Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

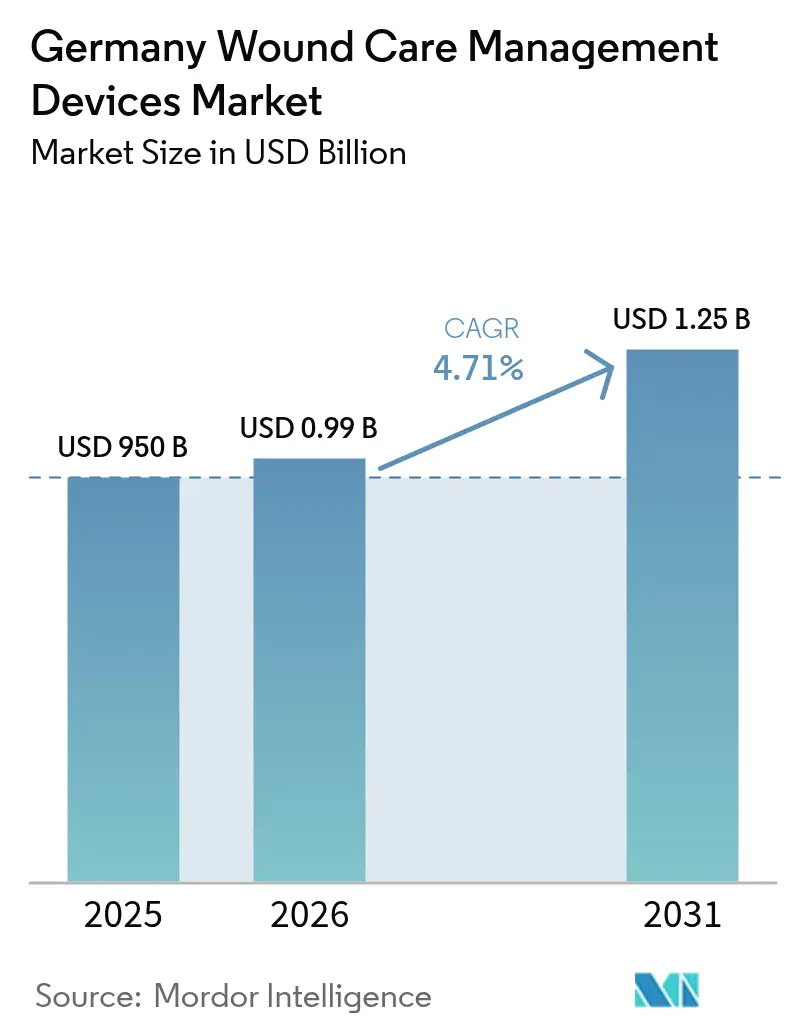

| Base Year Market Size (2025) | USD 950 Billion |

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Wound Care Management Devices Market Analysis by Mordor Intelligence

Germany wound care management devices market size in 2026 is estimated at USD 994.75 million, growing from 2025 value of USD 950 million with 2031 projections showing USD 1.25 billion, growing at 4.71% CAGR over 2026-2031. Demand is propelled by an ageing population, the high clinical burden of diabetes, and a reimbursement framework that rewards clinically validated innovation. Hospitals are still the prime buyers of advanced dressings and negative-pressure systems, yet digital therapeutics and extended-wear products have begun to shift care toward homes and community settings. The EU Medical Device Regulation (MDR) [1]European Commission, "Regulation (EU) 2017/745 - application of MDR requirements to ‘legacy devices’ and to devices placed on the market prior to 26 May 2021 in accordance with Directives 90/385/EEC or 93/42/EEC," health.ec.europa.eu now shapes competitive strategy by favouring companies that already possess extensive quality-management infrastructure. Meanwhile, the Digital Healthcare Act allows physicians to prescribe reimbursable digital health applications (DiGAs), a policy that is gradually pulling sensor-enabled bandages and tele-monitoring platforms into routine practice. Taken together, these forces signal that the Germany wound care management devices market will keep expanding even as institutional budgets tighten and skilled nursing capacity shrinks.

Key Report Takeaways

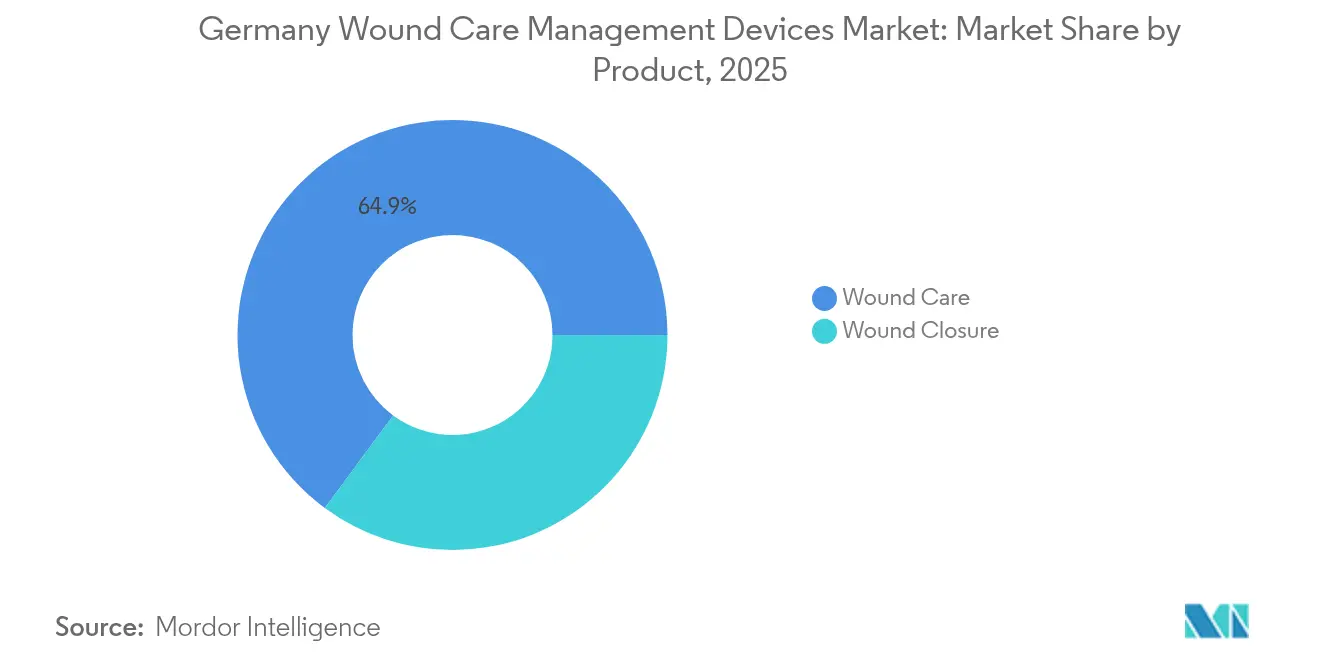

- By product type, wound care dressings captured 64.88% of Germany wound care management devices market share in 2025, while wound closure products are advancing at a 5.12% CAGR through 2031.

- By wound type, chronic wounds accounted for 59.95% of cases in 2025; acute wounds are set to grow at a 5.37% CAGR to 2031.

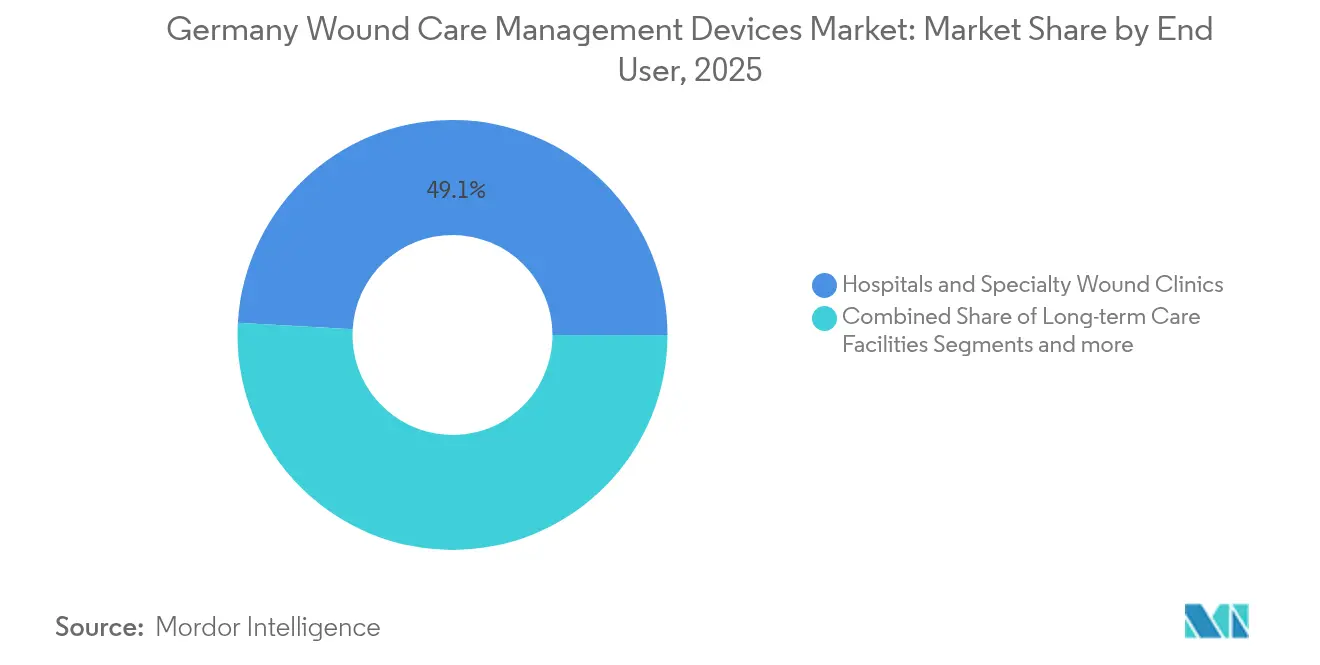

- By end user, hospitals and specialty wound clinics held 49.10% revenue share in 2025, whereas the home-healthcare segment is forecast to expand at a 5.62% CAGR.

- By mode of purchase, the institutional channel commanded 67.85% of Germany wound care management devices market size in 2025; retail/OTC purchases are rising at a 5.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic wounds & geriatric population | +1.2% | Nationwide, rural concentration | Long term (≥ 4 years) |

| Diabetes prevalence fuelling diabetic foot ulcers | +0.9% | Nationwide, higher in eastern states | Medium term (2-4 years) |

| Continuous product innovation (silicone super-absorbers, NPWTi-d) | +1.1% | Nationwide, urban centres first | Short term (≤ 2 years) |

| Hospital-digitalisation grants | +0.8% | Nationwide, federal variations | Medium term (2-4 years) |

| Reimbursed wound-care apps & tele-monitoring | +0.6% | Metro areas lead | Short term (≤ 2 years) |

| Strong cost-effectiveness evidence for NPWT | +0.7% | Institutional focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising chronic wounds & geriatric population

Germany already counts 17.3 million citizens aged 65 years or older, and the proportion living with severe disability continues to climb. Prevalence surveys place chronic wounds among nursing-home residents at 7.8%, with pressure ulcers representing half of these lesions. As hospital consolidation reduces inpatient beds, more care shifts toward the community, elevating the need for dressings that simplify self-application without compromising clinical outcomes. Patients with diabetes show a higher chronic-wound prevalence than non-diabetics, which pushes demand for premium multilayer dressings and sensor-equipped negative-pressure systems able to sustain therapy between less frequent nursing visits.

Diabetes prevalence fuelling diabetic-foot ulcers

Roughly 7.2% of German adults carry a formal diabetes diagnosis, and surveillance studies estimate that another 2% remain undiagnosed. Clinical registries record 250,000 new diabetic-foot ulcers each year and 13,000 major amputations despite multidisciplinary care pathways [2]Robert Koch Institute, "Epidemiology and Health Monitoring," rki.de. Evidence that specialised centres can cut amputation risk by 80% has accelerated procurement of advanced monitoring technologies and antimicrobial dressings capable of detecting sub-clinical infection markers.

Continuous product innovation including silicone super-absorbers and NPWTi-d

Manufacturers are embedding super-absorbent polymers within silicone borders to balance exudate control with atraumatic removal. In parallel, negative-pressure wound therapy with instillation and dwell (NPWTi-d) shortens dressing changes and lowers bacterial burden. Academic teams have unveiled smart bandages that track nitric-oxide and hydrogen-peroxide levels, signalling infection days before visual cues emerge. These advances resonate strongly with Germany’s reimbursement ethos, which rewards technologies that prevent costly complications.

Hospital-digitalisation grants accelerating advanced wound-tech uptake

Federal stimulus programmes provide hospitals with capital for electronic documentation and connected devices. As facilities modernise, procurement committees favour wound systems that integrate seamlessly with electronic health records, streamlining outcome reporting for payers. However, physician familiarity remains a barrier: only 12% of doctors have ever prescribed a DiGA, and self-assessed knowledge still averages below mid-scale levels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device costs & reimbursement gaps | -0.7% | Nationwide, acute in rural areas | Medium term (2-4 years) |

| Stringent EU-MDR post-market compliance burden | -0.5% | Nationwide | Long term (≥ 4 years) |

| Fragmented outpatient-financing limits home-care uptake | -0.4% | Nationwide, underserved regions | Medium term (2-4 years) |

| Shortage of specialised wound-care nurses | -0.6% | Nationwide, rural deficit | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of specialised wound-care nurses

Federal projections show a possible deficit of 690,000 nurses by 2049 [3]Destatis, "Nursing workforce forecast," destasis.de Fewer professionals mean less frequent dressing changes and greater reliance on products that maintain efficacy for a week or more without specialist intervention.

Stringent EU-MDR post-market compliance burden

The MDR requires manufacturers to run continuous post-market surveillance and maintain unique device identification systems. Smaller German companies face multi-year investment cycles to meet these demands, and some have withdrawn legacy lines rather than re-certify. Resulting product scarcity could curb price competition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Solutions Drive Market Evolution

Wound-care products generated 64.88% of Germany wound care management devices market revenue in 2025, reflecting a preference for multifunctional foams, hydrofibers, and silicone super-absorbers that address exudate control and skin integrity simultaneously. Negative-pressure systems, now equipped with automated pressure monitors, are gaining institutional traction as payers accept their cost-saving profile for complex surgical wounds. Smart hydrogels infused with antibiofilm peptides are moving from research labs toward commercial pipelines, promising additional gains in healing speed. Traditional gauze still serves primary-care settings but faces encroachment from low-cost composite dressings. Disposable NPWT kits target outpatient settings where pump rental logistics once constrained adoption. Together, these innovations ensure that the Germany wound care management devices market maintains a technology-led growth curve.

Wound-closure devices exhibit the fastest CAGR at 5.12% through 2031 as hospitals resume deferred surgeries and adopt bioresorbable staples and tissue adhesives. Bioengineered skin substitutes increasingly bridge extensive tissue defects, shortening hospital stays and enabling earlier discharge to home-care programmes. Smart bandages capable of real-time biomarker sensing, such as the iCares prototype, foreshadow an era in which closure products double as diagnostic platforms. These trends align closely with statutory insurance goals of complication prevention, indicating sustained procurement momentum despite overall budgetary constraints in the Germany wound care management devices industry.

By Wound Type: Chronic Conditions Shape Market Dynamics

Chronic lesions commanded 59.95% of Germany wound care management devices market size in 2025. Diabetic-foot ulcers alone account for 250,000 new cases every year, spurring hospital investment in multidisciplinary limb-saving teams. Pressure-ulcer prevalence remains highest in long-term-care institutions, reinforcing demand for dressings that can distribute shear forces while absorbing high exudate volumes. Venous leg ulcers also drive utilisation of compression-compatible materials with antimicrobial silver or polyhexanide. Clinical guidelines now recommend point-of-care fluorescence imaging to detect bacterial load, creating a pull-through effect for compatible dressings.

Acute wounds are expanding at a 5.37% CAGR, buoyed by rising orthopaedic and oncologic surgery volumes as pandemic backlogs clear. Extended-wear NPWT dressings now remain in situ for seven days, limiting theatre-to-ward hand-offs and freeing nursing resources. Skin-grafting adjuncts containing growth-factor matrices shorten recovery after burns and trauma, and absorbable sutures coated with antimicrobials lessen the risk of surgical-site infections. These developments collectively raise the performance expectations for all acute-care devices sold into the Germany wound care management devices market.

By End User: Home Healthcare Transforms Delivery Models

Hospitals and specialty clinics retained 49.10% of Germany wound care management devices market share in 2025. Large academic centres spearhead adoption of high-end imaging tools and robotic debridement platforms, while regional clinics focus on protocol standardisation to meet tightened length-of-stay targets. Institutional buyers increasingly evaluate total cost of ownership rather than headline price, awarding contracts to suppliers that bundle training and digital documentation modules.

Home-healthcare settings deliver the fastest growth at a 5.62% CAGR. Fifty-six DiGAs are reimbursable, yet only a fraction of physicians routinely issue prescriptions, highlighting education gaps. Pilot projects using intelligent plasters demonstrated reductions in nurse travel time and emergency admissions, but reimbursement codes still lag behind product capabilities. As the nursing shortage deepens, solutions that allow relatives or non-clinical carers to perform routine changes will capture a growing share of the Germany wound care management devices market.

By Mode of Purchase: Digital Channels Reshape Procurement

Institutional procurement represented 67.85% of Germany wound care management devices market size in 2025. Tendering cycles now attach greater weight to MDR compliance history and real-world-evidence dossiers, favouring incumbents with mature surveillance systems. Some university hospitals have already inserted “digital-connectivity” clauses into tender documents, effectively screening out legacy pumps lacking remote-monitoring functions.

Retail and OTC sales are rising at a 5.55% CAGR. Community pharmacies stock silicone-bordered foams and simplified NPWT kits, while e-commerce portals let patients reorder supplies in quantities tailored to their dressing-change schedules. Tele-consultations guide product selection, ensuring adherence to guideline-based care plans and reinforcing patient confidence. These dynamics add incremental revenue streams and extend brand reach for manufacturers in the Germany wound care management devices industry.

Geography Analysis

Germany’s federal insurance system provides a unified reimbursement baseline, yet state-level execution produces regional adoption gaps. Urban centres such as Berlin, Hamburg and Munich benefit from concentrated specialist clinics and digital-innovation grants, creating clusters where advanced NPWT adoption exceeds the national mean. Eastern states, including Saxony-Anhalt and Brandenburg, report higher diabetes prevalence, pushing local demand for diabetic-foot management solutions and driving device utilisation above per-capita averages. Rural areas face longer travel distances and fewer wound-care nurses, accentuating the appeal of long-wear dressings and tele-monitoring patches that can bridge gaps in professional coverage.

Hospital-consolidation plans project a reduction from 1,900 to 1,250 facilities by 2033, disproportionately affecting low-volume rural hospitals. As a result, outpatient clinics and home-care providers in those districts expect rising caseloads, stimulating demand for easy-to-use dressings that maintain integrity over multiple days. States such as North Rhine-Westphalia have earmarked digital health subsidies to assist smaller providers in adopting connected wound platforms, creating a multiplier effect for companies whose products integrate with standard telehealth dashboards.

Cross-border influences add another layer: Germany’s central location and MDR alignment make it a preferred launch pad for multinational manufacturers. Domestic players like HARTMANN export established dressings across the EU, yet also face intensified competition from global firms introducing sensor-based platforms. The DiGA framework positions Germany as an early-adopter market for digital wound care, encouraging foreign start-ups to partner with German clinics to secure pivotal real-world data. However, physician uptake remains modest, indicating that sustained educational outreach will be critical to unlock the full regional potential of the Germany wound care management devices market.

Competitive Landscape

The Germany wound care management devices market features moderately fragemented concentration. HARTMANN leverages domestic manufacturing and an extensive sales force to maintain leadership in traditional and silicone-lined dressings. Smith+Nephew’s technology-focused portfolio, highlighted by its RENASYS EDGE negative-pressure platform, posted 12.2% underlying growth in its Advanced Wound Management division during 2024. Coloplast expands via direct-to-consumer channels and consistently ranks high in patient-satisfaction scores for post-surgical dressings.

Strategic moves increasingly revolve around digital augmentation. Healiva’s acquisition of Smith+Nephew’s cell-therapy assets signals renewed interest in biologics capable of accelerating healing in chronic indications. Convatec plans a 2025 market debut for its nitric-oxide releasing ConvaNiox dressing, aiming to address resistant biofilms while conforming to EU antimicrobial-resistance targets. Manufacturers also court payer acceptance by funding economic-outcome studies that quantify reductions in home-visit frequency or hospital readmissions.

Regulatory readiness under MDR emerged as a key differentiator in 2025. Firms with mature quality-management systems completed re-certifications early, avoiding supply disruptions. Smaller entities, however, struggled with notified-body backlog, leading some distributors to rationalise catalogues and prioritise high-volume SKUs. Digital-health alignment offers a route to competitiveness for newcomers capable of embedding Bluetooth sensors or cloud-based dashboards into otherwise mature dressing categories.

Germany Wound Care Management Devices Industry Leaders

-

Smith & Nephew

-

Coloplast Group

-

Medtronic

-

Solventum

-

ConvaTec Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Convatec confirms an initial German launch of ConvaNiox, a nitric-oxide antimicrobial dressing focused on diabetic-foot ulcers.

- March 2025: Mérieux Equity Partners acquires a majority stake in German manufacturer Curea Medical to expand its advanced-dressing footprint.

- January 2025: The Bundestag extends reimbursement for hydrogels and silver-containing dressings under the Healthcare Strengthening Act, maintaining statutory-insurance coverage without extra clinical-benefit review.

- November 2024: Allmed Medical exhibits a full wound-care portfolio at the MEDICA trade fair in Düsseldorf.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany wound care management devices market as all single-use or reusable mechanical, electrical, and biologic devices that cleanse, debride, close, or monitor acute and chronic wounds in clinical or home settings, reported in USD value at manufacturer selling price.

Scope exclusion: consumable dressings, gels, and topical agents are modeled separately and are not counted within the device pool.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed German wound-care nurses, procurement managers in university hospitals across Bavaria and NRW, and distributors serving home-health agencies. These conversations validated out-patient penetration of portable NPWT, pressure-relief system life cycles, and real-world pricing spreads, filling gaps left by publicly available statistics.

Desk Research

We began with national datasets such as Destatis hospital discharge files, Digital-Health-Atlas reimbursement schedules, and German Diabetes Federation prevalence updates, which outline the treated population. Trade association briefs from BVMed and MedTech Europe helped us gauge installed bases for NPWT and hyperbaric chambers. Company 10-Ks, CE-mark certificates, and procurement tenders that flow through Volza and D&B Hoovers supplied shipment values and average device price corridors. Academic meta-analyses published in Deutsches Ärzteblatt offered utilization rates across wound types, while Dow Jones Factiva tracked product launches that shift replacement cycles. The sources listed are illustrative; many others supported data checks and clarifications.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build reconstructed demand volumes by matching chronic and acute wound incidence with treatment practices. Results were cross-checked with a sampled bottom-up roll-up of supplier revenues and channel checks to fine-tune total device value. Key variables include: diabetic foot ulcer prevalence, median length of stay for surgical wounds, NPWT price erosion trend, device replacement intervals, and hospital capital-budget growth. Forecasts to 2030 apply multivariate regression coupled with scenario analysis, tying unit uptake to diabetes growth, geriatric share, and reimbursement revisions. Where distributor mark-ups varied, midpoint estimates were imputed using sensitivity bands reviewed with interviewees.

Data Validation & Update Cycle

Outputs pass three-layer review: automated variance scans against historic ratios, senior-analyst peer review, and research-manager sign-off. We refresh every twelve months, with mid-cycle revisions when reimbursement codes, major recalls, or M&A events materially shift the baseline.

Why Mordor's Germany Wound Care Management Baseline Earns Trust

Published numbers differ because firms pick distinct product baskets, price assumptions, and refresh rhythms.

Device counts widen further when some studies add consumables or bundle Austria and Switzerland data under 'DACH' before currency conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.95 B (2025) | Mordor Intelligence | - |

| USD 1.26 B (2023) | Global Consultancy A | Older base year and includes dressings plus closure consumables |

| USD 1.03 B (2024) | Industry Databook B | Combines home-use OTC kits and applies list prices without discount normalization |

The comparison shows estimates swing by up to USD 0.31 B.

Our device-only scope, current-year refresh, and validated price corridors deliver a balanced, transparent baseline that executives can trace back to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current value of the Germany wound care management devices market?

The market stands at USD 994.75 million in 2026 and is forecast to reach USD 1.25 billion by 2031.

Which product category holds the largest revenue share?

Advanced wound-care products lead with 64.88% of Germany wound care management devices market share in 2025.

Why are home-healthcare settings growing faster than hospitals?

A looming nursing shortage and supportive reimbursement for digital health tools are shifting routine wound management toward the home, driving a 5.62% CAGR in that segment.

How does EU-MDR influence competitive dynamics?

Stricter post-market surveillance and re-certification requirements favour companies with robust quality-management systems, creating barriers for smaller manufacturers.

What digital health policies affect wound-care adoption?

Germany’s Digital Healthcare Act allows physicians to prescribe reimbursable DiGAs, enabling remote monitoring systems and sensor-equipped dressings to gain traction.

Page last updated on: