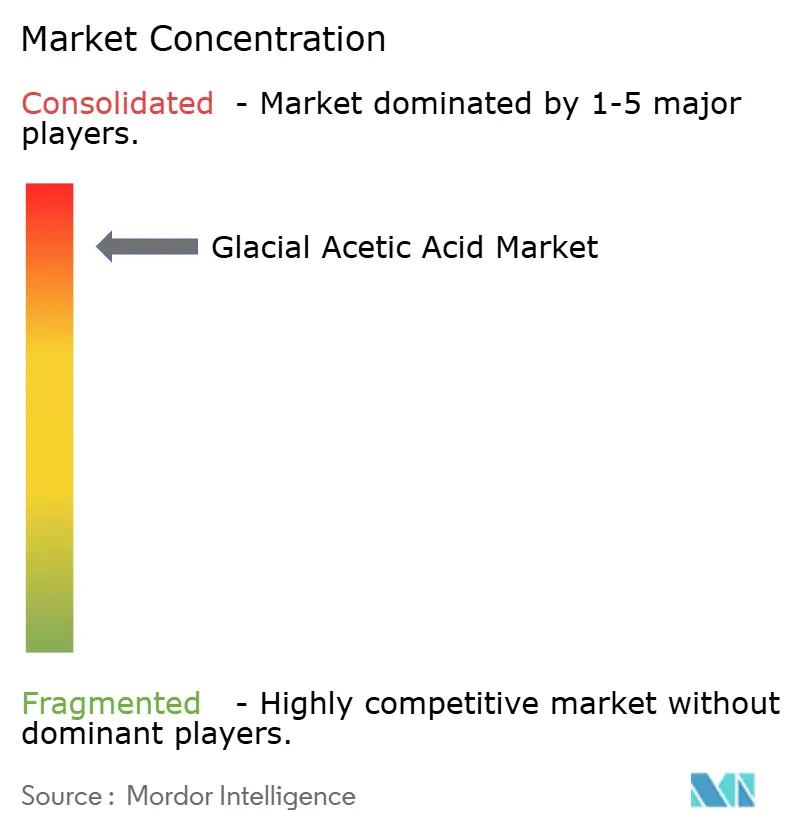

The glacial acetic acid market is consolidated, with the top five producers holding approximately 73% of the market share. Celanese leads through its integrated acetyl-chain assets across three continents, focusing on cost optimization. BP Acetyls and Eastman Chemical follow, leveraging regional and product-specific strengths.

Sustainability is becoming a key factor, with Celanese, Eastman, and BP incorporating captured carbon and renewable energy into acetic acid synthesis. Emerging players utilizing CO₂-to-acetic acid technologies are targeting specialty customers with low-carbon requirements, potentially challenging incumbents.

Oversupply in 2024-2025 is pressuring unintegrated producers, prompting some to consider alliances or divestitures. Meanwhile, integrated multinationals are focusing on ultra-high-purity grades, customized solvent blends, and sustainability-linked metrics to strengthen their competitive edge.

Glacial Acetic Acid Industry Leaders

BP p.l.c.

Celanese Corporation

Eastman Chemical Company

LyondellBasell Industries Holdings B.V.

Jiangsu Sopo (Group) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: INEOS Acetyls has signed a Memorandum of Understanding (MOU) with Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC) to assess the feasibility of establishing a 600 kt acetic acid plant at GNFC's Bharuch facility in Gujarat, India. GNFC is currently the only producer of glacial acetic acid in the country.

- April 2024: Eastman Chemical Company announced an off-list price increase for Eastman Glacial Acetic Acid in North and Latin America.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

The study defines the glacial acetic acid market as the worldwide supply-side value and volume of anhydrous acetic acid with a purity of ninety-nine percent or greater, produced through carbonylation or bio-fermentation routes and sold to downstream users in vinyl acetate monomer, purified terephthalic acid, solvents, food preservation, and pharmaceutical excipients. Measurements are captured at the manufacturer gate, expressed in million tons and converted to nominal US dollars at prevailing average selling prices.

Scope Exclusion: Diluted vinegar, mixed acetyl derivatives traded as finished products, and captive in-house consumption that never reaches merchant trade are left outside the market boundary.

Segmentation Overview

- By Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

- By Application

- Vinyl Acetate Monomer

- Ester Production

- Acetic Anhydride

- Solvent

- Food Additive

- Textile

- Other Applications

- By End-Use Industry

- Chemicals and Petrochemicals

- Food and Beverage

- Pharmaceuticals

- Textiles and Leather

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Rest of the World

- Middle East and Africa

- South America

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Extensive interviews with acetyl chemical producers, procurement managers in coatings and PET resin firms, regional distributors, and safety regulators across Asia-Pacific, North America, and Europe enable analysts to stress-test secondary numbers, gather plant utilization updates, and verify average pricing bands.

Follow-up surveys capture seasonality effects and feedstock sentiment that rarely appear in public data.

Desk Research

Desk research combines tier-one public datasets and proprietary tools. Trade statistics from UN Comtrade, China Customs, and the US International Trade Commission help us map trans-regional flows, while production and capacity disclosures from industry associations such as the European Chemical Industry Council anchor supply baselines. Academic chemistry journals, patent filings accessed through Questel, and commodity price bulletins clarify technology shifts and raw-material cost curves. Paid sources, including D&B Hoovers for company financials and Dow Jones Factiva for press scans, enrich competitor and expansion insights. The sources listed illustrate the breadth of material consulted; many other references were reviewed for validation and context.

Market-Sizing & Forecasting

Sizing the market starts with a top-down reconstruction of global output using reported plant capacities, utilization rates, and cross-border trade balances, which are then reconciled with selective bottom-up checks such as sampled ex-factory prices multiplied by shipment volumes to fine-tune totals. Key variables include methanol feedstock prices, VAM capacity additions, PTA operating rates, solvent demand in architectural coatings, and pharmaceutical excipient regulations; each is projected through multivariate regression, and scenario analysis frames high and low case bands.

Where bottom-up estimates are incomplete, substitution factors and regional analogs bridge data gaps before a final top-down and bottom-up triangulation delivers the baseline.

Data Validation & Update Cycle

Before release, model outputs pass anomaly screens, peer review, and leadership sign-off.

Analysts re-contact key respondents when quarterly price swings or capacity announcements exceed preset thresholds.

Reports refresh annually, and interim flash updates are issued after material events.

Why Mordor's Glacial Acetic Acid Baseline Stands Firm

Published estimates often diverge because firms vary concentration cut-offs, bundle derivatives, or freeze exchange rates at different points in the year.

Gap drivers include Mordor's strict >=99% purity scope, our use of live plant utilization surveys, and an annual refresh cadence, whereas many publishers roll forward older assumptions, blend diluted acetic acid sales, or extrapolate downstream product revenues.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 11.74 million tons (2025) | Mordor Intelligence | |

| USD 10.26 billion (2022) | Global Consultancy A | Includes diluted grades and earlier base year |

| USD 9.5 billion (2024) | Regional Consultancy B | Converts derivative revenues to glacial equivalents, risking double counting |

| USD 8.80 billion (2024) | Industry Journal C | Applies uniform ASPs and omits capacity shutdowns announced mid-year |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent baseline anchored to clearly defined purity thresholds, current utilization evidence, and repeatable update steps, giving decision-makers a dependable footing for strategic planning.

Key Questions Answered in the Report

What is driving the fastest growth segment in the glacial acetic acid market?

Pharmaceutical Grade material is growing at a 6.82% CAGR because of tighter purity demands in API synthesis and injectable drug formulations.

Which application consumes the largest volume of glacial acetic acid?

VAM production uses 34.70% of 2025 volumes, supporting adhesives, paints, and flexible packaging markets.

Why is Asia-Pacific expected to retain its lead?

The region combines 62.60% of 2025 volume with new capacity additions in China and India, and posts a 6.72% CAGR through 2031.

How are producers mitigating methanol price volatility?

Strategies include captive methanol integration, bio-based feedstock adoption, and commodity hedging.

Which new technologies could disrupt the market?

CO₂-to-acetic-acid and cellulosic biomass routes promise lower carbon footprints and reduced reliance on fossil methanol.

What is the outlook for solvent applications?

Solvents are projected to rise at a 6.43% CAGR as acetic-acid-based systems gain favor in adhesives and sealants under stricter VOC rules.

What is the current market size of glacial acetic acid market?

The Glacial Acetic Acid Market size is estimated at 12.38 Million tons in 2026, and is expected to reach 16.12 Million tons by 2031, at a CAGR of 5.43% during the forecast period (2026-2031).

Page last updated on: